2026-03-23

Home

Japanese

Omega Investment Co., Ltd.

Daiei Kankyo (Price Discovery)

Weak Hold

Conclusion

Weak Hold. Daiei Kankyo is a high-quality environmental infrastructure company with high barriers to entry and capital efficiency, centred on final disposal sites. In FY3/2027, the full-year contribution from M&A, price optimisation, and improved profitability in soil treatment is highly likely to drive profit growth. Even so, the share price appears already to discount EPS growth of around 9% per annum. This is a level above the profit growth rate indicated in the company’s medium-term management plan, and the valuation already reflects a degree of anticipation. The strength of the business is acknowledged, but at the current share price level, continuing to hold is appropriate, and this is not a stage at which aggressive new buying should be recommended.

Profile

A high-profit environmental infrastructure company that operates resource circulation on an integrated basis, founded on final disposal sites

Daiei Kankyo is an environmental infrastructure company engaged consistently in the collection and transportation of industrial waste and general waste, intermediate treatment and recycling, and final disposal. The core of its business lies in its waste treatment and resource circulation business, which is based on final disposal sites with high barriers to entry and a wide-area network. By combining this with soil remediation, facility construction, operation and management, energy creation, forest conservation, and other functions, the company has established its position not as a mere waste processor but as a comprehensive operator supporting a circular society. In recent years, it has expanded both its business domains and geographical coverage through M&A, PPP, and the advancement of resource circulation, and it is characterised by possessing both continuity and scalability as a social infrastructure operator.

Net sales composition by business segment % (operating margin %): Environment-related 97 (28), Other 3 (-8) (FY3/2025)

| Securities Code |

| TYO:9336 |

| Market Capitalization |

| 396,075 million yen |

| Industry |

| Service |

Stock Hunter’s View

In FY3/2027, the full-year contribution from M&A will be realised. Price optimisation in existing businesses is also advancing.

Daiei Kankyo provides a one-stop service covering the collection and transportation of industrial waste and general waste, intermediate treatment and recycling, and final disposal. In addition, it is engaged broadly in a broad range of activities, including soil remediation, forest conservation, facility construction and operations management, and the valuable resource recycling business.

On 24 March, the company presented its full-year earnings forecast for FY3/2027, projecting net sales of 93.9 billion yen (up 11.9% YoY) and operating profit of 24.3 billion yen (up 11.4% YoY). This reflects expectations, including the start of operations of the controlled final disposal site at the Gobo Recycling Center from FY3/2026, the planned full-scale operation of the advanced plastic sorting facility of consolidated subsidiary DINS Kansai, and the earnings contribution of Scarab Sacre, which was made a consolidated subsidiary last November.

Although the forecast for the current fiscal year (4.6% revenue growth and 1.2% operating profit growth) was left unchanged, transportation-related costs are rising above the company’s assumptions, and there is a possibility that operating profit will come in slightly below plan. At the same time, price optimisation is gradually advancing in the waste treatment and resource circulation business, while in the soil treatment business, the company is proceeding with the acquisition of mainly high-margin, difficult-to-process projects. In October-December, intake volume increased 34% YoY, and net sales also rose sharply, up 54% YoY. The increase in waste intake volume and price rises in the waste treatment and resource circulation business are likely to affect FY3/2027 as well.

Investor’s View

Weak Hold. The strength of the business is acknowledged, but the share price has already moved ahead of the next phase of growth.

