2026-07-27

Home

Japanese

Omega Investment Co., Ltd.

Chiome Bioscience (Company note – 4Q update)

| Share price (4/8) | ¥135 | Dividend Yield (24/12 CE) | – % |

| 52weeks high/low | ¥174/129 | ROE(TTM) | -83.6 % |

| Avg Vol (3 month) | 726.9 thou shrs | Operating margin (TTM) | -176.6 % |

| Market Cap | ¥7.4 bn | Beta (5Y Monthly) | 1.1 |

| Enterprise Value | ¥6.5 bn | Shares Outstanding | 52.634 mn shrs |

| PER (24/12 CE) | – X | Listed market | TSE Growth |

| PBR (23/12 act) | 6.23 X |

| Click here for the PDF version of this page |

| PDF Version |

Steady progress in Drug Discovery and Development Business. Drug Discovery Support Business is also steadily growing.

◇4Q FY12/2023 results summary

In 4Q FY12/2023 results, Chiome Bioscience (hereafter referred to as ‘the company’) reported steady growth in its Drug Discovery Support Business, with sales of 682 million yen (+8% YoY) and a slight reduction in losses in all profit categories from operating income onwards.

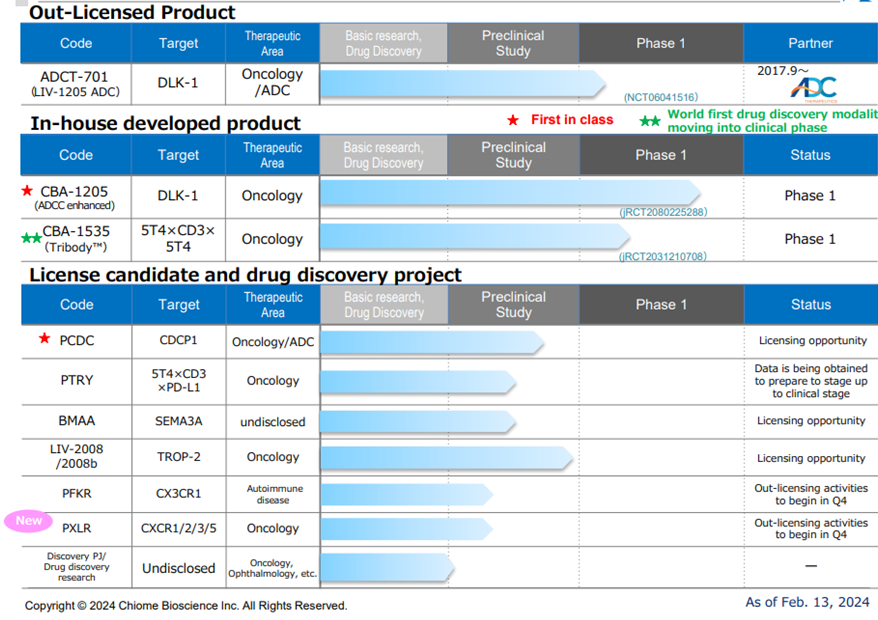

Regarding Q4 progress in the Drug Discovery and Development Business, the SD (stable disease) evaluation of the in-house pipeline CBA-1205 with tumour shrinkage in melanoma patients enrolled in the first part of the Phase 1 trial is continuing, and the drug has been administered continuously for more than 30 months. Additional supplies of active pharmaceutical ingredients (APIs) and investigational drugs have been initiated to support the second part of the Phase 1 study.

The National Cancer Institute (NCI) has completed an IND application for the out-licensed ADCT-701 for a phase I trial in the US and is preparing to start a clinical trial in paediatric neuroendocrine cancer.

Licensing activities to foreign companies for PCDC, which is in pre-clinical studies, continue. New out-licensing activities for PFKR and PXLR, also in pre-clinical studies, were initiated.

