2026-04-10

Home

Japanese

Omega Investment Co., Ltd.

KYODO PUBLIC RELATIONS (Price Discovery – 2Q update)

| Share price (8/28) | ¥920 | Dividend Yield (25/12 CE) | 1.5 % |

| 52weeks high/low | ¥600/974 | ROE(24/12) | 16.5 % |

| Avg Vol (3 month) | 250.9 thou shrs | Operating margin (24/12) | 14.7 % |

| Market Cap | ¥8.11 bn | Beta (5Y Monthly) | -0.31 |

| Enterprise Value | ¥5.10 bn | Shares Outstanding | 8.809 mn shrs |

| PER (25/12 CE) | 10.1 X | Listed market | TSE Standard |

| PBR (24/12 act) | 2.2 X |

| Click here for the PDF version of this page |

| PDF version |

Record-high first half. Toward an “AI-driven” re-rating on a stable PR base, plus growth in influencer/AI, consolidation of TCI, and reinforcement of public affairs (PA)

◇ Investment conclusion: neutral for now; increase positions in stages upon confirmation of “upside in quality.”

KYODO PUBLIC RELATIONS (the “Company”) continues to have significant medium- to long-term re-rating potential, in our view. For the first half, consolidated net sales were 3,958 million yen (YoY +11.0%) and operating profit was 632 million yen (YoY +11.8%), both at record-high levels; full-year progress is also on plan at 46.6% for net sales and 49.4% for operating profit. With an equity ratio of 62.0%, the Company has ample financial flexibility, giving it room to balance growth investment with shareholder returns, supporting the “proactive view as an undervalued growth name” presented in the May Basic Report.

Earnings drivers are a structure in which steady PR business (+8.7%) is augmented by growth in the Influencer marketing business (+27.0%) and the AI & Big Data solutions business (+7.9%). These two domains raise profit visibility in both volume and quality through unit-price effects and the visualization of recurring charges (MRR). In addition, making Total Communications, Inc. (TCI), a healthcare specialist, a subsidiary is expected to deepen proposal capabilities via collaboration with industry/association key opinion leaders (KOL) and acquired expertise, potentially contributing to unit-price improvement from the next fiscal year onward.

Points to note are upfront costs associated with hiring and implementing generative AI, as well as volatility in non-operating income and expenses. However, given the first-half profit increase and buildup of high-value-added projects and recurring revenues, these are likely absorbable. Accordingly, this report follows the analysis in the Basic Report while positioning incremental disclosure of qualitative KPIs (unit price, retention rate, MRR, etc.) as catalysts for evaluation.

While structural improvements (diversification of the business portfolio and financial soundness) are progressing, some short-term noise from upfront spending remains. We therefore consider it appropriate to raise the investment weight flexibly each time the unit-price effects in specialized domains and the KPIs are confirmed at events such as earnings results/briefings, disclosure of projects after consolidating TCI, and progress in implementing AI products.

◇ FY12/2025 second-quarter (2Q) highlights: record-level increases in sales and profit; visualization of segment contributions proceeds in tandem with strengthened financial soundness

The Company’s FY12/2025 2Q results were consolidated net sales of 3,958 million yen (YoY +11.0%), operating profit of 632 million yen (YoY +11.8%), ordinary profit of 626 million yen (YoY +8.6%), and interim net income attributable to owners of the parent of 355 million yen (YoY +34.3%). EPS was 40.76 yen, and the Company characterizes this as “record-high sales and profit.” Of the 391 million yen increase in net sales, contributions were PR +231 million yen, Influencer +124 million yen, and AI +36 million yen; the quantitative growth driver was PR, while the growth rate was led by Influencer (+27.0%) (PR +8.7%, AI +7.9%). The ordinary-profit growth rate lagged operating-profit growth due to a decline in non-operating profit and an increase in non-operating expenses (non-operating profit: 17,066 thousand yen in 2Q total previous year → 6,675 thousand yen current year; non-operating expenses: 5,759 thousand yen → 12,680 thousand yen). Meanwhile, SG&A increased from 1,063,894 thousand yen to 1,140,755 thousand yen, but this represents upfront spending through human capital investment (e.g., stepped-up hiring of AI/data talent) and is consistent with measures aimed at improving medium-term value added. On the financial side, the equity ratio improved to 62.0% (58.8% at the previous fiscal year-end), and net assets increased to 4,089 million yen. Operating CF was +566 million yen, investing CF −62 million yen, and financing CF −337 million yen; while implementing share buybacks and dividends, cash and cash equivalents increased to 3,387 million yen.

