2026-03-30

Home

Japanese

Omega Investment Co., Ltd.

Fuji Electric (Price Discovery)

Overvalued

Conclusion

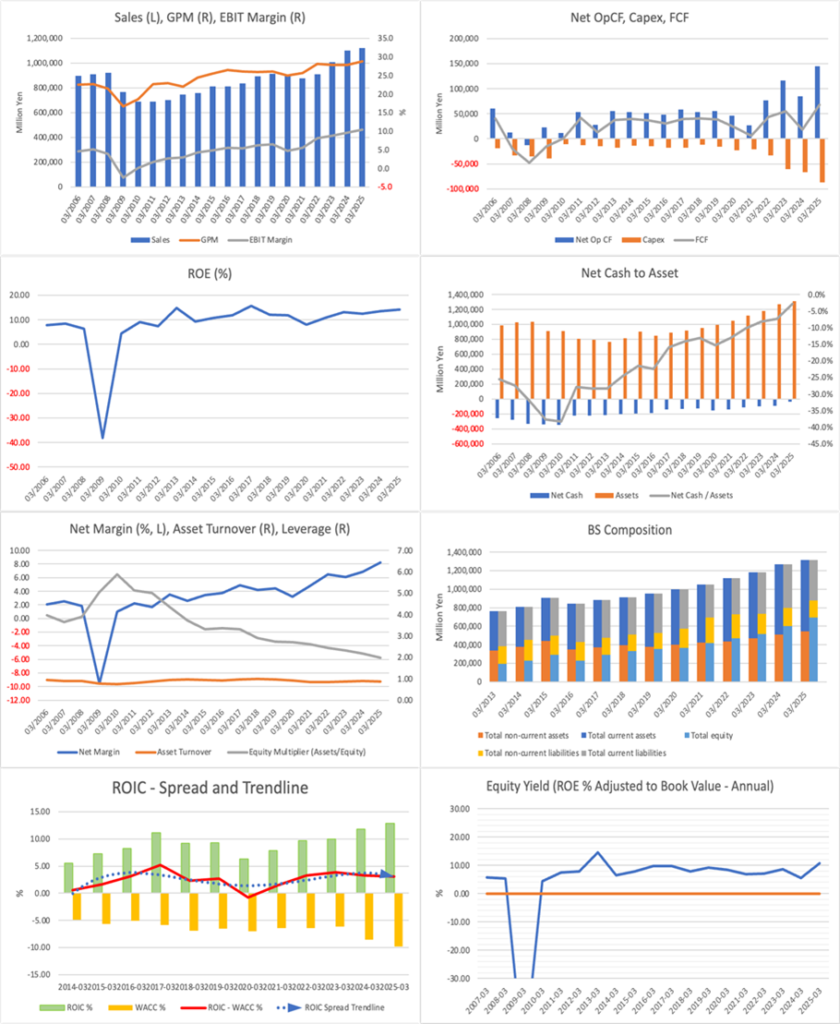

Overvalued. Fuji Electric’s long-standing improvement in EBIT margin since FY2009 has been impressive, and, in light of its ROE of around 10%, steadily growing top line, and decent cash flow, the company’s quality is highly rated. However, the current share price goes beyond assessing this stable earnings structure. It already reflects, to a considerable extent, the assumption that growth in energy, power-supply equipment for data centres, power-receiving and distribution equipment, and semiconductors will remain high going forward. The business quality is high, but the share price is even more bullish.

Profile

A comprehensive electrical equipment and heavy electrical machinery manufacturer centred on energy, industry, and semiconductors.

Fuji Electric is a comprehensive electrical equipment and heavy electrical machinery company, with power semiconductors, power receiving and distribution equipment, power generation and energy management, and industrial automation at its core. In recent years, it has steadily improved profitability, mainly through its Energy and Industry segments. In particular, the external environment, including decarbonisation investment, renewal of power infrastructure, advancement of capital investment, and demand for power supplies for data centres, has been a tailwind for the company. At the same time, semiconductors also support corporate value as a high-margin source of earnings. From a long-term perspective, the company is not merely a cyclical stock, but one that has improved its earnings structure while capturing structural demand.

Sales composition by business % (operating margin %): Energy 31 (9), Industry 35 (9), Semiconductors 21 (16), Food & Beverage Distribution 10 (12), Others 3 (7) Overseas 29 (FY3/2025)

| Securities Code |

|

TYO:6504 |

| Market Capitalization |

| 1,680,338 million yen |

| Industry |

| Electronic equipment |

Stock Hunter’s View

Strength continues in energy-related fields. Growth expected for power equipment for DCs.

Fuji Electric is Japan’s fourth-largest heavy electrical machinery company, with strength in power semiconductor technology. At present, the Energy segment (power generation plants, energy management, substation systems, facility and power supply systems, equipment construction) and the Industry segment (automation, social solutions, DX solutions, service solutions, IT solutions) are driving the company.

