2026-04-02

Home

Japanese

Omega Investment Co., Ltd.

CNS (Company note – 1Q update)

1Q FY25/5 results in-line with internal plan

Strategic increase in salaries and reinforcing new Consulting Business

| Click here for the PDF version of this page |

| PDF version |

SUMMARY

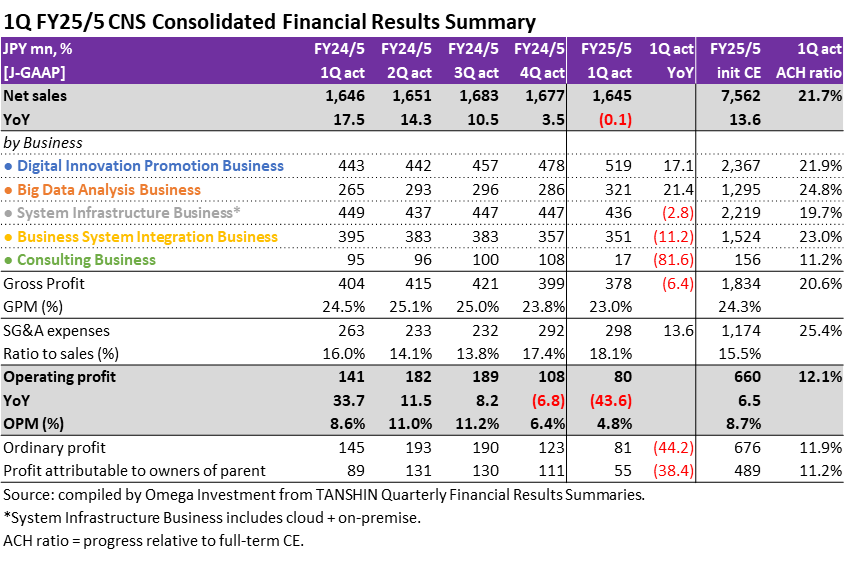

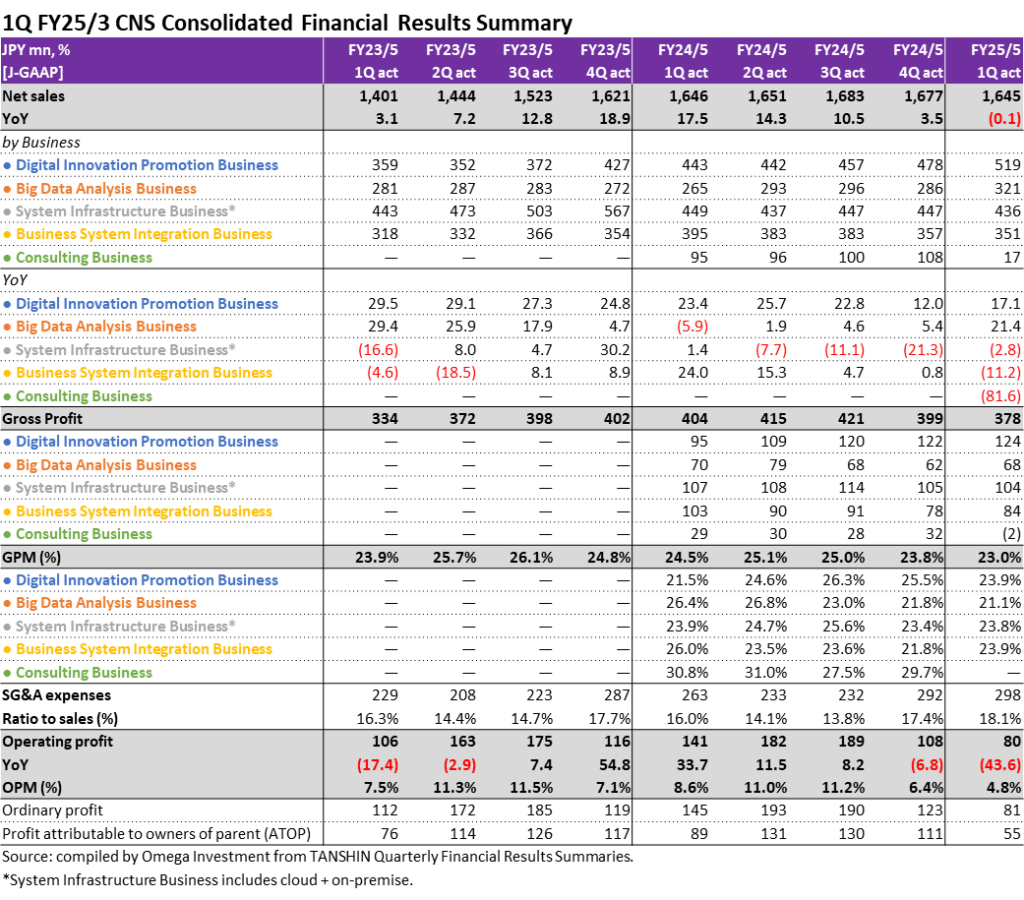

- CNS announced 1Q FY25/5 (Jun-Aug) results at 15:00 on October 11. Topline numbers were net sales -0.1% YoY, operating profit -43.6%, ordinary profit -44.2% and profit attributable to owners of parent -38.4%. According to the financial results supple-mentary explanation materials, the full-term initial forecast is weighted toward the 2H of the year, and 1Q profit margins were depressed as a result of implementation of the strategic salary increase of roughly 11% from the beginning of the fiscal year, as well as significant downsizing of the structure of the new Consulting Business with a view toward reconfiguration (net sales -81.6% YoY, see table on P2).