Sales in Drug Discovery Support Business exceeded forecasts with revenues of 682 million yen and segment profit of 399 million yen (+14% YoY). Transactions with existing customers are steadily increasing. In February 2024, a new basic agreement on outsourcing was signed with Takeda Pharmaceutical Co., Ltd., with whom the company had been conducting spot transactions, and further earnings growth is expected.

◇F12/2024 company forecasts and the highlights going forward

As it is difficult to calculate a reasonable forecast for the Drug Discovery and Development Business, only the sales of the Drug Discovery Support Business are disclosed. This is stated to be 720 million yen (+6% YoY).

The main focus of attention will be the progress of clinical trials for CBA-1205 and CBA-1535, which are in phase I trials, and the success or failure of the out-licensing of these and PCDC and other products. In recent years, the company has increasingly issued shares by exercising subscription rights to raise funds for research and development. Still, a successful out-licensing would raise expectations for medium- to long-term performance. At the same time, the company is likely to be profitable in a single year due to upfront payments and development milestone income. In addition, the company’s reliance on fundraising through new share issuance will be reduced as this will be the source of funds for research and development. As an essential turning point is approaching for the company, these out-licensing developments are likely to attract even more attention from the stock market than before.

| JPY, mn, % | Net sales | YoY % |

Oper. profit |

YoY % |

Ord. profit |

YoY % |

Profit ATOP |

YoY % |

EPS (¥) |

| 2019/12 | 447 | 110.3 | -1,401 | – | -1,410 | – | -1,403 | – | -44.61 |

| 2020/12 | 480 | 7.4 | -1,283 | – | -1,291 | – | -1,293 | – | -36.06 |

| 2021/12 | 712 | 48.3 | -1,334 | – | -1,329 | – | -1,479 | – | -36.74 |

| 2022/12 | 630 | -11.5 | -1,258 | – | -1,243 | – | -1,242 | – | -28.26 |

| 2023/12 | 682 | 8.2 | -1,205 | – | -1,217 | – | -1,220 | – | -24.62 |

| 2023/12 (CE) | – | – | – | – | – | – | – | – | – |

Note: The company discloses only the estimates for the Drug Discovery Support business (sales of 720 million yen), as it is difficult to make reasonable forecasts for the drug discovery and development business.

Source: Supplementary financial data for FY12/2023 (dated 13 February, 2024)

◇4Q FY12/2023 results: steady Drug Discovery Support Business expansion.

In the 4Q results for FY12/2023, the Drug Discovery Support Business achieved steady growth, with sales of 682 million yen (+8% YoY) and losses narrowing in operating income and all other profit categories.

The progress of each pipeline in the Drug Discovery and Development Business is shown in the diagram above. Each pipeline progresses well, but no sales were recorded during 4Q FY12/2023. Research and development costs within SG&A expenses amounted to 1,052 million yen (down 84 million yen YoY), a decrease due to CMC-related costs for CBA-1535 recorded in the previous year and no costs for the investigational formulation recorded in the current year. As a result, the segment loss for the business amounted to 1,052 million yen, corresponding to research and development costs.

The status of the pipeline is discussed below.

The Drug Discovery Support Business provides research support for antibody drugs to major domestic pharmaceutical companies by undertaking antibody generation, antibody affinity enhancement and protein preparation services using the company’s antibody generation technology platform, centred on its proprietary antibody production method, the ADLib® system. The stable revenue generated by the Drug Discovery Support Business helps to secure research and development expenditure for the Drug Discovery and Development Business.

Sales in this business exceeded forecasts with revenues of 682 million yen and segment profit of 399 million yen (+14% YoY). During the year under review, the company signed a new comprehensive outsourcing agreement with a major Japanese pharmaceutical company, started new outsourcing operations with a domestic diagnostics company, and commenced transactions with several new customers. In addition, the company is also promoting work with a national research and development corporation as a subcontractor for the generation of antibodies using the ADLib® system. In February 2024, the company signed a new basic agreement on outsourcing with Takeda Pharmaceutical Co., Ltd., with whom it had been conducting spot transactions.

