2026-04-06

Home

Japanese

Omega Investment Co., Ltd.

Daihen (Price Discovery)

Weak hold

Profile

Daihen Corporation manufactures, sells, and repairs power equipment, welding machines, industrial robots, and power supply equipment for semiconductor manufacturing systems. The company operates through three business segments: Energy Management, Factory Automation, and Material Processing, offering products that apply power control and automation technologies in each area. In the Energy Management segment, Daihen provides power equipment and systems that support the expansion of renewable energy usage and contribute to power infrastructure development. In the Factory Automation segment, the company supplies welding robots, industrial robots, and various systems for transportation, assembly, and processing, contributing to the automation and labour-saving of manufacturing sites. The Material Processing segment offers products utilising advanced energy control technologies for applications such as joining, cutting, film formation, surface treatment, and moulding of metals, semiconductors, and resin materials.

Sales by business segment % (OPM%): Energy Management 52 (9), Factory Automation 18 (12), Material Processing 30 (11), Others 0 (15) [Overseas] 21 (FY3.2024)

| Securities Code |

| TYO:6622 |

| Market Capitalization |

| 159,537 million yen |

| Industry |

| Electronic equipment |

Stock Hunter’s View

Stable demand in power infrastructure and semiconductors. The next focus lies on the medium-term plan and EMS growth.

Daihen was founded in 1919 as the only transformer specialist in Japan. The company continues to hold the top domestic market share for pole-mounted transformers and has since diversified its operations to include factory automation (FA) centred on welding robots, high-frequency power supplies, and wafer transfer robots in the semiconductor field.

Currently, the business is seeing a steady replacement demand for power distribution equipment and in-plant receiving facilities in Japan, along with growing sales of battery storage systems for renewable energy applications. Orders for transformers used in data centres are also intense, and the company aims to expand the production of large-scale transformers and storage systems in anticipation of continued demand. Daihen also plans to increase production of high-frequency power supply systems in line with rising semiconductor demand.

The recent announcement (on 4 February) of the third quarter results for the fiscal year ending March 2024 (April–December 2023) showed strong year-on-year performance, supported in part by the contribution of newly consolidated subsidiaries acquired in the previous half-year (Tohoku Electric Manufacturing and Shi-Hen Tech). Sales reached 155.825 billion yen (up 22.5% YoY), and operating profit was 10.256 billion yen (up 31.2% YoY). The company is on track to meet its full-year forecast (sales up 8.7%, operating profit up 5.6%). The next focus will likely be on achieving the medium-term targets of over 250 billion yen in sales and an operating margin exceeding 10% (i.e., 25 billion yen in operating profit).

By product, growth in EMS (Energy Management Systems) for renewable energy, which is expected to benefit from the full implementation of the Feed-in Premium (FIP) system and the expansion of data centres, is particularly noteworthy.

Investor’s View

Weak Hold. Low valuations, but rising debt weighs on ROIC, stalling economic value creation. It is a well-managed company, but the current share price appears sensibly priced at this point in its business cycle.

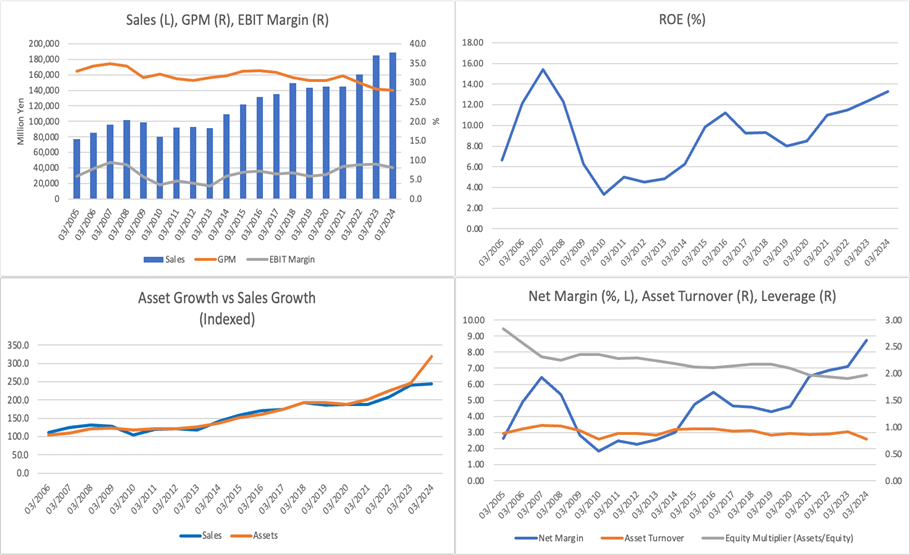

The company has steadily expanded its business performance in recent years. Particularly since FY2012, Daihen has reinforced its position as a research and development-driven company under its value creation initiative, the “DAIHEN Value Plan”. As a result, revenue has grown from 145.1 billion yen in FY2020 to 188.5 billion yen in FY2023, an increase of approximately 1.3 times.

Operating profit has also maintained a consistent growth trend. With an operating margin of 8.0%, the company delivers respectable profitability among manufacturing peers. Its product portfolio and efficient business operations have contributed to this success. In the latest results for the third quarter of FY2024 (April–December 2024), net profit declined to 7.6 billion yen (down 32.1% YoY) due to the absence of extraordinary gains recorded in the same period the previous year. Still, the company’s underlying earning power remains solid.

