2026-04-10

Home

Japanese

Omega Investment Co., Ltd.

Itoki (Company note – Basic)

| Share price (8/27) | ¥2,356 | Dividend Yield (25/12 CE) | 2.7 % |

| 52weeks high/low | ¥1,336/2,538 | ROE(24/12 act) | 13.8 % |

| Avg Vol (3 month) | 218.8 thou shrs | Operating margin (24/12 act) | 7.3 % |

| Market Cap | ¥125.7 bn | Beta (5Y Monthly) | 0.36 |

| Enterprise Value | ¥133.5 bn | Shares Outstanding | 53.382 mn shrs |

| PER (25/12 CE) | 14.0 X | Listed market | TSE Prime |

| PBR (24/12 act) | 2.2 X |

| Click here for the PDF version of this page |

| PDF version |

An Office DX company that designs tomorrow’s ‘work’

Transforming with the tailwind of customers’ human capital investment

Summary

◇Itoki Corporation (hereafter, the Company) is a leading office furniture manufacturer founded in Osaka in 1890. It is characterized by its high design quality and its integrated manufacturing and sales system. The Company’s mission is “We Design Tomorrow. We Design WORK-Style.” Beyond merely manufacturing and selling furniture, it advocates Office 3.0, the DX of offices, and promotes a fully integrated strategy that ranges from space design to the provision of services supporting productivity improvement. It is also steadily strengthening its earnings base in logistics and research facilities.

◇Leadership of President Koji Minato and improvement in performance and corporate value: Under President and Representative Director Koji Minato, who has led the Company since March 2022, profitability has improved significantly. Expectations are high in the stock market for his continued leadership.

◇Business overview: the Company’s main businesses are the Workplace Business and the Equipment & Public Works-Related Business.

◇Workplace Business: Provides services such as manufacturing and selling office furniture, office repairs, assembly and construction, office space design, and project management for office relocation. It is enhancing proposals and consulting services that contribute to improving office productivity, thereby increasing added value, and going forward will promote Office 3.0, which uses data to support office operations. In FY12/2024, net sales were 102.2 billion yen, operating profit was 8.0 billion yen, and the operating profit margin was 7.9%.

◇Equipment & Public Works-Related Business: Provides logistics solutions such as warehousing and automated logistics system equipment, equipment for research facilities, and environmental and space construction for public facilities. It boasts the No.1 track record in deliveries of shuttle-type automated warehouses. In FY12/2024, net sales were 34.5 billion yen, operating profit was 1.8 billion yen, and the operating profit margin was 5.4%.

◇New Medium-term Management Plan “RISE TO GROWTH 2026”: The new medium-term management plan announced in February 2024 positions the period from 2024 to 2026 as a “high-profitability phase” to enhance sustainable growth potential. Specifically, it consists of the key strategy “7 Flags” and ESG strategies based on the concept of “Tech x Design based on PEOPLE.” The financial targets for FY12/2026 are net sales of 150 billion yen, operating profit of 14 billion yen, an operating profit margin of 9%, and ROE of 15% (> assumed cost of capital of 9–10%). The Company is also working to reduce the cost of capital, fully meeting today’s stock market demands by maximizing shareholder value and increasing PBR.

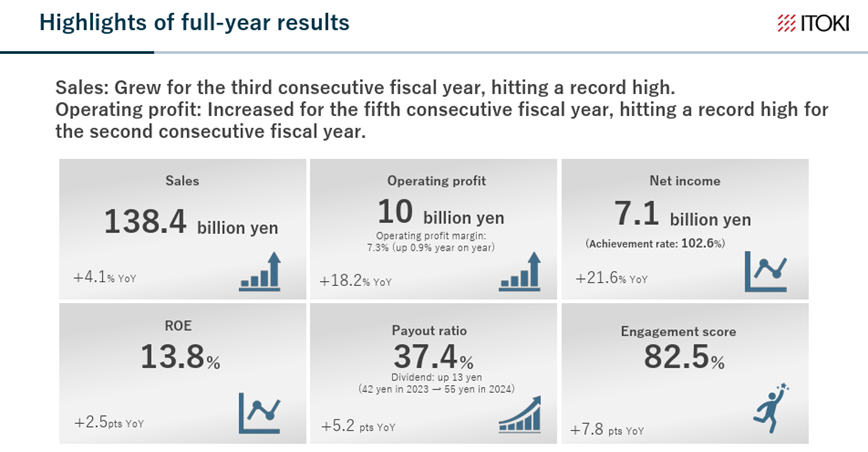

◇Performance trends reflecting the results of reforms: Business performance has been progressing steadily. Net sales for FY12/2024 were 138.4 billion yen (+4% YoY), marking the third consecutive year of revenue growth and a record high. Operating profit was 10.0 billion yen (+18% YoY), the fifth consecutive year of profit growth and the second consecutive year of record-high earnings. ROE also improved to 13.8%. The Company’s forecast for FY12/2025 is net sales of 150 billion yen and operating profit of 12 billion yen, indicating steady progress toward the targets of the medium-term management plan.

◇Share price trends and highlights: The Company’s share price rose from 347 yen at the end of March 2022, when President Minato took office, to 2,356 yen as of August 2025, with PBR increasing from below 1x to around 2.2x. This was driven by steadily capturing the growing investment appetite of customers for offices and other facilities with a focus on profitability, resulting in continued business expansion in line with the medium-term management plan. Going forward, new factors are expected to further emerge, including expansion into the Office 3.0 domain, thorough emphasis on profitability on a consolidated basis, the materialization of new revenue opportunities outside of domestic offices, and improved employee engagement and productivity.

Table of contents

| Summary | 1 |

| Key financial data | 2 |

| Company profile | 3 |

| History | 4 |

| Group overview / Production structure / Business diagram | 7 |

| Business overview | 9 |

| Workplace business | 9 |

| Equipment / Public business | 16 |

| Growth strategy | 18 |

| New medium-term management plan RISE TO GROWTH 2026 | 18 |

| Financial results | 21 |

| Full-year results for FY12/2024 | 21 |

| FY12/2025 full-year forecast | 22 |

| Stock information, etc. | 24 |

| Share Price Trend | 24 |

| Share price observation | 25 |

| Major shareholders, Shareholding by ownership, Shareholder return policy | 26 |

| Corporate governance and the top management | 27 |

| Sustainability | 30 |

| Financial data | 31 |

Key financial data

| Unit: million yen | 2020/12 | 2021/12 | 2022/12 | 2023/12 | 2024/12 | 2025/12 CE |

| Sales | 116,210 | 115,905 | 123,324 | 132,985 | 138,460 | 150,000 |

| EBIT (Operating Income) | 1,585 | 2,561 | 4,582 | 8,524 | 10,078 | 12,000 |

| Pretax Income | 1,277 | 1,523 | 8,372 | 8,378 | 10,071 | |

| Net Profit Attributable to Owner of Parent | -235 | 1,166 | 5,294 | 5,905 | 7,183 | 8,300 |

| Cash & Short-Term Investments | 18,246 | 17,451 | 26,976 | 24,795 | 22,482 | |

| Total assets | 105,096 | 103,898 | 115,288 | 117,437 | 120,521 | |

| Total Debt | 21,742 | 20,091 | 19,487 | 17,308 | 37,533 | |

| Net Debt | 3,496 | 2,640 | -7,489 | -7,487 | 15,051 | |

| Total liabilities | 60,901 | 58,818 | 65,374 | 62,434 | 71,174 | |

| Total Shareholders’ Equity | 43,812 | 44,931 | 49,871 | 54,960 | 49,260 | |

| Net Operating Cash Flow | 4,561 | 2,774 | 5,804 | 6,321 | -1,000 | |

| Capital Expenditure | 1,729 | 2,110 | 4,145 | 3,316 | 6,036 | |

| Net Investing Cash Flow | -1,152 | -1,170 | 4,923 | -4,012 | -7,107 | |

| Net Financing Cash Flow | -2,267 | -2,658 | -1,426 | -4,148 | 5,905 | |

| Free Cash Flow | 2,832 | 664 | 1,659 | 3,005 | -4,146 | |

| ROA (%) | -0.22 | 1.12 | 4.83 | 5.08 | 6.04 | |

| ROE (%) | -0.53 | 2.63 | 11.17 | 11.27 | 13.79 | |

| EPS (Yen) | -5.2 | 25.8 | 117.0 | 130.3 | 147.0 | 168.2 |

| BPS (Yen) | 970.4 | 993.9 | 1,101.3 | 1,212.0 | 1,001.1 | |

| Dividend per Share (Yen) | 13.00 | 15.00 | 37.00 | 42.00 | 55.00 | 65.00 |

| Shares Outstanding (Million shares) | 45.66 | 45.66 | 45.66 | 45.66 | 53.38 |

Source: Omega Investment from company materials

Company profile

Itoki is one of the four largest manufacturers of office furniture in Japan. It is a long-established company with a history of more than 130 years since its foundation in 1890.

With a mission statement of “We Design Tomorrow. We Design WORK-Style”, the Company not only manufactures and sells office furniture but also provides consulting on working styles and space design, offering the value of creating spaces, environments, and places for workers. The Company has long been committed to designing, and its products are renowned for design excellence.

The two business segments are.

Workplace business: mainly manufactures and sells office furniture, but as stated in its mission statement, the Company advocates the creation of ‘working environments’ tailored to how customers work. In recent years, the Company has actively responded to the needs of a growing number of ways of working, such as working from home and in dispersed locations, in addition to working “collectively” in an office. Moreover, the Company provides consulting services and other total solutions.

Main products and services; office furniture (desks and workstations, tables, office and conference chairs, system storage furniture, lockers), manufacture and sale of construction materials for office space construction, interior decoration work, office space design, project management for office relocation, etc., office repair and maintenance services, telework furniture, study furniture.

Equipment / Public business: provides logistics-related facilities, which have proliferated in recent years, as well as research facility equipment for pharmaceutical companies, universities and research institutions, and equipment for public facilities.

Main products and services; logistics equipment (shuttle cart automatic storage systems (SAS)), storage shelves, special doors, office security systems, research facility equipment, powder machinery and equipment, environmental and space construction for public facilities, etc.

The composition of sales by region is as follows: Japan, 125,945 million yen (91%); Asia, 11,869 million yen (9%); with domestic sales accounting for over 90%.

Sales by Segment

Source: Company materials

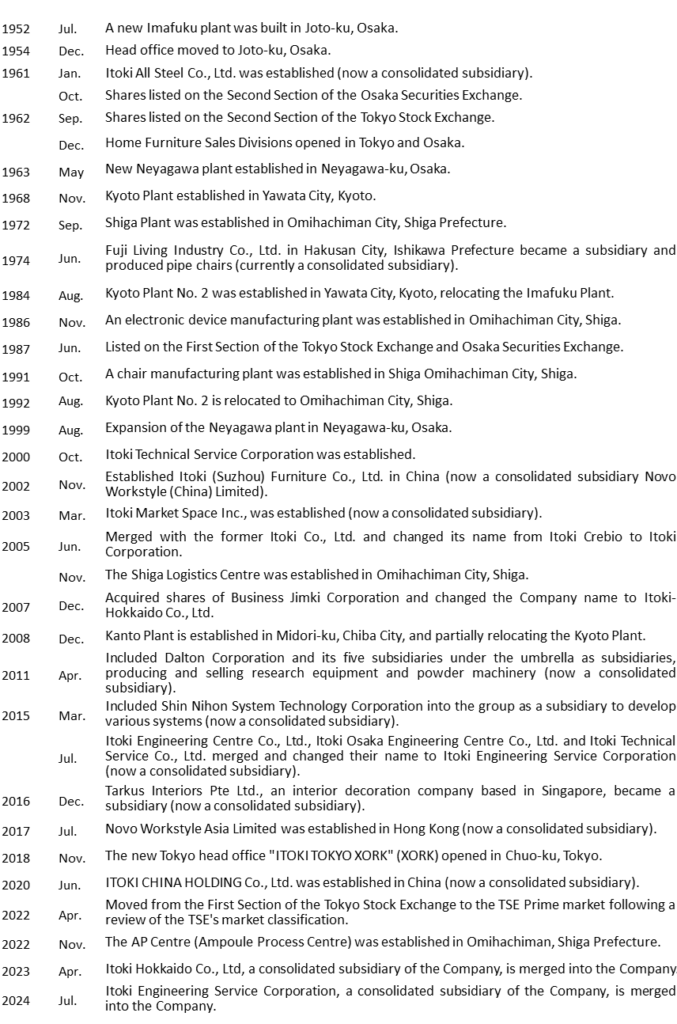

History (See the history table on the following page)

1890-1949: from popularising inventions and patents to selling and manufacturing office equipment.

