2026-04-06

Home

Japanese

Omega Investment Co., Ltd.

TRIAL Holdings (Price Discovery)

Weak Hold

Conclusion

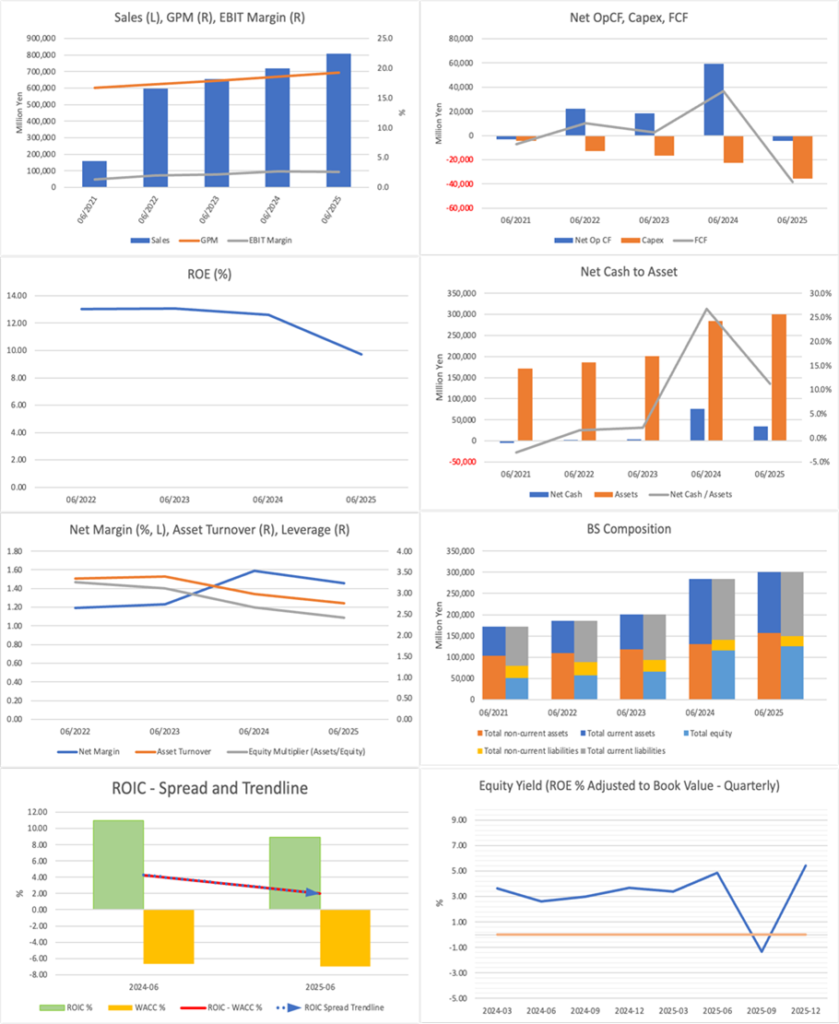

Weak Hold. PMI, following the acquisition of Seiyu, has made a good start, and results for the first half of FY06/2026 exceeded plan, with net sales of 674,117 million yen and operating profit of 16,677 million yen. Initial results of the integration are clearly visible, including increased customer traffic at existing stores, greater use of PB products and prepared foods, and a stronger price appeal. At the same time, the equity ratio declined from 42.0% to 15.1%, goodwill increased to approximately 298.8 billion yen, and short-term borrowings rose to 367.4 billion yen, indicating that the financial structure after the acquisition has become fundamentally different. The medium-term management plan’s target ROE of 16.5% for FY06/2029 is attractive, but the projected operating margin remains only 3.9%, and achieving the target ROE presupposes both high leverage and the completion of PMI. At this point, while the steady progress in the first half deserves recognition, it is somewhat too early to turn bullish without first seeing the first 12-month financial results after the acquisition.

Profile

A Kyushu-based discount retailer expands in one stroke into a nationwide group with sales exceeding 1 trillion yen through the acquisition of Seiyu

Trial Holdings is a Kyushu-based discount retail company, and through the full acquisition of Seiyu, it expanded in one stroke into a nationwide player. In its medium-term management plan, the company targets net sales of 1.6 trillion yen and operating profit of 64.0 billion yen in FY06/2029, but the focus of the investment case is not scale expansion itself, but whether it can achieve an improvement in gross profit margin, a decline in the SG&A ratio, and stronger cash generation through PMI. The acquisition of Seiyu has drastically changed the company’s scale, but what will determine the stock’s valuation is how firmly normalized earnings power after the acquisition can take hold.

Net sales composition by business (%) (operating margin %): Distribution/Retail 100 (3), Other 0 (9) (FY06/2025)

| Securities Code |

|

TYO:141A |

| Market Capitalization |

| 491,483 million yen |

| Industry |

| Retail trade |

Stock Hunter’s View

The acquisition of Seiyu and integration effects are emerging. Expectations for upside to the full-year results are high.

