2026-08-05

Home

Japanese

Omega Investment Co., Ltd.

DIGITAL HEARTS HOLDINGS (Company Note)

| Share price (8/17) | ¥1,922 | Dividend Yield (23/3 CE) | 1.09 % |

| 52weeks high/low | ¥2,700 / 1,405 | ROE(TTM) | 26.38 % |

| Avg Vol (3 month) | 101.5 thou shrs | Operating margin (TTM) | 8.60 % |

| Market Cap | ¥45.9 bn | Beta (5Y Monthly) | N/A |

| Enterprise Value | ¥43.5 bn | Shares Outstanding | 23.890 mn shrs |

| PER (23/3 CE) | 18.5 X | Listed market | TSE Prime section |

| PBR (22/3 act) | 5.53 X |

| Click here for the PDF version of this page |

| PDF Version |

Key company in the DX era providing cutting-edge QA (Quality Assurance) solution

Points of interest

Expanding from game debugging to enterprise software testing. Enterprise business is growing rapidly, driven by DX. Focus on global expansion in entertainment. The new management aims to generate sales of 50 billion yen in FY2024/3.

Summary

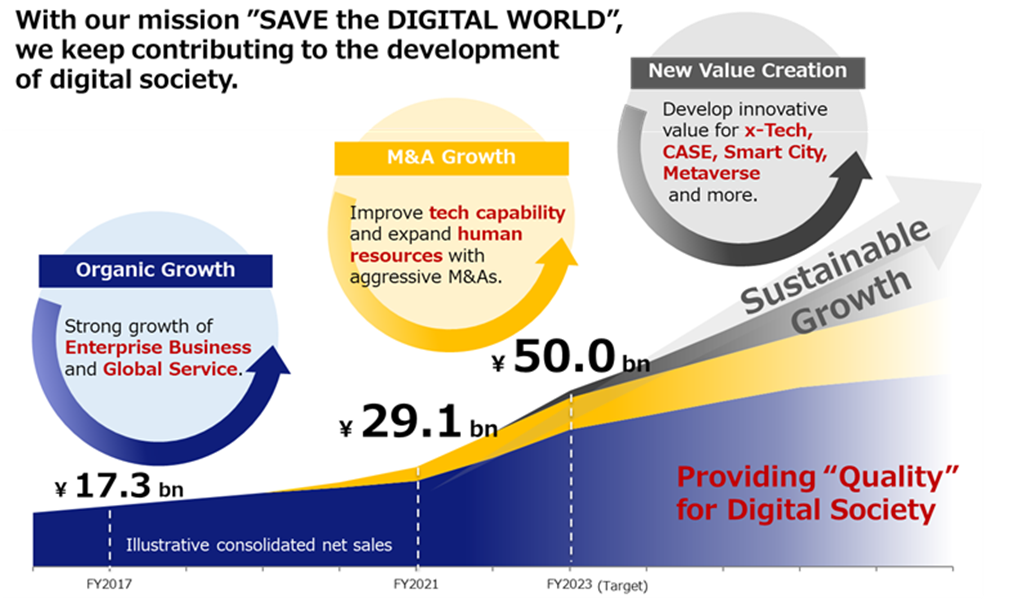

◇ DIGITAL HEARTS HOLDINGS is a software service company that provides software testing, security, game debugging and media services. Under the mission “SAVE the DIGITAL WORLD”, the company aims to provide safe and secure “quality” to the digital society. The company’s unrivalled strengths lie in its rapidly growing Enterprise Business and its track record in Entertainment Business, which has generated stable cash flows in recent years. In addition to organic growth, the company aims to accelerate growth through M&A and achieve sales of 50 billion yen in FY2024/3.

◇ The business model is turning over well: One of the focuses for the company from an investment perspective is its Enterprise Business, which is expected to grow at a high rate. Sales in this business, which the company has been focusing on in recent years, have grown rapidly at a CAGR of 57% over the last four years and are now at a stage where they generate stable profits. It is expected to continue to grow strongly as a growth driver for the company. Meanwhile, Entertainment Business has an oligopoly position in the domestic game debugging market and generates high and stable profits. This ample cash flow and strong financial base ensure a future growth path based on Enterprise Business.

◇ Thoughts on share price: The company’s share price was temporarily on a downtrend due to a series of profit declines that fell short of the management’s projections because of heavy upfront investment in Enterprise Business. However, the share price reversed course when Enterprise Business turned profitable in FY2021/3, hitting a high of 2,700 yen on 13 December 2021, the highest price since listing. In addition to the company’s high ROE, the shares appear to be undervalued in terms of valuation, considering the profitability and high growth of Enterprise Business. Given the company’s clear growth strategy, the management team that continues to lead and deliver results, solid financial strength and financial strategy, a revaluation of the shares is expected.

◇ Enterprise Business: With the rapid development of DX, ensuring software quality has become essential for social infrastructure. Software testing has until now been carried out in-house but outsourcing of the testing process is expected to expand further due to the worsening shortage of IT personnel in Japan and the need to improve specialisation, providing a tailwind for the company. The company has invested heavily in Enterprise Business since 2017 and has grown it to become the second business pillar in terms of both sales and profits. In addition to organic growth, the company will continue to make full use of M&A, aiming for sales growth of more than 40% CAGR from FY2021/3 to FY2024/3.

◇ Entertainment Business: The company’s ancestral Entertainment Business is an oligopoly, although the domestic market is maturing, and generates stable, high profits of around 20% on an operating margin basis. It is the source of the company’s solid financial base. Meanwhile, the overseas games market is expected to grow strongly in the future, and the company is actively expanding into this field, which should contribute to earnings over the medium to long term.

◇ Recent earnings: In FY2022/3, sales and operating profit both hit record highs, with sales of 29.1 billion yen (up 29% yoy) and operating profit of 2.7 billion yen (up 42%). Operating profit was 30% higher than initially planned. The main reason for this is that Enterprise Business is now firmly in the black, while Entertainment Business has seen an improvement in gross profit margins in addition to the increased revenues. The company plans a 22% yoy increase in revenue and a 22% rise in profit for FY2023/3 and announced a forecast for a significant increase in dividends (from 15 yen a share to 21 yen) for FY2023/3.

◇ Medium-term management vision: Having achieved profitability in Enterprise Business, the company aims to achieve further business growth based on further expansion of this business in the future. The company aims to achieve sales of 50 billion in FY2024/3, comprising over 25 billion in Enterprise Business and over 23 billion in Entertainment Business. The company has also announced financing to realise growth, and we will keep a close eye on the progress.

Table of contents

| Summary | 1 |

| Key financial data | 2 |

| Company profile | 3 |

| History, company’s group | 4 |

| Business overview | 7 |

| Enterprise Business | 7 |

| Entertainment Business | 11 |

| Financial results | 14 |

| Full-year results for 2022/3 | 14 |

| FY2023/3 full-year forecast | 16 |

| Growth strategy | 16 |

| Medium-term management vision | 16 |

| Stock information, etc. | 18 |

| Share Price Trend | 18 |

| Stock price observation | 19 |

| Major shareholders, Shareholding by ownership, Shareholder return policy | 21 |

| Corporate governance and the top management | 22 |

| Sustainability | 24 |

| Financial data | 25 |

Key financial data

| Fiscal Year (Unit: ¥mn) |

2016/3 | 2017/3 | 2018/3 | 2019/3 | 2020/3 | 2021/3 | 2022/3 |

| Net sales | |||||||

| Enterprise Business | 2,382 | 1,952 | 1,892 | 3,302 | 5,022 | 7,021 | 11,492 |

| Entertainment Business | 12,696 | 13,544 | 15,568 | 15,951 | 16,115 | 15,647 | 17,687 |

| Total net sales | 15,011 | 15,444 | 17,353 | 19,254 | 21,138 | 22,669 | 29,178 |

| Cost of sales | 10,691 | 10,939 | 12,394 | 13,791 | 15,566 | 16,236 | 20,787 |

| Gross profit | 4,321 | 4,506 | 4,959 | 5,463 | 5,572 | 6,434 | 8,391 |

| SG&A expenses | 2,357 | 2,600 | 3,223 | 3,858 | 4,178 | 4,525 | 5,690 |

| Operating income | 1,964 | 1,907 | 1,736 | 1,606 | 1,394 | 1,908 | 2,701 |

| Ordinary income | 1,958 | 1,997 | 1,783 | 1,651 | 1,372 | 1,975 | 2,778 |

| Net income | 361 | 795 | 1,200 | 1,575 | 792 | 974 | 1,780 |

| Current assets | 5,064 | 6,221 | 6,813 | 7,403 | 7,453 | 9,744 | 10,392 |

| Cash and deposits | 2,197 | 3,344 | 3,894 | 4,197 | 3,739 | 5,076 | 5,208 |

| Non-current assets | 1,469 | 1,430 | 1,761 | 2,428 | 3,183 | 4,593 | 7,172 |

| Goodwill | 437 | 201 | 150 | 481 | 1,027 | 2,467 | 4,763 |

| Total assets | 6,533 | 7,651 | 8,575 | 9,832 | 10,637 | 14,338 | 17,565 |

| Total liabilities | 3,444 | 4,793 | 5,005 | 4,819 | 5,198 | 8,024 | 9,989 |

| Total net assets | 3,089 | 2,858 | 3,570 | 5,012 | 5,438 | 6,314 | 7,576 |

| Equity ratio (%) | 43.1 | 34.4 | 39.3 | 48.7 | 46.3 | 39.7 | 39.9 |

| Cash flow from operating activities | 1,080 | 1,825 | 1,436 | 889 | 1,086 | 1,416 | 3,077 |

| Cash flow from investing activities | (17) | (610) | (618) | 62 | (1,018) | (1,813) | (2,537) |

| Cash flow from financing activities | (1,913) | (69) | (250) | (693) | (515) | 1,730 | (546) |

| Increase/decrease in cash and cash equivalents | 21 | 149 | 1,108 | 58 | 493 | 5,041 | 5,173 |

Source: Omega Investment from company materials

Company profile

DIGITAL HEARTS HOLDINGS (hereafter referred to as ‘the company’) is a pure holding company whose group companies focus on system testing and debugging services that detect software defects and report them to client companies. It also provides related software development support, operation and maintenance, security and other services. Under the corporate mission of “SAVE the DIGITAL WORLD”, the company provides comprehensive support for high-quality software development at client companies.

The two business segments are.

Enterprise Business: Provides system testing, IT services and security, mainly for enterprise systems such as web systems and business systems. Features differentiated services through QA solutions and test automation.

Entertainment Business: Mainly targets console games, mobile games and other entertainment content, and provides debugging services (detecting software defects from the user’s perspective and reporting them to the client company), support services for the overseas development of game titles, commissioned game development and the operation of a comprehensive game information website.

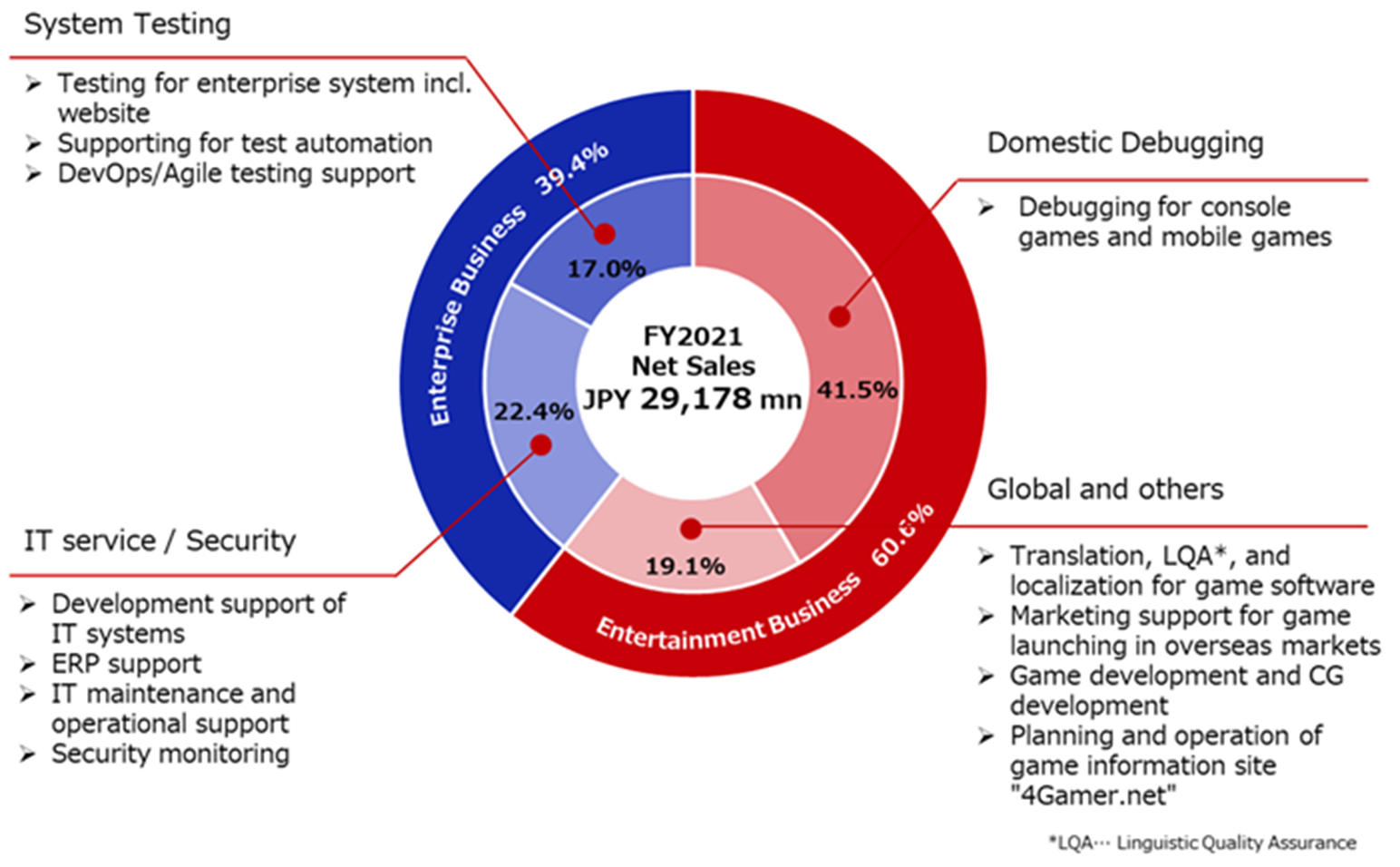

The company’s main business at its inception was debugging services for games software, but in recent years it has focused on expanding the enterprise sector. Enterprise Business accounts for approximately 40% of all sales in FY2022/3, while Entertainment Business comprises approximately 60%, growing to become the next major earnings driver.