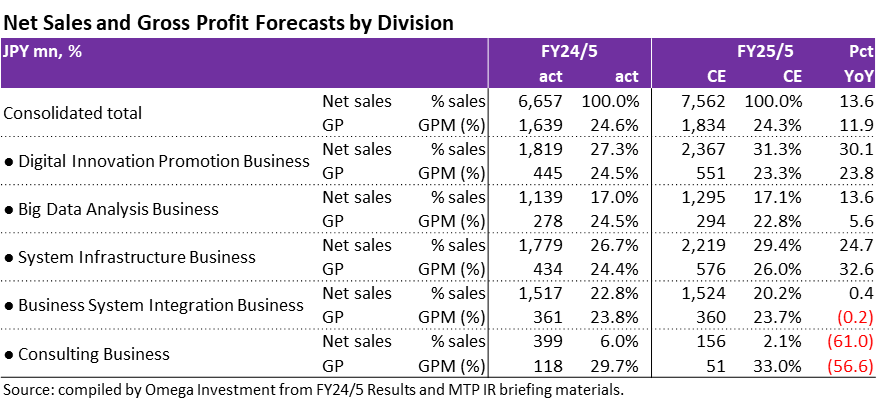

- As a recap from the results for FY24/5, in addition to poor performance of CNS Hokkaido, delayed startup of Consulting Business resulted in a 14.5% shortfall of profits from the initial full-term forecast. Newly launched Consulting Business started off with a shortage of consultants, and the business was commenced with existing engineers. Efforts were also focused on building a track record in business transformation design projects, but the inability to hire consultants as planned had a negative impact due to a lack of securing new consulting projects. Consulting Business net sales and gross profit recorded 20% and 30% shortfalls, respectively. The initial forecast for FY25/5 Consulting Business is net sales -61.0% YoY and GP -56.6% (see detailed initial forecasts on P3).