With regard to BS, total assets at the end of December 2023 amounted to 1,629 million yen (a decrease of 463 million yen from the end of December 2022), and cash and deposits were 1,326 million yen (1,727 million yen at the end of December 2022). The company raised 555 million yen by issuing shares on the exercise of subscription rights, resulting in net assets of 1,158 million yen at the end of the year.

◇Progress in the pipeline: extending the plan to maximise the out-licensing value of CBA-1205

<In-house developed products>

*CBA-1205: A humanised anti-DLK-1 monoclonal antibody with enhanced ADCC activity. It is first-in-class. The Second half of Phase I clinical trials. Positive signs were observed in Phase I clinical trials. The company aims to obtain multiple PR cases in patients with hepatocellular carcinoma and maximise upfront licensing payments.

CBA-1205 is being tested in the first part of a Phase I clinical trial in patients with solid tumours at the National Cancer Centre. The second part of the study is being conducted in patients with hepatocellular carcinoma. In the first part, a high safety profile has already been confirmed, and the melanoma patients enrolled in the first part have continued to receive the drug for more than 30 months with SD (stable disease) evaluation with tumour shrinkage, which is still ongoing.

In addition, a partial response (PR: tumour reduction of 30% or more) was confirmed in one patient with hepatocellular carcinoma enrolled in the study’s second part.

To verify the drug’s therapeutic potential, the criteria for selecting patients for enrolment in clinical trials were tightened, and the clinical trial period was extended. The aim was to analyse the scientific relationship between PR cases and the drug’s administration. In response, additional manufacturing of the investigational drug was completed, and supply started in 4Q.

The second half of the Phase I clinical trial is scheduled to be completed in 2025, and business alliance and out-licensing activities will be conducted in parallel.

If multiple PR cases in hepatocellular carcinoma patients can be acquired, out-licensing is expected to gain momentum.

*CBA-1535; Humanised anti-5T4 and anti-CD3 multispecificity antibody. World’s first drug discovery modality. The first half of the Phase I clinical trial, with a second half part beginning in 2024.

In February 2022, the company submitted a clinical trial plan notification to the PMDA. At the end of June, it began administering the drug in Phase I clinical trials at the National Cancer Centre Hospital and Shizuoka Cancer Centre. Safety and efficacy signals were evaluated in patients with solid tumours in the first half of the Phase I clinical trial. The drug will be administered in stages, starting from a low volume to find the maximum dose that can be safely administered and to assess the initial drug effect signal.

In the second part, the drug’s efficacy in combination with cancer immunotherapy drugs will be efficiently evaluated. The second part is planned to start after the efficacy signal in the first part is confirmed, with the second part beginning in 2024.

CBA-1535 is the world’s first clinical trial of TribodyTM and, if the concept is confirmed, will expand the applicability of TribodyTM to many cancer antigens. The combination of the number of binding targets and the number of moves to which they bind is expected to provide benefits in terms of patient quality of life and healthcare economics, as it is expected to be more effective than conventional antibodies and to have multiple medicinal effects with only one dose of multiple drugs when administered in combination.

<Out-licensed products>

*ADCT-701; IND filing completed for Phase I clinical trials in the US.

Out-licensed to ADC Therapeutics, Switzerland, for ADC use only. In the US, an Investigational New Drug (IND) application has been completed for a Phase I clinical trial in paediatric neuroendocrine cancer, with the National Cancer Institute (NCI) as the lead developer.

<Out-licensing candidates>

*PCDC; First-in-class ADC targeting CDCP1, out-licensing activities continue.

PCDC is a humanised anti-CDCP1 antibody-drug conjugate (ADC) created by the company. Licensing activities target pharmaceutical companies with proprietary ADC technology that wish to use an antibody targeting CDCP1. Discussions are underway with many pharmaceutical companies, focusing on the scientific aspects.

CDCP1 is expressed in a wide range of solid tumours, including cancer types resistant to standard therapies, making the drug potentially first-in-class.