Segment structure and service breakdown

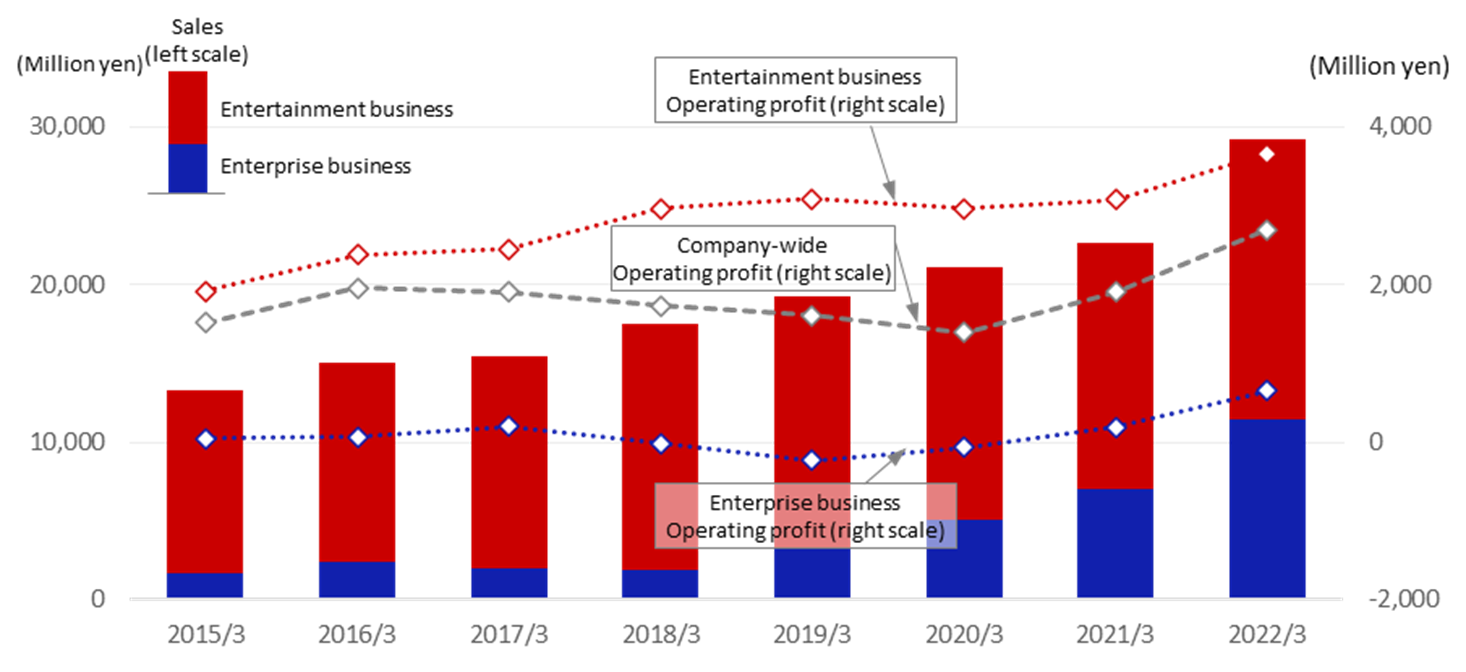

Trends in sales and operating profit

Source: Omega Investment from company materials

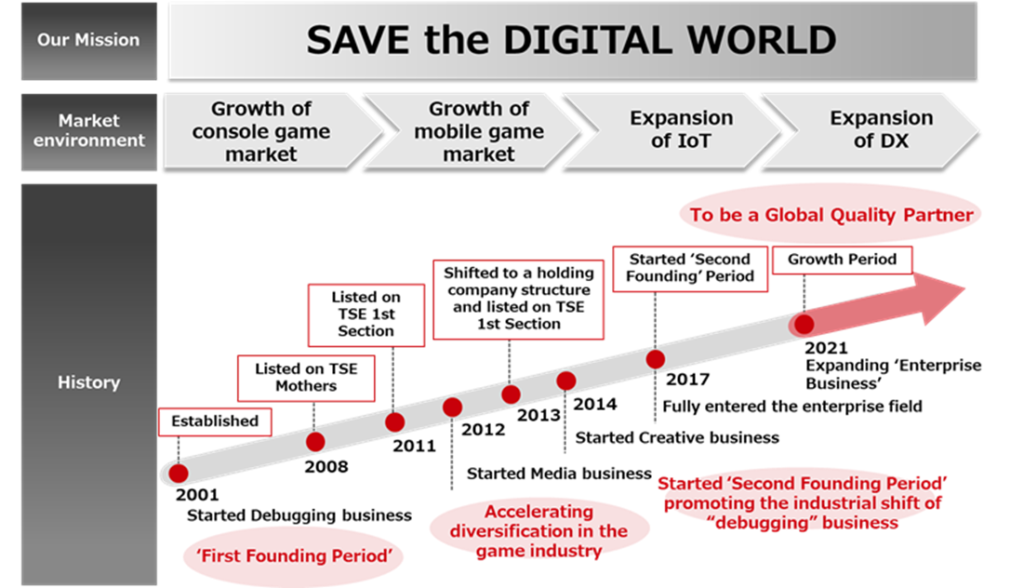

History (for a detailed timeline, see the history table on the following page)

Founding – IPO/becoming a holding company

The company was founded in April 2001. It began when Eiichi Miyazawa, the current Director and Chairman, established DIGITAL Hearts Ltd. to provide debugging services to detect faults in the game software. One of the pioneers in the outsourced game debugging business. Mr Miyazawa’s shrewdness in spotting a business opportunity in debugging (detecting faults in game software) at the time of the rise of the video game industry is remarkable. After achieving IPO, the company expanded overseas. In 2013, it established Hearts United Group co., Ltd. and shifted to a holding company structure (in July 2018, the company changed its name to DIGITAL HEARTS HOLDINGS Co., Ltd.)

’Second Founding’ Period: focus on Enterprise Business.

Subsequently, the company moved beyond the game debugging field to accumulate technology in the system testing and security fields and entered the enterprise field on a full-scale basis. At that time, Mr Miyazawa became Director and Chairman and invited Mr Genichi Tamatsuka, who had a proven track record of managing major listed companies, etc., to become President. Under Mr Tamatsuka’s leadership, the company invested management resources intensively in the enterprise sector as a ’Second Founding’ Period. On top of recruiting personnel from outside the company who are strong in this field, the company is actively investing in human resources and technology, including retraining and empowering internal personnel. Moreover, the company accelerated the growth of its Enterprise Business by actively utilising M&A, including the acquisition of US-based LOGIGEAR CORPORATION (‘LogiGear’), which has a proven track record in software test automation, in August 2019, as well as promoting collaboration with external parties, etc. In addition to LogiGear, the company has since continued to make M&A deals in Japan and abroad to strengthen its enterprise human resources and technology. The earnings from the ancestral, cash cow Entertainment Business provide the financial basis for these deals.

Entertainment Business seeks to capture growth in overseas markets

Meanwhile, in Entertainment Business, the company is accelerating its expansion from the domestic market, where growth is limited, to overseas operations: in March 2021, it acquired Metaps Entertainment Limited (now DIGITAL HEARTS CROSS Marketing and Solutions Limited), which provides marketing support to game manufacturers in Asia, mainly in Greater China, from Metaps Inc. While the domestic games market is maturing, the overseas games market is expected to continue to grow strongly at double-digit rates, so the company is exploring the possibility of increasing revenues by capturing overseas business.

Changes in the company’s group

| year (e.g. AD) |

month | Item |

| 2001 | Apr. | DIGITAL Hearts Ltd. established.Debugging services mainly for console games are launched. |

| 2003 | Oct. | Reorganised as a joint stock company. |

| 2007 | Sep. | First Japanese company to be accredited by Microsoft Corp. as a recommended game testing company (AXTP) for Xbox 360R. |

| 2008 | Feb. | Listed on the Mothers market of the Tokyo Stock Exchange. |

| 2011 | Feb. | Listed on the First Section of the Tokyo Stock Exchange. |

| Jul. | DIGITAL Hearts Korea Co., Ltd. is established as a consolidated subsidiary in South Korea. | |

| Oct. | DIGITAL Hearts USA Inc. is established as a consolidated subsidiary in the USA. | |

| Dec. | DIGITAL Hearts (Thailand) Co., Ltd. is established as a consolidated subsidiary in Thailand. | |

| 2012 | Mar. | G & D Co., Ltd. is established as a consolidated subsidiary. Starts providing outsourcing services for game software development. |

| May. | DIGITAL Hearts Visual Co., Ltd. is established as a consolidated subsidiary, separating 3D content production and related operations from the company. |

|

| Nov. | Acquired shares in Aetas, Inc. and made it a consolidated subsidiary. Start of media business operating the comprehensive game information website 4Gamer.nets. |

|

| 2013 | Oct. | Transition to a pure holding company structure with the establishment of a pure holding company, Hearts United Group Co., Ltd. through a share transfer. |

| Nov. | Acquired shares in NetWork21 Co.,Ltd., a systems development business, and made it a consolidated subsidiary. |

|

| 2014 | Apr. | Premium Agency Inc., a contracted game developer, becomes a consolidated subsidiary through the acquisition of shares and subscription to a third-party allocation of new shares. |

| 2016 | Jan. | G & D Co., Ltd. , DIGITAL Hearts Visual Co., Ltd. and Premium Agency Inc. merged to form FLAME Hearts Co.,Ltd. |

| Jul. | DIGITAL Hearts (Shanghai) Co., Ltd. is established as a consolidated subsidiary in Shanghai, China. | |

| 2017 | Jun. | Changes to the management structure, including a change of representative directors. Start of ‘second founding phase’ to accelerate business expansion in the enterprise domain. |

| Oct. | Merged with NetWork21 Co.,Ltd. with DIGITAL Hearts Co., Ltd. as the surviving company. | |

| 2018 | Jun. | Started working with US security venture Syack, Inc. Full-scale entry into the security business. |

| July. | Company name changed from Hearts United Group co., Ltd. to DIGITAL HEARTS HOLDINGS Co., Ltd. | |

| Aug. | Acquisition of shares in ANET Corporation, a system testing business, making it a consolidated subsidiary. |

|

| Nov. | The company has the largest number of qualified software testers in Japan and has been accredited as a Platinum Partner in the partnership programme of the International Software Testing Qualification Board (ISTQB), an international certification body for software testing. Platinum Partner accreditation |

|

| 2019 | Jan. | Orgosoft Co., Ltd, which provides game debugging and localisation services in South Korea, becomes a consolidated subsidiary. |

| Aug. | LOGIGEAR CORPORATION, which has extensive test automation know-how and test engineers, becomes a consolidated subsidiary through the acquisition of shares and subscription to a third-party allocation of new shares. |

|

| Nov. | Red Team Technologies Co., Ltd. established to provide penetration testing. | |

| Dec. | The company’s consolidated subsidiary DIGITAL HEARTS Co., Ltd. establishes Digital Hearts Linguitronics Taiwan Co., Ltd. in Taiwan as a joint venture with LINGUITRONICS Co.Ltd. |

|

| 2021 | Mar. | Acquisition of shares in Metaps Entertainment Limited, which provides marketing support to Chinese game makers in Asia, making a total of eight companies, including subsidiaries, consolidated subsidiaries. |

| Mar. | The company’s consolidated subsidiary LOGIGEAR CORPORATION acquired shares in MK Partners, Inc, a system consulting company that focuses on Salesforce implementation, maintenance and operation, and made it a consolidated subsidiary. |

|

| Mar. | The company’s consolidated subsidiary LOGI GEAR VIETNAM CO, LTD. establishes TPP Soft, JSC in Vietnam as a joint venture with TP&P Technology Company, Ltd. |

|

| Jun. | identity Inc., which operates an IT human resources support business, is acquired and made a consolidated subsidiary. |

|

| Jul. | Achieved Global Partner accreditation, the highest level of the ISTQB Partner Programme, with an industry-leading number of qualified software testers. |

|

| 2022. | Jan. | LOGIGEAR CORPORATION, a consolidated subsidiary of the company, acquired shares in DEVELOPING WORLD SYSTEMS LIMITED, which provides support for the introduction, maintenance and operation of ORACLE products, and made it a consolidated subsidiary. |

| Mar. | CEGB Ltd, which has a proven track record in SAP implementation and operation consulting, becomes a consolidated subsidiary. |

|

| Apr. | Business restructuring to integrate the company’s Enterprise Business into AGEST, Inc. (formerly Digital Hearts Networks Inc.). |

|

| Apr. | Transferred from the First Section of the Tokyo Stock Exchange to the Prime Market as a result of a review of the market classification of the Tokyo Stock Exchange. |

|

| Jun. | Capital and business alliance with GameWith, Inc. to strengthen the entertainment sector. | |

| Aug. | AGEST, a consolidated subsidiary of the company, absorbed the software testing business of Soval Corporation. |

■M&A-related matters

Source: prepared by Omega Investment from company data and other sources (history of Digital Hearts Inc. until November 2013).

The new management team takes on the challenge of a period of development

In FY2021/3, with Enterprise Business achieving full-year profitability, the company moved from its ’Second Founding’ Period to a period of development. A medium-term management vision for new growth was formulated, and Yasumasa Ninomiya, who had led Enterprise Business together with President Tamatsuka, was appointed as the new President and CEO, while Toshiya Tsukushi, who had promoted several M&As as Director and CFO, was appointed as Executive Vice President and CFO. Under the new management team, the company will continue to accelerate growth, particularly in Enterprise Business, and aims to achieve sales of 50 billion yen in FY2024/3.

Group overview

Group restructuring: AGEST, which is responsible for Enterprise Business, is now in place.

The group consists of 27 consolidated subsidiaries (10 domestic and 17 overseas) and one non-consolidated subsidiary under the pure holding company DIGITAL HEARTS HOLDINGS Co., Ltd. (as of end-March 2022). In April 2022, the company was reorganised into an organisational structure centred on AGEST , Inc. (which took over Enterprise Business of the former DIGITAL HEARTS NETWORKS and DIGITAL HEARTS Co., Ltd.), which is responsible for Enterprise Business, and DIGITAL HEARTS Co., Ltd., which is responsible for Entertainment Business. The structure was designed to further enhance expertise and strongly promote the creation of new value in each of these business areas.