On the business side, PR began pilot operation of generative-AI-based tools and accelerated the shift toward a consulting model; influencer expanded cross-media monetization centered on short-form video; and AI broadened its base through product strengthening and increased orders for in-house development support. In July, healthcare-specialized PR firm TCI became a subsidiary. From the third quarter onward, expansion of specialized domains and deeper KOL collaboration are expected. Full-year plans (net sales 8,500 million yen, operating profit 1,280 million yen, ordinary profit 1,280 million yen, net income 730 million yen) are unchanged, and progress stands at 46.6% for net sales, 49.4% for operating profit, 48.9% for ordinary profit, and 48.6% for net income, indicating steady performance. The negative factor of worsening non-operating items has ample room for absorption under the current policy of increasing on-hand liquidity and strengthening equity. Margins are expected to be raised by higher value added in PR and unit-price improvement in influencer/AI.

Despite headwinds in non-operating items, improvement on the operating side led to net income. From the third quarter onward, the “unit-price effect” of incorporating TCI and applying generative AI will be the focus of verification. We see room for upward revision in both progress rates and capital efficiency.

◇ Segment analysis: record-level increases in sales and profit; visualization of segment contributions proceeds in tandem with strengthened financial soundness

The Company reports three segments: the PR business, the Influencer marketing business, and the AI & Big data solutions business. For FY12/2025 2Q total: PR 2,889 million yen (YoY +8.7%), influencer 583 million yen (YoY +27.0%), AI & Big Data 485 million yen (YoY +7.9%), consolidated total 3,958 million yen (YoY +11.0%). The sales mix is roughly PR about 73%, influencer about 15%, and AI about 12%. High-growth two domains stack on top of core PR, increasing the thickness of the earnings portfolio.

PR business: centered on long-term retainer contracts, the Company provides a comprehensive offering including press conference operations, crisis communications, and media relations, 2Q total sales: +8.7%. Pilot operation of PR support tools utilizing generative AI has begun, targeting gains in productivity and accuracy. The client portfolio review is progressing, with the proportion of foreign-affiliated clients for single-company retainers at 36.7% (end-June 2025). In addition, from August 2024, the Company entered into a strategic partnership with U.S.-based Ballard Partners. In Japan, it is strengthening the crisis consulting structure (including a collaboration with the Japan Corporate Crisis Management Association).

Influencer marketing business: production tie-ups and social media contributed to profit, marking record highs in both sales and profit, 2Q total sales: +27.0%. In April, distribution on a new channel for TikTok began, accelerating cross-platform rollout centered on short-form video. Further, through development projects targeting Generation Alpha and Generation Z, the Company is creating new IP businesses to build multi-layered future revenue sources.

AI & Big data solutions business: progress continued in enhancing proprietary product functions and winning projects in data science. In AI in-house development support, orders were received from major companies in food and apparel. Despite higher costs due to stepped-up hiring, 2Q total sales still rose +7.9%. A significant update to the monitoring tool “CERVN” enhanced visualization of PR linkage, and support for introducing the generative AI platform “Dify” has begun to promote in-house use of LLMs.

◇ Outlook: full-year plan maintains increases in sales and profit; assuming stacking of new domains on the PR foundation, progress on the mid-term plan is broadly on track