The Company’s origins date back to December 1890, when founder Kiichiro Itoh founded Itoh Ki Shoten in Osaka’s Koraibashi district to promote his inventions and patents and to handle imports. In 1903, the Company began importing and selling paper clips and staples. Both are commonly used in offices today but trace their origins back more than 100 years when the Company started to sell them. Later, in 1908, the Itoki Shoten Engineering Department was established. It started producing office equipment such as hand-carry safes and simple stationery. In the sense that the Company began its business by importing, selling and repairing foreign products after the opening of Japan to the outside world in the Meiji era, and later took on the challenge of domestic production and expanded its business, it has something in common with other Japanese manufacturing companies that are now world leaders, such as Seiko Group Corporation (Hattori Watch Shop) and Brother Industries (Yasui Sewing Machine Shop).

In 1910, the Company began importing and selling English typewriters, thermal bottles, etc. In 1913, it launched the independently developed ‘Zeni-ai-ki’ (money recording and disbursing machine). In 1925, it began manufacturing its steel-made furniture, including lockers. In 1937, it expanded into Tokyo, opening a Tokyo branch in Gofukubashi, Chuo-ku.

1950-1969: Steel furniture creates modern offices. Highly regarded in terms of design.

After the war, demand for office furniture surged as Japan’s economy grew rapidly; in 1955, the Company began manufacturing and selling steel desks. The Company’s steel furniture subsequently paved the way for various types of desks. In 1960 it established three major systems for filing, slip accounting and office layout. In response to the demand for office rationalisation during the period of high economic growth, the Company offered filing and slip accounting systems, as well as ‘office layout’, a functional arrangement of furniture, office equipment and supplies centred on desks, thereby establishing the Itoki brand in office systematisation.

Furthermore, in 1962, the Company expanded into the field of home and student desks. In 1967, the Company adopted the catchphrase ‘Good Design, Good System’, establishing its image as a design company.

Meanwhile, as its business expanded, the Company listed its shares on the Second Section of the Osaka Securities Exchange in October 1961 and on the Second Section of the Tokyo Stock Exchange in September 1962.

1970-1989: office planning, promoting the New Office.

In the 1970s, the Company began technical cooperation with overseas companies and introduced state-of-the-art office systems to Japan. Beyond the mere supply of office furniture, the Company had come to offer ‘office planning’. In 1976, 14 of its products were selected for the G-Mark, and the Company’s reputation for design continued to grow. Since then, many products have been awarded the G Mark every year. In 1977, the Company launched a research equipment and furniture system in cooperation with the Swiss company Vivo. With this, the Company entered the current Equipment / Public business field.

In 1984, local subsidiaries were established in Singapore and the USA. The Company also developed its business with an eye on overseas markets. In 1985, the Company adopted its CI, which is still used today. In 1987, the Company was listed on the First Section of the Tokyo Stock Exchange and the Osaka Securities Exchange.

1990 to present: over 100 years in business and creating offices for the 21st century.

Even after 100 years in business, the Company continues to provide products and services that meet the demands of the times. In 1994, the Company began selling free-access floors to meet the needs of the times. It also focuses on quality control, and in 1998 it was registered for ISO 9001 certification. In 2001, the Company completed the accreditation of all its offices.

In 2005, the manufacturing division Itoki Crebio and the sales division Itoki merged and changed the Company name to Itoki Corporation. The integration of manufacturing and sales enabled quicker management decisions and rationalisation of the group in the face of accelerating global trends.

Since then, the Company has developed and marketed various new products in response to the demands of the times. The Company offers ergonomically designed office chairs and office furniture; in 2017, the FLIP FLAP (chair) won the international design award Red Dot Design Award.

In 2018, offices in the metropolitan area were consolidated in Nihonbashi, and ITOKI TOKYO XORK was established. It advocates a comprehensive work style strategy that maximizes workers’ abilities and intends to conduct various demonstrations as a place to practize the next generation of work styles, and to disseminate the various knowledge and know-how generated from these experiments to society.

Itoki Shoten was founded in December 1890 in Higashi-ku, Osaka.

In 1908 the Itoki Shoten Craft Department was established, and office equipment production began.

In April 1950, the Company was spun off from Itoki Shoten and established Itoki Kosakusho Co. in Izumio, Taisho-ku, Osaka.

The main changes since then have been as follows.

Source: company’s annual securities report

Management leadership in the spotlight

One recent development of note is the current management team.

The current President and CEO, Koji Minato, joined the Company in September 2021 and assumed his current position in March 2022. He joined NTT in 1994 and holds an MBA from USC. He has since served as general manager of Sun Microsystems and (after Oracle acquired Sun Microsystems) vice-president of Oracle Japan, an unusual background for a top corporate executive.

He is expected to appropriately guide the Company in light of technological trends, such as the shift to IoT in the office, and to utilise his management experience in foreign-owned companies to activate internal human resources and improve financial performance.

Since his appointment as President, his performance has fully met these expectations in terms of financial results, qualitative aspects, and share price. In other words, since he took office, business performance has steadily expanded, employee engagement has improved, and the share price has risen from 347 yen at the end of March 2022 to 2,538 yen at the end of August 2025. Expectations are high for his leadership to be further demonstrated going forward.

President Minato’s approach

Source: Omega Investment from company materials

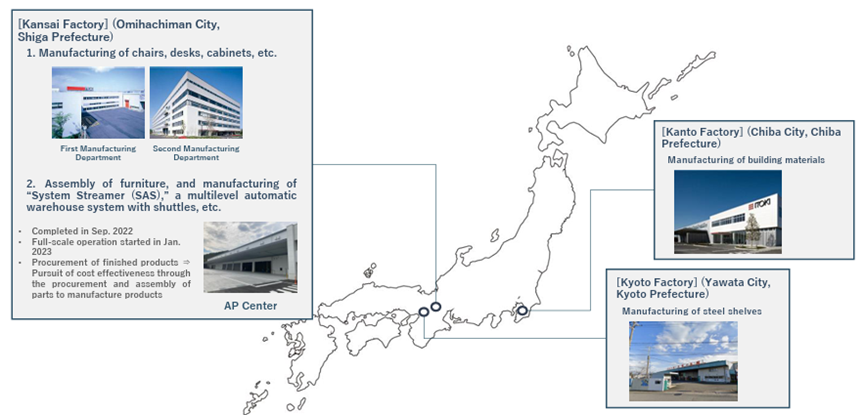

Production structure

Source: Company materials

Group overview

As seen in the history, the Company was founded in Osaka, but its current head office is in Chuo-ku, Tokyo (relocated in 2018). The Company group comprises 32 consolidated subsidiaries, seven non-consolidated subsidiaries, and one affiliated company (see next section). Since the 2000s, the Company has been actively expanding overseas, particularly in ASEAN and China, acquiring local companies and establishing subsidiaries and affiliates in each region.

Production structure

The Company’s production system is based at its domestic plants. This is because the Company’s primary market is the domestic market, and office furniture is bulky in volume due to its storage characteristics, so it is not cost-effective to produce it overseas and import it at high transport costs.

The current main plant is the Shiga Plant, which manufactures chairs, desks, cabinets, and other products for the Workplace business. It employs about 300 people. In September 2022, the Assembling Process Centre (AP Centre) was opened at the same site, which started full operation in January 2023. The AP Centre is working to reduce the cost ratios by centrally managing the Company’s products’ storage, assembly, and shipping. The centre will also relocate the production line for the system streamer SAS-R, whose demand is increasing rapidly in the logistics market, to meet growing demand. The Neyagawa plant, one of the Company’s main plants for many years, was closed in 2022, with its production consolidated at the Shiga plant. The Company sold the idle land of the plant for 6.5 billion yen and is working on improving asset efficiency.

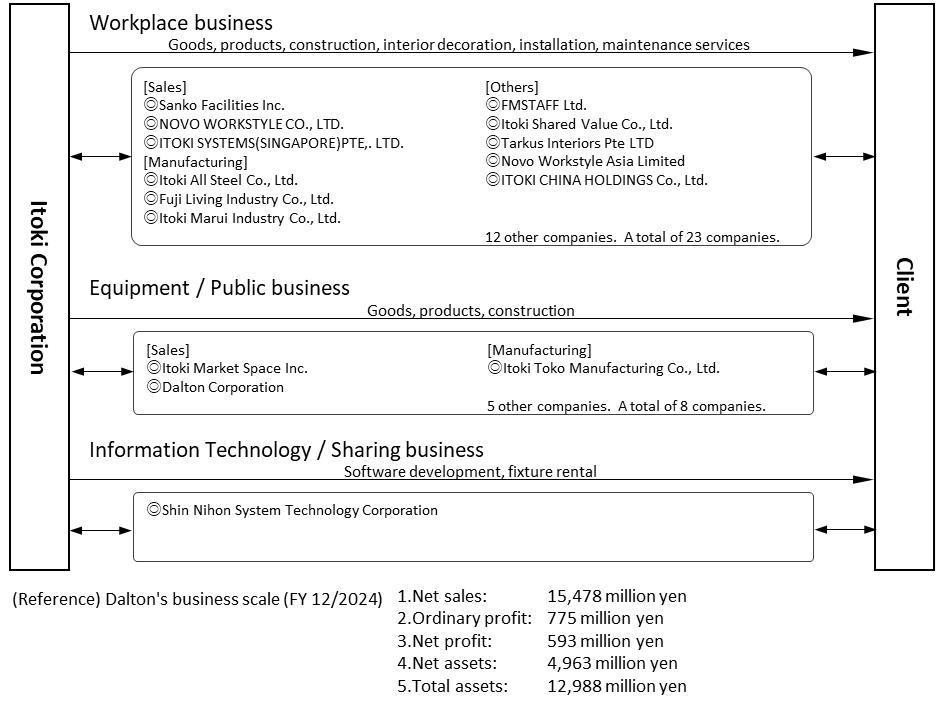

Business diagram

See the next page for a diagram of the business structure. The Company and its group companies are involved in manufacturing, sales, construction, interior decoration, installation, and maintenance services.

Overseas office furniture manufacturers often specialize only in manufacturing and sales and rarely provide interior design, construction, or workplace design. In Japan, consulting companies and office design firms are generally engaged between the office furniture provider and the client for large-scale projects to provide work style design and workplace design. However, in recent years, office furniture manufacturers have also started to offer a comprehensive service from upstream to construction and delivery of office furniture, starting with small and medium-sized projects, to obtain fees commensurate with the proposal’s value.