Business overview

Enterprise Business

Enterprise software testing market with significant and expanding growth potential

Ensuring software quality is a key issue in the development of DX

As society and business become increasingly ICT-oriented, as typified by the term DX, information systems have become an important management resource that determines the competitiveness of companies. As information systems become more important than ever before, it has become critical to find and solve problems inherent in software in advance and provide systems with a high degree of completeness. Modern systems are becoming ever more expansive and complex, and network connectivity is constant, so it is not easy to ensure system quality, including security. As already witnessed, system failures in various fields, such as finance and telecommunications, have had a significant impact on social life.

Outsourcing of software testing is underway

Traditionally, software development in Japan has been a relatively closed system, with vendors such as major system developers and system integrators taking on bulk orders and delivering to customers in a ‘requirements definition → design → implementation → testing → operation’ (waterfall-type development). One of the characteristics of the Japanese information services industry is that most system engineers (around 70%) belong to vendors, and system testing has been carried out in-house by vendors. On the other hand, as society becomes increasingly ICT-oriented, the shortage of IT personnel such as SEs and programmers is becoming more serious in Japan, partly due to a mismatch of skills among IT personnel. Some estimates suggest a shortage of up to 800,000 personnel (according to the Ministry of Economy, Trade and Industry). As a result, major system developers are maintaining their development capabilities by using their own engineers for key development tasks and outsourcing system testing. In addition, the skill sets required for software quality assurance are different from those required for system development, and to ensure high quality, it is more effective to verify software from the eyes of a third party who is skilled in software testing. Furthermore, the recent shift from legacy software development to agile development methods has increased the expertise required for software testing. As a result, a major trend is to outsource software testing, which used to be carried out in-house, to specialist testing companies.

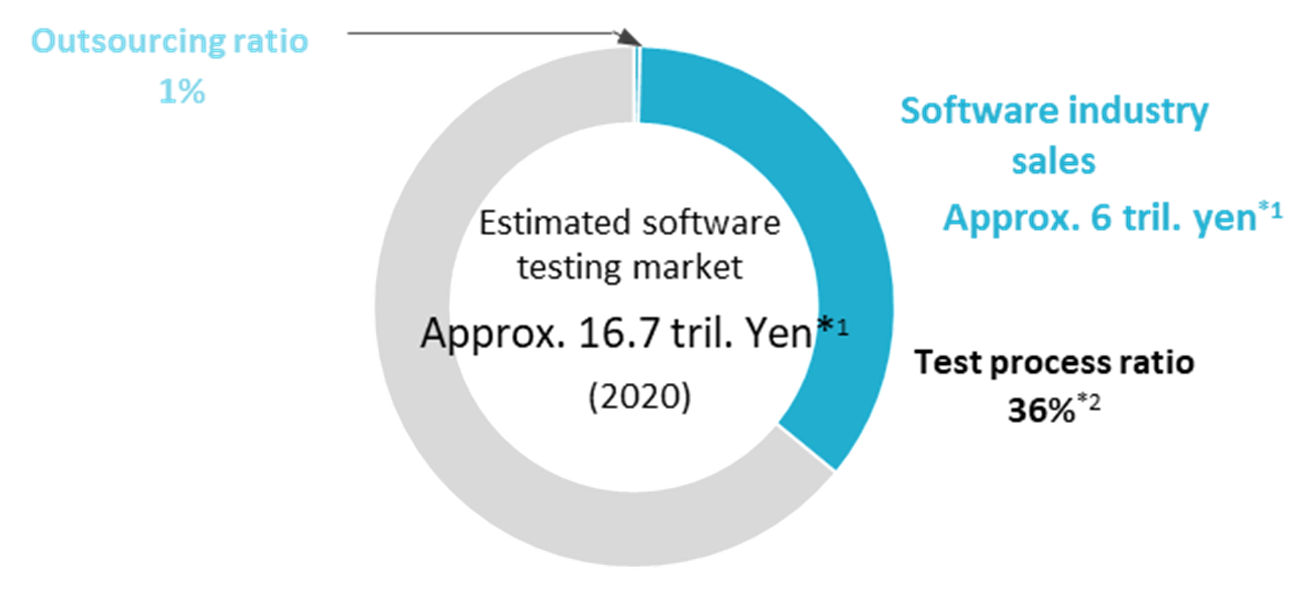

The software testing market is worth approximately 6 trillion yen

The software industry in Japan has a turnover of 16,661.9 billion yen (Source: 2021 Basic Survey of the Information and Communications Industry, Ministry of Internal Affairs and Communications and Ministry of Economy, Trade and Industry). Of this, the ratio of testing processes to development processes is estimated to be around 35.6% (Source: estimated from the ratio of actual man-hours by a process in the White Paper on Software Development Data 2018-2019, Information-technology Promotion Agency (IPA), Japan). Multiplying the software industry revenue by the ratio of testing processes, the software testing market is estimated to be worth just under 6 trillion yen. As mentioned above, most of this testing process is currently carried out in-house, and even if only part of this is outsourced, the market potential is huge for companies specialising in software testing. Incidentally, there are currently three listed software testing specialists in the enterprise sector, including the company itself, and the combined recent sales of the three companies (Enterprise Business only) are less than JPY 100 billion, representing only 1% of the estimated market. According to a survey in the US, where outsourcing of software testing has been progressing, a certain amount of in-house software testing will remain, and the outsourcing ratio is estimated at 30-40%. In any case, it can be said that a large growth market (blue ocean) is currently expanding for the company.

Estimated software testing market size

※2 Information-technology Promotion Agency (IPA), White Paper on Software Development Data 2018-2019.

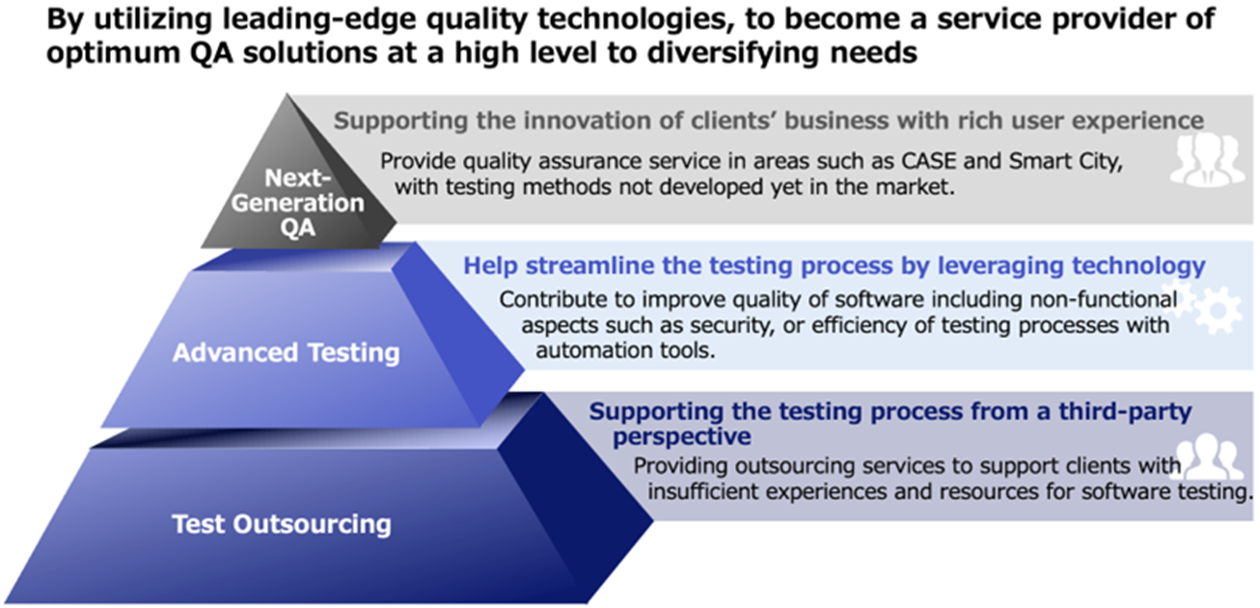

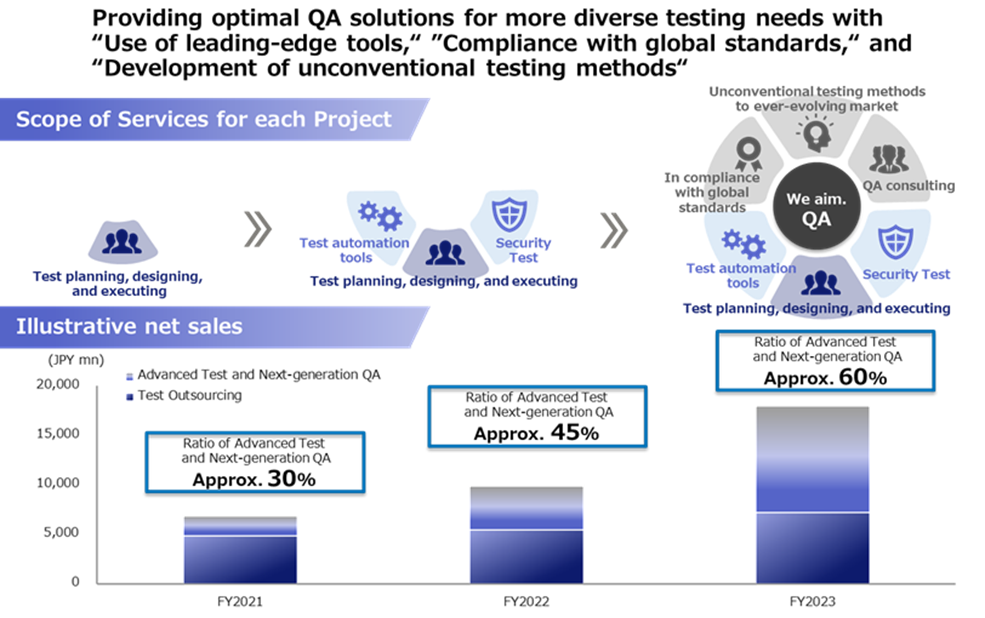

The company’s strengths in the enterprise market

Differentiation through investment in leading-edge quality technology

In achieving top-line growth in its Enterprise Business, the company is differentiating itself from its competitors by improving its competitiveness through the introduction of state-of-the-art quality technology. As part of its efforts to enhance the quality of its human resources to strengthen the quality, the company is promoting the acquisition of certification from the International Software Testing Qualifications Board (ISTQB). The company is one of only three Global Partners in Japan, and 365 of its employees including engineers hold ISTQB qualifications (as of end-March 2022).

It also focuses on software test automation and provides a diverse range of automation tools. One example is the acquisition of LogiGear, a leading company in the field of software testing with strong automation tools, as a subsidiary. In addition, the company recruits a wide range of high-level personnel and cooperates with national and international authorities in software testing. In addition, the AGEST Testing Lab. was established as a research institute to promote the research and practical application of new testing methods through industry-academia collaboration.

The software industry tends to fall into a labour-intensive profit model, but the company differentiates itself in advanced testing, including security and automation, based on software testing outsourcing by making full use of these cutting-edge technologies. In the future, the company aims to realise a high-value-added revenue model by providing next-generation QA for which methods have not yet been established.

Support system by national and international software testing authorities

What we aim to become in Enterprise Business

Enterprise Business’s M&A aims and achievements

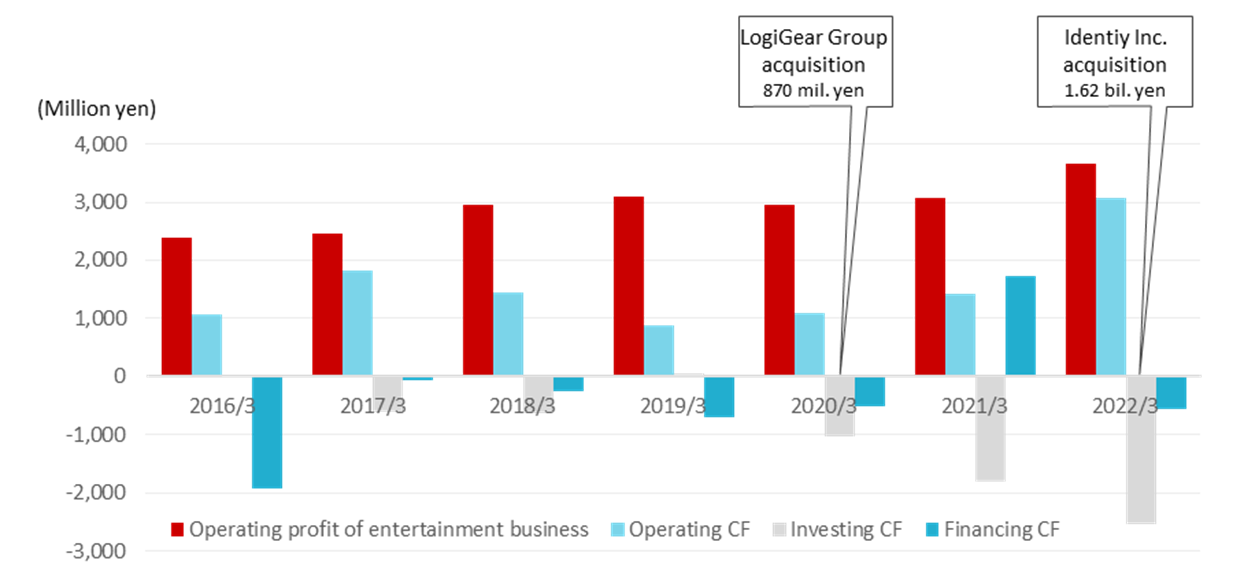

Entertainment Business: operating profit and CF

Solid financial base to support M&A strategy

To realise the aforementioned technological advantages in a short time, the company has secured human resources and acquired technological capabilities and know-how in Enterprise Business through aggressive mergers and acquisitions. This has been made possible by the company’s solid financial base. Entertainment Business, which is the company’s cash cow, has secured an operating margin of around 20% and has generated operating profits to the tune of 3 billion yen. As a result, the company generates operating cash flow in the order of 1-3 billion yen every year. This cash flow, together with cash and deposits of over 5 billion yen accumulated on the balance sheet, has enabled it to make upfront investments in Enterprise Business and M&A strategies.

