2026-04-06

Home

Japanese

Omega Investment Co., Ltd.

Mitsubishi Electric (Price Discovery)

Hold

Conclusion

Hold. The recent share price has incorporated the effectiveness of the structural reform and the tailwinds in infrastructure and defence, and, with the progress in remediation of quality-related inappropriate conduct and governance reform, it has also incorporated that the uncertainty of additional costs and order deterioration has receded, reaching a high valuation of forecast PER 33x and trailing PBR 2.76x. The effective upward revision and upside in fixed-cost reductions are certainly positive, but there is a high likelihood that the current share price exceeds the theoretical fair value. Until medium-term growth expectations are further confirmed, holding is more appropriate than making new purchases.

Profile

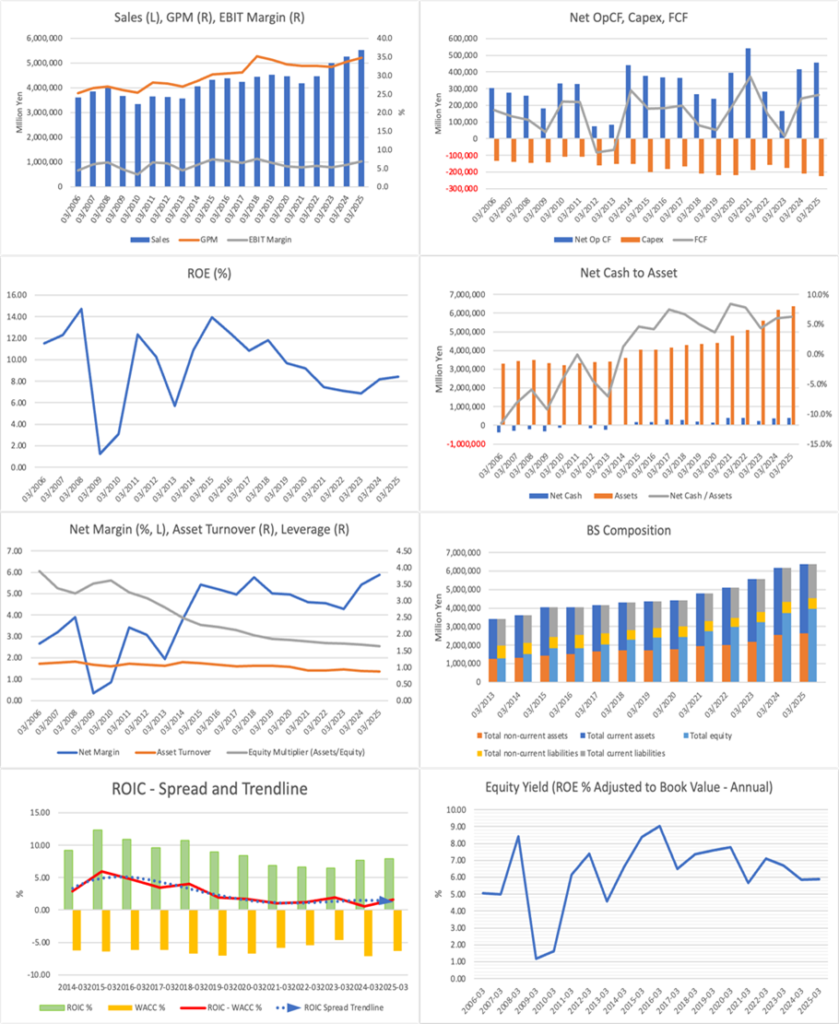

Mitsubishi Electric is a diversified electrical manufacturer engaged broadly in infrastructure, factory automation, mobility, life, semiconductors and devices, and other areas. The current investor assessment is formed by the combination of 1 the firmness of demand in infrastructure areas such as social, energy, and data centres, 2 the expansion of projects in the defence and space area, 3 reductions in fixed costs and improvement in profit margins through structural reform, and 4 reduced risk following responses to governance and quality issues. In 3Q, while recording costs for voluntary retirement, operating profit excluding the cost impact reached a record-high level, confirming an uplift in earnings power.

Sales composition by business, % (operating profit margin, %): Infrastructure 22 (7), Industry Mobility 29 (5), Life 39 (7), Business Platform 2 (7), Semiconductors & Devices 5 (14), Others 3 (6), Overseas 51 <FY3/2025>

| Securities Code |

| TYO:6503 |

| Market Capitalization |

| 12,501,700 million yen |

| Industry |

| Electronic equipment |

Stock Hunter’s View

FY3/2026 is effectively an upward revision. Infrastructure is robust, and growth potential increases as fixed costs decline.

Mitsubishi Electric is expected to deliver structural reform effects exceeding initial assumptions, and steady earnings growth from the next fiscal year onward appears likely.