*PTRY; humanised anti-5T4, anti-CD3 and anti-PD-L1 multi-specific antibody; a Tribody™ antibody with the potential to add immune checkpoint inhibition to the T cell engager function of CBA-1535.

Early evaluations in animal models have shown strong anti-tumour effects. Results of joint research on cancer immunotherapy conducted with the Italian public research institute Ceinge-Biotechnologie Avanzate in the international journal ‘Journal of Experimental & Clinical Cancer Research.’ A patent application has been completed for the results obtained through this collaboration. In vivo efficacy data in a lung cancer model have confirmed that it exerts a strong tumour growth inhibitory effect.

The company focuses on research and development and exploring early licensing opportunities.

*PFKR; a humanised anti-CX3CR1 antibody that targets CX3CR1, a GPCR, and is a new out-licensing candidate in the area of autoimmune CNS, which the company is investigating in collaboration with the National Institute of Neurology and Psychiatry. A patent application with secondary progressive multiple sclerosis (SPMS) and other diseases as potential indications has been completed. The number of patients with multiple sclerosis is estimated to be around 7,000 in Japan and more than 3 million worldwide. Licensing activities have been initiated.

*PXLR; humanised anti-CXCL1/2/3/5 antibody; administration of XLR antibodies is expected to reduce immunosuppressive cells, overcome drug resistance and inhibit cancer recurrence. They are intended for solid tumours (e.g. gastric, breast and ovarian cancer).New out-licensing candidates that the company has been working on in collaboration with Osaka Public University. A patent application has been completed. Licensing activities have been newly initiated.

◇F12/2024 Full-year forecasts: sales in Drug Discovery and Development Business are in line with plans. Expect to be around the previous year’s level.

As it is difficult to calculate a reasonable forecast for the Drug Discovery and Development Business, only sales from the Drug Discovery Support Business are disclosed. This is estimated at 720 million yen (+6% YoY). As the customer base is being strengthened in this business, it is expected to continue to support R&D activities financially as a stable source of revenue.

◇Share price trend and the points of focus: watch the progress of clinical trials such as CBA-1205 and CBA-1535 and the out-licensing of PCDC.

The company’s share price performance over the past year is shown below. The share price has been slowly declining, but there are signs of a slight bottoming out.

One reason for the gradual decline in share prices appears to be the company’s current profit structure. Although the Drug Discovery Support Business is growing steadily, this alone has not been sufficient to fully cover R&D costs. As a result, the company has continued to raise the necessary funds by issuing shares through subscription rights and other means, and investors appear to have become aware of this.

However, it is worth noting that, as we saw earlier, steady progress is being made in expanding the pipeline, particularly in CBA-1205, where there are promising drug cases, given that CBA-1205 and CBA-1535 are scheduled to complete the late phase 1 part of their clinical trials by the end of 2025, From a schedule perspective, investors are becoming aware of the upside potential from licensing-out. If the company achieves licensing-out, investor sentiment will improve as the company will be able to generate a profit in a single year from the upfront payment income and gain R&D resources that are not from share warrants.

The share price, which has recently stopped falling, suggests that investors are aware of this upside. The progress of the company’s pipeline over the next 1-2 years will likely attract more attention.

Financial data

| FY (¥mn) | 2020/12 | 2021/12 | 2022/12 | 2023/12 | ||||||||||||

| 1Q | 2Q | 3Q | 4Q | 1Q | 2Q | 3Q | 4Q | 1Q | 2Q | 3Q | 4Q | 1Q | 2Q | 3Q | 4Q | |

| [Statements of income] | ||||||||||||||||

| Net sales | 91 | 82 | 139 | 169 | 246 | 139 | 157 | 171 | 128 | 149 | 156 | 197 | 169 | 189 | 165 | 159 |