The Company leaves its full-year plan unchanged at net sales of 8.5 billion yen (YoY +16.1%), operating profit of 1.28 billion yen (YoY +19.1%), ordinary profit of 1.28 billion yen (YoY +18.3%), and net income of 730 million yen (YoY +38.7%). Progress versus first-half results is 46.6% for net sales, 49.4% for operating profit, 48.9% for ordinary profit, and 48.6% for net income; considering typical seasonality, achievability is high. During the year, PR retainers and project accumulation form the quantitative base, while influencer and AI & Big Data are expected to provide upside in growth rates. The decision in July to make Total Communications, in which only staff with licensed dietitians are employed, a consolidated subsidiary aims to reinforce specialized domains and strengthen proposal capabilities through KOL collaboration;. However, consolidation is expected from the third quarter, with annual sales of around 100 million yen the impact on this fiscal year’s figures is seen as limited. On the cost side, the plan incorporates upfront costs associated with hiring/developing data science talent and implementing generative AI. Still, absorption is to be achieved through improved PR unit prices/retention, improved inventory turnover in influencer, and more substantial recurring revenue in AI. The dividend plan is a year-end dividend of 14 yen, and capital policy remains a balance between growth investment and shareholder returns. In the medium term, the Company targets net sales of 10.0 billion yen and operating profit of 1.6 billion yen (operating margin 16%) in FY12/2026. Given current first-half progress and the diversified business portfolio, we evaluate that a scenario bringing these within range through both volume expansion and unit-price increases is plausible. Negative factors are short-term deterioration in non-operating items and front-loaded costs accompanying hiring reinforcement. Still, improvement in the equity ratio, ample on-hand liquidity, and stable PR earnings are expected to function as buffers.

First-half progress is on plan; the focus for the second half is how much upside from new domains can be added on top of PR accumulation. Even if the quantified impact of consolidating TCI is limited, if unit-price improvement through expansion of specialized domains becomes visible, profit visibility for the next fiscal year will rise another notch.

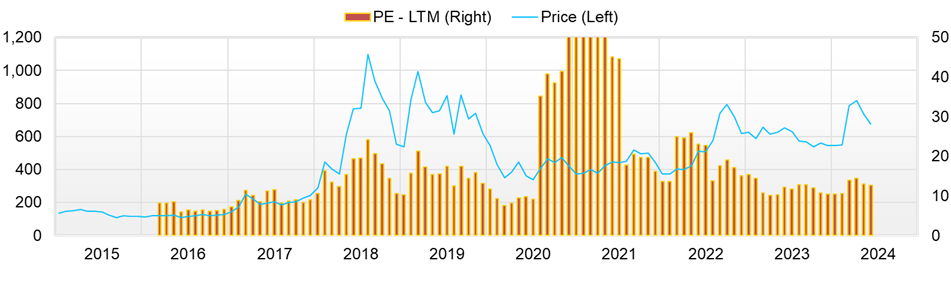

◇ Share price trend and points to watch: responsive to events; testing the top of the range; room to break out depending on the quality of qualitative KPIs

Current valuation (forecast PER 10.86x, actual PBR 2.16x, market capitalization 7.9 billion yen, ROE 16.5%, ROIC 16.2%, beta 0.85) shows little sign of excessive expensiveness relative to profitability. We see the conditions for testing the upside as “simultaneous confirmation of volume (project accumulation) × quality (unit price/retention/MRR).” Over the past three months, after a steady rise from mid-May, the share price extended on event-driven flows in late July. It rose from 909 yen at the close on July 24 to 938 yen on the 25th (+3.2%); trading volume increased to 56 thousand shares; and the intraday high of 961 yen on July 25 has been recognized as short-term resistance. Subsequently, the year-to-date high of 974 yen was updated on August 7; on the 2Q results day of August 13 it was firm at 958 yen (volume 100 thousand shares), but on the following 14th and 15th it was pushed back to the lower end of the range at 905 yen and 901 yen, respectively, by profit taking after the event.

The news flow has a strong “region × function” complementarity. Consolidating Nagoya-based DBPR strengthened the sales base in the Chubu region and media relations in the Tokai area. Completion of PR support for Expo 2025, Osaka, Kansai, contributes to visualizing a track record in crisis management and media training. The partnership with the Japan Corporate Crisis Management Association and collaboration with MS&AD InterRisk Research & Consulting in sustainability expanded consulting functions in non-financial domains. In addition, implementing Deep Research into the in-house operations tool “SAKAE” represents deepening PR-DX and tends to contribute to improved KPI quality (visualization and proposal depth).