Major consolidated subsidiaries

| Company name | Business activities |

| Itoki All Steel Co., Ltd. | Manufacture of counters, large top desks, wall storage furniture, desk panels, etc. |

| Fuji Living Industry Co., Ltd. | Manufacture of meeting and amenity chairs. |

| Itoki Market Space Inc. | Sales of shop fixtures/store planning |

| Itoki Toko Manufacturing Co., Ltd. | Manufacture of steel doors, safety deposit boxes, various types of shielding doors, fire-resistant walls, nuclear radiation shielding doors, etc. |

| Itoki Marui Industry Co., Ltd. | Manufacture of steel office machinery and equipment |

| Sanko Facilities Inc. | Sales of office equipment, furniture, fixtures and incidental goods, construction work, design management |

| FMSTAFF Ltd. | Consulting services related to facility management, etc. |

| Itoki Shared Value Co., Ltd. | Office space sharing business, office furniture rental and reuse business, etc. |

| Shin Nihon System Technology Corporation | Provision of IT solution services. |

| Dalton Corporation | Design, manufacture and sale of research and education equipment; design and sale of powder processing machinery; design and sale of high-tech plant systems. |

| Soar Co., Ltd. | Office furniture sales, delivery, installation, and general freight transportation services. |

| Tarkus Interiors Pte Ltd | Singaporean interior decoration company, made a subsidiary in 2016. |

| Novo Workstyle Asia Limited | Regional business headquarters for Asia, in Hong Kong, established 2017. |

| Novo Workstyle CO., Limited | Established in Jiangsu Province, China, to supply manufacturing components. |

| ITOKI SYSTEMS (SINGAPORE) PTE., LTD | Singapore subsidiary, sales of office furniture, proposals and logistics systems. |

| ITOKI CHINA HOLDINGS Co., Ltd. | Holding company for Chinese operations. Under the umbrella of Novo Workstyle Co. Offices in Beijing, Shanghai, Suzhou, Shenzhen, etc. |

| 16 other companies |

Business diagram

Source: Omega Investment from company materials

Business overview

Workplace business

A core business accounting for 74% of the consolidated sales: focus on proposal-based marketing to improve profitability.

The Company’s Workplace business recorded FY12/2024 sales of 102.2 billion yen, an operating profit of 8.0 billion yen and an operating profit margin of 7.9%. Sales grew by +8.2% YoY, operating profit by +29.2% YoY and operating profit margin by +1.3 percentage points YoY, achieving both sales growth and improved profitability. The operating profit margin has steadily improved over the past three years, indicating that the management policy of emphasizing added value and profitability is gaining ground.

Sales by region were 90,308 million yen (88.3% of the total) in Japan, 11,635 million yen (11.4%) in Asia and 317 million yen (0.3%) in others, indicating that the domestic business is currently the main focus. However, the Company is also looking to expand overseas markets.

Since the launch of steel desks in 1955, the Company’s office furniture business has successively developed and provided products to meet office needs in line with Japan’s economic growth and corporate business expansion. The Company has made a significant contribution to developing the Japanese economy.

In the Workplace business, the aim is not just to sell office furniture but to provide higher added value by proposing workplace design and obtaining commensurate value. In the past, it was challenging to differentiate office furniture on a stand-alone basis, leading to price competition, which in turn led to significant discounts together with non-office fixtures and fittings, which sometimes resulted in a decline in profitability. Although the Company’s office furniture was originally well-designed and had won many G Marks (see figure above, next page), it could be said that the Company needed to receive more compensation commensurate with the value it provided. As mentioned above, recent efforts to review the operating structure and culture (shift from sales-oriented to profit-oriented), generate revenue commensurate with enhanced customer value, and sell higher-value-added products and services are bearing fruit.

Workplace business revenue and profit trends

| Workplace business /Financial year | 2020/12 | 2021/12 | 2022/12 | 2023/12 | 2024/12 |

| Net sales | 83,032 | 80,561 | 85,945 | 94,546 | 102,261 |

| YoY | -3.0% | 6.7% | 10.0% | 8.2% | |

| Segment profit | 1,273 | 1,914 | 2,579 | 6,226 | 8,047 |

| YoY | 50.4% | 34.7% | 141.4% | 29.2% | |

| profit margin | 1.5% | 2.4% | 3.0% | 6.6% | 7.9% |

Source: Omega Investment from company materials

The office furniture market could add value as new ways of working evolve.

Japan’s office furniture market: market size of 840 billion yen, with stable growth.

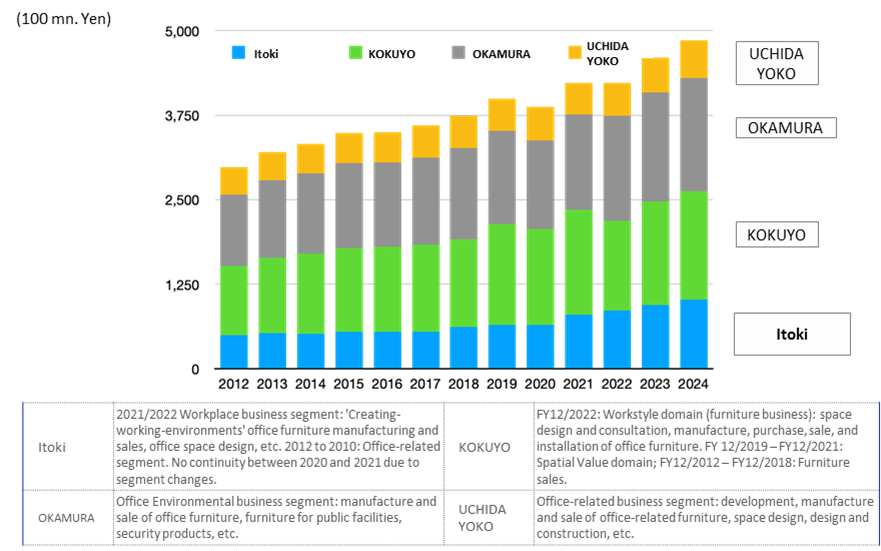

The Japan Office and Institutional Furniture Association (JOIFA), which has 109 member companies in the office furniture industry, publishes statistics and surveys as an industry association, but does not make the data publicly available.

Therefore, as a reference, figures for the four major office furniture companies, including the Company, were extracted from segment information and aggregated into a graph (differences in segment definitions among companies and differences in fiscal periods were ignored; Itoki and KOKUYO use December-period figures, OKAMURA uses FY3/2025 figures, and UCHIDA YOKO uses figures through FY7/2024).

Within the total of the four companies, shares in FY2024 were: the Company 21%, KOKUYO 33%, OKAMURA 34%, and UCHIDA YOKO 12%. KOKUYO and OKAMURA each hold nearly one-third of the market, while the Company ranks third and UCHIDA YOKO fourth; however, the Company’s share has been gradually increasing. In addition, the total value of the four companies has been growing steadily at around 3–4%.

In practice, when including sales of companies other than the four, the market size is estimated to be around 840 billion yen annually (of which approximately 400 billion yen is office furniture alone, with the remainder including consulting and construction), based on Omega Investment’s estimates from the sales size of JOIFA member companies and Itoki materials.

Office furniture business sales of the four major office furniture companies

Source: Prepared by Omega Investment from the annual reports of the companies.

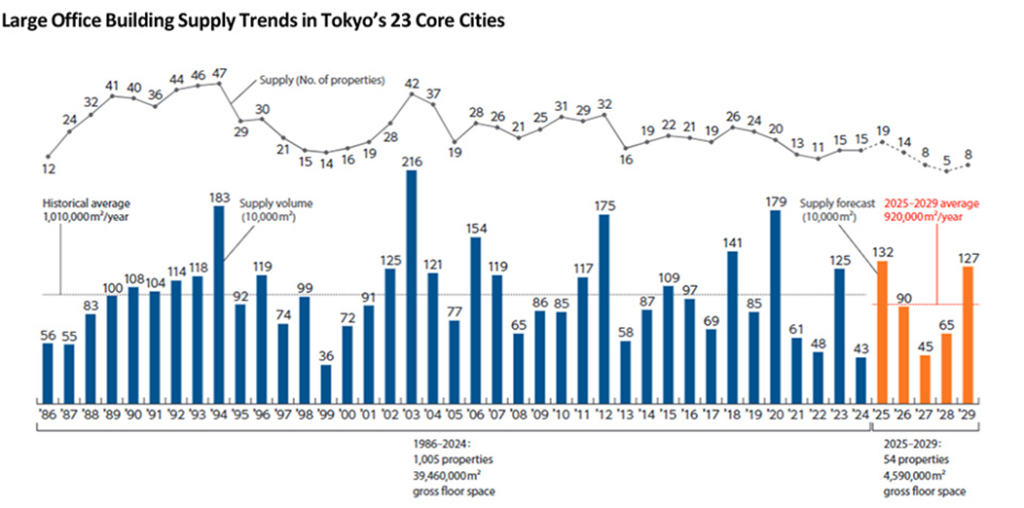

Office building market outlook: Supply of large office buildings in Tokyo’s 23 wards is expected to decline slightly, but the renewal market remains active.

Demand for office furniture is influenced by the supply of new office buildings as well as trends in office renewals.

First, regarding the supply of new office buildings, according to Mori Building’s “Tokyo 23 Wards Large Office Building Market Trend Study 2025,” supply is expected to increase in 2025 and 2026, but the average annual supply over the next five years is projected to fall below the long-term average (1986–2024).

Supply of large office buildings in the 23 wards of Tokyo (Mori Building survey)

Source: Omega Investment, based on Mori Building’s ‘Tokyo 23 Wards Large Office Building Market Trend Study 2025’.

However, what is important for this business are renewal projects, particularly those outside Tokyo.

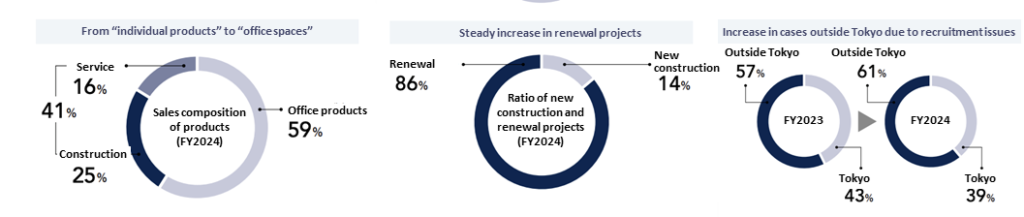

Starting with services such as space design and consulting, projects that also encompass construction and office product sales in an integrated manner allow the Company to deliver optimal office proposals tailored to each customer, while also contributing positively to profitability. Accordingly, the Company has been focusing its business development on renewal projects and projects outside the Tokyo metropolitan area. In particular, it has increased the number of space design designers from 120 to 180 over the past three years. As shown below, these efforts have borne fruit, with renewal projects now accounting for more than 80% of the total and the proportion of projects outside Tokyo steadily rising.

Structure of Itoki’s Workplace business

Source: Company materials

Recent developments in the office furniture market: new business opportunities due to the increasing sophistication of office needs.

In recent years, office needs have undergone a significant transformation. With the introduction of remote work due to the spread of infectious diseases and the subsequent return to the office, the role of the office is changing from what it used to be. This is expected to mean new business opportunities for office furniture companies. Background includes.

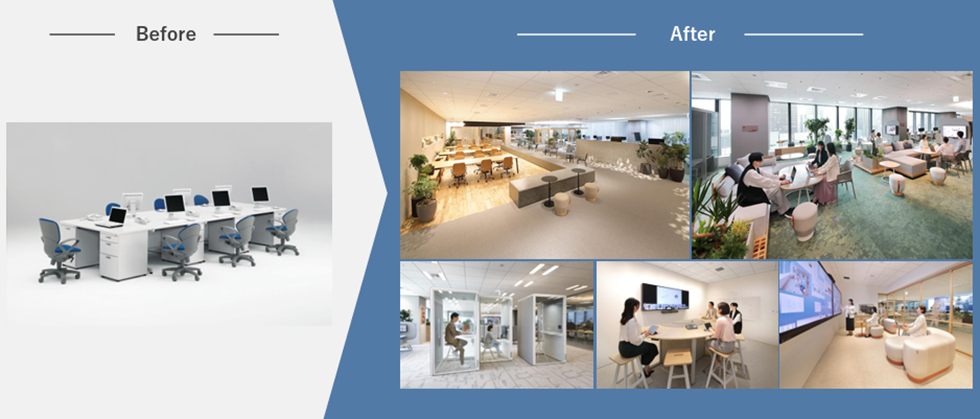

- Reform of work style: the Japanese economy has been stagnant for a long time. As the era of high growth, when productivity could be increased mainly in the manufacturing sector, ended and the proportion of tertiary industry increased, it became difficult to increase productivity, particularly among white-collar workers. Against this backdrop, there are indications that productivity should be improved through reforms in how people work. To achieve this, the internal organization of Japanese companies needs to change, and the composition of corporate offices is undergoing a significant transformation from the old fixed-seat-based office environment (see figure, next page).

