2026-07-27

Home

Japanese

Omega Investment Co., Ltd.

Nomura Micro Science (Price Discovery)

Buy

Conclusion

The shares are rated a Buy. Nomura Micro Science experienced the reactionary decline from large-scale US projects, a sharp decline in sales and profits, a large decline in ROE and EPS, deterioration in FCF, and a shift to net debt in FY3/2026, but the essence of this is not a structural decline in competitiveness, but a phase in which revenue recognition, contract assets, short-term borrowings, and working capital burden associated with large-scale water treatment equipment projects appeared intensively. The FY3/2027 company plan indicates a recovery to a record-high profit zone, with sales of 97.0 billion yen, operating profit of 16.0 billion yen, and EPS of 289.90 yen. The tailwinds from AI and memory investment, Korean semiconductor investment, and the global decentralisation of semiconductor manufacturing bases remain strong. The current share price of 4,700 yen is not a simple low-valuation stock, with a forecast PER of 16.2x and PBR of 4.58x. Assuming a recovery in ROE to 28%, it is difficult to say that the share price is excessively pricing this in. If the acquisition of large-scale orders, FCF normalisation, and a reduction in net debt are confirmed, there remains room for medium-term share price revaluation.

Profile

A dedicated manufacturer of ultrapure water production equipment for semiconductors and pharmaceuticals, whose growth is influenced by large-scale overseas projects in the US, South Korea, Taiwan, and other regions

Nomura Micro Science is a dedicated manufacturer of water treatment equipment, with a mainstay product line of ultrapure water production equipment used in manufacturing processes for semiconductors, liquid crystal displays, pharmaceuticals, biotechnology, food, and other fields. Its main businesses are the design, construction, and sale of water treatment equipment, maintenance, and sales of consumables. As customers’ capital investment scales and technological requirements rise with semiconductor miniaturisation, investment in advanced memory and in upgrading pharmaceutical plants expands the company’s business opportunities. By region, it operates in Japan, South Korea, China, Taiwan, the US, and other regions. Although FY3/2026 saw lower sales and profits due to the completion of large-scale US projects, the company plans a V-shaped recovery in FY3/2027, supported by a reacceleration of semiconductor-related investment. Because dependence on large-scale projects is high, sales, profits, ROE, and FCF tend to fluctuate significantly from year to year, but the fact that ultrapure water production equipment is indispensable infrastructure for semiconductor manufacturing supports the company’s medium- to long-term business value.

Sales ratio by business %: Water treatment equipment 65.3%, maintenance and consumables 33.1%, other 1.6% (FY3/2026). The company discloses profits by regional segment, and the operating profit margin by business is not disclosed.

| Securities Code |

| TYO:6254 |

| Market Capitalization |

| 190,858 million yen |

| Industry |

| Machinery |

Stock Hunter’s View

A dedicated manufacturer of ultrapure water production equipment indispensable for semiconductor manufacturing. The current March fiscal year is expected to see a V-shaped recovery.

Nomura Micro Science is a major manufacturer of ultrapure water production equipment used in semiconductor and liquid crystal display manufacturing processes, and its main customers are Samsung Electronics of South Korea and major semiconductor manufacturers in Taiwan. In terms of sales scale, it ranks next among Japanese players after Kurita Water Industries (6370) and Organo (6368). By regional sales, sales to the US account for just over 50%.

In the FY3/2026 results, orders halved due to the completion of large-scale water treatment equipment projects in the US, and sales and operating profit also declined sharply. On the other hand, in the current fiscal year, the company plans a V-shaped recovery, with sales of 97.0 billion yen (up 72.5% YoY) and operating profit of 16.0 billion yen (2.3x YoY). Semiconductor-related capital investment remains robust, and investment scale is also increasing, with orders in the water treatment equipment business expected to expand to 3.4x YoY. Enquiry conditions are strong for both semiconductor and pharmaceutical plant applications, and large-scale orders are expected towards mid-2026. Both orders and the order backlog are expected to reach record highs.

More recently, it has become clear that Samsung Electronics and SK Hynix will each build two new semiconductor manufacturing fabs in South Korea. The total investment amount will reach 800 trillion won (approximately 84 trillion yen), and it is highly likely to become a medium- to long-term tailwind for Nomura Micro Science. South Korea aims to double DRAM manufacturing capacity over the next five years.

Investor’s View

If the deterioration in financial conditions in FY3/2026 is viewed as the trough of the large-scale project cycle, the share price can be assessed as still reflecting a medium-term recovery.