In individual events, the 24, July resolution to make TCI a consolidated subsidiary was the most share-price-sensitive factor, directly leading to the rise on the following 25th and entry into the year-to-date high zone. Going forward, spillover effects are expected in the form of unit-price improvement in healthcare and higher order-certainty through KOL collaboration (scheduled to be consolidated from the third quarter; the impact on this fiscal year’s results is expected to be limited). In addition, the acquisition of Company shares by Representative Director Masataka Ishiguri (holdings after acquisition: 174,733 shares; ownership 2.00%; third-largest individual shareholder) is a positive signal that can reduce the risk premium from the standpoint of governance and incentive alignment.

Technically, it is reasonable to view demand on dips around 900 yen and resistance zones at 961 yen and 974 yen; as long as support holds around the 25-day moving average, a breakout above 961–974 yen accompanied by volume would confirm a trend reversal, whereas a break below 900 yen would mark a phase to consider a correction scenario due to momentum slowing. Market focus is shifting to how far the “unit-price effect” from new domains (influencer/AI & Big Data, plus healthcare) can overlap with the stability of PR. A topside breakout of the range requires strengthening of qualitative KPIs (PR retainer retention rate and proportion of foreign-affiliated clients; creator unit price and utilization; AI MRR) and disclosure of case studies. While remaining neutral as a base stance, there is ample room to tilt overweight if improvement in the above KPIs is confirmed. Event-driven timing for investment is organized as the phases in which “volume × quality” progress is shown simultaneously: KPI disclosure at results/briefings; concretization of crisis-management/sustainability collaborations into specific projects; visualization of high-unit-price healthcare projects after consolidating TCI; and PR-DX updates such as “SAKAE” Deep Research and “AI-Press.”

Post-results pullbacks are mainly supply-demand in nature. To break through 961/974 yen with volume, incremental qualitative KPIs, and unit-price increases stemming from specialized domains (healthcare, crisis management, sustainability) are indispensable. The CEO’s purchase of Company shares is corroborating evidence for a bullish bias.

Company profile

◇ From a long-established independent PR firm to an integrated communications company,; accelerating growth on three pillars

KYODO PUBLIC RELATIONS CO., LTD., while maintaining its foundation as a long-established independent PR firm, is evolving into an integrated communications company through the trinity of PR, Influencer, and AI/Big Data. It was established on November 14, 1964; its head office is in Tsukiji, Chuo-ku, Tokyo; and the consolidated headcount is 361 (as of June 2025). The core of the business model is long-term retainer contracts, with diversification of the client portfolio and growth in foreign-affiliated accounts progressing. Segment sales for FY12/2025 2Q total were PR 2,889.78 million yen, Influencer 583.20 million yen, AI & Big Data 485.48 million yen, and consolidated total 3,958.46 million yen, dispersing the earnings pillars. In management, with “AI × New’S Design Studio” at the core, the Company has declared a “full AI shift,” clarifying a shift toward an “AI-driven company” that encompasses visualization of processes, work-efficiency gains via the in-house tool “SAKAE,” human resource development, and new product development. Furthermore, through its strategic partnership with U.S. firm Ballard Partners, the Company is establishing a framework for mutually providing PA/government relations support between Japan and the U.S., accelerating the integration of the capability to “create news” and the ability to “spread news.”

Key financial data

| Unit: million yen | 2020/12 | 2021/12 | 2022/12 | 2023/12 | 2024/12 | 2025/12 CE |

| Sales | 4,990 | 5,610 | 5,265 | 6,896 | 7,324 | 8,500 |

| EBIT (Operating Income) | 157 | 381 | 720 | 841 | 1,075 | 1,280 |

| Pretax Income | 70 | 288 | 768 | 862 | 1,034 | |

| Net Profit Attributable to Owner of Parent | 13 | 132 | 520 | 488 | 526 | 730 |