Trial Holdings is a Kyushu-based discount store operator. With the acquisition of Seiyu in July last year, it became a nationwide player, and, combined, the two companies now have net sales of 1.2 trillion yen, placing them behind Seven & i Holdings and Aeon in the food retail industry. At present, integration with Seiyu is progressing smoothly, and customer traffic at existing stores is showing a recovery trend as pricing measures bear fruit.

The second-quarter results for the current fiscal year ending June (July-December), announced in February, significantly exceeded plan, with net sales of 674,117 million yen (up 67% year on year and 9.9 billion yen above the first-half plan) and operating profit of 16,677 million yen (up 71.9% year on year and 6.27 billion yen above plan). Progress was made in pricing, the mutual use of prepared foods and private-brand products, and cost control. Through measures such as the introduction of “Exciting Price,” the company succeeded in raising gross profit by balancing customer-drawing power with price-appealing products and earnings power with value-appealing products.

In the second half, upfront investment expenses are expected to arise, including aggressive store openings and the rebuilding of Seiyu’s existing stores. On the other hand, the effects of improved purchasing terms from the integration of procurement channels are also expected to emerge. Although the full-year plan has been left unchanged at this point, upside is anticipated. Against the backdrop of rising prices, demand for low-priced food supermarkets is increasing, and the company can continue to attract attention as a defensive stock.

Investor’s View

The shares are discounting the likelihood of a successful integration in advance, and the investment attraction at this point is limited.

The company plans to target a net sales CAGR of +7% over the next three years, but an operating margin of 3.9% in FY06/2029 is not necessarily attractive. On the other hand, the target ROE of 16.5% does look attractive. However, compared with the period before the acquisition of Seiyu, this level presupposes a substantial use of financial leverage, and it would be difficult for investors to be fully convinced at this point. To calculate a more reliable fair value, there is no need to rely hastily on the figures presented in the company’s medium-term management plan; it is not too late to first confirm the financial figures in the 12-month results for FY06/2026.

What the market is looking at is not this fiscal year’s EPS, but normalized earnings after the integration.

Under the company’s plan for FY06/2026, against net sales of 1,322,500 million yen and operating profit of 25,400 million yen, net profit attributable to owners of parent is only 500 million yen, and EPS remains at 4.09 yen. On the other hand, EPS before goodwill amortization is 128.37 yen, and the way accounting profit is presented differs greatly from the way underlying earnings power is presented. Even in the interim period, interim net profit per share before goodwill amortization was 95.82 yen, whereas on a standard basis it remained only 33.17 yen. In the first half, approximately 7.6 billion yen of goodwill amortization and approximately 1.8 billion yen of interest expense related to M&A financing were recorded. The current stock price should be viewed as pricing in, ahead of time, normalized earnings after these acquisition-related burdens have passed through, rather than looking at the current period’s accounting profit.

What is being priced in is not so much an expectation of high growth as an expectation of a recovery in profitability.

Working backward from the set of indicators of forecast PER of 33.6x, forecast EPS of 39.1 yen, and forecast dividend of 16 yen, the implied stock price is approximately 1,314 yen. On this assumption, the dividend yield is approximately 1.2%, and if the required return is set at around 8%, the Emarket’s implied PS growth rate is approximately 6-7% annually. Judging from the numbers alone, this is not an extreme expectation of high growth. But the actual medium-term management plan calls for a net sales CAGR of 7.2% and an operating profit CAGR of 36.1% through FY06/2029, and the focus lies not on net sales growth itself, but on the recovery in profit margin through improvement in gross profit margin and a decline in the SG&A ratio through PMI. In other words, what the market is valuing is not the dream of a high-growth stock, but a scenario in which the profitability that declined after the integration of Seiyu steadily returns. The issue is that the stock price appears somewhat optimistic relative to the probability of that scenario occurring.

The point of the medium-term management plan is not net sales growth, but the recovery of capital efficiency.

The medium-term management plan targets net sales of 1.6 trillion yen, operating profit of 64.0 billion yen, EBITDA of 100.0 billion yen, and ROE of 16.5% in FY06/2029. Even so, the operating margin remains only 3.9%, and that alone does not make the company a highly profitable retailer. The company also positions these three years as “three years of building a foundation for distribution reform”. It explains that its primary mission is to steadily advance PMI at Seiyu and strengthen cash generation, with synergies at its core. Accordingly, the essence of this medium-term management plan lies not in the growth rate itself of the net sales CAGR of +7%, but in how far capital efficiency can be restored while carrying the heavy balance sheet after the integration. ROE of 16.5% is attractive, but at this stage, it remains a target, not proven earning power.