| Drug Discovery and Development Business | 1 | 1 | 0 | 1 | 103 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Drug Discovery Support Business | 90 | 82 | 138 | 168 | 143 | 138 | 157 | 171 | 128 | 149 | 156 | 197 | 169 | 189 | 165 | 159 |

| Cost of sales | 61 | 46 | 59 | 70 | 64 | 62 | 78 | 86 | 57 | 69 | 72 | 83 | 73 | 76 | 67 | 68 |

| Gross profit | 30 | 36 | 80 | 99 | 182 | 77 | 79 | 84 | 70 | 80 | 84 | 114 | 95 | 112 | 98 | 94 |

| SG&A expenses | 456 | 346 | 424 | 303 | 337 | 337 | 515 | 568 | 557 | 373 | 344 | 334 | 321 | 545 | 344 | 394 |

| R&D expenses | 343 | 266 | 342 | 206 | 216 | 243 | 401 | 451 | 446 | 245 | 225 | 219 | 193 | 408 | 202 | 249 |

| Operating profit | -426 | -310 | -344 | -204 | -155 | -260 | -436 | -483 | -486 | -292 | -260 | -220 | -225 | -433 | -246 | -301 |

| Non-operating income | 2 | 0 | 3 | 0 | 7 | 0 | 2 | 4 | 0 | 16 | 0 | 5 | 0 | 0 | 1 | 0 |

| Non-operating expenses | 0 | 2 | 10 | 1 | 1 | 0 | 1 | 6 | 4 | 1 | 1 | -1 | 1 | 1 | 9 | 2 |

| Ordinary profit | -425 | -311 | -351 | -205 | -150 | -259 | -434 | -486 | -491 | -278 | -261 | -214 | -227 | -434 | -254 | -302 |

| Extraordinary income | 0 | 0 | 0 | 6 | 0 | 1 | 0 | 1 | 0 | |||||||

| Extraordinary expenses | 0 | 0 | 0 | |||||||||||||

| Loss before income taxes | -425 | -310 | -351 | -205 | -149 | -247 | -433 | -636 | -491 | -278 | -255 | -214 | -226 | -434 | -254 | -301 |

| Total income taxes | 1 | 0 | 1 | 1 | 11 | 1 | 1 | 0 | 1 | 2 | 1 | 1 | 1 | 1 | 1 | 2 |

| Net income | -425 | -311 | -352 | -206 | -161 | -248 | -434 | -637 | -492 | -279 | -257 | -215 | -227 | -435 | -254 | -304 |

| [Balance Sheets] | ||||||||||||||||

| Current assets | 2,309 | 2,805 | 3,316 | 3,249 | 3,294 | 3,088 | 2,675 | 2,216 | 2,005 | 1,792 | 1,955 | 2,092 | 1,964 | 1,566 | 1,633 | 1,629 |

| Cash and deposits | 1,967 | 2,472 | 2,881 | 2,686 | 2,580 | 2,302 | 2,071 | 1,790 | 1,744 | 1,471 | 1,592 | 1,727 | 1,566 | 1,245 | 1,341 | 1,326 |

| Non-current assets | 247 | 249 | 249 | 246 | 244 | 241 | 274 | 122 | 121 | 128 | 126 | 123 | 120 | 118 | 119 | 122 |

| Tangible assets | 10 | 9 | 8 | 7 | 6 | 6 | 4 | 4 | 3 | 3 | 2 | 2 | 2 | 1 | 1 | 1 |

| Investments and other assets | 237 | 240 | 241 | 238 | 237 | 235 | 269 | 118 | 117 | 124 | 122 | 120 | 118 | 117 | 117 | 121 |

| Total assets | 2,556 | 3,054 | 3,566 | 3,495 | 3,537 | 3,329 | 2,950 | 2,339 | 2,126 | 1,920 | 2,081 | 2,215 | 2,085 | 1,685 | 1,753 | 1,751 |

| Current liabilities | 315 | 427 | 378 | 343 | 378 | 428 | 468 | 392 | 419 | 390 | 376 | 370 | 469 | 486 | 4887 | 539 |