- Advances in IT and networking: the way work is carried out in a company has changed significantly over the last 10-20 years due to IT development. The office must respond to the evolution of hardware, software, networks, etc. The change has been within the scope of Itoki’s Office 2.0, which the Company has advocated. In the future, Office 3.0, or the DX orientation of the office, will determine competition for superiority between companies.

- The office as a place for new value creation: as indicated in a), how people work will change significantly. The pandemic disease has triggered the introduction of remote work, but at the same time, it is still essential to have places where people meet face-to-face and communicate with each other. In the future, it will be crucial to maximize workers’ abilities by combining the central office as a place to share experiences with remote work, which is a flexible way of working at a high level.

- Attracting high value-added human resources: human resources are the biggest asset for future growth in all companies, but IT and other creative personnel need more supply. To retain such talented people, it is essential to have a great office environment and space.

Evolution of office spaces

Source: Company materials

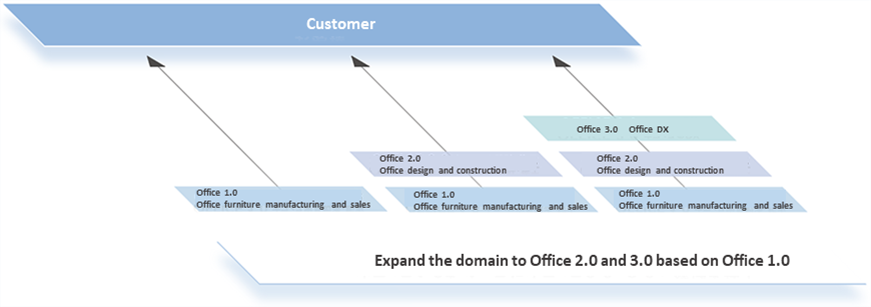

The Company’s approach: multiplying Office 1.0, 2.0 and 3.0 to increase corporate value.

The Company’s answer to the changes in the office furniture and office space market described above is shown in the diagram below: in Office 2.0, the Company has added value through office design and construction in addition to manufacturing and selling office furniture. Office 3.0 will further promote office DX. Data is collected by attaching sensors to office furniture and various parts of the office. By analysing this big data, it will be possible to provide customers with higher value-added services.

The Company’s proposed Office 3.0 concept

Source: Company materials

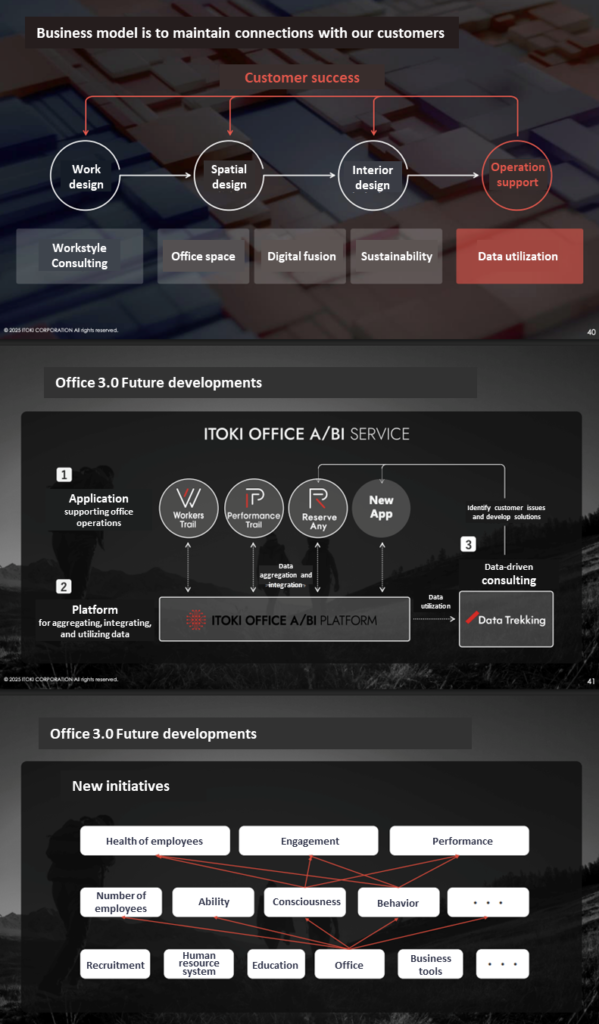

As a place to put Office 3.0 into practice, the Company consolidated its Tokyo headquarters in Nihonbashi in 2018 and opened ITOKI TOKYO XORK, which also serves as a showroom. (Current: ITOKI DESIGN HOUSE)

In 2024, this concept materialized as the “Data Trekking” service based on the “ITOKI OFFICE A/BI PLATFORM,” which was launched on February 14, 2024.

It is a consulting service for customers planning to relocate or renew their offices, using sensing data in the office as a guidepost to support office construction and operation in a companionable manner.

This system is for accumulating and analysing space operation data, organisational survey data, layout data and customer-specific index data based on a unique platform, the ITOKI OFFICE A/BI PLATFORM. Data is acquired using Workers Trail, an application that enables visualisation of “work” using beacon-based location information. Itoki’s proprietary cloud-based organisational survey allows for visualising individual and organisational performance and conditions. Itoki’s proprietary Performance Trail is a cloud-based organisational survey that visualises individual and organisational performance and conditions. The Company’s consulting team will analyse the data using the Office Data Map, a dashboard-type system developed independently by the Company, which will be linked to the office designers.

Furthermore, on March 13, 2024, the Company signed a joint development agreement for generated AI with AI start-up AKARI Inc. and has started developing applications related to automatic office design generation AI as part of the ‘ITOKI OFFICE A/BI SERVICE’ initiative.

Such a development will capture customers’ individual needs and specifically help them reform their office productivity. It has the potential to improve customer satisfaction, retain customers, and generate recurring revenues. The future development of this system will be the focus of much attention. The number of estimates appears to be steadily increasing.

Data Trekking service based on ITOKI OFFICE A/BI PLATFORM

Source: Company materials

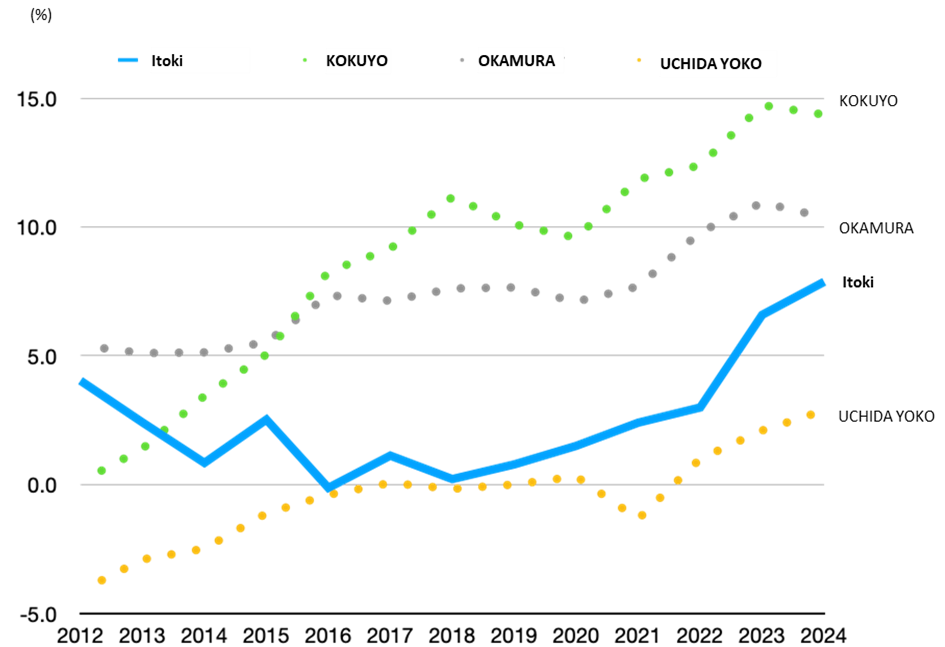

Peer competition:

As seen in the office furniture market, the four major players in this market – the Company, Kokuyo (TSEP: 7984), Okamura (TSEP: 7994) and Uchida Yoko (TSEP: 8057) – hold about 50% of the market. The table below compares each company’s most recent figures and other data. All but Okamura have a history of more than 100 years, while Okamura also has a long track record of more than 70 years. Regarding the companies’ businesses, most sales for Itoki Corporation and Okamura come from office furniture, fixtures, and fittings for commercial facilities. Kokuyo, on the other hand, as is well known, also generates a large proportion of its sales from stationery-related products. For Uchida Yoko, public-related (e.g., education-related ICT) and information-related (e.g., software licensing) sales account for 80% of its sales.

The following graph compares the profitability of each company’s office furniture business. As noted on page 10, the definition of each company’s segments is not necessarily the same, but it should serve as a rough guide. It shows that in recent years, profit margins have been improving for all companies, that KOKUYO and OKAMURA, which have large market shares, maintain high margins, and that although Itoki ranks third, it has been steadily improving its profit margin and narrowing the gap with the top two. As the industry overall is shifting toward an emphasis on profitability, it can be said that the Company’s efforts in pricing, value-added proposals, and proactive acquisition of projects outside Tokyo are beginning to bear fruit.

Four office furniture companies, operating profit margin trends in office furniture-related businesses

Source: Prepared by Omega Investment from the annual reports of the companies

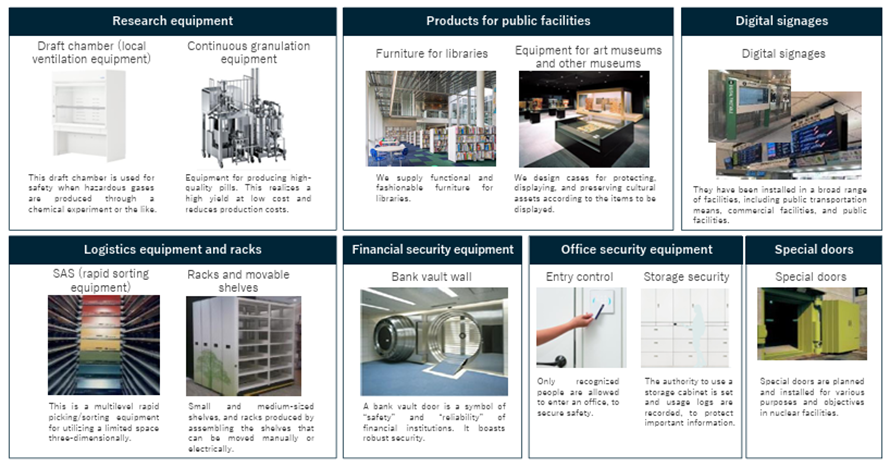

Equipment / Public business

Logistics-related facilities, research facility equipment and other unique products.

FY12/2024 sales in the Company’s Equipment / Public business were 34,572 million yen (-6% YoY), operating profit was 1,857 million yen (-2% YoY), and operating profit margin was 5.4%.

Sales by region were 34,184 million yen in Japan, 234 million yen in Asia, and 153 million yen in other areas. Again, the domestic market is the main market.