Enterprise Business segment

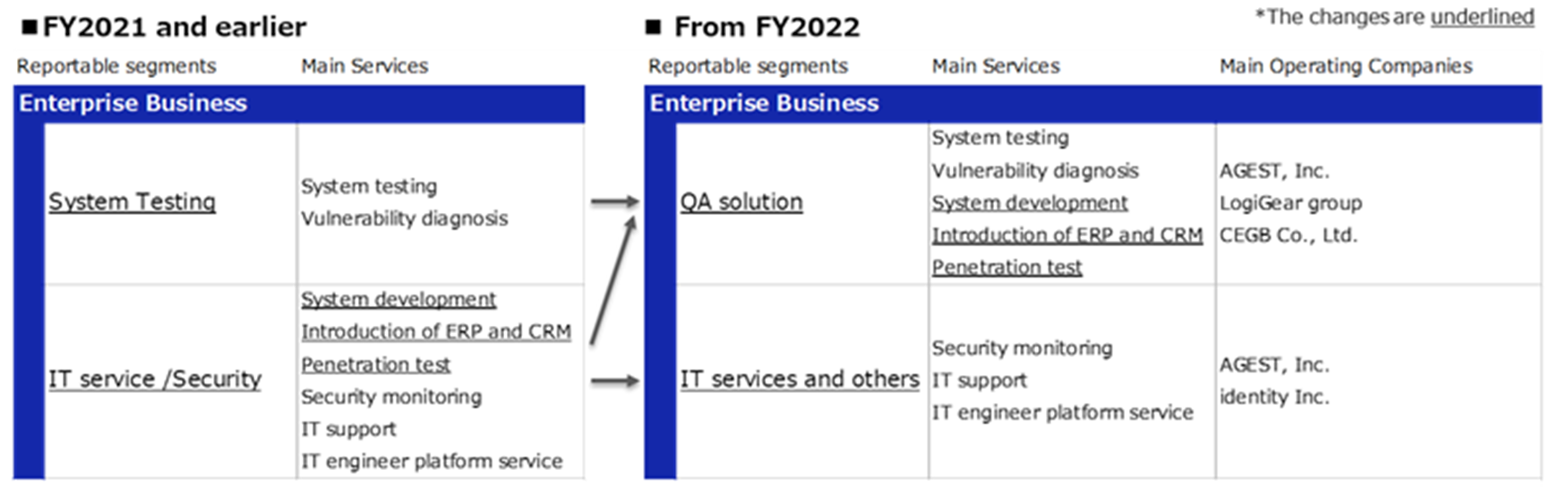

Enterprise Business comprises two sub-segments: a) System testing: detecting faults in a wide range of software, mainly web systems, business systems and business applications; and b) IT services and security: providing commissioned system development services, IT support such as maintenance and operational support, and security and other services. (The sub-segments have been changed from FY2023/3, so please refer to the supplementary explanation in the second part of the next page).*

As noted in the company history, the company has been actively investing in its Enterprise Business since 2017 as its ’Second Founding’ Period. It has focused on and developed this business as a growth driver for the next generation. As a result, the company recorded a high sales growth CAGR of 42.6% from FY2017/3 to FY2022/3. Segment losses continued from FY2018/3 to FY2020/3 due to upfront investment in business expansion, but the business returned to profitability in FY2021/3. In FY2022/3, the business recorded an operating margin of 5.6%. The number of employees in the business increased at a CAGR of 60% over the same period, partly because of M&A. The segment’s number of employees at the end of FY2022/3 was 929, accounting for the majority of the total number of employees (see table, next page).

Enterprise Business revenue trends

| Financial year | 2017/3 | 2018/3 | 2019/3 | 2020/3 | 2021/3 | 2022/3 | CAGR 17/3〜22/3 |

| Net sales (all company) | 15,444 | 17,353 | 19,254 | 21,138 | 22,669 | 29,178 | 13.6% |

| YoY | 2.9% | 12.4% | 11.0% | 9.8% | 7.2% | 28.7% | – |

| Enterprise Business | 1,952 | 1,892 | 3,302 | 5,022 | 7,021 | 11,492 | 42.6% |

| YoY | -18.1% | -3.8% | 75.8% | 52.1% | 39.8% | 63.7% | – |

| Composition of sales | 12.6% | 10.8% | 17.1% | 23.8% | 31.0% | 39.4% | – |

| System testing | 778 | 1,084 | 1,395 | 2,414 | 3,581 | 4,954 | 44.8% |

| YoY | 14.2% | 39.3% | 28.7% | 73.0% | 48.4% | 38.3% | – |

| Composition of sales | 5.0% | 6.2% | 7.2% | 11.4% | 15.8% | 17.0% | – |

| IT services and security | 1,193 | 808 | 1,907 | 2,608 | 3,439 | 6,537 | 40.5% |

| YoY | -29.9% | -32.3% | 136.0% | 36.8% | 31.9% | 90.1% | – |

| Composition of sales | 7.7% | 4.7% | 9.9% | 12.3% | 15.2% | 22.4% | – |

| Operating profit (Corporate-wide) | 1,906 | 1,735 | 1,605 | 1,394 | 1,908 | 2,701 | 7.2% |

| YoY | -2.9% | -9.0% | -7.5% | -13.1% | 36.9% | 41.5% | – |

| Operating profit margin | 12.3% | 10.0% | 8.3% | 6.6% | 8.4% | 9.3% | – |

| Enterprise Business | 203 | (14) | (226) | (67) | 188 | 649 | 26.2% |

| YoY | 185.9% | – | – | – | – | 244.8% | – |

| Segment profit margin | 10.4% | -0.7% | -6.8% | -1.3% | 2.7% | 5.6% | – |

| No. of employees (all company, persons) | 648 | 750 | 862 | 1,330 | 1,431 | 1,683 | 21.0% |

| No. of employees (Enterprise Biz, persons) | – | – | 213 | 619 | 709 | 929 | 63.4% |

| [Temporary employees] (persons) | – | – | 45 | 103 | 123 | 130 | 42.4% |

| No. of employees (incl. temporary employees) | – | – | 258 | 721 | 832 | 1,059 | 60.1% |

Source: Omega Investment from company materials

(a) System testing

System testing is a service that detects faults in a wide range of business software, including web systems, business systems and business applications used by the enterprise. The service is provided by AGEST, a business company in the enterprise sector, and other group companies such as ANET, LogiGear, MK Partners, Inc, TPP SOFT and DWS.

Specific services include web and business system validation, test automation support, vulnerability assessment and DevOps/agile testing support.

The sales CAGR for the last five years in system testing was 44.8%. Sales increased significantly by 73% yoy in FY2020/3, when LogiGear’s performance made a contribution.

(b) IT services and security

In addition to commissioned system development, the company provides ERP implementation support, maintenance and operation support, as well as penetration testing and security monitoring. Security needs are particularly high in recent years, with cyber-attacks becoming more active. The service is provided by AGEST, identity and CEGB.

identity Inc. provides client companies with human resources services such as freelance matching, human resources introduction and temporary staffing for freelance engineers and other IT personnel. The grouping of identiy Inc. has enabled the utilisation of approximately 13,000 (on a registered basis) high-level IT engineers, significantly expanding capacity in Enterprise Business.

*Changes to sub-segments

The company has changed the sub-segments of its Enterprise Business as follows from FY2023/3. Although this sub-segment will be used to look at the future, this report discusses the previous segment to analyse the past trends.

Entertainment Business

The domestic market has become an oligopoly and is growing steadily. In overseas markets, high growth is expected to continue.

The domestic games market has matured and is growing steadily

Entertainment Business is the company’s ancestral business, based on debugging services for game consoles. Currently, the two main areas of entertainment debugging are game consoles (Sony Playstation, Nintendo, Microsoft Xbox and other home consoles) and mobile games. Basically, debugging revenues do not correlate to the sales value of individual software titles, but depend on the number of game titles released according to the respective market trends. A look at the current size of the respective markets in Japan is as follows.

(1) Game consoles (hardware + software): peaked at 703.1 billion yen in 2007 and have been on a downward trend since but are expected to reach 361.4 billion yen in 2021, partly due to the emergence of a stay-at-home demand following the spread of COVID. (Source: Famitsu Game White Paper).

(2) Mobile games: the market size in 2021 is 1,306 billion yen. The market grew at a CAGR of 34% when smartphones were introduced but has grown at a CAGR of 6% over the last five years (source: Famitsu Mobile Game White Paper).

As such, each of these markets is maturing and can be expected to remain stable. In the case of game consoles, when a new console model goes on sale, new titles are produced around that time, which also generates demand for debugging.

Most recently, the number of debugging needs for game consoles increased, mainly due to the stay-at-home demand under the spread of the new coronavirus infection.

Debugging markets: high barriers to entry

Unlike enterprise software, debugging of software in the entertainment market is relatively commonly outsourced. While the development schedule for game production is often fluid, debugging work is not a constant occurrence, which is thought to have led to outsourcing by specialised companies that can provide debugging personnel in a flexible manner. On the other hand, the game debugging business is also characterised by high barriers to entry. The reasons include the need to prepare verification equipment certified by hardware companies and to have a variety of verification equipment to meet customer needs, the need for a large number of testers to respond over a short time to coincide with the launch of a new game, and the strict security management required by clients to maintain the confidentiality of pre-launch titles.

Debugging market: increasingly oligopolistic, market size estimated at around 30-40 billion yen

Currently, the Japanese debugging market is an oligopoly, with the company and Pole To Win Holdings (TSE: 3657; debugging is conducted by the operating company Pole To Win Corporation) almost bisecting the market. SHIFT (TSE: 3697) also entered the market in 2013. Based on the annual reports of the three companies, the market size of debugging in 2021 is estimated to be around 30-40 billion yen (however, Pole To Win may include services such as translation. Also, the companies other than the three needs to be considered). The market has grown at a steady single-digit rate every year for the past five years or so.

Debugging services enjoy relatively high profit margins

Debugging companies enjoy relatively high profit margins because debugging services are increasingly oligopolistic due to high barriers to entry and because they are an essential service for clients. The company has consistently achieved operating profit margins of around 20%, while SHIFT has achieved similar operating profit margins in its Entertainment Business (22.2%, FY2021/8). That of Pole To Win Holdings has also been around 15%, although declining in recent years. After all, debugging service is a highly profitable business for each of them.

The global games market continues to grow strongly

The Japanese games market is mature but continues to grow at a high rate on a global level: the global games market was worth 208.6 billion dollars in 2022, growing at a CAGR of 7.9% and is expected to reach 304.7 billion dollars by 2027. Growth is particularly significant in the Asian region, represented by China, and the market size is expected to grow from 118.3 billion dollars in 2022 to 175.3 billion dollars in 2027, at a CAGR of 8.3% (source: Statista). The size of the game debugging market is not known, but with the increasing overseas expansion of game titles in recent years, demand is expected to be high for the translation and other market support services provided by the company’s group.

The company’s strengths in the entertainment market

High debugging share

The company boasts a high debugging involvement rate of approximately 75% of the top 100 new console game titles (FY2022/3, company survey). The company has long-standing business relationships with game developers through game titles (e.g., series titles) and has accumulated mutual know-how. Switching costs are also high for clients, so once a client is acquired, the company receives debugging orders on an ongoing basis.

A talent pool of about 8,000 testers and more than 20 test centres

The company’s major strength in the entertainment sector is its approximately 8,000 registered testers. The skills required for debugging games differ according to the type of game, e.g., shooting games, sports games, car racing, etc. To respond accurately to customer needs in a short time, it is necessary to secure experienced testers, and the company has the industry’s top-level tester workforce. Thirteen test centres (Lab.) in Japan and eight overseas have been established as bases for testers to work, with Lab. equipped with full security measures. In June 2022, the company opened its first dedicated global service centre, Tokyo Lab. in Shibuya. As a measure against infectious diseases, some work can also be carried out remotely.

Diverse verification equipment

Verification equipment certified by hardware companies is essential for console game debugging. Mobile game debugging also requires a wide variety of verification equipment, and the company has a large collection of such equipment thanks to its many years of experience. The company currently has 2,054 console game machines and 6,782 smart devices (smartphones, etc.), enabling it to respond to a variety of customer needs.

Strong cash generating ability

As noted in the Enterprise segment, the company’s Entertainment Business is strong in generating stable cash. It enjoys high profit margins due to its oligopoly in this market, backed by a stable domestic market. The business generates an operating profit of approximately 3 billion yen every year. The cash generated by the business has consequently enabled Enterprise Business to achieve rapid growth.

Entertainment Business segment

Mainly targeting entertainment content such as console games and mobile games, the following services are provided: a) Domestic debugging: detecting software defects from the user’s perspective and reporting them to the client company; (b) Global and others: In addition to global services including translation, LQA (Linuistic Quality Assurance; checking the quality of translated text and composition) and marketing support for the overseas development of game titles, the company also provides creative services including commissioned game development, 2D/3D graphic production, and media services such as the operation of 4Gamer.net, which is a comprehensive game information website.

As already mentioned, Entertainment Business generates stable profits on the back of its high market share in Japan. Over the last five years, the business has registered a CAGR of 5.5% on sales, with an average operating margin of 19.4% over the same period.

Meanwhile, while the domestic market is maturing, overseas markets, including China and Asia, are growing remarkably. The company is focusing on overseas markets as a future growth target for its Entertainment Business. The company acquired shares in Metaps Entertainment Limited, which provides marketing support to Chinese game makers in the Asian region, and including Metap’s subsidiaries, consolidated a total of eight companies as subsidiaries. Renaming it DIGITAL HEARTS CROSS Marketing & Solutions (DHX) in June 2021, the company is focusing on expanding business in the region. It is expected to take time for DHX to contribute to bottom-line earnings, but the plan is to make it part of the company’s global expansion.

