2026-04-06

Home

Japanese

Omega Investment Co., Ltd.

VRAIN Solution (Price Discovery)

Hold

Conclusion

Hold. The share price is already factoring in, to a meaningful extent, the scenario in which, in addition to the growth of AI systems for the manufacturing industry, repeat deployments are reproduced as a pipeline of projects, starting from implementation track records and expanding to multiple lines within the same customer and further to additional plants.

Profile

AI systems account for 83% of revenue, and the company aims to grow by deploying to additional lines and plants.

VRAIN Solution’s core business is the provision of AI solutions for the manufacturing industry, and it engages in the development and implementation of AI systems and DX consulting. The source of its competitive strength lies not only in its AI development capabilities but also in its ability to provide, as an integrated package, imaging devices such as cameras and inspection equipment (including control and eject mechanisms), and to handle, on a one-stop basis, implementation through to deployment on manufacturing lines. The essence of growth lies in leveraging results at customer companies to expand deployments to multiple lines within the same customer and, further, to additional plants, thereby accumulating project scale and depth of engagement. On the other hand, at present the company is prioritising the expansion of sites and strengthening hiring to remove supply constraints, and profits are therefore prone to short-term volatility. For investors, the key monitoring points are whether the accumulation of order backlog, the certainty of delivery, revenue recognition, and the progress of profit recovery are progressing simultaneously.

Revenue breakdown by business (%): AI systems 83, DX consulting 17 (FY2/2025)

| Securities Code |

| TYO:135A |

| Market Capitalization |

| 25,127 million yen |

| Industry |

| Information / Communication |

Stock Hunter’s View

An AI solution provider specialised in the manufacturing industry. Establishing a “winning pattern” for deployment across multiple lines and plants.

VRAIN Solution sells AI systems specialised in the manufacturing industry and provides DX consulting. Although it is a young company established in March 2020, the number of client companies has already exceeded 300. It has expanded its customer base in the food sector, as well as in materials industries such as metals and paper, and in the pharmaceutical field.