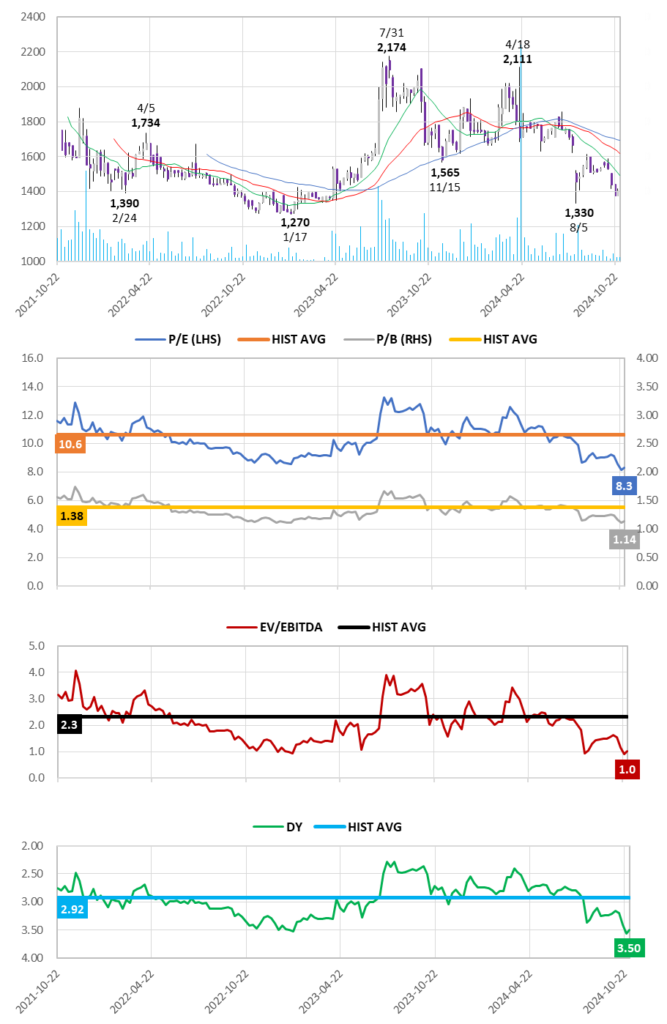

Financial Indicators

| Share price (10/31) | 1,401 | 25.5 P/E (CE) | 8.3x |

| YH (24/4/18) | 2,111 | 25.5 EV/EBITDA (CE) | 1.0x |

| YL (24/8/5) | 1,300 | 24.5 ROE (act) | 13.2% |

| 10YH (21/8/20) | 3,035 | 24.5 ROIC (act) | 12.6% |

| 10YL (23/1/17) | 1,270 | 24.8 P/B (act) | 1.14x |

| Shrs out. (mn shrs) | 2.906 | 25.5 DY (CE) | 3.50% |

| Mkt cap (¥ bn) | 4.071 | | |

| EV (¥ bn) | 0.709 | | |

| Equity ratio (8/31) | 75.8% | | |

1Q EARNINGS REVIEW AND FY25/5 FORECAST

- According to the 1Q TANSHIN financial results summary filing, the business environment for the CNS Group continued to show strong client demand for investing in DX toward transformation of business processes / business models, remaining brisk. Net sales of the Digital Innovation Promotion Business increased +17.1% YoY, with GPM increasing from 21.5% → 23.9%, driven by existing projects, new client projects related to ServiceNow, which were acquired in the previous fiscal year, expanded structure of cashless payment service projects, and new development projects from existing clients. Big Data Analysis Business net sales increased +21.4% YoY, relative to the low base of the same period the previous year, which was affected by a decrease in personnel due to organizational restructuring, the number of personnel available to handle projects increased due to an increase in career hires and business partner personnel, with an increase in personnel for existing projects, and several new clients were acquired.

- System Infrastructure Business net sales decreased slightly by -2.8% YoY, despite acquiring new end users leveraging the “U-Way Oracle Cloud VMware Solution Migration and Implementation Support Service,” due to the impact of the completion of projects at existing customers, the freezing of some projects due to customer circumstances, and delayed project starts. Business System Integration Business net sales decreased -11.2% YoY due to a significant reduction in the structure for operation and maintenance projects for some existing customers, and delayed startup of newly acquired projects relative to plan.

- As mentioned on P1, Consulting Business net sales decreased -81.6% YOY due to significant downsizing of the structure of the new Consulting Business with a view toward reconfiguration, however, the progress ratio was in-line with internal plan as a result of acquisition of new consulting projects and the early hiring of additional staff for existing projects.