Equipment product range

Source: Company materials

Equipment / Public business revenue and profit trends

| Equipment / Public business /Financial year | 2020/12 | 2021/12 | 2022/12 | 2023/12 | 2024/12 |

| Net sales | 31,602 | 33,488 | 35,667 | 36,839 | 34,572 |

| YoY | 6.0% | 6.5% | 3.3% | -6.2% | |

| Segment profit | 1,225 | 974 | 1,482 | 1,906 | 1,857 |

| YoY | -20.5% | 52.2% | 28.6% | -2.6% | |

| Profit margin | 3.9% | 2.9% | 4.2% | 5.2% | 5.4% |

Source: Omega Investment from company materials

The Equipment / Public business dates to 1914, when the Company began selling vent-type safes. Since then, the Company has manufactured and sold a variety of warehouse-related fixtures and fittings and, since the 1980s, has been an industry pioneer in developing and supplying a range of automated warehouse equipment. Based on its experience producing safe doors, the Company also produced and launched special large doors for nuclear power facilities. The Company has continued developing numerous industry firsts, including developing secure locking systems. In recent years, there has been an extreme need for automation equipment for warehouse and distribution systems.

The main customers for logistics equipment are the automotive industry and equipment manufacturers. The main customers for public facilities products are museums, art galleries and libraries. Sales of logistics equipment depend on economic trends and corporate earnings. Still, they are expected to grow, as reducing logistics costs is an ongoing and vital management issue in the manufacturing industry. On the other hand, sales of public facilities are affected by budget execution by public offices and local authorities.

In the same segment, research equipment is another product to note. Dalton Corporation, which the Company invested in in 2011 and became a wholly owned subsidiary in 2016, manufactures and sells these products. Dalton Corporation was founded in 1939 as a manufacturer and distributor of scientific instruments and glassware for analysis (the Company was called San-Ei Seisakusho when it was founded). It established a scientific research facilities division, which developed and sold products used in various research facilities; in 1996, it acquired a powder and granular equipment manufacturer and expanded into powder machinery; in 2014, it introduced the Uni-X Lab Series of draft chambers and laboratory tables.

Dalton Corporation research facility equipment

Source: Omega Investment from company materials

Customers of laboratory equipment include pharmaceutical companies, universities and research institutions, and the sales are affected by trends in R&D expenditure/capital investment by pharmaceutical companies and scientific research funding by universities. Pharmaceutical companies, the largest customers, actively invest in R&D expenditure to develop new drugs. On the other hand, while there are concerns that research budgets at Japanese universities continue to be cut, major pharmaceutical customers’ robust research investment budgets are expected to continue. Hence, the sales of the Company’s research facility equipment should grow.

Growth strategy

◇ New medium-term management plan RISE To GROWTH 2026: Moving into “Profitability enhancement phase”

On 13 February 2024, the Company announced its new medium-term management plan, RISE TO GROWTH 2026, covering 2024-2026. It is positioned as a ‘high-profitability phase’ to enhance sustainable growth.

As mentioned earlier, the nature of the workplace, including the office, and its productivity improvements are attracting increasing attention. The thinking style of management at client companies is changing from a one-dimensional view of the office as a cost to a view of the office as an object of human capital investment that pursues investment effects. Furthermore, office DX and the IoT of office equipment are expected to advance. The Company holds the mission “We Design Tomorrow. We Design WORK-Style”, hoping that this transformation in workplace needs will lead to a long-term leap forward for the Company.

This medium-term management plan is based on the “Tech x Design based on PEOPLE” concept and consists of the vital strategy “7 Flags” and ESG strategies.

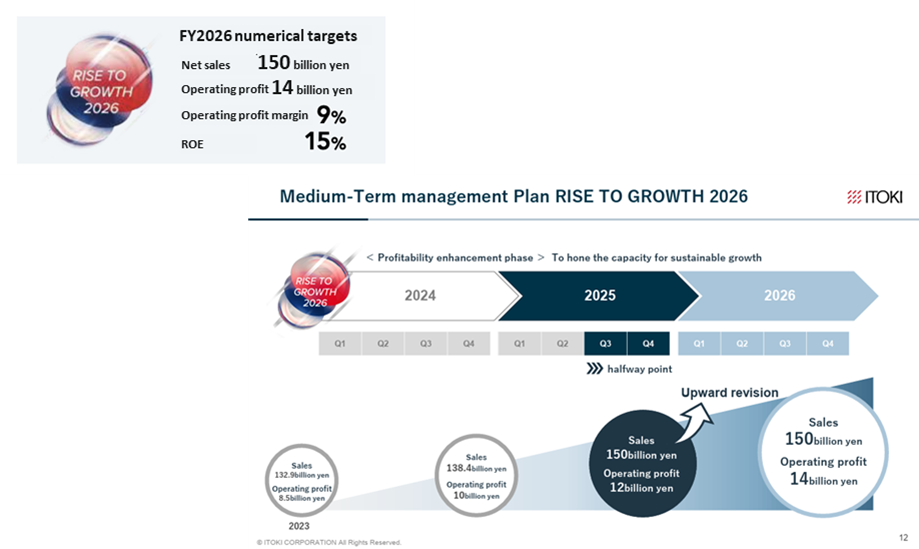

The Company’s financial targets for FY2026 are sales of 150 billion yen (up 13% from FY12/2023), operating profit of 14 billion yen (up 64%), operating profit margin of 9% (up 3 percentage points), and ROE of 15% (up 4 percentage points). These are more focused on improving profitability than increasing revenue and show the Company’s ambition to become an industry leader in terms of profitability by 2026.

Operating profit is expected to increase by a cumulative +5.5 billion yen from the FY2023, of which +4.8 billion yen is planned to be covered by increased earnings from the Workplace business. More specifically, the profit plan is based on the effects of improvements through enhanced customer value, cost reductions in production and logistics, improved profitability overseas, group synergies and increased revenues. It is set as a must-achieve target rather than a challenging target.

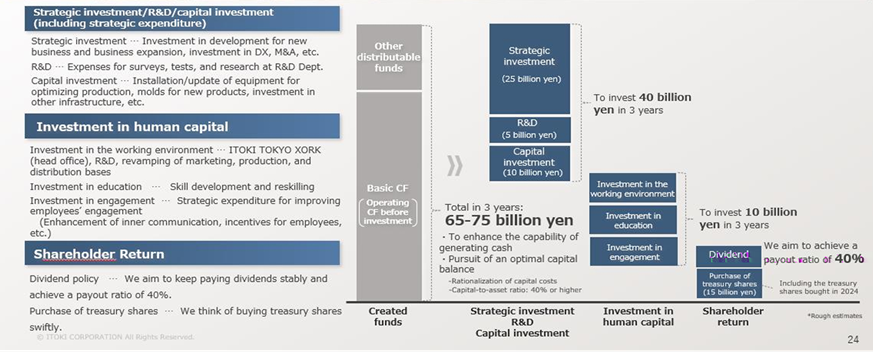

The Company’s message to the stock market is to maximize shareholder value and improve PBR by reducing the cost of capital while aiming to achieve ROE in excess of the assumed 9-10% cost of equity capital. Regarding shareholder returns, the Company will raise its dividend payout ratio by 10 percentage points to 40%. This is more than sufficient to meet the current expectations of the stock market.

The details of the plan will be discussed later in this report. Still, it can be said that it is a broadly well-developed plan that includes strengthening the core business base, seeding new office-related businesses, developing specialized facility areas, strengthening the earnings structure on a consolidated basis, human capital, and financial strategies. At the end of the first half of FY12/2025, the full-year earnings forecast is net sales of 150 billion yen and operating profit of 12 billion yen, with progress proceeding smoothly.

Source: Company materials

The following is a summary of these seven priority measures and their KPIs.

Source: Omega Investment from company materials

Supplementary Information: Allocate the results of improved profitability to reinvestment in line with the medium- to long-term strategy and strengthen shareholder returns.

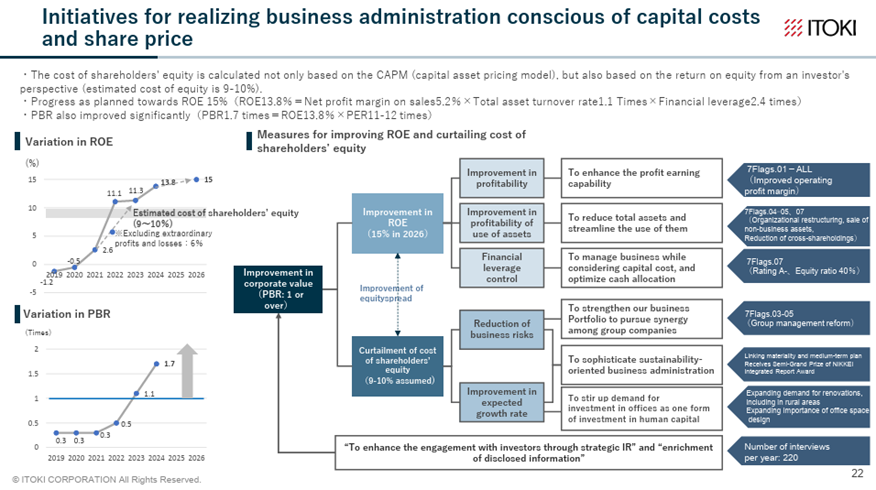

Supplementary Information: Achieve ROE that exceeds the cost of shareholders’ equity and promote higher PBR through expansion of equity spread.

Source: Company materials

Financial results

FY12/2024 financial results

◇ Establishment of a profitable structure. Highest profit and dividend increase.

The Company’s FY12/2024 results showed sales of 138.4 billion yen (+4% YoY) and operating profit of 10.0 billion yen (+18% YoY), with sales, operating profit, recurring profit and net profit all reaching record highs. ROE was 13.8% (+ 2.5pt YoY).

While steadily building up sales from renewal projects and office relocations, the Company significantly improved its profit margin through enhanced customer value. As a result, profits exceeded the Company’s forecasts despite increased SG&A expenses due to strategic spending.

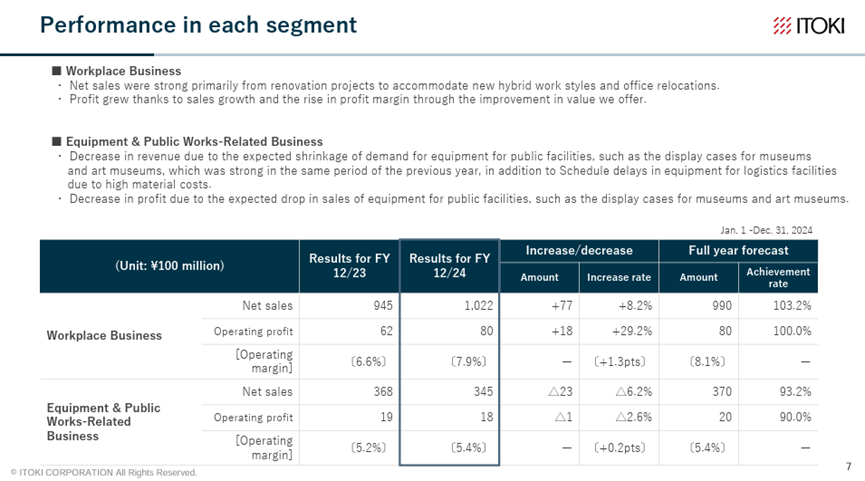

By segment, the Workplace-related business and the Equipment / Public business-related business each posted increased revenue and operating profit, and operating profit margins improved. The results were flawless.

By segment, the Workplace Business recorded revenue and profit growth, driving overall performance. The Equipment & Public Works-Related Business posted lower revenue and profit due to timing delays, but its operating profit margin improved. Overall, it was a flawless set of results. In addition, reflecting the strong performance, the year-end dividend for FY12/2024 was increased by 13 yen YoY to 55 yen.