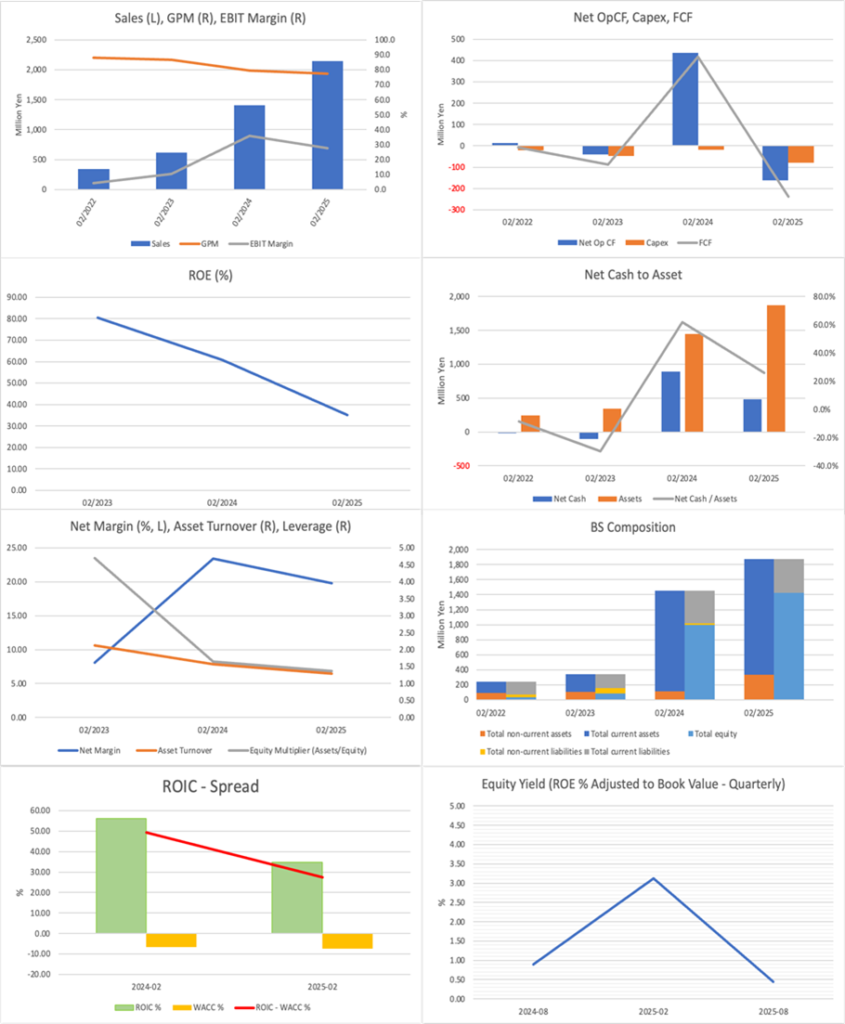

For FY2/2026, the company plans revenue of 3,215 million yen (up 50.0% YoY) and operating profit in a range of 890 million yen to 940 million yen (up 49.6% YoY to 58.0% YoY). Growth investments, site expansion,n and headcount increases came first, and the previously announced third-quarter results (March–November) showed an operating profit of 74 million yen (down 59.9% YoY). In addition, revenue was 1,628 million yen (up 35.7% YoY) and progress against the full-year forecast remains around 50%; however, the combined amount with the order backlog at the end of 3Q (1,262 million yen) covers 89.9% of the full-year forecast revenue, and when 4Q orders and expected orders are also taken into account, it appears to be an achievable level.

In its medium-term management policy, the company has set an aggressive revenue CAGR target of +50%; however, many of the current deployment track records are customers in the introduction phase to deployment across up to two lines, and the expansion phase to multiple products and multiple plants has yet to arrive. In the previous fiscal year, the operating track record of newly deployed AI systems was evaluated, and the company subsequently achieved a winning pattern, such as additional batch deployments across six plants.

Investor’s View

Hold. We will maintain existing holdings, but do not recommend additional new accumulation. The share price already reflects that the accumulation of order backlog will translate into revenue and that the company will transition smoothly from a phase of upfront investment to a phase of profit growth.

While FY2/2026 3Q cumulative revenue grew 1,628 million yen (YoY +35.7%), operating profit was 74 million yen (YoY -59.9%), a sharp decline, and growth investments have depressed short-term profitability. The company has set out a return to full-year revenue of 3,215 million yen and operating profit of 890–940 million yen and has disclosed an order backlog of 1,262 million yen as of the end of 3Q; however, what matters for investors is not whether demand exists, but whether that demand translates into delivery and revenue recognition, and whether profit margins recover at the same time.

In addition, the burden of working capital has become evident: cash and deposits totaled 74 million yen, and short-term borrowings totaled 400 million yen as of the end of 3Q. Low uncollectibility risk and the absorption of cash by working capital in a growth phase are different issues, and the stronger the growth continues, the more likely on-hand liquidity is to decline. Accordingly, from an investment action perspective, a cautious stance of remaining with continued shareholding is appropriate until it can be confirmed simultaneously that the order backlog is being worked through, 4Q orders are accumulating as revenue recognition, that the pace of SG&A increases is settling, and that concerns over funding ease.

The company can win on on-site deployment (operations), and growth will accelerate if additional deployments are replicated.

The attractiveness of VRAIN Solution’s business does not lie in AI as a technology theme itself, but in its ability to handle, as an integrated package, everything from requirements definition in manufacturing sites through to on-site deployment (operation) at plants, and to present results as operating track records. The company centres on AI visual inspection systems (Phoenix Vision/Eye), provides imaging devices and inspection equipment (including control and eject mechanisms) as an integrated package, and deploys and operates on-site automation of manufacturing lines. The focus of competitiveness is not software alone, but the ability to provide a one-stop offering in a form that can be deployed (operated) in manufacturing sites. What matters for investors is not the accumulation of initial deployments but whether, starting from deployment track records, additional deployments expand to multiple lines within the same customer and further to additional plants, and whether project scale and depth of engagement are reproduced as a pipeline of projects. When this holds, growth does not depend simplistically on the increase in the number of deployed customers, and the repetitiveness of additional deployments within customers improves the quality of growth.