Operating profit for FY3/2026 is expected to reach 128.5 billion yen, up 9.2% YoY, marking a new record high. In the Energy segment, large-scale hydroelectric power equipment projects contributed, while energy storage systems and substation equipment for electric power and industrial applications drove the segment overall. Power supply systems for data centres (DCs) also continue to perform strongly. In the Industry segment, large-scale projects in the education sector associated with the GIGA School concept increased, while in Social Solutions, demand increased in the railway vehicle sector (transportation systems).

It should also be noted that earnings tend to be weighted toward 4Q (January to March). Strength in energy-related fields is expected to continue, and growth expectations are particularly high over the medium to long term for DC-related operations, including the announcement of entry into the US market.

Investor’s View

Overvalued. Long-term stable growth and capital profitability are highly rated, but the share price is above fair value.

What should first be recognised in the investment case for Fuji Electric is the quality of the company itself. The fact that improvement in EBIT margin has continued over a long period since FY2009 cannot be fully explained by cyclical tailwinds alone and indicates that improvements in the business portfolio, thorough profit management, and resource allocation to growth areas have worked to a reasonable degree. Although the ROIC/WACC margin still leaves something to be desired, the company has maintained an ROE of around 10% over a long period, continued to deliver steady top-line growth, and generated decent cash flow, meaning that its fundamental corporate strength is sufficiently high. It is not an outstandingly flamboyant company, but its essential strength lies in having remained a very good company over a long period.

Against that backdrop, from an equity investment perspective, the current issue is not the company’s quality, but how far the share price has moved ahead of that quality. At present, Fuji Electric’s core earnings base of energy, industry, and semiconductors each has a certain degree of credibility, and areas such as energy-related fields, power receiving and distribution equipment, and power supply equipment for data centres are particularly easy to associate with medium- to long-term growth expectations. Even so, the current share price appears to have already moved beyond the stage of valuing such growth opportunities and is premised on that growth continuing for a long time at quite a high level.

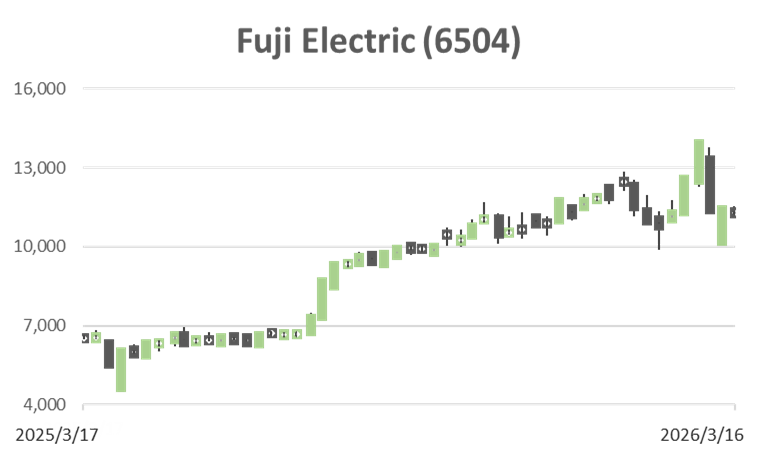

In fact, fair value based on the three methods of PBR, DCF, and ROIC is roughly in the range of 6,100 yen to 11,300 yen, with a median of about 9,300 yen. Against this, the current share price is in the low 11,000-yen range, placing it near the upper end of the fair value range, or slightly above it. Under the PBR method, the central value is about 9,300 yen; under the DCF method, about 10,400 yen; and under the ROIC method, about 7,700 yen. Although the methods differ in perspective, the conclusion common to all of them is that the current share price already reflects fairly strong assumptions. Long-term stable growth and capital profitability are fully satisfactory. Still, the share price should be regarded as having moved beyond properly valuing that quality and as already discounting a considerable degree of optimism.

Furthermore, Fuji Electric’s strength lies not in the explosive growth potential of a rapidly expanding emerging growth company, but in the fact that it has improved profitability over a long period while being rooted in relatively stable areas of demand. In that sense, the company’s genuine attraction lies in its steadiness. Even so, the current share price appears to reflect not only an assessment of that steadiness but also a fairly optimistic assumption that multiple tailwinds, including data centres, renewal of power infrastructure, GX, and semiconductor demand, will continue simultaneously for an extended period. The company’s quality and the share price’s bullish valuation should be considered separately. While Fuji Electric can be highly evaluated in the former respect, it is in a phase where the latter should clearly be viewed strictly.

Accordingly, the conclusion is clear. Fuji Electric is a company that fully deserves credit for long-term stable growth, continued improvement in profitability, an ROE of around 10%, and decent cash flow. However, the current share price has moved beyond a level that merely reflects that it deserves such credit and is already discounting, to a considerable extent, the continued persistence of high-quality growth. The company’s quality can be affirmed, but the share price is above fair value. The investment judgement should therefore be Overvalued.

Financials and Valuations

Price

PBR (LTM)

PER (LTM)

ROE (LTM)

EPS (Actual)

BPS (LTM)