Entertainment Business revenue trends

| Financial year | 2017/3 | 2018/3 | 2019/3 | 2020/3 | 2021/3 | 2022/3 | CAGR 17/3〜22/3 |

| Net sales (Corporate-wide) | 15,444 | 17,353 | 19,254 | 21,138 | 22,669 | 29,178 | 13.6% |

| YoY | 2.9% | 12.4% | 11.0% | 9.8% | 7.2% | 28.7% | – |

| Entertainment Business | 13,544 | 15,568 | 15,951 | 16,115 | 15,647 | 17,687 | 5.5% |

| YoY | 6.7% | 14.9% | 2.5% | 1.0% | -2.9% | 13.0% | – |

| Composition of sales | 87.7% | 89.7% | 82.8% | 76.2% | 69.0% | 60.6% | – |

| New sub-segments | |||||||

| Domestic debugging | – | – | – | – | 11,536 | 12,123 | – |

| YoY | – | – | – | – | – | 5.1% | – |

| Composition of sales | – | – | – | – | 50.9% | 41.5% | – |

| Global and others | – | – | – | – | 4,111 | 6,537 | – |

| YoY | – | – | – | – | – | 19.2% | – |

| Composition of sales | – | – | – | – | 18.1% | 19.1% | – |

| Old sub-segments | |||||||

| Debugging | 11,524 | 13,186 | 13,103 | 13,823 | 13,058 | – | – |

| YoY | 10.2% | 14.4% | -0.6% | 5.5% | -5.5% | – | – |

| Composition of sales | 74.6% | 76.0% | 68.1% | 65.4% | 57.6% | – | – |

| Game Consoles | 3,483 | 4,174 | 4,356 | 4,709 | 4,830 | – | – |

| YoY | 1.0% | 19.8% | 4.4% | 8.1% | 2.6% | – | – |

| Composition of sales | 22.6% | 24.1% | 22.6% | 22.3% | 21.3% | – | – |

| Mobile solutions | 6,262 | 7,399 | 8,172 | 8,173 | 7,653 | – | – |

| YoY | 25.4% | 18.2% | 10.4% | 0.0% | -6.4% | – | – |

| Composition of sales | 40.5% | 42.6% | 42.4% | 38.7% | 33.8% | – | – |

| Amusement | 1,778 | 1,612 | 775 | 939 | 573 | – | – |

| YoY | -11.6% | -9.3% | -51.9% | 21.2% | -38.9% | – | – |

| Composition of sales | 11.5% | 9.3% | 4.0% | 4.4% | 2.5% | – | – |

| Creative | 1,465 | 1,743 | 1,891 | 1,226 | 1,449 | – | – |

| YoY | -15.3% | 19.0% | 8.5% | -35.2% | 18.2% | – | – |

| Composition of sales | 9.5% | 10.0% | 9.8% | 5.8% | 6.4% | – | – |

| Media and others | 554 | 638 | 956 | 1,066 | 1,139 | – | – |

| YoY | 8.2% | 15.2% | 49.8% | 11.5% | 6.9% | – | – |

| Composition of sales | 3.6% | 3.7% | 5.0% | 5.0% | 5.0% | – | – |

| Operating profit (Corporate-wide) | 1,906 | 1,735 | 1,605 | 1,394 | 1,908 | 2,701 | 7.2% |

| YoY | -2.9% | -9.0% | -7.5% | -13.1% | 36.9% | 41.5% | – |

| Operating profit margin | 12.3% | 10.0% | 8.3% | 6.6% | 8.4% | 9.3% | – |

| Entertainment Business | 2,453 | 2,966 | 3,086 | 2,964 | 3,077 | 3,668 | 26.2% |

| YoY | 3.1% | 20.9% | 4.0% | -4.0% | 3.8% | 19.2% | – |

| Segment profit margin | 18.1% | 19.1% | 19.3% | 18.4% | 19.7% | 20.7% | – |

| No. of employees (all company, persons) | 648 | 750 | 862 | 1,330 | 1,431 | 1,683 | 21.0% |

| No. of employees (Entertainment Biz, persons) | – | – | 555 | 552 | 567 | 525 | -1.8% |

| [Temporary employees] (persons) | – | – | 3,261 | 3,416 | 3,288 | 3,466 | 2.1% |

| No. of employees (incl. temporary employees) | – | – | 3,816 | 3,968 | 3,855 | 3,991 | 1.5% |

Source: Omega Investment from company materials

Financial results

Full year consolidated sales / operating profit trend

Full-year results for 2022/3

The first year of the new management team – perfect achievement

In both Enterprise Business and Entertainment Business, sales and operating profit posted record highs, partly due to M&A. Operating profit came in 30% above the initial guidance. From the beginning of April 2022, AGEST, the core company for Enterprise Business formed as a result of the group reorganisation, started operations. The company plans a 20% yoy increase in sales and a 20% increase in operating profit for FY2023/3. It announced a forecast for a large increase in dividends. These make us interested to keep track of the share price going forward.

FY2022/3 full-year results: record highs in both sales and profits.

The company’s full-year results for FY2022/3 were strong in both Enterprise Business and Entertainment Business. The company achieved a significant increase in sales and profits, with growth in existing businesses and the effect of mergers and acquisitions. Sales reached a record high of 29.1 billion yen (+29% yoy) and operating profit 2.7 billion yen (+42% yoy). Operating profit exceeded the initial plan by approximately 30%.

Enterprise Business, which had undergone aggressive upfront investments, grew to a scale that generates stable profits from the Q2 of FY2021/3 (segment profit was 650 million yen, up 3.5 times). Entertainment Business, which is a cash cow, secured a high operating margin of 20% and generated good cash with a segment profit of 3.67 billion yen (+19% yoy).

| JPY, mn, % | Net sales | YoY % |

Oper. profit |

YoY % |

Ord. profit |

YoY % |

Profit ATOP |

YoY % |

EPS (¥) |

DPS (¥) |

| 2018/3 | 17,353 | 12.4 | 1,735 | -9.0 | 1,782 | -10.8 | 1,200 | 50.9 | 55.14 | 11.50 |

| 2019/3 | 19,254 | 11.0 | 1,605 | -7.5 | 1,651 | -7.4 | 1,575 | 31.3 | 72.13 | 13.00 |

| 2020/3 | 21,138 | 9.8 | 1,394 | -13.2 | 1,372 | -16.9 | 792 | -49.7 | 36.31 | 14.00 |

| 2021/3 | 22,669 | 7.2 | 1,908 | 36.9 | 1,975 | 43.9 | 974 | 23.0 | 45.15 | 14.00 |

| 2022/3 (Act) | 29,178 | 28.7 | 2,701 | 41.5 | 2,778 | 40.7 | 1,780 | 82.7 | 82.35 | 15.00 |

| 2023/3 (CE) | 35,500 | 21.7 | 3,290 | 21.8 | 3,290 | 18.4 | 2,250 | 26.4 | 104.04 | 21.00 |

Sales/Profit by Segment

In line with the growth of Enterprise Business, the core company responsible for Enterprise Business, AGEST, Inc., was launched on 1 April as a result of the group reorganisation, as previously announced. In Enterprise Business, the company aims to achieve further growth by providing QA solutions at a higher quality level, for example, by promoting collaboration with authorities in the field. Meanwhile, Entertainment Business will continue to be handled by the operating subsidiary DIGITAL HEARTS Co., Ltd.

Segmental trends

Enterprise Business: sales increased by 60% yoy (11,491 million yen), posting a profit margin of 5.7%.

Enterprise Business saw a 60% increase in sales thanks to the acceleration of DX and aided by recent M&A. Segment profits were also firmly in the black, amounting to 649 million yen, or 3.5 times higher than in the previous year. The segment profit margin was 5.7%, and 6.9% in Q4 alone, after amortising goodwill on M&A.

System testing: sales increased by 38.3% yoy (4,954 million yen). While continuing to reinforce engineers and marketing strength, the company grew the number of new customers and improved the annual average sales per existing customer by measures such as aggressive proposals for total solutions that improve quality. The company has been pursuing mergers and acquisitions. (The graph on the next page). Acquisition of MK Partners and TPP SOFT kicked in the consolidated accounts from Q2, while DEVELOPING WORLD SYSTEMS was included from Q4. Existing businesses also achieved growth of 20% yoy. Despite ongoing investment in business expansion, the company has maintained a high level of profitability at 35.2% on a gross margin basis. The company will differentiate itself from the competition by providing high-standard QA solutions, including the use of test automation tools.

IT services and security: 90.1% yoy revenue growth (6,537 million yen). Against the backdrop of the acceleration of DX and the expansion of remote working, all services, including commision development/SES, maintenance/operation and security, recorded growth of more than 20% yoy. identity Inc., which was acquired through M&A in June 2021, contributed to the results from 2Q. Investment in human resources, the key to growth, continues to be active, with the number of in-house security personnel increasing by 1.4 times over the previous year.

Entertainment: 13.0% yoy increase in revenue (17,687 million yen), segment profit rose 19.2%.

The console games market remained buoyant, while overseas development of content accelerated. Against these backdrops, the company ensured that it captured the increasing demand, and domestic debugging, Global and others all performed well. Global and others increased by 35.3%, partly because of M&A. Profit increased by 19.2% to 3,668 million yen due to rising revenue and improved gross margins. The company’s cash cow has continuously generated high levels of profit. The segment profit margin was also high at 20.7%.

Domestic debugging: 5.1% yoy increase in sales (to 12,123 million). With FY2022/3 seeing a rebound from the impact of development delays at clients caused by the spread of infectious diseases in the first half of FY2021/3. Furthermore, the development of new titles for major domestic console games was boosted by the active development of new titles. In addition to this revenue growth, the gross profit margin improved by 2.5 percentage points due to the active promotion of operational reforms and other measures, ensuring a high profit margin of 31.1% for the full year.

Global and others: +35.3% yoy (5,563 million). Cross-border/global projects were won against the backdrop of a favourable environment in the games market. Achieved double-digit revenue growth in all Global, Creative, Media and Other services. From Q2 of the current financial year, the DIGITAL HEARTS CROSS Group (DHX, formerly Metaps Entertainment Limited, acquired in March 2021), which was acquired through M&A, has also made a significant contribution to results.

FY2023/3 full-year forecast: the company expects high growth to continue and boots dividend payment.

The company expects full-year sales to rise 20% yoy, with Enterprise Business driving growth. It plans to increase profits by 20% while accelerating growth investment. Sales of Enterprise Business are expected to grow by 34% yoy (to 15.3 billion yen) thanks to organic growth against a backdrop of progress in DX, as well as the full-year contribution by those companies acquired through M&A in FY2022/3. Meanwhile, Entertainment Business plans a 14% yoy increase in revenue (20.1 billion yen) due to the expansion of new services in response to changes in the market environment and the strengthening of the global field.

The good performance will be reflected in shareholder returns, with a record dividend increase of 6.0 yen a share.

Growth strategy

Medium-term management vision

Accelerate growth with Enterprise multiplied by Entertainment.

The company announced its medium-term management vision when it announced its financial results for FY2021/3, positioning the period from 2021 onwards as a period of development. The company then presented concrete measures, including specific numerical targets and measures to realise them. The grand design is to accelerate the growth of Enterprise Business by providing optimum QA solutions through strengthening human resources and technology, based on the stable growth of the highly profitable Entertainment Business. The goal is to become a “Global Quality Partner”. As has been reiterated, the company will accelerate the growth of Enterprise Business, which is the growth driver for the future, by leveraging the stable and highly profitable profits of Entertainment Business.

Growth story

Enterprise Business: providing optimal QA solutions to diverse needs at a high standard.

With the acceleration of DX and technological evolution, demand for software testing is growing, and specialisation is increasing, and there is a strong need for software testing outsourcing. In addition, the level of customer requirements is also becoming more sophisticated. The company, therefore, offers comprehensive testing, including non-functional testing such as security and load diagnosis, as well as test automation and other technologies to improve the efficiency of the testing process, rather than simply executing tests as in the past. Furthermore, the company plans to provide test consultancy in areas where testing techniques such as AI have not yet been established to offer a wide range of services, with an aim to contribute to the creation of a safe and secure digital society.

Realising a global level of talent, technology and process

In order to realise the above, the company promotes initiatives to raise the quality of its personnel, technology and processes to global standards. In terms of human resources, the company cooperates with software testing authorities at home and abroad, academically learning the know-how of testing authorities at the AGEST Academy and training test engineers in the latest researched technologies. On the technology front, the company will promote the research and practical application of new testing methods through the expansion of automation tools and collaboration with industry and academia. In terms of processes, the company aims to become a leading company in the software testing industry by quickly complying with ISO/IEC/IEEE 29119, a comprehensive international standard for software testing.

Numerical targets: in FY2024/3, target sales of 50 billion yen and ROIC of 15% or more.

Through the above measures for growth, the company has set a target of 50 billion yen in sales for FY2024/3, comprising over 25 billion yen in Enterprise Business (3-year CAGR of 40% or more inclusive of M&A and the synergies) and over 23 billion in Entertainment Business (domestic debugging; CAGR of 5-10% including M&A and the synergies, Global and others; CAGR of 30% or more including M&A and the synergies). To realise these targets, the company will carry out at least five M&As in the three years to FY2024/3. The number of domestic corporate clients will be doubled from 1,005 in FY2022/3 to 2,000 in FY2024/3. At the same time, the company will ensure ROIC of at least 15% (22.0% in FY2022/3), taking into account investment efficiency.

The management resolved on equity finance for M&A and other purposes.

On 30 June, the company announced a plan of equity finance through the issue of stock subscription rights with a revised exercise price (allotment date: 19 July 2022). These will be allocated to financial institutions, and the estimated amount raised is 4.24 billion yen (approximate net proceeds, if all the warrants are exercised at the initial exercise price). The funds will be used for: 1) standby funds for M&A of 2.94 billion yen; 2) repayment of past M&A funds of 1 billion yen; and 3) expenses for technological research and securing and training engineers of 300 million yen. The number of shares to be issued under the new warrants is 2,388,000 shares, including the 7th warrant and the 8th warrant. (10% of the total number of outstanding shares; however, the 7th warrant will be allocated to treasury shares).

Enterprise Business growth image

Stock information, etc.

Digital Hearts Holdings (3676) Share Price Trend (5Year-to-date)

Stock price observation

The shares rose on good results and a dividend boost. Will they head back up again from the adjustment phase?