Because the model does not rely on recurring revenue, timing slippage and working capital can become constraints on the share price.

On the other hand, the company’s risks are also clear. If it does not rely on recurring revenue, such as maintenance services at present, the stability of performance depends on the extent to which additional deployments after initial deployment repeat with a certain level of confidence, and quarterly numbers are strongly linked to progress from orders through delivery, inspection/acceptance, and revenue recognition. In projects involving on-site deployment (operations) at plants, revenue recognition can slip due to customer-driven specification changes, and profitability is also prone to temporary declines due to prior execution of growth investments. Furthermore, in a growth phase, working capital tends to absorb cash, and even if profits recover, the share price is likely to be capped if the visibility of cash does not catch up. Accordingly, what investors should evaluate is not the pace of revenue growth itself, but whether the reproducibility of additional deployments becomes visible as a pipeline of projects, and whether both profit margins and cash enter a recovery trajectory simultaneously.

Financials and Outlook

FY2/2026 3Q cumulative results were revenue of 1,628 million yen (YoY +35.7%) and operating profit of 74 million yen (YoY -59.9%). The company explains this against the backdrop of timing slippage caused by customer-driven specification changes and growth investments, such as site expansion and strengthened hiring. For the full year, it plans revenue of 3,215 million yen and operating profit of 890–940 million yen, and achievement depends less on the strength or weakness of demand than on the confidence with which the order backlog will fall into revenue recognition after delivery and acceptance inspection, and whether timing slippage remains limited.

The company has disclosed an order backlog of 1,262 million yen at the end of 3Q and explains its achievability on that basis. However, in a business involving on-site deployment (operation) at plants, the effectiveness of the supply side is questioned at the same time; therefore, this is a phase in which it should be verified on a quarterly basis whether strengthened hiring and site expansion function as an expansion of delivery capacity and whether profit margins return to a recovery trajectory.

Valuation

The current share price of 2,500 yen is on the upper end of the fair value range based on the three methods: PBR, DCF, and ROIC. The median of the medians of the three methods is approximately 1,290 yen, and the difference from the current share price is large. However, valuation sensitivity is high, and the conclusion is prone to change depending on whether the full-year plan is achieved and on the view regarding the subsequent duration of growth and profitability.

PBR yields approximately 760–2,580 yen (median approximately 1,210 yen), DCF yields approximately 1,430–3,180 yen (median approximately 2,130 yen), and ROIC yields approximately 980–1,800 yen (median approximately 1,290 yen), resulting in a wide integrated range of approximately 760–3,180 yen. To justify the current level, in addition to achieving the full-year plan, it is necessary that profit recovery is shown in a sustainable form rather than as a one-off, and that the increase in working capital subsides and concerns over funding ease.

Ownership

The shareholder structure is: insiders 72.64%, institutional investors 5.29%, and free float 27.4%. A structure in which major shareholders have a strong influence makes it easier to make long-term decisions, such as site and human capital investments, and it underpins long-term execution capability by strengthening the alignment of interests between management and shareholders. On the other hand, because the free float is small, supply and demand can become tight, and changes in expectations tend to be reflected excessively in the share price. In situations where plan underachievement or timing slippage becomes evident, it can also accelerate a decline.

Issues investors should confirm

For the time being, verification focuses on whether the order backlog is being worked through and 4Q orders are accumulating as revenue recognition proceeds, and whether the pace of SG&A increases is stabilizing. Profit margins are regaining a recovery trend, and whether the expansion of working capital subsides and funding becomes stable. If these are satisfied simultaneously, the high valuation can be maintained; however, if any of them breaks down, valuation adjustment is likely to become sharp, compounded by the thinness of supply and demand. Therefore, at this time, while maintaining existing holdings as the base case, a flexible risk-management stance is required in line with the progress of the verification items.

Financials and Valuations

Price

PBR (LTM)

PER (LTM)

ROE (LTM)

EPS (Actual)