Source: Company materials

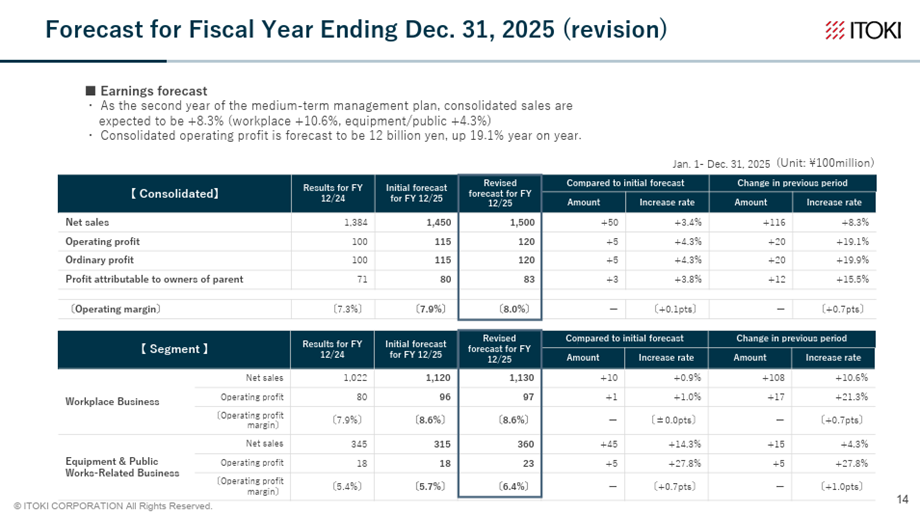

◇ FY12/2025 Company Forecast: Continued revenue and profit growth, with an upward revision to the full-year earnings forecast

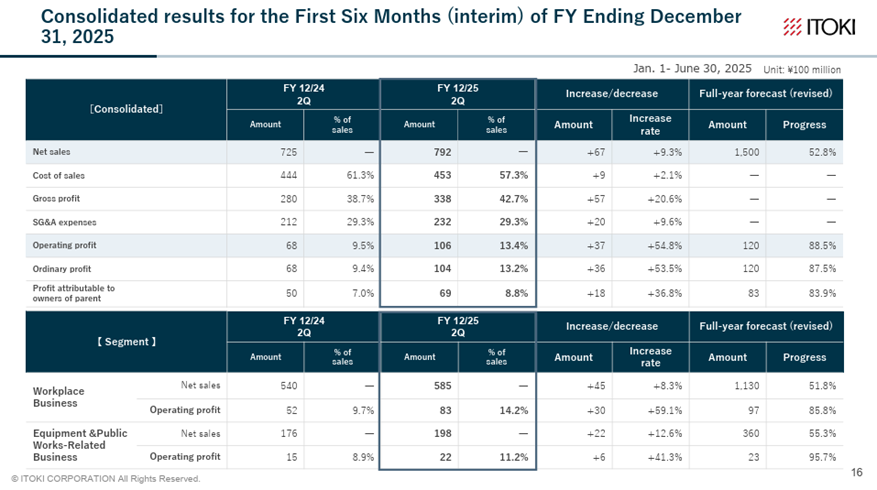

In the second quarter (interim) of FY12/2025, earnings were strong, and the full-year earnings forecast was revised upward.

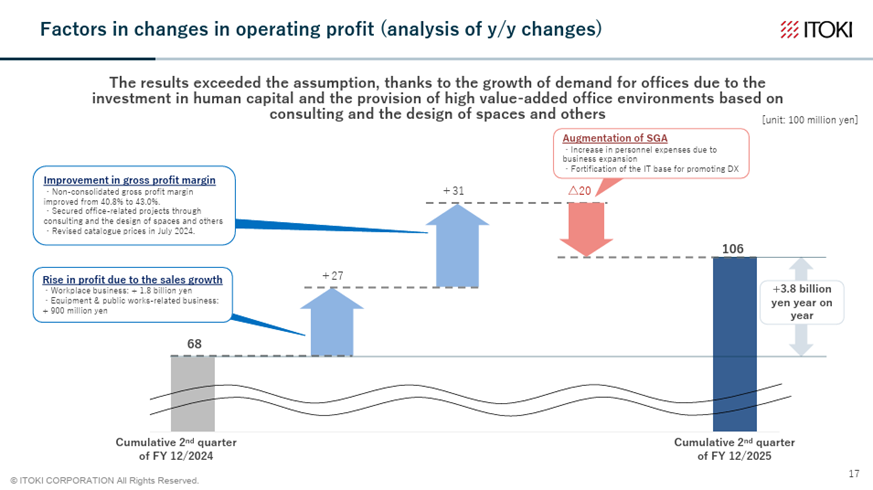

In the second quarter (interim) of FY12/2025, net sales were 79.2 billion yen (+9% YoY), operating profit was 10.6 billion yen (+54% YoY), ordinary profit was 10.4 billion yen (+53% YoY), and net income attributable to owner of parent was 6.9 billion yen (+36% YoY). In addition to revenue growth, the operating profit margin further improved. Both the Workplace Business and the Equipment & Public Works-Related Business recorded revenue and profit growth. In the Workplace Business, the Company steadily captured renewal projects and regional projects, and value-added offerings in offices based on space design proved effective. In the Equipment & Public Works-Related Business, equipment for research facilities performed strongly.

Source: Company materials

The full-year earnings forecast for FY12/2025 has been revised upward. The revised figures are net sales of 150 billion yen (+8% YoY), operating profit of 12 billion yen (+19% YoY), ordinary profit of 12 billion yen (+19% YoY), and net income attributable to owner of parent of 8.3 billion yen (+15% YoY), with upward revisions in both the Workplace Business and the Equipment & Public Works-Related Business. The deal pipeline is progressing smoothly, and the revised forecast provides a sense of reassurance.

Although profits in the second half of the current fiscal year will decline compared to the second half of the previous fiscal year, this is due to increased depreciation expenses from the cutover of the Company’s core system, higher bonuses, and increased R&D expenditure, and is not considered a cause for concern.

Source: Company materials

◇ Share price trends and focus: the results of reforms are reflected in share prices.

From the end of March 2022, when President Minato took office, to the end of August 2025, the Company’s share price rose from 347 yen to 2,538 yen, and PBR went from below 1x to about 2.27x. It is believed that the management policy and performance under President Minato’s regime have significantly turned around investment sentiment, which was concerned about the receding office needs that emerged with the COVID-19 disaster and the Company’s past low profitability.

Secondly, there is a danger that when investors consider the Company’s prospects, they are too caught up in the view that it sells goods to domestic offices, which narrows their view of the Company’s future potential. This view should be swept away, and the Company’s future should be assessed flatly.

In other words, progress on qualitative milestones should be considered in addition to the financial KPIs outlined in the medium-term management plan.

In other words, in addition to the progress made toward the financial KPIs set forth in the medium-term management plan, attention should also be paid to the qualitative initiatives underway. As conditions such as the persistent demand for improving office productivity, a reinforced focus on profitability on a consolidated basis, higher employee motivation toward creativity and innovation, the rising contribution of solution-based revenue centered on Office 3.0, and the materialization of new revenue opportunities beyond domestic offices, including logistics facilities, research laboratories, and expansion into Asian markets, come together, the Company’s business outlook for 2027–2029 will become increasingly clearer, and its share price is expected to move to the next stage. The timing when the stock market’s focus shifts to the blueprint of the next medium-term management plan also appears to be approaching.

Source: Company materials

Valuations

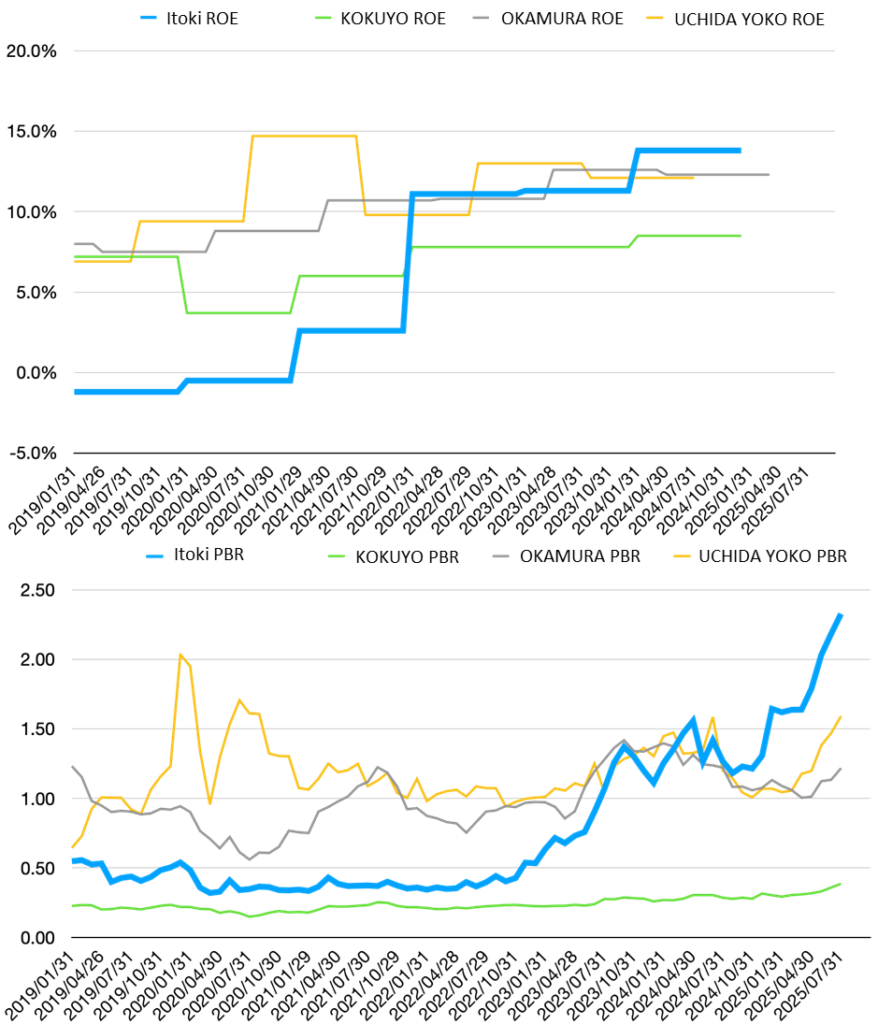

The charts below plot the ROE trends over the past six years and the PBR trends for the Company and three industry peers.

As shown, the Company’s ROE has now risen to the top among competitors, and its PBR is also the highest. This suggests that the current share price reflects the market’s strong evaluation of the Company’s strategy under its current medium-term management plan, which focuses on expanding earnings in its core Workplace business by emphasizing profitability while offering added value that supports customers’ human capital investment.

Looking ahead, it will be essential not only to steadily achieve the final targets of the current medium-term plan, but also to broaden its customer base in non-office domains and to accelerate recurring revenue generation in the office domain, thereby stabilizing ROE at a high level. Market attention is expected to gradually shift toward the next medium-term plan, making it a development that investors cannot afford to overlook.

Source: prepared by Omega Investment based on financial data from various companies.