| Cash & Short-Term Investments | 1,531 | 1,943 | 2,318 | 2,691 | 3,260 | |

| Total assets | 3,068 | 3,572 | 5,044 | 5,428 | 5,810 | |

| Total Debt | 531 | 591 | 967 | 767 | 539 | |

| Net Debt | -1,000 | -1,352 | -1,351 | -1,925 | -2,721 | |

| Total liabilities | 1,254 | 1,630 | 2,267 | 2,097 | 1,921 | |

| Total Shareholders’ Equity | 1,814 | 1,942 | 2,595 | 3,090 | 3,553 | |

| Net Operating Cash Flow | 384 | 442 | 546 | 771 | 911 | |

| Capital Expenditure | 30 | 155 | 67 | 54 | 33 | |

| Net Investing Cash Flow | -102 | -26 | -397 | -35 | -37 | |

| Net Financing Cash Flow | 242 | 16 | 220 | -375 | -311 | |

| Free Cash Flow | 355 | 286 | 479 | 717 | 878 | |

| ROA (%) | 0.43 | 3.97 | 12.08 | 9.31 | 9.36 | |

| ROE (%) | 0.68 | 7.03 | 22.94 | 17.15 | 15.84 | |

| EPS (Yen) | 1.6 | 16.3 | 61.2 | 56.6 | 60.6 | 84.1 |

| BPS (Yen) | 229.8 | 236.1 | 299.5 | 356.7 | 408.2 | |

| Dividend per Share (Yen) | 6.00 | 7.00 | 8.00 | 10.00 | 12.00 | 14.00 |

| Shares Outstanding (Million shrs) | 8.18 | 8.64 | 8.74 | 8.78 | 8.79 |

Source: Omega Investment from company data, rounded to the nearest whole number.

Share price

Key stock price data

Financial data (quarterly basis)

| Unit: million yen | 2023/12 | 2024/12 | 2025/12 | ||||||

| 2Q | 3Q | 4Q | 1Q | 2Q | 3Q | 4Q | 1Q | 2Q | |

| (Income Statement) | |||||||||

| Sales | 1,615 | 1,689 | 1,943 | 1,788 | 1,779 | 1,716 | 2,041 | 2,037 | 1,922 |

| Year-on-year | 43.3% | 21.3% | 16.8% | 8.4% | 10.2% | 1.6% | 5.0% | 13.9% | 8.0% |

| Cost of Goods Sold (COGS) | 903 | 956 | 1,128 | 972 | 966 | 925 | 1,147 | 1,108 | 1,077 |

| Gross Income | 712 | 734 | 815 | 816 | 814 | 791 | 894 | 929 | 845 |

| Gross Income Margin | 44.1% | 43.4% | 42.0% | 45.6% | 45.7% | 46.1% | 43.8% | 45.6% | 44.0% |

| SG&A Expense | 532 | 540 | 616 | 519 | 545 | 530 | 646 | 560 | 581 |

| EBIT (Operating Income) | 180 | 194 | 200 | 297 | 269 | 261 | 248 | 369 | 264 |

| Year-on-year | -7.1% | 26.6% | 45.6% | 11.2% | 49.2% | 34.4% | 24.4% | 24.1% | -1.7% |

| Operating Income Margin | 11.2% | 11.5% | 10.3% | 16.6% | 15.1% | 15.2% | 12.2% | 18.1% | 13.7% |

| EBITDA | 235 | 251 | 254 | 349 | 319 | 312 | 298 | 414 | 311 |

| Pretax Income | 189 | 202 | 206 | 277 | 271 | 230 | 256 | 366 | 260 |

| Consolidated Net Income | 108 | 126 | 152 | 147 | 177 | 147 | 150 | 244 | 167 |

| Minority Interest | 9 | 19 | 15 | 31 | 28 | 26 | 10 | 28 | 27 |

| Net Income ATOP | 99 | 106 | 137 | 116 | 148 | 121 | 141 | 215 | 140 |

| Year-on-year | -45.5% | 24.1% | 39.3% | -19.5% | 49.1% | 13.6% | 2.5% | 85.1% | -5.6% |

| Net Income Margin | 6.2% | 6.3% | 7.1% | 6.5% | 8.3% | 7.0% | 6.9% | 10.6% | 7.3% |

| (Balance Sheet) | |||||||||

| Cash & Short-Term Investments | 2,310 | 2,327 | 2,691 | 2,657 | 2,980 | 2,946 | 3,260 | 3,115 | 3,422 |