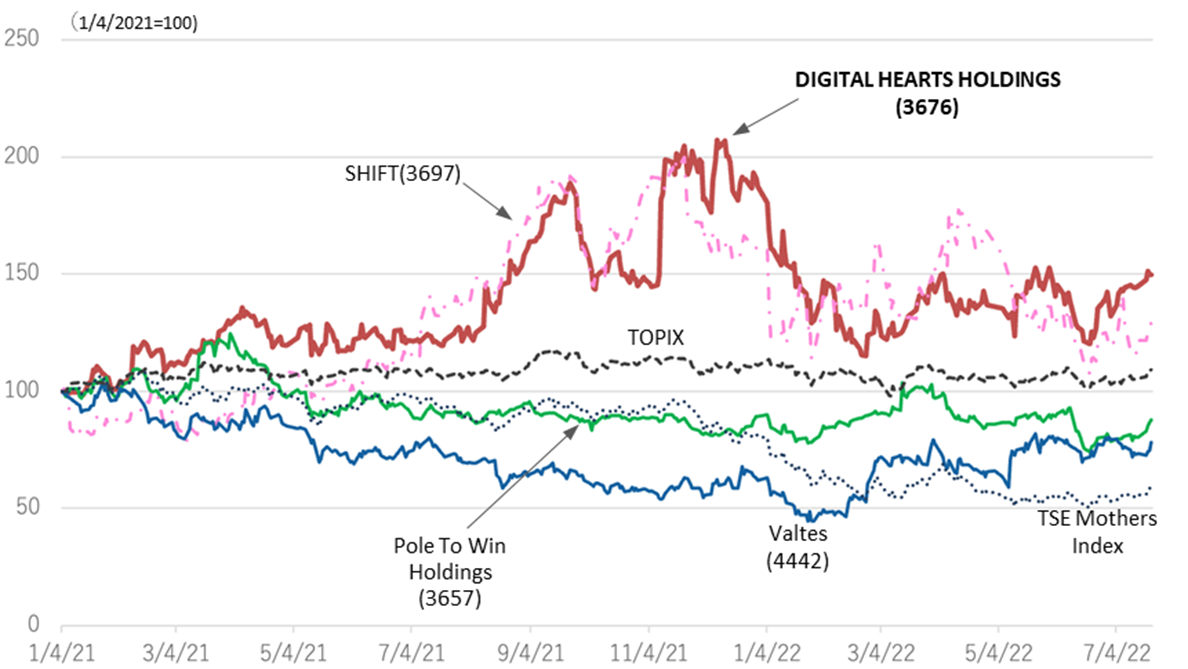

The company’s share price rose significantly on 13 May following the announcement of good results revealed on 12 May. The announcement of a forecast for a large dividend increase is also thought to have been well rated by investors. The company’s share price, which hit a record high of 2,700 yen on 13 December 2021, fell in the wake of the global growth stock correction. The stock market will continue to be affected by macroeconomic trends such as global economic conditions and geopolitical developments. However, the company’s performance is expected to continue to be strong, and it is expected to record its highest profits in FY2023/3. Hence, there should be little concern about share price formation in the future.

The chart below compares the share price performance of the four software testing companies. The price performance of the four companies has been maintained relative to the equity market, although their share prices have been down since last autumn following the global correction in growth stocks. The share prices of the company and SHIFT (TSE: 3697) are rated well, in view of the year-to-date negative share price performance of the other two companies and the TSE Mothers Index.

Share price performance (four software testing companies, TOPIX, TSE Mothers Index)

Historical PER/PBR (last five years)

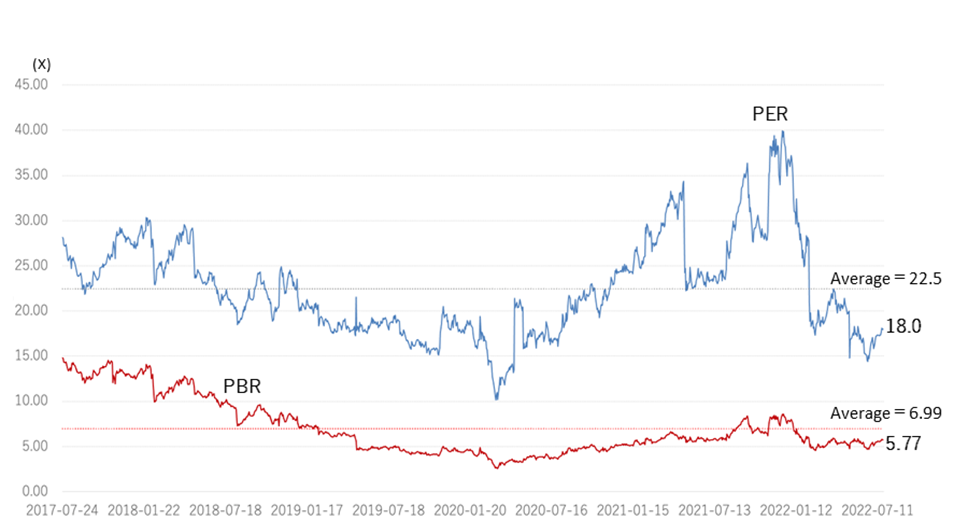

Thoughts on share price valuation

The company’s historical PER and PBR have been above the historical average for some time but are now below the average due to the adjustment in tech stocks (see above). Given the company’s recent strong earnings and its forecast for FY2023/3, when sales and profits are expected to increase further and the dividend to rise substantially, the shares are thought to be undervalued.

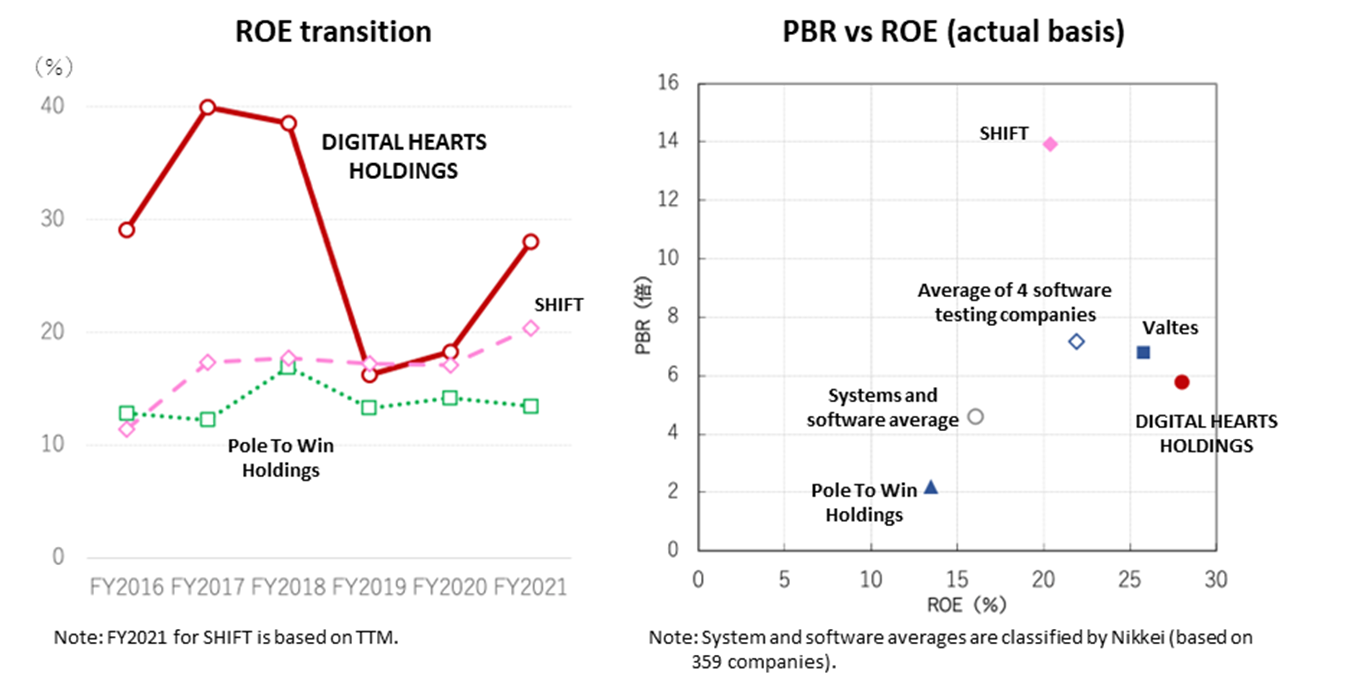

Meanwhile, the chart below compares financial indicators of the systems and software sector. The company’s high asset turnover, combined with its financial leverage, gives it a higher ROE than Pole To Win Holdings (TSE: 3657) and SHIFT (TSE: 3697). In terms of PBR vs ROE, the company’s ROE is well above that of its software testing competitors and the systems software industry average, but it is not fully reflected in PBR.

See the table on the next page for a comparison of the share price and financial data of the four software testing companies. Regarding PER, SHIFT stands out: its sales composition is more than 90% enterprise, and investors rated the company’s rapid expansion of its performance through M&A highly. Digital Hearts Holdings also has an enterprise ratio of approximately 40% and has steadily delivered results through business expansion via M&A. Considering that the company expects its sales to continue to grow at a CAGR of 30%-40%, mainly in Enterprise Business, and that Entertainment Business is generating stable and high profits, we would think that there is a good upside to the company’s shares.

Software Testing four Companies Comparison

| Code | 3676 | 3657 | 3697 | 4442 | |

| Company name | DIGITAL HEARTS HOLDINGS |

Pole To Win Holdings |

SHIFT | Valtes | |

| Financial year | March, 2022 | January, 2022 | August, 2021 | March, 2022 | |

| Share price (7/22) | 1,811 | 1,020 | 19,050 | 1,720 | |

| Market cap. (milion yen) | 44,606 | 38,919 | 339,302 | 12,298 | |

| PER (x) | 22.7 | 18.3 | 72.5 | 28.1 | |

| PBR (x) | 5.77 | 2.20 | 13.91 | 6.80 | |

| Dividend yield (%) | 0.8 | 1.5 | – | – | |

| Share price increase since the beginning of the year |

-20.3% | -2.0% | -20.2% | 26.4% | |

| Yearly high | 2,343(1/4) | 1,224(3/16) | 26,990(4/14) | 1,828(7/1) | |

| Yearly low | 1,405(2/24) | 856(6/20) | 15,560(6/20) | 963(1/28) | |

| 10-year high | 2,700(21/12/13) | 1,585.0(18/9/27) | 29,580(21/11/18) | 3,390(20/10/22) | |

| 10-year low | 552(20/3/23) | 335.0(13/1/9) | 640(16/2/12) | 751(20/3/23) | |

| Financial indicators (%) | |||||

| ROE | 28.03% | 12.52% | 10.42% | 25.78% | |

| ROA | 11.16% | 9.57% | 10.80% | 15.13% | |

| ROIC | 16.14% | 11.96% | 10.80% | 22.13% | |

| Equity Ratio | 39.7% | 79.2% | 65.4% | 60.2% | |

| Per Share Indicators | |||||

| Number of shares outstanding at end of period (thousand shares) |

23,890 | 38,156 | 17,811 | 7,150 | |

| EPS (yen) | 82.4 | 59.2 | 162.71 | 60.17 | |

| BPS (yen) | 323.8 | 467.2 | 1,277.48 | 252.85 | |

| DPS (yen) | 15.00 | 14.00 | 0.00 | 0.00 | |

| Financial data | |||||

| Net sales | 29,179 | 34,252 | 46,055 | 6,707 | |

| Three-year growth rate | 14.9% | 13.0% | 53.2% | 26.9% | |

| Gross profit | 8,391 | 9,717 | 13,913 | 1,866 | |

| Gross profit margin | 28.8% | 28.4% | 30.2% | 27.2% | |

| Operating profit | 2,701 | 3,305 | 3,995 | 570 | |

| Three-year growth rate | 18.9% | 1.5% | 49.3% | 44.5% | |

| Operating profit margin | 9.3% | 9.6% | 8.7% | 8.5% | |

| Net profit attributable to owners of the parent |

1,781 | 2,241 | 2,819 | 414 | |

| Three-year growth rate | 4.2% | 6.8% | 97.1% | 40.9% | |

| Net profit margin | 6.1% | 6.5% | 6.1% | 6.2% | |

| Number of employees at end of term | 1,683 | 2,466 | 4,440 | 546 | |

| Three-year growth rate | 25.0% | 16.1% | 51.7% | 23.8% | |

| Sales per Employee (thousand yen) | 17,337 | 13,890 | 10,361 | 12,283 | |

| EBITDA | 3,429 | 4,199 | 5,199 | 627 | |

| EBITDA margin | 11.8% | 12.3% | 11.3% | 9.3% | |

| Statements of Cash Flows | |||||

| Cash flow from operating activities | 3,077 | 1,844 | 4,758 | 505 | |

| Cash flow from investing activities | -2,537 | -2,662 | -5,433 | -104 | |

| Cash flow from financing activities | -547 | -660 | 8,286 | -236 | |

| Free cash flow | 540 | -818 | -675 | 401 | |

| Sales Composition | |||||

| Enterprise | 39.4% | – | 90.7% | 100.0% | |

| Entertainment | 60.6% | – | 9.3% | 0.0% | |

Major shareholders

| Name | Number of shares owned |

Ratio of the number of shares owned to the total number of issued shares (%) |

| Eiichi Miyazawa | 9,184,714 | 42.46 |

| NORTHERN TRUST CO. (AVFC) RE FIDELITY FUNDS | 1,882,156 | 8.70 |

| The Master Trust Bank of Japan (Trust Account) | 1,837,900 | 8.50 |

| Custody Bank of Japan, Ltd. (Trust Account) | 1,383,400 | 6.40 |

| A-1 LLC | 1,324,900 | 6.13 |

| FIDELITY INVESTMENT TRUST: FIDELITY JAPAN FUND | 307,692 | 1.42 |

| STATE STREET BANK AND TRUST COMPANY 505103 | 231,000 | 1.07 |

| UBS AG LONDON A/C IPB SEGREGATED CLIENT ACCOUNT | 220,300 | 1.02 |

| FIDELITY INVESTMENT TRUST: FIDELITY PACIFIC BASIN FUND | 193,000 | 0.89 |

| NORTHERN TRUST CO. (AVFC) SUB A/C NON TREATY | 147,000 | 0.68 |

| Total | 16,712,062 | 77.26 |

| Number of shares issued and outstanding | 23,890,800 |

Note: The company holds 2,260,031 treasury shares but is excluded from the above major shareholders. The percentage of shares held to the total number of shares issued (%) excludes treasury shares.