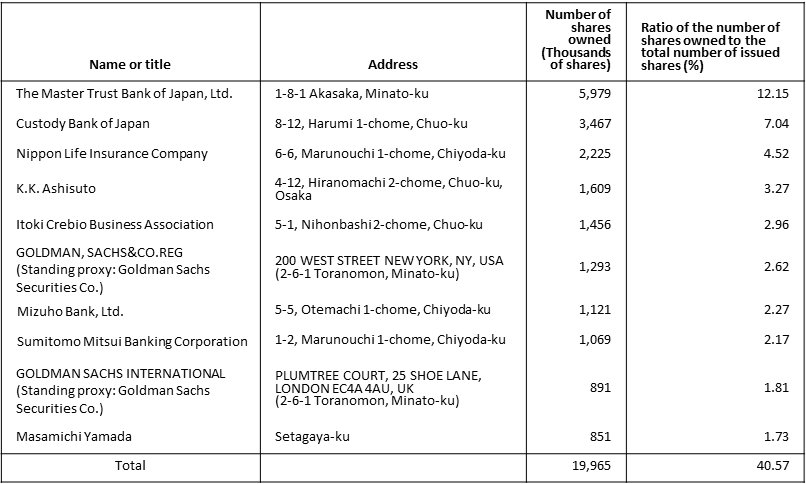

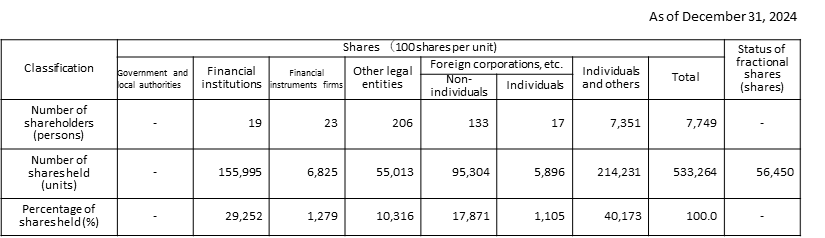

Major shareholders

Shareholding by ownership

Source: Annual Securities Report of the Company

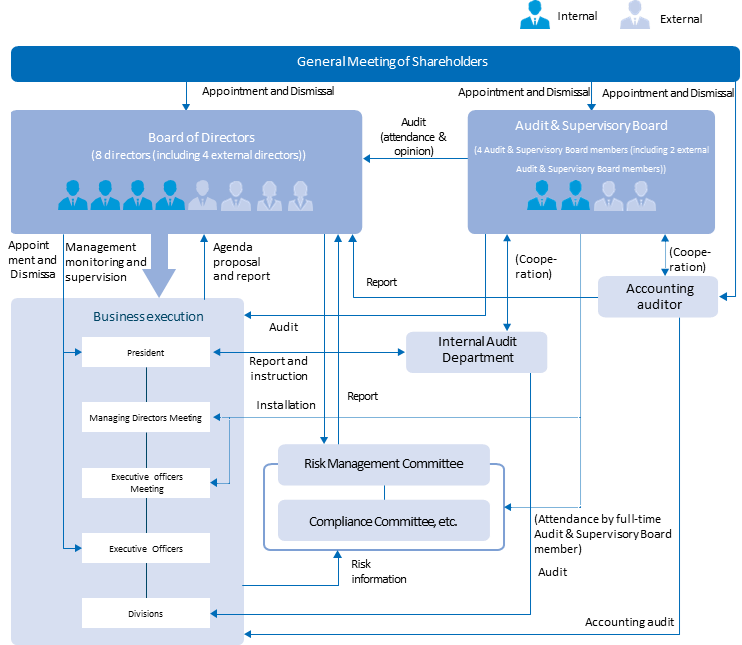

Corporate governance and top management

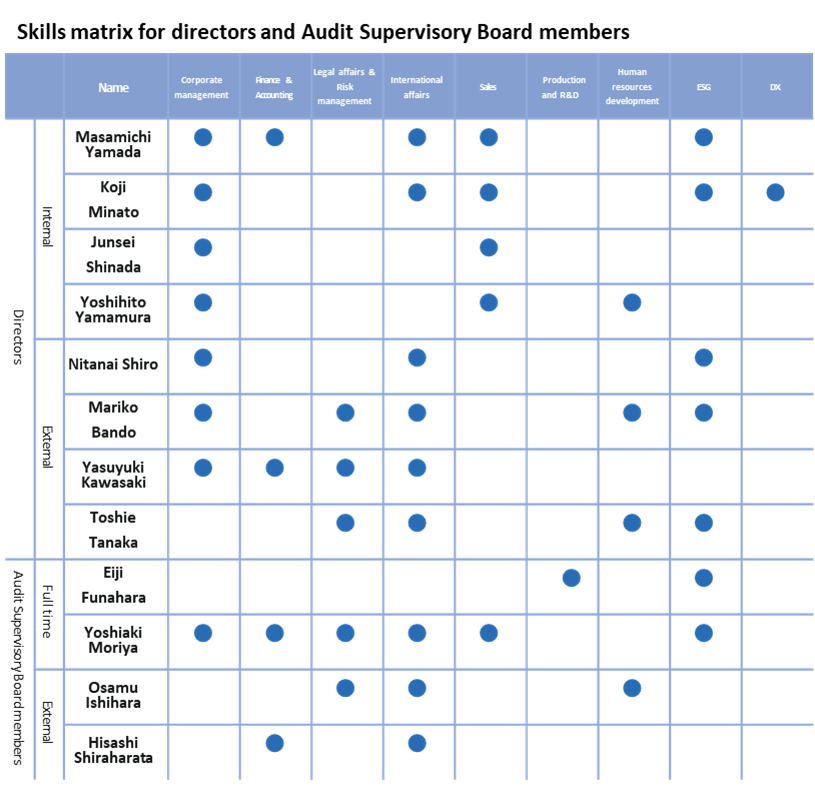

The Company has a board of auditors with eight directors, four of whom are outside directors and designated as independent directors, two full-time auditors, and two part-time auditors (all are independent officers). The Company has also adopted an executive officer system to separate management oversight from business execution.

The Company has not established voluntary advisory committees, such as nomination and remuneration. However, when discussing the nomination and remuneration of senior management and directors, the committee’s chairperson actively seeks the opinion of independent outside directors and receives appropriate advice and involvement, so governance is considered to be practically functioning within the current framework.

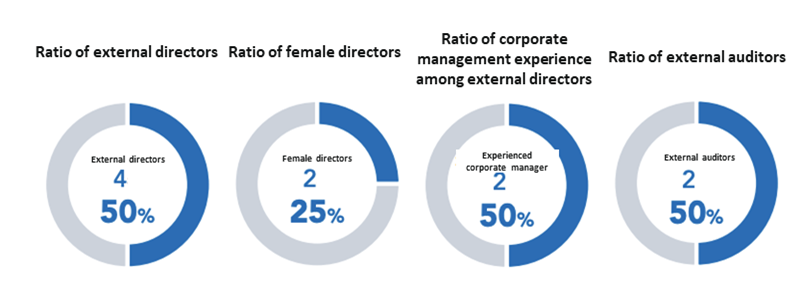

The diversity of the Board of Directors has been improving year by year, but further progress is required, particularly in terms of gender representation.

The Company’s corporate governance structure

Source: Omega Investment from company materials

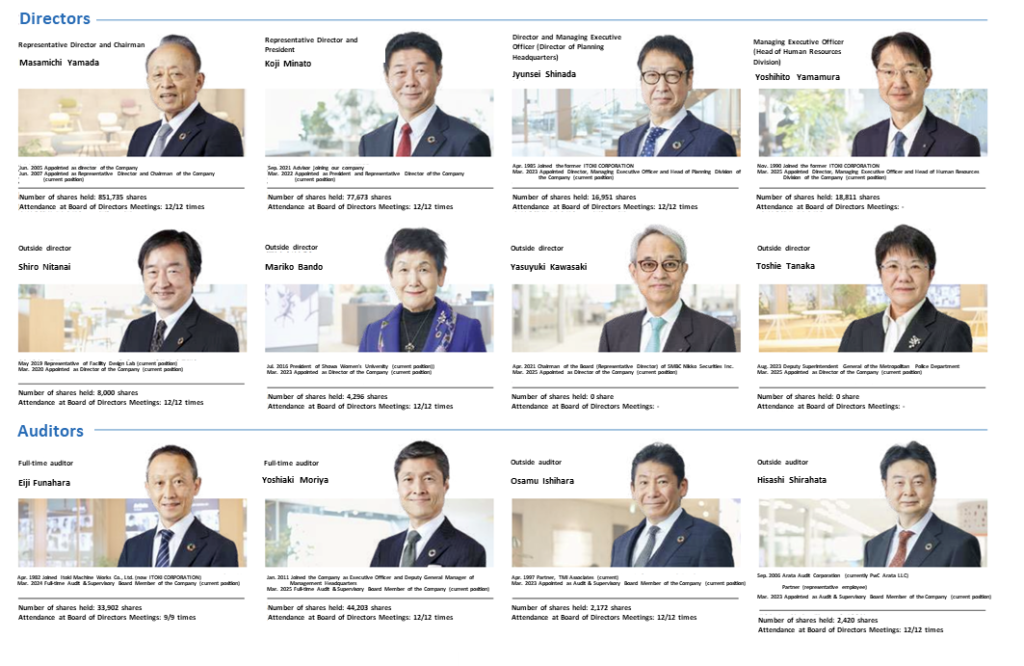

List of directors and officers

Source: company materials

Skills matrix for directors

Source: Company materials

Sustainability

As the Company is a manufacturing company, CO2 emissions are inevitable in office furniture and logistics equipment production. Therefore, the Company is highly aware of the SDGs and ESGs and has prepared an integrated report since 2021. In addition, the ESGDATA BOOK was published in 2022. It details the Company’s evaluation of its materiality, KPI performance and other information.

Particularly noteworthy is that it has developed a medium-term environmental plan regarding the environment, which communicates concrete and quantitative progress for each year. For greenhouse gas emissions, the plan sets out reduction targets not only for Scope 1 and 2 but also for Scope 3. Besides CO2 emissions, the plan also includes quantitative analyses of the introduction of renewable energy, carbon offsets, biodiversity, environmental accounting, etc.

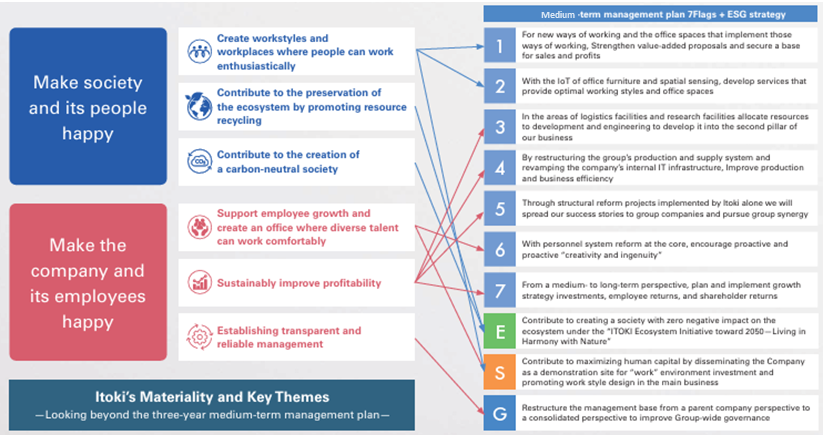

With respect to the SDGs, the Company has defined the following materiality issues, which are linked to its medium-term management plan 7 Flags as well as its ESG strategy.

The Company’s approach to materiality

Source: Company materials

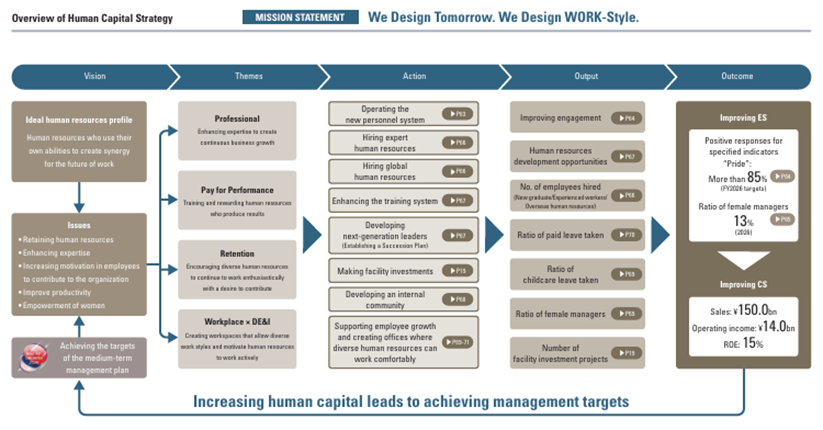

Human Capital Strategy

The Company is developing an environment that supports the growth and challenges of each employee, and is promoting a human resource strategy that leverages expertise and diversity. The specific framework and performance indicators are as follows.