| Total assets | 4,940 | 4,905 | 5,428 | 5,286 | 5,448 | 5,342 | 5,810 | 5,598 | 5,871 |

| Total Debt | 885 | 826 | 767 | 707 | 647 | 586 | 539 | 490 | 445 |

| Net Debt | -1,426 | -1,500 | -1,925 | -1,950 | -2,333 | -2,360 | -2,721 | -2,625 | -2,977 |

| Total liabilities | 1,945 | 1,771 | 2,097 | 1,885 | 1,855 | 1,615 | 1,921 | 1,704 | 1,782 |

| Total Sharehjolders’ Equity | 2,788 | 2,908 | 3,090 | 3,129 | 3,293 | 3,401 | 3,553 | 3,617 | 3,786 |

| (Profitability %) | |||||||||

| ROA | 8.53 | 9.03 | 9.31 | 9.12 | 9.79 | 10.20 | 9.36 | 11.49 | 10.90 |

| ROE | 16.43 | 16.52 | 17.15 | 15.92 | 16.72 | 16.57 | 15.84 | 18.54 | 17.43 |

| (Per-share) Unit: JPY | |||||||||

| EPS | 11.5 | 12.3 | 15.9 | 13.4 | 17.1 | 13.9 | 16.2 | 24.7 | 16.0 |

| BPS | 323.6 | 337.0 | 356.7 | 361.1 | 379.0 | 391.4 | 408.2 | 415.5 | 433.6 |

| Dividend per Share | 0.00 | 0.00 | 10.00 | 0.00 | 0.00 | 0.00 | 12.00 | 0.00 | 0.00 |

| Shares Outstanding(million shrs) | 8.75 | 8.75 | 8.78 | 8.79 | 8.79 | 8.79 | 8.79 | 8.81 | 8.81 |

Source: Omega Investment from company materials

Financial data (full-year basis)

| Unit: million yen | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 |

| (Income Statement) | |||||||||||

| Sales | 4,063 | 3,705 | 4,100 | 4,379 | 5,318 | 5,758 | 4,990 | 5,610 | 5,265 | 6,896 | 7,324 |

| Year-on-year | 1.1% | -8.8% | 10.7% | 6.8% | 21.4% | 8.3% | -13.3% | 12.4% | -6.1% | 31.0% | 6.2% |

| Cost of Goods Sold | 2,223 | 1,385 | 1,703 | 1,822 | 2,546 | 2,879 | 2,367 | 2,614 | 2,843 | 3,894 | 4,010 |

| Gross Income | 1,840 | 2,320 | 2,396 | 2,558 | 2,772 | 2,879 | 2,623 | 2,996 | 2,422 | 3,002 | 3,314 |

| Gross Income Margin | 45.3% | 62.6% | 58.5% | 58.4% | 52.1% | 50.0% | 52.6% | 53.4% | 46.0% | 43.5% | 45.3% |

| SG&A Expense | 569 | 597 | 2,216 | 2,293 | 2,324 | 2,374 | 2,456 | 2,597 | 1,685 | 2,147 | 2,225 |

| EBIT (Operating Income) | 1,271 | 1,723 | 180 | 265 | 444 | 502 | 157 | 381 | 720 | 841 | 1,075 |

| Year-on-year | -34.0% | 35.5% | -89.5% | 46.7% | 68.0% | 12.9% | -68.8% | 143.8% | 88.7% | 16.8% | 27.8% |

| Operating Income Margin | 31.3% | 46.5% | 4.4% | 6.0% | 8.4% | 8.7% | 3.1% | 6.8% | 13.7% | 12.2% | 14.7% |

| EBITDA | 1,282 | 1,733 | 195 | 284 | 468 | 534 | 202 | 447 | 857 | 1,059 | 1,279 |

| Pretax Income | -386 | 132 | 181 | 257 | 432 | 502 | 70 | 288 | 768 | 862 | 1,034 |

| Consolidated Net Income | -515 | 108 | 163 | 221 | 366 | 372 | 13 | 132 | 539 | 546 | 621 |

| Minority Interest | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 18 | 58 | 95 |

