2026-08-03

Home

Japanese

Omega Investment Co., Ltd.

WOLVES HAND (Price Discovery)

Sell on Strength

Conclusion

Sell on Strength. However, if high profit growth continues, post-M&A PMI takes hold in a disciplined manner, and the financial burden is reduced, the current share price level may still be justified and could also be valued in a higher range. WOLVES HAND is a rare animal healthcare group in Japan with a structure that provides everything from primary care to advanced medical care within a single company, the ability to train young veterinarians, and strengths as a recipient of business succession M&A. The quality of the business itself is high. In fact, in 1H FY6/2026, profit increased substantially, and the company also revised its full-year plan upward.

Nevertheless, the share price already reflects a fair degree of evaluation, and compared with the median fair value estimate, there is no significant sense of undervaluation. In addition, issues such as goodwill, dependence on M&A, a thin free float, and concerns over sales by major shareholders remain. Therefore, at this point, while recognising the merits of the business, we believe that profit-taking is appropriate in phases when the share price strengthens.

Profile

One of Japan’s largest animal hospital groups, providing everything from primary care to advanced medical care within a single company

WOLVES HAND is a comprehensive animal healthcare group centred on the operation of animal hospitals, while also having adjacent businesses such as pet salons, software for animal hospitals, and veterinary medical education content. Its greatest feature is that, rather than having primary care and secondary care divided as in the general industry structure, it can seamlessly provide everything from routine care to advanced medical care using CT, MRI and the like within the group. It has expanded its hospital network mainly in Kansai, Kanto, and Kyushu/Okinawa, and has accumulated both the number of veterinarians and the number of consultations by combining M&A with in-house training. As the market expands against the backdrop of pets being treated as family members and the ageing of pets, the fact that it can serve as a recipient for privately owned hospitals facing succession difficulties is also part of the company’s growth opportunity.

Revenue composition by business (%): Animal hospitals 100 (FY6/2025).

| Securities Code |

| TYO:194A |

| Market Capitalization |

| 14,162 million yen |

| Industry |

| Service |

Stock Hunter’s View

A comprehensive animal healthcare company. A seamless structure capable of providing consistent care for any type of case.

WOLVES HAND is Japan’s largest animal hospital group. At general animal hospitals, primary care and advanced care are handled by separate hospitals, with advanced care involving transfers and referrals to other hospitals. By contrast, the company’s distinguishing feature is that it handles everything within a single organization, from primary-care hospitals (family veterinary care) to secondary-care hospitals that provide advanced care requiring specialized diagnostic equipment and surgery.

Supported by the trend toward treating pets as family members and greater health consciousness, the veterinary medical market has experienced rapid growth over the past decade. Meanwhile, although the total number of animal hospitals continues to grow slightly, it is nearing a plateau. In particular, the shortage of successors at privately operated animal hospitals is severe, and the company aims to become a provider to meet this demand.

There are several other companies active in the M&A of animal hospitals, but many are led mainly by funds or run by management teams that are not veterinarians. Since the company’s top executive is a veterinarian (President Masashi Kitai is a practicing veterinarian), M&A negotiations and business succession tend to proceed smoothly.

In addition, business expansion through M&A has been supported by the development of young veterinarians’ capabilities. By establishing an early force-multiplication system, a pattern based on the provision of clinical opportunities, the transfer of skills from veteran doctors, and the optimization of personnel placement, it has become the key to achieving coverage through new graduate recruitment without relying on veterans.