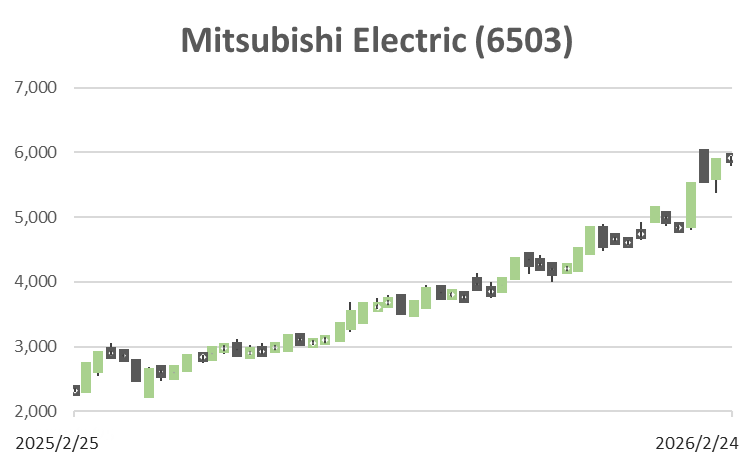

The FY3/2026 third-quarter results for April to December, announced on 3 February, were revenue of 4,156.01 billion yen, up 3.9 percent year on year, and operating profit of 294.757 billion yen, down 2.9 percent. The decline in operating profit was driven by the recognition of 74.3 billion yen in voluntary retirement expenses; operating profit excluding this impact was 369.0 billion yen, up 21.6 percent, thereby renewing the record high.

For the full-year forecast, reflecting strong performance in the infrastructure segment and the FA systems business, and a revision to foreign exchange assumptions, revenue was revised upward to 5,760.0 billion yen, up 4.3 percent from the previous fiscal year and 90.0 billion yen above the previous forecast. On the other hand, operating profit was revised downward to 400.0 billion yen, down 2.1 percent, which is 30.0 billion yen below the previous forecast, because the company brought forward voluntary retirement expenses for subsidiaries that had been assumed from the next fiscal year onward, causing the related expenses to expand from the initially assumed 60.0 billion yen to 100.0 billion yen. Operating profit excluding this impact is 500.0 billion yen, up 27.6 percent, representing an effective upward revision.

In this voluntary retirement programme, about 4,700 people across the group are expected to apply. The fixed-cost reduction effect from FY3/2027 onward, due to headcount reductions, is expected to increase from the previously expected about 20.0 billion yen to about 50.0 billion yen. Earnings power has strengthened, and the market is raising its assessment of medium-term growth potential.

Investor’s View

Hold. The share price already reflects not only high sustainable growth but also the receding uncertainty stemming from remediation of quality-related inappropriate conduct and progress in governance reform. The short-term upside is likely to be limited unless additional positive catalysts become visible.

Investor assessment has shifted from restoring trust to assessing sustainable growth centred on structural reform and tailwind businesses.

The share price increase over the past four years is difficult to explain solely by the business cycle, and the valuation premises have changed significantly. In addition to the shrinkage in the discount previously incorporated as responses progressed following the quality misconduct issue, the presence of tailwind areas such as power and social infrastructure, data centre-related businesses, and defence and space has been increasingly emphasized, leading to renewed recognition of the earnings areas. Furthermore, the effects of structural reform centred on fixed-cost reductions are evident in the figures, strengthening the view of the sustainability of profit-margin improvement. While voluntary retirement expenses recorded in 3Q reduced reported profit in the short term, the fact that operating profit excluding the cost impact reached a record high indicates an improvement in earnings power.

Actual EPS has grown at an annual rate of about 15 percent over the past five fiscal years, and the market is valuing the company on the assumption that earnings growth of around 20 percent will continue next fiscal year.

However, the past growth is driven more by a jump in the most recent two fiscal years than by annual accumulation. If measuring underlying growth capacity in normal conditions, it is natural to set a more modest growth rate as the reference. Even so, the current valuation assumes the recent upside is not one-off and that earnings growth will continue from next fiscal year onward, supported by improvements in the earnings structure through structural reform and the strength of tailwind businesses. The core of the valuation is whether the jump in profit is sustainable and will continue to accumulate; if it is not, the quality of expectations is likely to deteriorate.

The median fair share price is approximately 4,600 yen, with a range of 3,050 to 6,900 yen; the current share price exceeds the median.

Current market data indicate a share price of 5,625 yen, PER about 32x, PBR about 2.77x, and a forecast dividend of 55 yen. If the assumptions are aligned through dividend discounting and the clean surplus relationship, and then inverted, the market’s long-term EPS growth rate is approximately 7 percent. Under this assumption, if the cost of equity is set at 7.5-8.5 percent, the fair share price based on DCF, PER, and PBR falls within a broadly similar range, with median and mean values within the range shown above. As long as the current share price exceeds this level, additional upside is expected only if uncertainty recedes and the cost of equity falls further, or if the view that growth of around 7 percent will be sustained over the long term is strengthened.

Financials and Valuations

Price

PBR (LTM)

PER (LTM)

ROE (LTM)

EPS (Actual)

BPS (LTM)