| Net Income ATOP | -515 | 108 | 163 | 221 | 366 | 372 | 13 | 132 | 520 | 488 | 526 |

| Year-on-year | 803.1% | -121.0% | 51.2% | 35.3% | 65.8% | 1.5% | -96.6% | 943.0% | 294.4% | -6.3% | 7.9% |

| Net Income Margin | -12.7% | 2.9% | 4.0% | 5.0% | 6.9% | 6.5% | 0.3% | 2.4% | 9.9% | 7.1% | 7.2% |

| (Balance Sheet) | |||||||||||

| Cash & Short-Term Investments | 851 | 473 | 611 | 659 | 1,012 | 1,032 | 1,531 | 1,943 | 2,318 | 2,691 | 3,260 |

| Total assets | 2,408 | 2,247 | 1,784 | 2,113 | 2,637 | 2,831 | 3,068 | 3,572 | 5,044 | 5,428 | 5,810 |

| Total Debt | 478 | 402 | 462 | 390 | 280 | 163 | 531 | 591 | 967 | 767 | 539 |

| Net Debt | -373 | -71 | -149 | -269 | -732 | -869 | -1,000 | -1,352 | -1,351 | -1,925 | -2,721 |

| Total liabilities | 1,910 | 1,622 | 1,003 | 1,105 | 1,109 | 930 | 1,254 | 1,630 | 2,267 | 2,097 | 1,921 |

| Total Sharehjolders’ Equity | 498 | 625 | 782 | 1,008 | 1,528 | 1,901 | 1,814 | 1,942 | 2,595 | 3,090 | 3,553 |

| (Cash Flow) | |||||||||||

| Net Operating Cash Flow | 76 | -260 | 125 | 152 | 437 | 274 | 384 | 442 | 546 | 771 | 911 |

| Capital Expenditure | 9 | 8 | 13 | 9 | 15 | 36 | 30 | 155 | 67 | 54 | 33 |

| Net Investing Cash Flow | 8 | -68 | -16 | -15 | -131 | -123 | -102 | -26 | -397 | -35 | -37 |

| Net Financing Cash Flow | 68 | -79 | 31 | -89 | 47 | -132 | 242 | 16 | 220 | -375 | -311 |

| Free Cash Flow | 67 | -264 | 112 | 144 | 422 | 238 | 355 | 286 | 479 | 717 | 878 |

| (Profitability %) | |||||||||||

| ROA | -22.91 | 4.64 | 8.11 | 11.34 | 15.43 | 13.60 | 0.43 | 3.97 | 12.08 | 9.31 | 9.36 |

| ROE | -69.43 | 19.25 | 23.24 | 24.69 | 28.89 | 21.69 | 0.68 | 7.03 | 22.94 | 17.15 | 15.84 |

| Net Margin | -12.68 | 2.92 | 3.99 | 5.05 | 6.89 | 6.46 | 0.25 | 2.35 | 9.89 | 7.07 | 7.18 |

| Asset Turn | 1.81 | 1.59 | 2.03 | 2.25 | 2.24 | 2.11 | 1.69 | 1.69 | 1.22 | 1.32 | 1.30 |

| Assets/Equity | 3.03 | 4.15 | 2.87 | 2.18 | 1.87 | 1.59 | 1.59 | 1.77 | 1.90 | 1.84 | 1.69 |

| (Per-share) Unit: JPY | |||||||||||

| EPS | -69.9 | 14.7 | 22.2 | 30.0 | 46.6 | 46.6 | 1.6 | 16.3 | 61.2 | 56.6 | 60.6 |

| BPS | 67.5 | 84.7 | 106.0 | 136.7 | 191.9 | 237.9 | 229.8 | 236.1 | 299.5 | 356.7 | 408.2 |

| Dividend per Share | 0.00 | 0.00 | 0.00 | 0.00 | 2.50 | 5.00 | 6.00 | 7.00 | 8.00 | 10.00 | 12.00 |

| Shares Outstanding(million shrs) | 7.56 | 7.56 | 7.56 | 7.56 | 8.15 | 8.17 | 8.18 | 8.64 | 8.74 | 8.78 | 8.79 |

Source: Omega Investment from company materials