- Following efforts to curtail external PR activities during the previous fiscal year, the ratio of SG&A expenses to sales during the 1Q increased from 16.0% → 18.1% due to an increase in the cost of hiring consultants who can be deployed immediately and the payment of increased fees for outsourcing back-office operations, and as a result, OP decreased -43.6% YoY. The impact of the salary increase of approximately 11% including the base up implemented at the beginning of the current fiscal year, including labor costs included in manufacturing cost of sales, is a 3pp increase in the personnel cost ratio compared to the previous period.

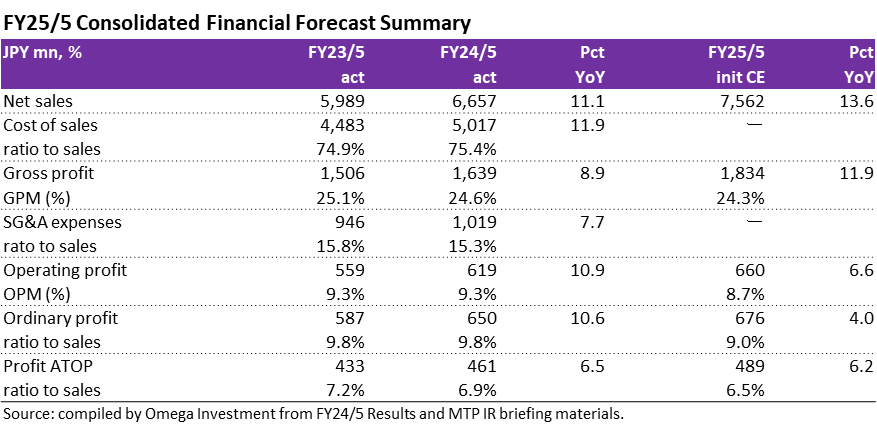

- The CNS Group will celebrate its 40th Anniversary since founding during FY25/5. Initial forecasts are summarized below. The main reason for the slowdown in profit growth relative to accelerating top line growth is factoring in implementation of a uniform 8% base increase and regular salary increases of approximately 11%, which are aimed at improving work ethic and attracting and retaining talented employees, as well as the anticipation of a certain level of expenses due to planned leading investments in innovation creation. The initial dividend indication is for a +1yen hike to ¥49 per share under the new progressive dividend policy (see details on the bottom of P5).

SHARE PRICE AND VALUATIONS

3-Year Weekly Share Price Chart, 13W/26W/52W MA, Volume and Valuation Trends

Source: compiled by Omega Investment from historical price data. Forecast values based on current Company estimates.

Key takeaways:

❶ The P/E and P/B ratios are trading 21% and 18% below their respective historical averages.

❷ EV/EBITDA on 1.0x is one of the lowest in the industry by far, and it is trading 55% below its historical average.

❸ The DY at 3.50% is one of the highest among peers, and some have yet to pay a dividend, trading 20% above its historical average.

➡ Even adjusting for the lower liquidity of the TSE Growth Market shown on the following page using the TSE Mothers index, CNS valuations are all trading at the bottom of their listing ranges, presenting a contradiction with the underlying strong earnings, and prospects for double-digit growth to continue for the next 4-5 years. Apparent weak 1Q results on the surface present an opportunity to buy on weakness.

3-Year Relative Share Price Performance versus Major Customers and Partners

Shareholder return policy

Expanding business by quickly identifying changes in the ICT industry and being proactive in taking on challenges in new fields, based on the trust and track record with major system integrators and ongoing relationships with them → these business characteristics enable CNS to secure stable revenues. In order to achieve sustainable growth together with share-holders, continuation of the progressive dividend policy to increase dividends in line with profit growth, with a target payout ratio of 30% or more.

Omega Investment’s case for CNS as an attractive opportunity

Omega Investment believes that CNS is one of those rare hidden gems among small cap growth companies waiting to be discovered. First, as an investor, it is reassuring that the Chairman and President are major shareholders, so their financial interests are directly aligned with shareholders. More importantly, management is taking steps to ensure a steady transition from the current DX-driven high market growth to sustainable growth regardless of underlying market conditions, including transforming the profit structure to higher margins not dependent on contract-based orders.