Source : The Company annual report (FY2022/3)

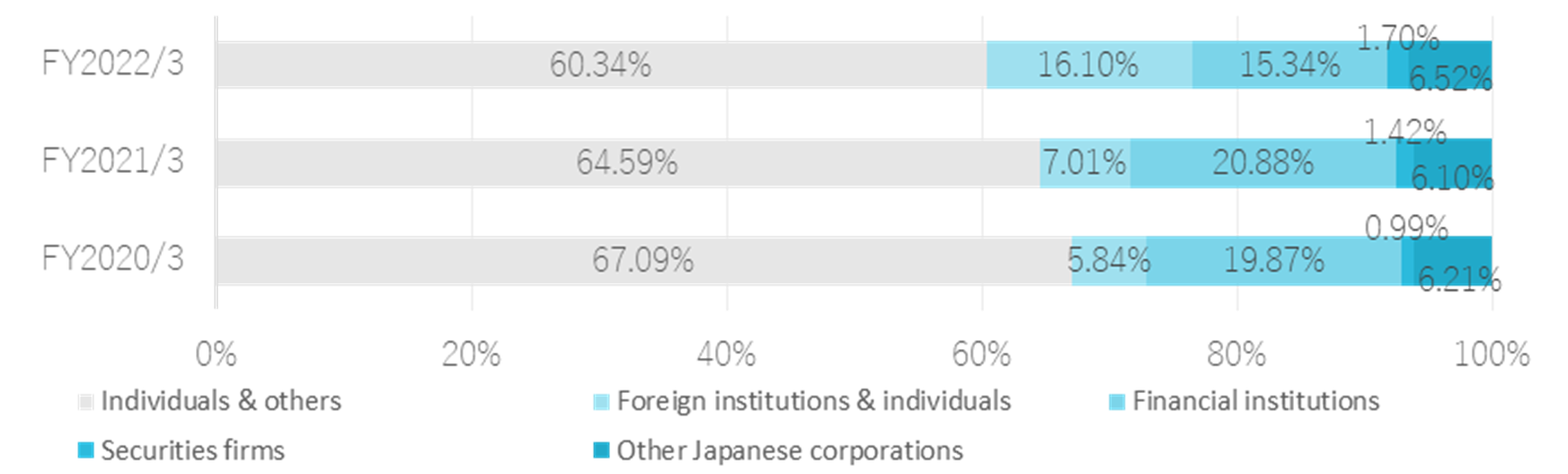

Founder Eiichi Miyazawa and his asset management company, A-1 LLC, together own 48.59% of the company. The recent strong performance of the company’s share price has led to an increase in the shareholding of foreign institutions, and foreign funds are also among the top shareholders.

Shareholding by ownership

Shareholder return policy

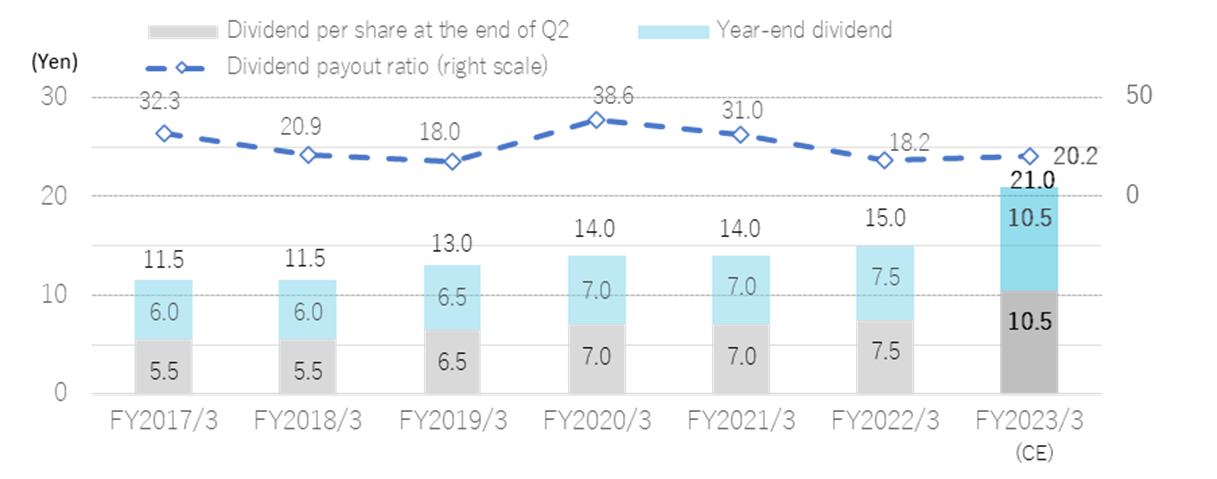

The company regards shareholder returns as an important management issue and has a policy of paying stable dividends with a target dividend payout ratio of around 20%, while securing the internal reserves needed to invest in business growth and reinforce the management strength. In line with this policy, the company has increased its dividend almost every year and plans to significantly increase the dividend for FY2023/3 in view of the strong business performance.

Dividends

Corporate governance and the top management

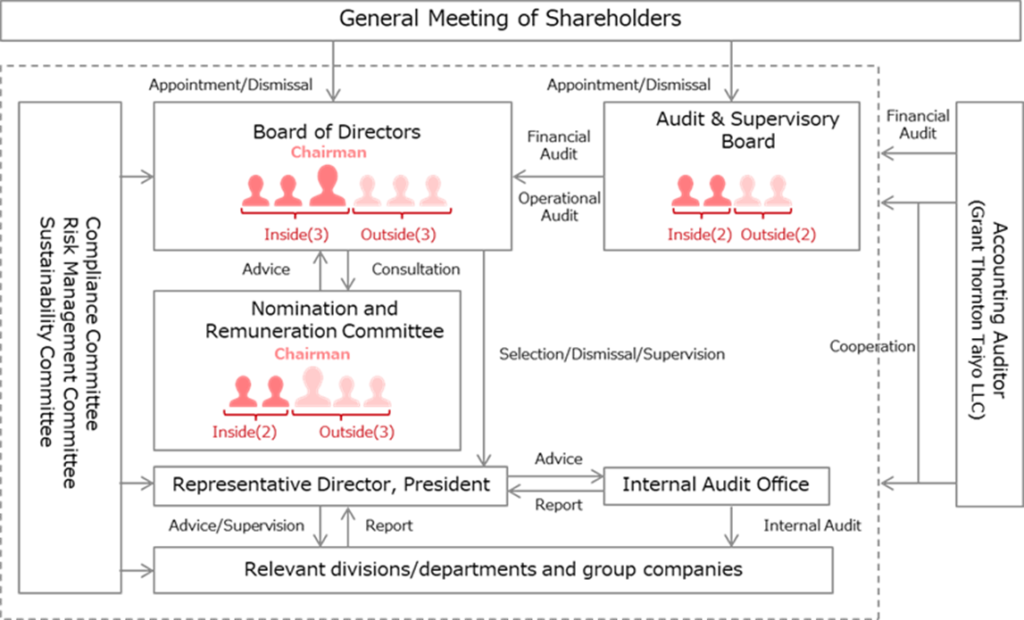

The company is a company with a board of auditors and has one full-time auditor. 6 directors were elected at the General Meeting of Shareholders in June 2022. Half (three) of them are outside directors. Two of the outside directors are designated as independent directors. Of the total of 10 directors and auditors, eight are male, and two are female. All nationalities are Japanese (see next page, references). The new corporate governance code requires diversity, including gender and internationality, as a prerequisite for ensuring the effectiveness of the board of directors and board of auditors. Although no exact description is available, it is assumed that, due to repeated mergers and acquisitions, including overseas, a significant number of the 1,683 employees (at end-March 2022) are from overseas. The company plans to accelerate its growth strategy in global markets as part of its medium-term management vision, and further diversity in the management team is expected from a corporate governance perspective.

The company has also established a voluntary Nomination and Remuneration Committee as an advisory body to the Board of Directors to ensure fairness and objectivity in decision-making on management nominations and remuneration, including for group companies, and to strengthen corporate governance functions. The committee consists of three outside directors, the President and CEO and Director and Chairman, and is chaired by an outside director.

The company’s corporate governance structure

See the next page for the company’s top management. As previously mentioned, a new management team of President and CEO Ninomiya and Executive Vice President and CFO Tsukushi was established in June 2021. Both will be supported by Director and Chairman Miyazawa from the perspective of the company’s founder.

Management

Representative Director, President and CEO: Yasumasa Ninomiya

Born in 1972.

He served as a director of U-NEXT Co., Ltd. (currently USEN-NEXT Holdings) and executives of its group companies. Joined us in 2017 and promoted the launch of Enterprise Business as a director in charge of this division.

Appointed Representative Director, President and CEO in 2021.

Director and Chairman: Eiichi Miyazawa

Born in 1972.

He established the original business of DIGITAL HEARTS in 2001 and rapidly expanded it by launching a unique business model utilizing diverse human resources such as core gamers.

In 2013, shifting to a holding company structure, he became its Representative Director, President and CEO, and in 2017 he was appointed Director and Chairman.

Director, Executive Vice President and CFO: Toshiya Tsukushi

Born in 1965.

After working for a consulting company and a financial institution, he promoted the formulation of growth strategies as a director, executive officer and CFO of Nissen Holdings Co., Ltd.

Joined us in 2017 and promoted M&A deals as Director and CFO.

Appointed Director, Executive Vice President and CFO in 2021.

Outside Director: Takashi Yanagiya

Born in 1951.

At Nomura Securities Co., Ltd., he served as Representative Director, Senior Managing Director and as other titles of officers. Appointed as our Outside Director in 2014.

Outside Director: Emiko Murei

Born in 1969.

She is a certified public accountant, and currently serves as the head of her own accounting firm while serving as an associate professor of Aoyama Gakuin University Graduate School of Professional Accountancy.

Appointed as our Outside Director in 2022.

Outside Director: Ryo Chikasawa

Born in 1984.

He is qualified as an attorney and currently serves as a partner lawyer at Mori Hamada & Matsumoto.

Appointed as our Outside Director in 2022.

Standing Audit & Supervisory Board Member: Masahide Date

Born in 1971.

After working for KAIBUNDO PUBLISHING CO., LTD., he joined DIGITAL HEARTS Co., Ltd. in 2002. After serving in the Accounting Section Manager of the Administration Department, he was appointed as an Audit & Supervisory Board Member of the company in 2005.

Appointed as our Audit & Supervisory Board Member in 2013.

Audit & Supervisory Board Member: Keiya Kazama

Born in 1975. Holds certified public accountant and tax accountant qualifications. After working for Deloitte Touche Tohmatsu (currently Deloitte Touche Tohmatsu LLC), he joined DIGITAL HEARTS Co., Ltd. in 2010.

He served as General Manager of the Administration Division, Executive Officer, and Director at this company. Appointed as our director in 2013.

Appointed as our Audit & Supervisory Board Member in 2018.

Outside Audit & Supervisory Board Member: Toshifumi Nikawa

Born in 1948.

After working for financial institutions including The Mitsubishi Bank, Ltd. (currently MUFG Bank, Ltd.), he was appointed Outside Audit & Supervisory Board Member of DIGITAL HEARTS Co., Ltd. in 2008.

Appointed as our Outside Audit & Supervisory Board Member in 2013.

Outside Audit & Supervisory Board Member: Yoko Okano

Born in 1975.

She is qualified as an attorney. She has been affiliated with Gokita and Miura Law Office since 2006.

Appointed as our Outside Audit & Supervisory Board Member in 2021.

Directors’ skills matrix

| Name | Position | Director tenure |

Expertise/experience | |||||

| Business management, global |

Finance, accounting, M&A |

Legal, risk management |

ESG, sustainability |

IT (Quality and DX security) |

Sales and marketing |

|||

| Yasumasa Ninomiya | Representative Director, President |

3 | ● | ● | ● | ● | ||

| Eiichi Miyazawa | Director and Chairman | 9 | ● | ● | ● | ● | ||

| Toshiya Tsukushi | Executive vice president | 4 | ● | ● | ● | ● | ● | |

| Takashi Yanagiya | Outside director | 8 | ● | ● | ● | ● | ● | |

| Emiko Murei | Outside director | – | ● | ● | ||||

| Ryo Chikasawa | Outside director | – | ● | ● | ● | ● | ||

Source: Company materials

Sustainability

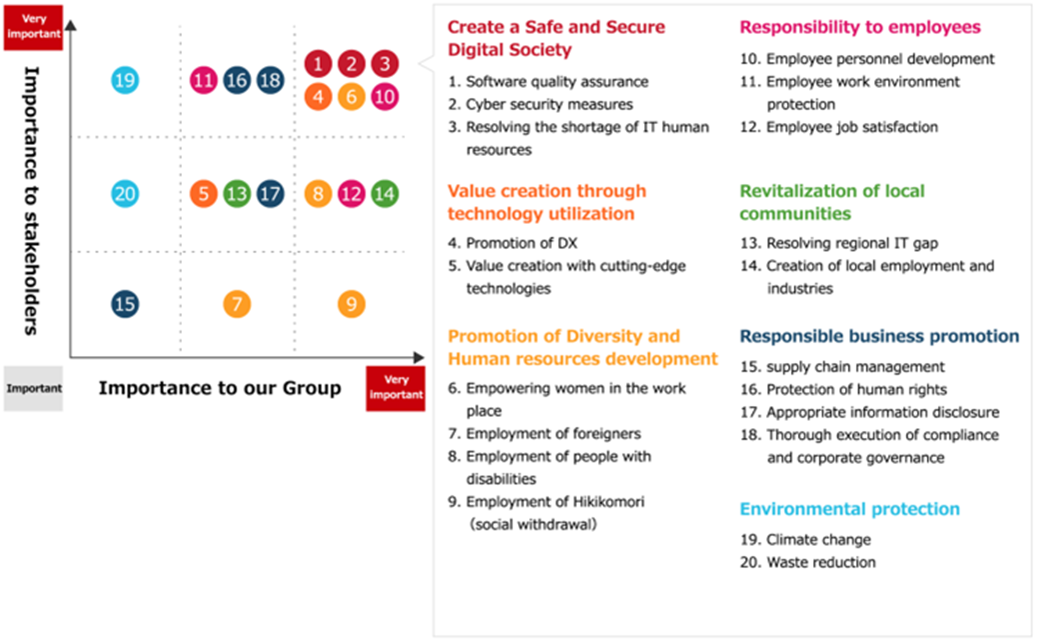

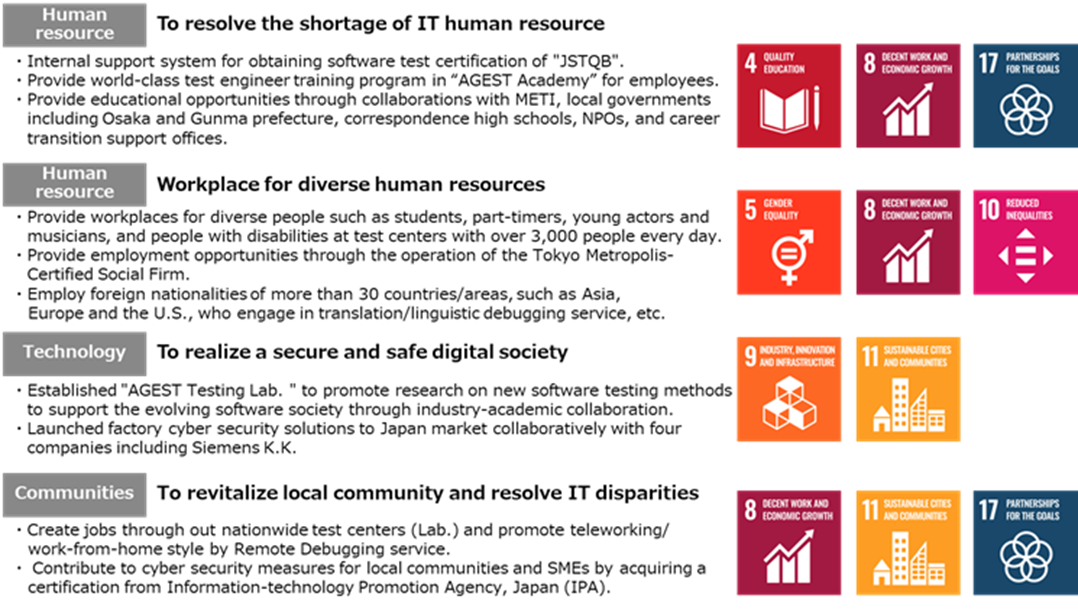

The company established a Sustainability Committee in March 2021, based on the belief that it is important to have a diverse workforce in realising its corporate mission, ‘SAVE the DIGITAL WORLD’. Various initiatives were launched based on the themes of ‘human resources’, ‘technology’ and ‘communities’. The importance to stakeholders and the importance to the Group are mapped out as a coordinate axis, and issues are resolved in order of priority.