| Short-term borrowings | 142 | 199 | 199 | 180 | 180 | 190 | 199 | 183 | 183 | 188 | 188 | 184 | 304 | 298 | 316 | 291 |

| Non-current liabilities | 42 | 42 | 42 | 42 | 42 | 42 | 53 | 53 | 53 | 54 | 54 | 54 | 54 | 54 | 54 | 55 |

| Total liabilities | 357 | 469 | 420 | 385 | 420 | 470 | 522 | 446 | 473 | 444 | 431 | 424 | 523 | 540 | 542 | 594 |

| Total net assets | 2,199 | 2,585 | 3,146 | 3,110 | 3,118 | 2,859 | 2,428 | 1,893 | 1,653 | 1,476 | 1,650 | 1,790 | 1,562 | 1,144 | 1,211 | 1,157 |

| Total shareholders’ equity | 2,199 | 2,585 | 3,146 | 3,110 | 3,118 | 2,859 | 2,428 | 1,857 | 1,621 | 1,445 | 1,631 | 1,777 | 1,549 | 1,132 | 1,189 | 1,139 |

| Capital stock | 6,133 | 846 | 1,303 | 1,388 | 1,471 | 1,471 | 1,472 | 1,515 | 1,642 | 1,695 | 1,916 | 2,097 | 2,097 | 2,106 | 2,262 | 2,388 |

| Legal capital reserve | 6,123 | 2,446 | 2,903 | 2,987 | 3,071 | 3,071 | 3,072 | 3,115 | 3,242 | 3,295 | 3,516 | 3,696 | 3,696 | 3,706 | 3,861 | 3,988 |

| Retained earnings | -10,080 | -736 | -1,088 | -1,294 | -1,455 | -1,703 | -2,136 | -2,773 | -3,262 | -3,544 | -3,801 | -4,016 | -4,244 | -4,679 | -4,934 | -5,236 |

| Subscription rights to shares | 24 | 30 | 28 | 29 | 30 | 19 | 19 | 35 | 31 | 30 | 18 | 13 | 12 | 12 | 22 | 18 |

| Total liabilities and net assets | 2,556 | 3,054 | 3,566 | 3,495 | 3,537 | 3,329 | 2,950 | 2,339 | 2,126 | 1,920 | 2,081 | 2,215 | 2,085 | 1,685 | 1,753 | 1,751 |

| [Statements of cash flows] | ||||||||||||||||

| Cash flow from operating activities | -528 | -1,361 | -560 | -1,131 | -660 | -1,191 | -595 | -1,069 | ||||||||

| Loss before income taxes | -734 | -1,290 | -396 | -1,466 | -768 | -1,237 | -661 | -1,215 | ||||||||

| Cash flow from investing activities | – | 3 | – | -35 | – | – | 0 | 0 | ||||||||

| Purchase of investment securities | – | – | – | – | – | – | – | – | ||||||||

| Cash flow from financing activities | 894 | 1,944 | 176 | 271 | 341 | 1,127 | 113 | 667 | ||||||||

| Proceeds from issuance of common shares | 697 | 1,769 | 166 | 253 | 336 | 1,126 | – | 555 | ||||||||

| Net increase in cash and cash equiv. | 366 | 580 | -384 | -895 | -319 | -63 | -481 | -402 | ||||||||

| Cash and cash equiv. at beginning of period | 2,105 | 2,105 | 2,686 | 2,686 | 1,790 | 1,790 | 1,727 | 1,727 | ||||||||

| Cash and cash equiv. at end of period | 2,472 | 2,686 | 2,301 | 1,790 | 1,471 | 1,727 | 1,245 | 1,326 | ||||||||

Note) For the cash flow statement, Q2 is the cumulative of Q1 to Q2, and Q4 is the cumulative of Q1 to Q4. Therefore, the beginning balance will be the beginning balance of Q4 for both Q2 and Q4.

Source: Omega Investment from Company materials.