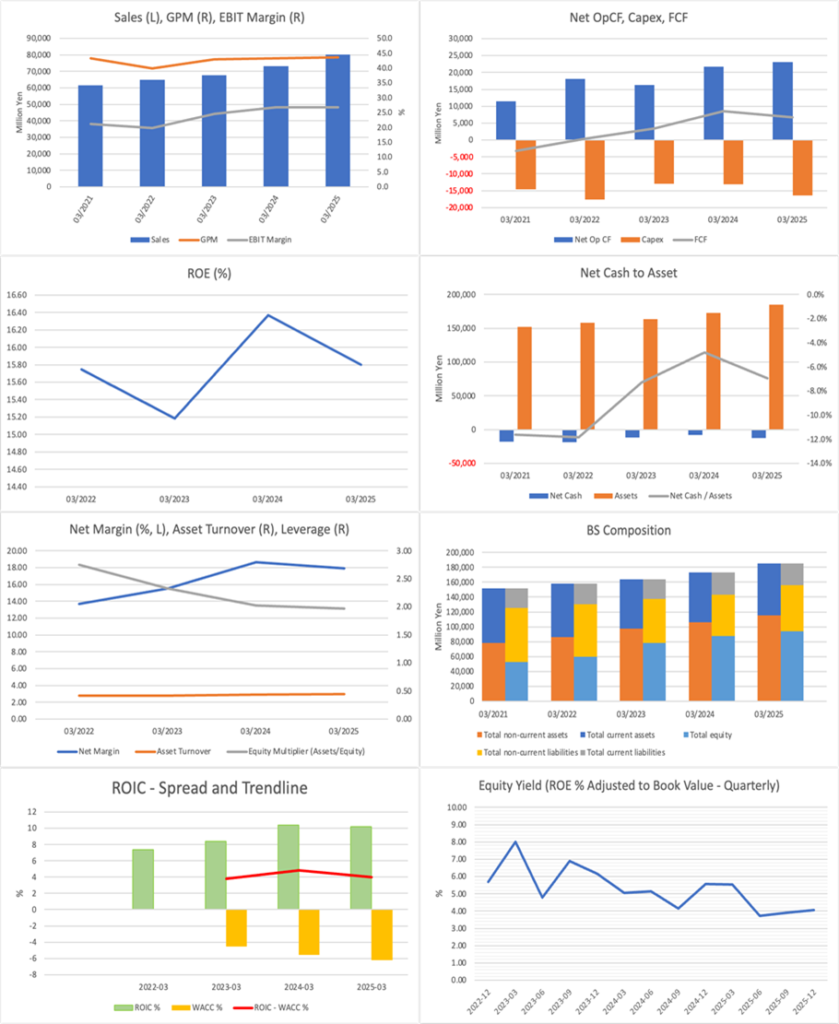

The starting point for assessing Daiei Kankyo is the strength of its business foundation. Its structure, which enables integrated operation centred on final disposal sites, covering collection and transportation, intermediate treatment, recycling, and final disposal, cannot easily be replicated, and its actual ROE of 15.8% and ROIC of 14.1% indicate that the company has combined high profitability with capital efficiency. In addition, in its medium-term management plan, the company targets net sales of 100.0 billion yen, operating profit of 25.0 billion yen, and EPS of 169.46 yen in FY3/2028. Nevertheless, it retains scope for expansion through M&A and organic growth. Its rarity as environment-related infrastructure and its position to capture the progress of a circular society are clear.

The current valuation already discounts growth above the company plan

On the other hand, the key issue from an investment perspective is not whether growth potential exists, but whether that growth can sustain the current valuation. Based on the indicators of a forecast PER of 27.3, an actual PBR of 3.76, a forecast ROE of 13.8%, a forecast EPS of 144.2 yen, and a forecast dividend of 49.5 yen, the medium-term EPS growth rate, discounted by the share price, is estimated at around 9% per annum. The actual EPS growth rate over the past three years exceeds this, but the EPS growth rate projected by the company’s medium-term management plan for the next three years is lower. In other words, the market is already assuming continued growth above the company plan. This is where the difficulty in valuing the current share price lies.

Re-rating requires a clear recovery in profitability.

Recent earnings remain high in absolute terms, but they do not yet contain enough to prompt a further re-rating. In the cumulative third quarter of FY3/2026, the company achieved revenue growth, but the operating margin declined, and higher costs, depreciation, and the burden of goodwill amortisation have become a weight on earnings. The equity ratio has also declined following the consolidation of Scarab Sacre, and the focus of future valuation will be on how the fruits of M&A are recovered in terms of both profit growth and capital efficiency. What matters is not mere revenue growth, but confirmation of a recovery in profitability through price optimisation and the accumulation of high-margin projects.

Growth drivers for FY3/2027 onward are visible.

Even so, the seeds of growth are clear. The start of operations for the second phase of Gobo RC, the full-scale operation of DINS Kansai’s advanced plastic-sorting facility, and the full-year contribution from Scarab Sacre are all directly linked to the expansion of processing capacity, area, and functions. In particular, securing remaining capacity at final disposal sites is directly related to the company’s competitive advantage, and its significance in strengthening the medium- to long-term earnings base is considerable. If price optimisation steadily penetrates and high-margin projects in the soil treatment business continue to grow, there remains scope for upside in profit growth from FY3/2027 onward.

The share price is above fair value estimates.

In comparison with fair value, the market’s view appears considerably optimistic. The central fair value indicated by the three methods of PBR, DCF, and ROIC is approximately 2,900 yen, and the current share price level is clearly above that range. The market is thus assigning a high valuation to the company’s advantages, but the issue ultimately comes down to whether the company can continue to demonstrate profit growth commensurate with that high valuation.

Ownership supports valuation but can amplify volatility.

The shareholder structure also has both strengths and weaknesses. A stable shareholder structure with a strong presence of the founder and related parties tends to underpin supply and demand in normal times and contribute to maintaining a high valuation. On the other hand, a structure with limited free float can make share price movements more unstable when the company fails to meet expected growth rates. The presence of overseas long-term funds can be viewed positively, but share price formation remains susceptible to liquidity constraints.

The key is whether the next phase of growth can justify the premium.

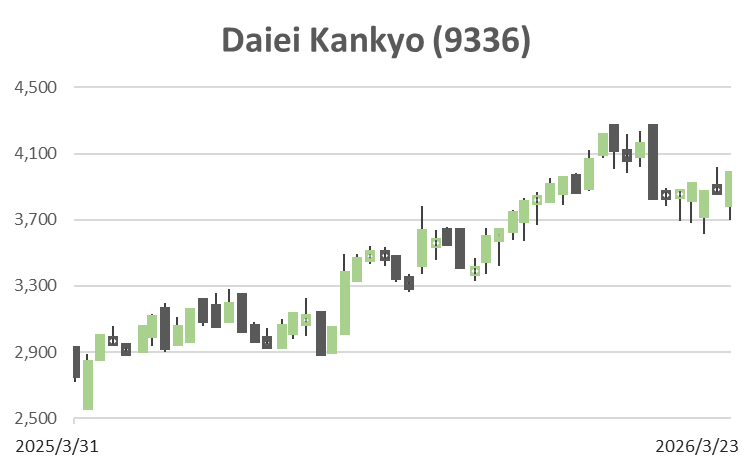

Since listing, the share price has risen substantially alongside earnings expansion, but what is being required at present is not confirmation of stable growth, but proof of the next phase of growth. If, in FY3/2027, the full-year contribution from M&A, price optimisation, and high-margin growth in the soil treatment business is clearly reflected in both operating profit and EPS, the current high valuation can be maintained. At present, while the strength of the business supports a hold stance, the upside sufficient to justify aggressive new buying is judged to be limited.

Financials and Valuations

Price

PBR (LTM)

PER (LTM)

ROE (LTM)

EPS (Actual)