The chart below shows examples of the company’s initiatives and how they relate to each of the SDGs’ goals. The system testing and cyber security services provided by the company build the foundations of industry and technological innovation through the creation of a safe and secure digital society. In addition, human resource development, one of the company’s key management tasks, contributes to alleviating the shortage of IT personnel in Japan. It is a little-known fact that the company has employed people from a wide range of backgrounds since its inception, contributing to the promotion of gender equality and decent work. Meanwhile, the company’s nationwide test centres (Lab.) are also helping to eliminate regional IT disparities by creating jobs and industry in rural areas.

Mapping of social issues

Examples of the company group’s initiatives and their relation to each of the SDG’s targets

Financial data I (quarterly basis )

| (Unit: million yen) | 2020/3 | 2021/3 | 2022/3 | |||||||||

| 1Q | 2Q | 3Q | 4Q | 1Q | 2Q | 3Q | 4Q | 1Q | 2Q | 3Q | 4Q | |

| [Sales by segment] | ||||||||||||

| Net sales | 4,988 | 5,234 | 5,455 | 5,460 | 5,093 | 5,437 | 5,782 | 6,355 | 6,098 | 7,400 | 7,747 | 7,932 |

| YoY | 12.1% | 7.2% | 7.8% | 15.0% | 2.1% | 3.9% | 6.0% | 16.4% | 19.7% | 36.1% | 34.0% | 24.8% |

| Enterprise Business | 954 | 1,140 | 1,133 | 1,794 | 1,523 | 1,540 | 1,710 | 2,246 | 2,029 | 2,833 | 3,074 | 3,553 |

| YoY | 46.3% | 41.5% | 32.0% | 82.5% | 59.6% | 35.1% | 50.9% | 25.2% | 33.2% | 83.9% | 79.7% | 58.2% |

| Composition of sales | 19.1% | 21.8% | 20.8% | 32.9% | 29.9% | 28.3% | 29.6% | 35.3% | 33.3% | 38.3% | 39.7% | 44.8% |

| System testing | 430 | 570 | 488 | 924 | 788 | 777 | 937 | 1,078 | 1,018 | 1,144 | 1,233 | 1,558 |

| YoY | 65.8% | 99.5% | 33.5% | 91.4% | 83.1% | 36.2% | 92.0% | 16.7% | 29.2% | 47.2% | 31.5% | 44.5% |

| Composition of sales | 8.6% | 10.9% | 8.9% | 16.9% | 15.5% | 14.3% | 16.2% | 17.0% | 16.7% | 15.5% | 15.9% | 19.6% |

| IT services and security | 523 | 569 | 645 | 869 | 735 | 763 | 772 | 1,167 | 1,011 | 1,688 | 1,841 | 1,995 |

| YoY | 33.4% | 9.5% | 30.9% | 73.9% | 40.4% | 34.1% | 19.8% | 34.3% | 37.5% | 121.2% | 138.2% | 70.9% |

| Composition of sales | 10.5% | 10.9% | 11.8% | 15.9% | 14.4% | 14.0% | 13.4% | 18.4% | 16.6% | 22.8% | 23.8% | 25.2% |

| Entertainment Business | 4,033 | 4,093 | 4,321 | 3,666 | 3,566 | 3,900 | 4,072 | 4,109 | 4,069 | 4,566 | 4,672 | 4,378 |

| YoY | 6.2% | 0.5% | 2.9% | -5.4% | -11.6% | -4.7% | -5.8% | 12.1% | 14.0% | 17.1% | 14.7% | 6.6% |

| Composition of sales | 80.9% | 78.2% | 79.2% | 67.1% | 70.0% | 71.7% | 70.4% | 64.7% | 66.7% | 61.7% | 60.3% | 55.2% |

| New sub-segments | ||||||||||||

| Domestic debugging | 2,681 | 2,846 | 2,953 | 3,054 | 2,931 | 3,030 | 3,149 | 3,011 | ||||

| YoY | – | – | – | – | 9.3% | 6.4% | 6.7% | -1.4% | ||||

| Composition of sales | 52.7% | 52.4% | 51.1% | 48.1% | 48.1% | 41.0% | 40.7% | 38.0% | ||||

| Global and others | 887 | 1,049 | 1,118 | 1,054 | 1,137 | 1,536 | 1,522 | 1,366 | ||||

| YoY | – | – | – | – | 28.2% | 46.3% | 36.1% | 29.6% | ||||

| Composition of sales | 17.4% | 19.3% | 19.3% | 16.6% | 18.7% | 20.8% | 19.7% | 17.2% | ||||

| Old sub-segments | ||||||||||||

| Debugging | 3,444 | 3,480 | 3,730 | 3,167 | 3,023 | 3,235 | 3,375 | 3,424 | – | – | – | – |

| YoY | 10.8% | 6.0% | 6.8% | -1.5% | -12.2% | -7.0% | -9.5% | 8.1% | – | – | – | – |

| Composition of sales | 69.1% | 66.5% | 68.4% | 58.0% | 59.4% | 59.5% | 58.4% | 53.9% | – | – | – | – |

| Game Consoles | 1,186 | 1,056 | 1,341 | 1,126 | 1,023 | 1,147 | 1,258 | 1,402 | – | – | – | – |

| YoY | 21.1% | 5.4% | 15.9% | 10.7% | -13.7% | 8.6% | -6.2% | 24.5% | – | – | – | – |

| Composition of sales | 23.8% | 20.2% | 24.6% | 20.6% | 20.1% | 21.1% | 21.8% | 22.1% | – | – | – | – |

| Mobile solutions | 2,013 | 2,171 | 2,141 | 1,848 | 1,819 | 1,959 | 2,005 | 1,870 | – | – | – | – |

| YoY | 1.0% | 1.7% | 2.0% | -4.9% | -9.6% | -9.8% | -6.4% | 1.2% | – | – | – | – |

| Composition of sales | 40.4% | 41.5% | 39.2% | 33.8% | 35.7% | 36.0% | 34.7% | 29.4% | – | – | – | – |

| Amusement | 245 | 253 | 248 | 193 | 179 | 130 | 111 | 153 | – | – | – | – |

| YoY | 77.5% | 75.7% | 4.6% | -24.3% | -26.9% | -48.6% | -55.2% | -20.7% | – | – | – | – |

| Composition of sales | 4.9% | 4.8% | 4.5% | 3.5% | 3.5% | 2.4% | 1.9% | 2.4% | – | – | – | – |

| Creative | 350 | 307 | 282 | 285 | 311 | 367 | 372 | 398 | – | – | – | – |

| YoY | -31.4% | -45.2% | -33.1% | -27.6% | -11.2% | 19.6% | 32.0% | 39.2% | – | – | – | – |

| Composition of sales | 7.0% | 5.9% | 5.2% | 5.2% | 6.1% | 6.8% | 6.4% | 6.3% | – | – | – | – |

| Media and others | 238 | 306 | 308 | 212 | 234 | 294 | 324 | 286 | – | – | – | – |

| YoY | 35.5% | 32.6% | 8.7% | -19.4% | -1.5% | -3.9% | 5.0% | 34.5% | – | – | – | – |

| Composition of sales | 4.8% | 5.9% | 5.7% | 3.9% | 4.6% | 5.4% | 5.6% | 4.5% | – | – | – | – |

| Operating profit | 189 | 328 | 547 | 327 | 158 | 369 | 655 | 725 | 636 | 733 | 753 | 577 |

| YoY | -37.2% | -30.9% | 18.0% | -9.9% | -16.4% | 12.4% | 19.7% | 121.3% | 301.3% | 98.5% | 14.9% | -20.4% |

| Operating profit margin | 3.8% | 6.3% | 10.0% | 6.0% | 3.1% | 6.8% | 11.3% | 11.4% | 10.4% | 9.9% | 9.7% | 7.3% |

| Enterprise Business | -184 | 2 | 14 | 100 | -21 | -7 | 64 | 152 | 87 | 144 | 171 | 246 |

| YoY | – | – | – | – | – | – | 363.5% | 52.4% | – | – | 163.8% | 61.9% |

| Segment profit margin | -19.4% | 0.3% | 1.2% | 5.6% | -1.4% | -0.5% | 3.8% | 6.8% | 4.3% | 5.1% | 5.6% | 6.9% |

| Entertainment Business | 727 | 760 | 891 | 585 | 517 | 700 | 936 | 923 | 930 | 975 | 978 | 783 |

| YoY | 7.3% | -8.8% | 6.1% | -20.3% | -28.9% | -8.0% | 5.0% | 57.9% | 79.9% | 39.3% | 4.5% | -15.2% |

| Segment profit margin | 18.0% | 18.6% | 20.6% | 16.0% | 14.5% | 18.0% | 23.0% | 22.5% | 22.9% | 21.4% | 20.9% | 17.9% |

Source: Omega Investment from company materials

Financial data II (quarterly basis )

| (Unit: million yen) | 2020/3 | 2021/3 | 2022/3 | |||||||||

| 1Q | 2Q | 3Q | 4Q | 1Q | 2Q | 3Q | 4Q | 1Q | 2Q | 3Q | 4Q | |

| [Statements of income] | ||||||||||||

| Net sales | 4,988 | 5,234 | 5,455 | 5,460 | 5,093 | 5,437 | 5,782 | 6,355 | 6,098 | 7,400 | 7,747 | 7,932 |

| Cost of sales | 3,772 | 3,830 | 3,949 | 3,953 | 3,819 | 4,002 | 4,001 | 4,700 | 4,271 | 5,290 | 5,579 | 5,645 |

| Gross profit | 1,216 | 1,403 | 1,506 | 1,507 | 1,273 | 1,437 | 1,781 | 1,655 | 1,827 | 2,109 | 2,167 | 2,287 |

| SG&A expenses | 1.026 | 1,074 | 958 | 959 | 1,115 | 1,067 | 1,126 | 1,150 | 1,191 | 1,375 | 1,414 | 1,709 |

| Operating profit | 189 | 328 | 547 | 327 | 158 | 369 | 655 | 725 | 636 | 733 | 753 | 577 |

| Non-operating income | 3 | 2 | 1 | 1 | 38 | 10 | 24 | 5 | 38 | 31 | 12 | 30 |

| Non-operating expenses | 3 | 7 | 7 | 7 | 2 | 3 | 4 | 10 | 4 | 4 | 5 | 21 |

| Ordinary profit | 189 | 323 | 542 | 542 | 194 | 376 | 675 | 720 | 670 | 760 | 759 | 587 |

| Extraordinary income | 0 | 0 | 0 | 19 | 32 | 13 | 66 | 1 | 1 | |||

| Extraordinary expenses | 0 | 0 | 75 | 82 | 13 | 16 | 415 | 2 | 42 | 32 | 35 | |

| Net profit before income taxes | 189 | 323 | 542 | 240 | 113 | 381 | 691 | 318 | 681 | 785 | 730 | 552 |

| Total income taxes | 77 | 159 | 162 | 99 | 38 | 122 | 224 | 145 | 189 | 281 | 233 | 38 |

| Net profit attributable to owners of the parent |

112 | 165 | 375 | 139 | 99 | 256 | 438 | 180 | 487 | 429 | 445 | 417 |

| [Balance Sheets] | ||||||||||||

| Current assets | 6,717 | 7,574 | 7,710 | 7,453 | 6,648 | 7,291 | 8,017 | 9,744 | 9,604 | 9,848 | 10,658 | 10,392 |

| Cash and deposits | 3,650 | 3,849 | 3,882 | 3,739 | 3,027 | 3,482 | 4,085 | 5,076 | 4,911 | 5,435 | 5,746 | 5,208 |

| Notes and accounts receivable | 2,677 | 3,017 | 3,013 | 2,985 | 2,889 | 3,099 | 3,201 | 4,097 | ||||

| Notes, accounts receivable and contract assets |

4,161 | 3,872 | 4,372 | 4,411 | ||||||||

| Non-current assets | 2,481 | 3,252 | 3,227 | 3,184 | 3,205 | 3,167 | 3,160 | 4,593 | 6,321 | 6,178 | 6,342 | 7,172 |

| Tangible fixed assets | 545 | 646 | 627 | 579 | 560 | 549 | 565 | 598 | 602 | 623 | 621 | 693 |

| Intangible fixed assets | 793 | 1,404 | 1,390 | 1,379 | 1,445 | 1,424 | 1,433 | 2,670 | 4,389 | 4,244 | 4,225 | 5,094 |

| Goodwill | 491 | 1,066 | 1,033 | 1,027 | 1,032 | 991 | 950 | 2,467 | 4,175 | 4,042 | 3,945 | 4,763 |

| Investments and other assets | 1,142 | 1,202 | 1,209 | 1,225 | 1,199 | 1,193 | 1,161 | 1,324 | 1,330 | 1,309 | 1,495 | 1,384 |

| Total assets | 9,199 | 10,827 | 10,938 | 10,637 | 9,854 | 10,459 | 11,177 | 14,338 | 15,925 | 16,026 | 17,001 | 17,565 |

| Current liabilities | 3,621 | 4,679 | 4,863 | 5,135 | 4,450 | 4,655 | 5,061 | 7,904 | 8,954 | 8,775 | 9,354 | 9,679 |