Source: Company materials

Financial data (quarterly basis)

| Unit: million yen | 2023/12 | 2024/12 | 2025/12 | ||||||

| 2Q | 3Q | 4Q | 1Q | 2Q | 3Q | 4Q | 1Q | 2Q | |

| (Income Statement) | |||||||||

| Sales | 31,225 | 28,667 | 36,128 | 40,918 | 31,592 | 29,613 | 36,337 | 42,744 | 36,500 |

| Year-on-year | 9.9% | 9.4% | 8.3% | 10.7% | 1.2% | 3.3% | 0.6% | 4.5% | 15.5% |

| Cost of Goods Sold (COGS) | 18,955 | 17,483 | 22,090 | 24,545 | 19,888 | 17,644 | 21,182 | 23,993 | 21,381 |

| Gross Income | 12,270 | 11,184 | 14,038 | 16,373 | 11,704 | 11,969 | 15,155 | 18,751 | 15,119 |

| Gross Income Margin | 39.3% | 39.0% | 38.9% | 40.0% | 37.0% | 40.4% | 41.7% | 43.9% | 41.4% |

| SG&A Expense | 10,047 | 11,006 | 12,694 | 10,333 | 10,878 | 11,029 | 12,883 | 11,328 | 11,915 |

| EBIT (Operating Income) | 2,223 | 178 | 1,344 | 6,040 | 826 | 940 | 2,272 | 7,423 | 3,204 |

| Year-on-year | 444.9% | -162.2% | 171.5% | 26.4% | -62.8% | 428.1% | 69.0% | 22.9% | 287.9% |

| Operating Income Margin | 7.1% | 0.6% | 3.7% | 14.8% | 2.6% | 3.2% | 6.3% | 17.4% | 8.8% |

| EBITDA | 2,906 | 910 | 2,079 | 6,753 | 1,582 | 1,684 | 3,166 | 8,189 | 4,055 |

| Pretax Income | 2,275 | 363 | 936 | 6,006 | 1,328 | 1,035 | 1,702 | 7,257 | 3,208 |

| Consolidated Net Income | 1,411 | 202 | 997 | 4,104 | 985 | 725 | 1,409 | 4,910 | 2,045 |

| Minority Interest | 0 | 0 | 0 | 2 | 1 | 11 | 25 | -6 | 2 |

| Net Income ATOP | 1,411 | 202 | 996 | 4,101 | 985 | 714 | 1,383 | 4,916 | 2,044 |

| Year-on-year | 389.9% | -227.0% | -44.0% | 24.4% | -30.2% | 253.5% | 38.9% | 19.9% | 107.5% |

| Net Income Margin | 4.5% | 0.7% | 2.8% | 10.0% | 3.1% | 2.4% | 3.8% | 11.5% | 5.6% |

| (Balance Sheet) | |||||||||

| Cash & Short-Term Investments | 24,788 | 23,292 | 24,795 | 24,751 | 28,513 | 30,536 | 22,482 | 24,296 | 25,288 |

| Total assets | 111,693 | 111,573 | 117,437 | 127,459 | 120,701 | 120,935 | 120,521 | 132,329 | 126,248 |

| Total Debt | 17,361 | 17,342 | 17,308 | 38,662 | 41,566 | 42,881 | 37,924 | 44,114 | 41,268 |

| Net Debt | -7,427 | -5,950 | -7,487 | 13,911 | 13,053 | 12,345 | 15,442 | 19,818 | 15,980 |

| Total liabilities | 58,270 | 57,730 | 62,434 | 81,595 | 73,584 | 73,305 | 71,174 | 80,689 | 72,262 |

| Total Shareholders’ Equity | 53,379 | 53,800 | 54,960 | 45,818 | 47,068 | 47,571 | 49,260 | 51,562 | 53,908 |

| (Profitability %) | |||||||||

| ROA | 5.67 | 6.09 | 5.08 | 5.52 | 5.41 | 5.85 | 6.04 | 6.16 | 7.34 |

| ROE | 12.45 | 13.12 | 11.27 | 13.76 | 12.51 | 13.41 | 13.79 | 16.43 | 17.94 |

| (Per-share) Unit: JPY | |||||||||

| EPS | 31.1 | 4.5 | 22.0 | 85.7 | 20.0 | 14.5 | 28.1 | 99.9 | 41.4 |

| BPS | 1,177.1 | 1,186.4 | 1,212.0 | 933.1 | 956.6 | 966.8 | 1,001.1 | 1,047.9 | 1,091.1 |

| Dividend per Share | 0.00 | 0.00 | 42.00 | 0.00 | 0.00 | 0.00 | 55.00 | 0.00 | 0.00 |

| Shares Outstanding (million shares) | 45.66 | 45.66 | 45.66 | 53.38 | 53.38 | 53.38 | 53.38 | 53.38 | 53.38 |

Source: Omega Investment

Financial data (full-year basis)

| Unit: million yen | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 |

| (Income Statement) | ||||||||||

| Sales | 106,516 | 101,684 | 108,684 | 118,700 | 122,174 | 116,210 | 115,905 | 123,324 | 132,985 | 138,460 |

| Year-on-year | 3.4% | -4.5% | 6.9% | 9.2% | 2.9% | -4.9% | -0.3% | 6.4% | 7.8% | 4.1% |

| Cost of Goods Sold | 68,424 | 65,071 | 70,012 | 77,479 | 80,712 | 74,536 | 74,186 | 77,575 | 80,744 | 83,259 |

| Gross Income | 38,092 | 36,613 | 38,672 | 41,221 | 41,462 | 41,674 | 41,719 | 45,749 | 52,241 | 55,201 |

| Gross Income Margin | 35.8% | 36.0% | 35.6% | 34.7% | 33.9% | 35.9% | 36.0% | 37.1% | 39.3% | 39.9% |

| SG&A Expense | 33,949 | 33,862 | 35,761 | 39,336 | 40,776 | 40,089 | 39,158 | 41,167 | 43,717 | 45,123 |

| EBIT (Operating Income) | 4,143 | 2,751 | 2,911 | 1,885 | 686 | 1,585 | 2,561 | 4,582 | 8,524 | 10,078 |

| Year-on-year | 70.9% | -33.6% | 5.8% | -35.2% | -63.6% | 131.0% | 61.6% | 78.9% | 86.0% | 18.2% |

| Operating Income Margin | 3.9% | 2.7% | 2.7% | 1.6% | 0.6% | 1.4% | 2.2% | 3.7% | 6.4% | 7.3% |

| EBITDA | 6,551 | 5,316 | 5,551 | 4,615 | 4,436 | 5,603 | 6,148 | 7,821 | 11,417 | 13,185 |

| Pretax Income | 4,246 | 2,918 | 3,401 | 3,083 | 938 | 1,277 | 1,523 | 8,372 | 8,378 | 10,071 |

| Consolidated Net Income | 4,631 | 1,850 | 2,442 | 1,744 | -579 | -355 | 933 | 5,181 | 5,907 | 7,223 |

| Minority Interest | 101 | -56 | 40 | 19 | -28 | -119 | -233 | -113 | 1 | 39 |

| Net Income ATOP | 4,530 | 1,907 | 2,402 | 1,725 | -550 | -235 | 1,166 | 5,294 | 5,905 | 7,183 |

| Year-on-year | 109.7% | -57.9% | 26.0% | -28.2% | -131.9% | -57.3% | -596.2% | 354.0% | 11.5% | 21.6% |

| Net Income Margin | 4.3% | 1.9% | 2.2% | 1.5% | -0.5% | -0.2% | 1.0% | 4.3% | 4.4% | 5.2% |

| (Balance Sheet) | ||||||||||

| Cash & Short-Term Investments | 21,533 | 19,839 | 19,977 | 16,529 | 17,030 | 18,246 | 17,451 | 26,976 | 24,795 | 22,482 |

| Total assets | 98,175 | 95,681 | 102,451 | 108,710 | 108,778 | 105,096 | 103,898 | 115,288 | 117,437 | 120,521 |

| Total Debt | 18,927 | 19,931 | 17,892 | 16,834 | 22,166 | 21,742 | 20,091 | 19,487 | 17,308 | 37,924 |

| Net Debt | -2,606 | 92 | -2,085 | 305 | 5,136 | 3,496 | 2,640 | -7,489 | -7,487 | 15,442 |

| Total liabilities | 50,864 | 50,275 | 54,997 | 61,200 | 62,940 | 60,901 | 58,818 | 65,374 | 62,434 | 71,174 |

| Total Shareholders’ Equity | 45,677 | 44,949 | 46,863 | 46,857 | 45,370 | 43,812 | 44,931 | 49,871 | 54,960 | 49,260 |

| (Cash Flow) | ||||||||||

| Net Operating Cash Flow | 4,522 | 5,073 | 3,565 | 1,384 | 3,586 | 4,561 | 2,774 | 5,804 | 6,321 | -1,000 |

| Capital Expenditure | 1,114 | 1,641 | 1,333 | 3,477 | 3,226 | 1,729 | 2,110 | 4,145 | 3,316 | 6,036 |

| Net Investing Cash Flow | -803 | -4,044 | -2,971 | -3,094 | -3,221 | -1,152 | -1,170 | 4,923 | -4,012 | -7,107 |

| Net Financing Cash Flow | -3,807 | -2,571 | -706 | -2,463 | 0 | -2,267 | -2,658 | -1,426 | -4,148 | 5,905 |

| Free Cash Flow | 3,408 | 3,664 | 2,342 | -1,924 | 635 | 2,832 | 664 | 1,659 | 3,005 | -4,146 |

| (Profitability ) | ||||||||||

| ROA (%) | 4.65 | 1.97 | 2.42 | 1.63 | -0.51 | -0.22 | 1.12 | 4.83 | 5.08 | 6.04 |

| ROE (%) | 10.38 | 4.21 | 5.23 | 3.68 | -1.19 | -0.53 | 2.63 | 11.17 | 11.27 | 13.79 |

| Net Margin (%) | 4.25 | 1.87 | 2.21 | 1.45 | -0.45 | -0.20 | 1.01 | 4.29 | 4.44 | 5.19 |

| Asset Turn | 1.09 | 1.05 | 1.10 | 1.12 | 1.12 | 1.09 | 1.11 | 1.13 | 1.14 | 1.16 |

| Assets/Equity | 2.23 | 2.14 | 2.16 | 2.25 | 2.36 | 2.40 | 2.36 | 2.31 | 2.22 | 2.28 |

| (Per-share) Unit: JPY | ||||||||||

| EPS | 91.6 | 40.1 | 52.7 | 37.8 | -12.1 | -5.2 | 25.8 | 117.0 | 130.3 | 147.0 |

| BPS | 953.5 | 986.8 | 1,028.9 | 1,027.4 | 995.8 | 970.4 | 993.9 | 1,101.3 | 1,212.0 | 1,001.1 |

| Dividend per Share | 13.00 | 13.00 | 13.00 | 13.00 | 13.00 | 13.00 | 15.00 | 37.00 | 42.00 | 55.00 |

| Shares Outstanding (million shares) | 52.14 | 52.14 | 52.14 | 45.61 | 45.66 | 45.66 | 45.66 | 45.66 | 45.66 | 53.38 |

Source: Omega Investment