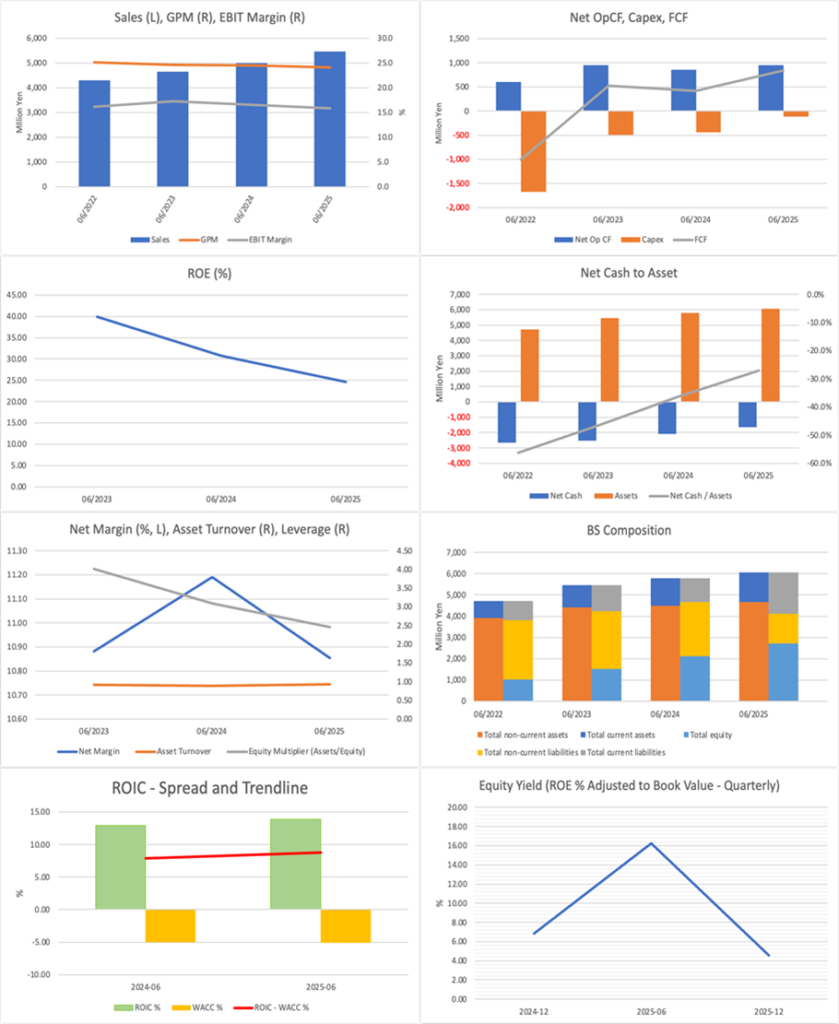

Earnings are weighted toward 4Q (April to June). The company has recently announced an upward revision to its full-year earnings forecast. It now expects FY6/2026 sales of 6.15 billion yen (up 12.6% YoY) and operating profit of 1.1 billion yen (up 21% YoY).

Investor’s View

Sell on Strength. While the share price is beginning to reflect the business’s quality, the sense of undervaluation remains limited.

The share price is within our estimated fair value range of 980 yen to 1,900 yen. However, it is already above the 1,430 yen median, and at this point, it is appropriate to prioritize profit-taking in phases of share price strength. However, this judgment does not constitute a denial of the business’s qualities. The company has a structure that enables it to deliver everything from routine to advanced medical care within a single organization. That structure has led to a virtuous cycle of training young veterinarians, accumulating clinical experience, improving its reputation, and securing further M&A opportunities. The market environment, in which pets are increasingly treated as family members and medical care spending is rising, is also supportive, and there is considerable room for growth as a recipient of privately owned hospitals facing succession difficulties. In addition, recent earnings are strong, with both sales and profit in 1H FY6/2026 increasing substantially, and the company revised its full-year forecast upward. A high ROE is also attractive, and the long-term EPS growth expectation embedded in the share price remains restrained relative to the historical realized growth rate.

On the other hand, it is difficult to say that this is a phase from which one should buy aggressively with a bullish stance. First, there is limited substantial undervaluation from a valuation perspective. Although the current share price falls within the fair value ranges derived from the PBR, DCF, and ROIC methods, it is already above the median, and there is insufficient valuation appeal to push the case through on the strength of the business alone. Second, the substance of the growth story remains under examination. As long as M&A continues, what matters is not the number of acquisitions, but whether profitability can be maintained and improved after each acquisition. The quality of PMI will continue to be tested. Third, constraints on supply and demand remain significant. The founder-manager and J-STAR hold thick stakes, and when treasury shares are included, the free float is thin. While this makes the share price more likely to jump on positive news, concerns over sales by major shareholders remain a constant overhang and also tend to hinder full-scale entry by institutional investors. In fact, despite strong earnings, the company’s share price has experienced periods in which its valuation failed to advance due to supply-demand imbalances and financial burdens.

In short, this stock is not in a position to be added based on the business’s high quality; rather, while recognizing the business value, profit-taking should be prioritized in phases where the share price has already reflected the business’s merits to a fair extent. However, the reservation to this judgment is also clear. If organic growth at existing hospitals continues, post-M&A integration proceeds smoothly, improvements in the number of consultations, consultation unit prices, and profitability accumulate, and market caution toward borrowings and goodwill also fades, the current share price range could prove to be only a passing point. In that sense, the current judgment is not pessimistic toward the business but disciplined with respect to price. The quality of the business is high. However, in phases when the share price is strong, it is more rational, as an investment action, to prioritize selling while assessing how much of the valuation has already been priced in, rather than chasing that strength.

Financials and Valuations

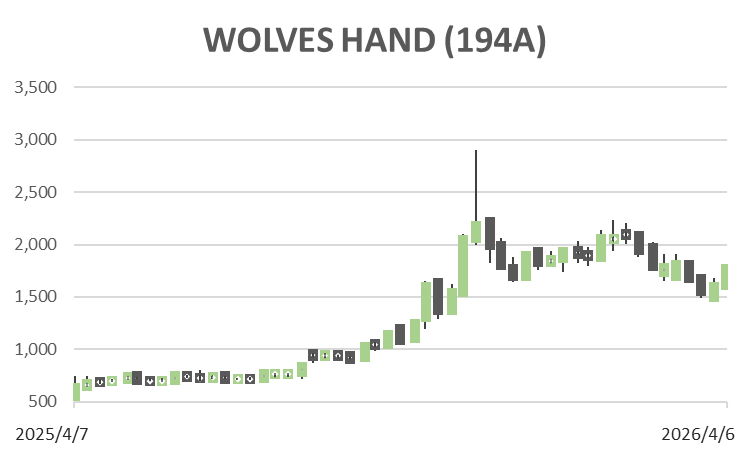

Price

PBR (LTM)

PER (LTM)

ROE (LTM)