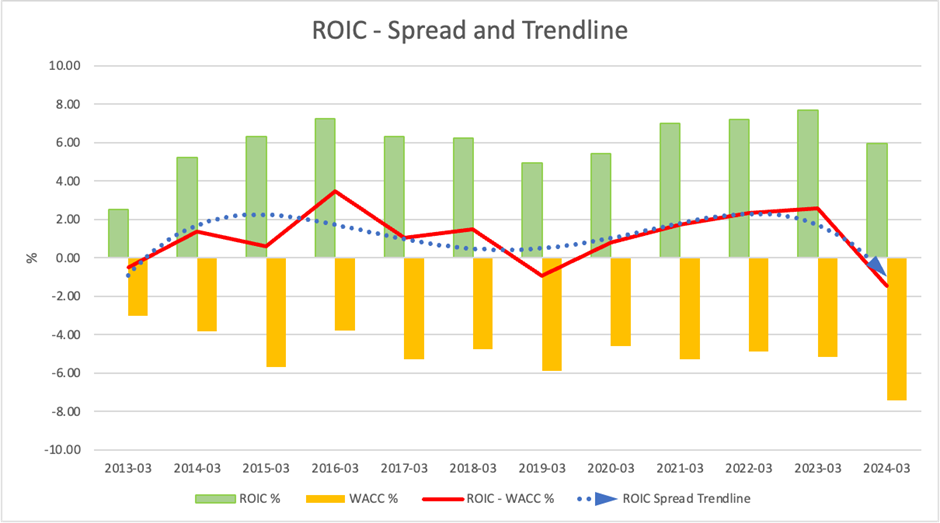

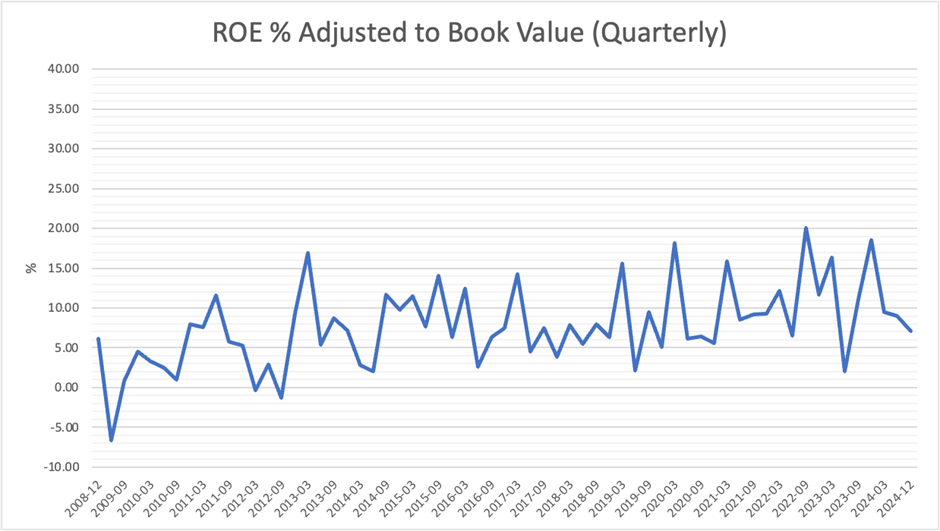

While ROE has exceeded the 12% target set in the FY2026 medium-term plan and is viewed favourably, the balance sheet has significantly changed due to acquisitions, resulting in a substantial debt increase. Consequently, ROIC has stagnated, and the company is currently in a position where economic value is barely created.

The capital investment cycle is likely to continue upward, and the company is pursuing a top-line growth strategy at the expense of ROIC. Although the stock trades at a demanding valuation—approximately 12x forward PER, around 1.1x PBR, and an equity yield of about 10% %—the outlook is uncertain. This phase involves substantial risk regarding whether the forthcoming growth investments will yield tangible results. While Daihen is an excellent company, its current share price seems sensibly priced, given its position in the business cycle.

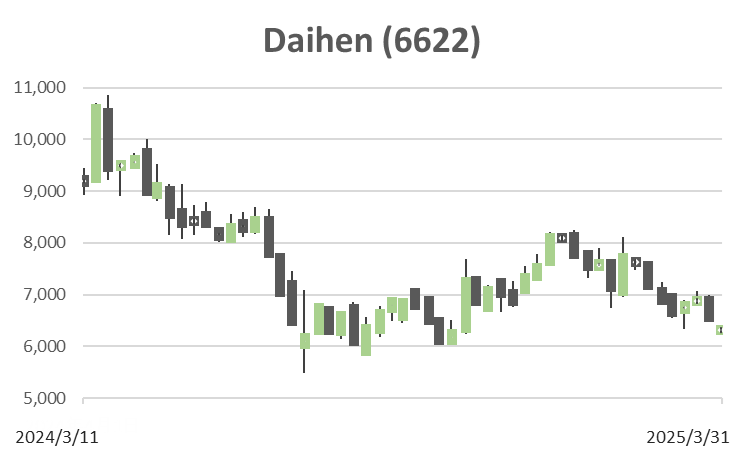

Price

PBR (LTM)

PER (LTM)

ROE (LTM)

EPS (LTM)

BPS (LTM)