Initial results from PMI are certainly emerging.

First-half consolidated net sales were 674,117 million yen, and operating profit was 16,677 million yen, exceeding the company’s plan. The company says it aims to improve the gross profit margin in the second half as well through more sophisticated, data-driven pricing, stronger development and sales of prepared foods and PB products, and improved transaction terms through synergies with Seiyu. In addition, regarding sales at Seiyu’s existing stores, the company explained that strengthening price appeal, eliminating out-of-stocks in staple products, and creating Trial-style sales floors are leading to the return of customers who had drifted away and to the acquisition of new customers. At the same time, Seiyu’s gross profit margin in 2Q also included the temporary factor of an upside in December rebates. PMI is progressing smoothly, but it is still too early to regard all of the profit improvement as a sustained improvement in business quality.

Fair value is still viewed as below the current price.

The fair value at this point does not justify a level in the 4,000-yen range. Under the PBR method, even assuming normalized profit after the integration, the central value is around 3,000 yen, with a range of approximately 2,700-3,300 yen. Under the DCF method, although the 64.0 billion yen of operating profit in FY06/2029 is used as an upper reference value, growth investments and debt repayments must also be incorporated; therefore, the central value is slightly below 3,000 yen, with a range of approximately 2,500-3,400 yen. Under the ROIC method as well, the structure is one in which ROIC clearly exceeds WACC only after PMI succeeds, and the central value is around 3,200 yen, with a range of approximately 2,900-3,600 yen. The median of the three methods is approximately 3,050 yen, and the judgment is that the current stock price is above that level. The assumptions are conservative throughout and do not directly place the figures in the company’s medium-term management plan into present value.

The shareholder structure is a strength for management, but it has quirks for the stock.

The shareholder structure is a clear strength in a phase in which PMI is being advanced. By shareholder category, other domestic corporations account for 70.1%. Among the major shareholders, T.H.C. Co., Ltd. holds 53.93%, Heroic Investment Co., Ltd. holds 7.66%, and Hisao Nagata holds 1.91%. This stable shareholder structure, with a strong founding-family character, is a major asset in advancing a large-scale project such as the integration of Seiyu. This is because decisions can be pushed through without being swayed by short-term stock price movements. On the other hand, individuals and others account for only 15.5%, foreign corporations and others for 9.4%, and financial institutions for 2.8%, so the depth of liquidity is insufficient. It is a positive for management stability, but as a listed stock, it also tends to carry the negatives of being easily swayed by supply and demand and of market discipline from outside shareholders being less likely to function.

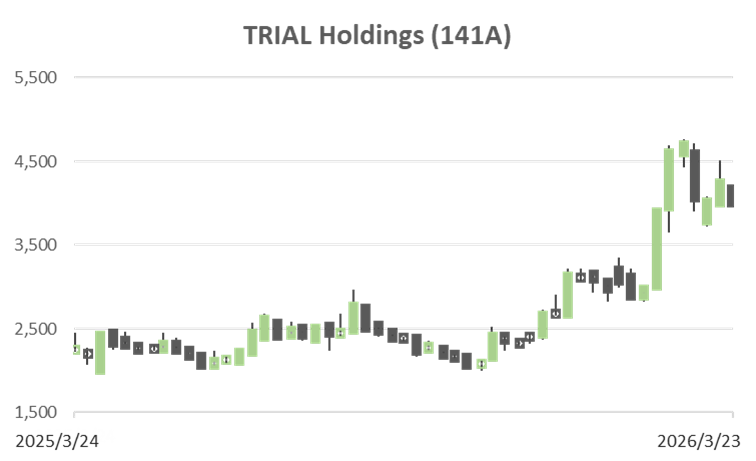

The stock price, which was weak last year, is strong this year because earnings have improved and the integration story has emerged at the same time.

The reason the stock price is strong this year is simple. First, first-half results exceeded plan in both net sales and operating profit, confirming that PMI is progressing more smoothly than expected. Second, the medium-term management plan presented target end points of 64.0 billion yen in operating profit, a ROE of 16.5%, and 100.0 billion yen in EBITDA in FY06/2029, making the post-acquisition form of the company visible. Third, by positioning PMI at Seiyu as the greatest mission, and by presenting favorable case studies such as the Hanakoganei store and a plan to convert 30 of approximately 70 stores into the “Trial Seiyu” format over three years, the market found it easier to buy into the story of the company as a leader in nationwide retail reorganization. Last year, the fading of expectations immediately after listing and the difficulty of seeing standalone growth were burdens, but this year, the axes of evaluation shifted because upside results and the presentation of a future vision coincided.

Financials and Valuations

Price

PBR (LTM)

PER (LTM)

ROE (LTM)

EPS (Actual)

BPS (LTM)