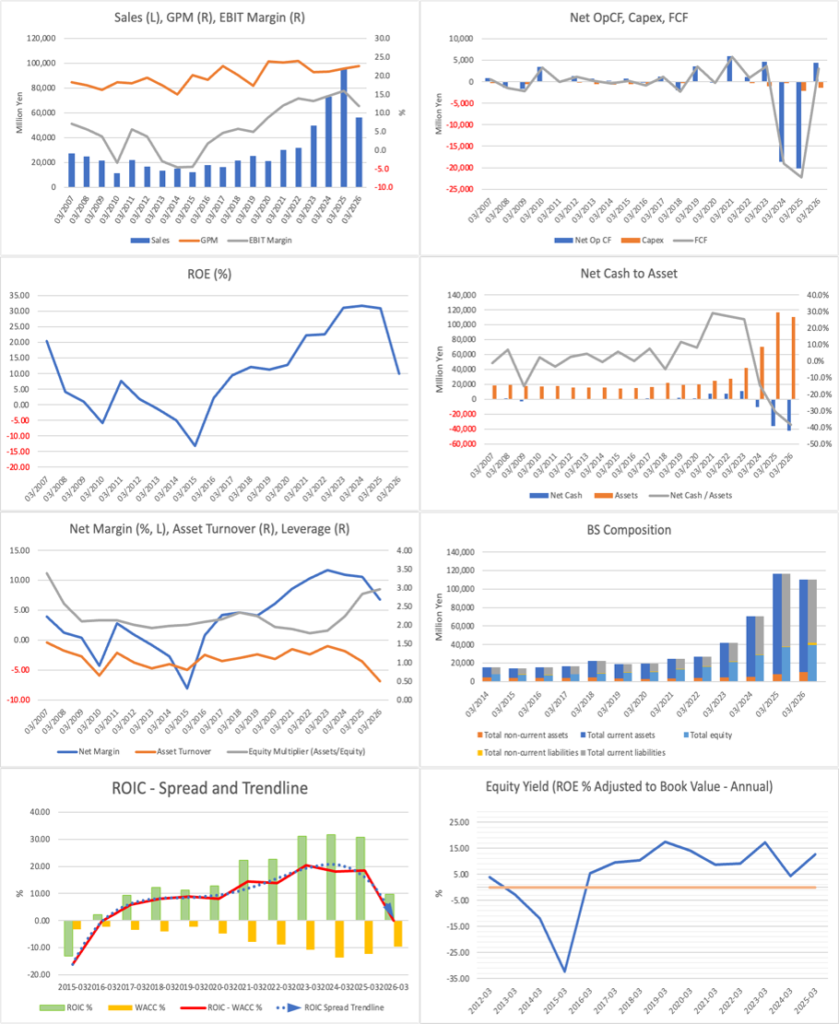

The most important point in the investment judgement for the company is whether the sharp decline in profits and deterioration in financial conditions in FY3/2026 should be viewed as a permanent decline in earnings power or as a temporary trough associated with the large-scale project cycle. In FY3/2025, contract assets increased sharply in line with revenue recognition for large-scale US water treatment equipment projects, and short-term borrowings also expanded significantly. Operating CF and FCF became significantly negative, the balance sheet expanded at once, and the company shifted from net cash to net debt. The charts also confirm that total assets and liabilities expanded sharply from FY3/2024 to FY3/2025, and that FCF fell deeply into negative territory. However, in FY3/2026, operating CF returned to positive territory due to a decline in trade receivables and other factors, and this should be understood not as a collapse in profitability but as a phase in which progress on large-scale projects and working capital appeared strongly in the financial statements.

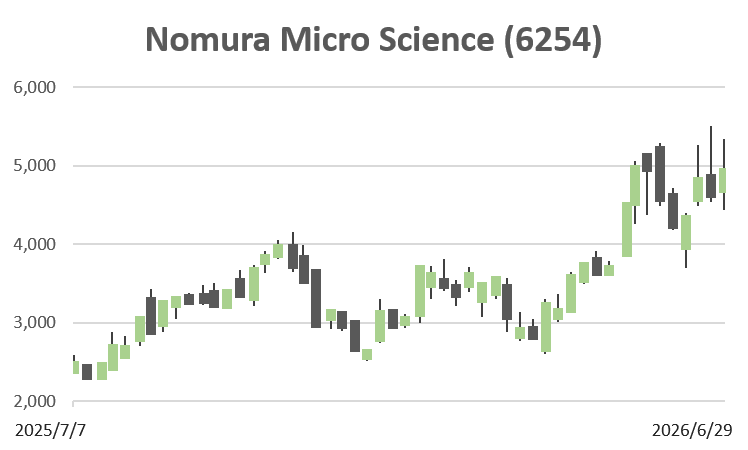

At the same time, fluctuations in ROE and EPS pose a risk that investors cannot ignore. ROE declined from 31.4% in FY3/2025 to 10.1% in FY3/2026, and EPS also fell sharply from 270.75 yen to 100.36 yen. Under normal circumstances, this would lead to a large decline in PBR, but in reality, PBR remained high, and the share price significantly outperformed TOPIX from 2025 to 2026. This gap means the market is looking not at actual profits but at the V-shaped recovery and renewed expansion of the order backlog in FY3/2027. The company plan calls for sales of 97.0 billion yen, operating profit of 16.0 billion yen, and EPS of 289.90 yen, with room to price in a return to a profit level exceeding FY3/2025, with FY3/2026 as the trough.

Against the current share price of 4,700 yen, the forecast PER is 16.2x and PBR is 4.58x, and apparent undervaluation is limited. Nevertheless, assuming a forecast ROE of 28.0%, a PBR in the mid-4x range is not necessarily excessive. Based on a payout ratio of 29.3% and a cost of equity of 8.0% to 9.0%, the medium-term EPS growth expectation priced into the share price is in the 6% to 7% range. The actual EPS CAGR from FY3/2022 to FY3/2026 is low, but if the FY3/2027 forecast is included, the company’s profit level will again return to record-high territory. Therefore, the current share price can be understood as buying not an extension of the past five years’ actual performance, but rather the next large-scale order cycle against the backdrop of AI and memory investment.

The sustainability of the firm’s share price depends on whether the build-up in orders and the order backlog, and the normalisation of FCF, can be confirmed simultaneously. Amid the semiconductor AI boom, ultrapure water production equipment is indispensable peripheral infrastructure for advanced semiconductor capital investment, and Korean DRAM investment, advanced memory, and demand for semiconductors for data centres are clear tailwinds for the company. However, if the share price advances to a PBR in the 6x to 7x range solely on the back of the AI theme, while the working capital burden of large-scale projects again erodes FCF, the risk-reward profile will deteriorate rapidly. The timing for selling would be when a peak-out in order backlog, postponement of customers’ investment, a mismatch between PBR re-expansion and ROE improvement, or structuralisation of net debt expansion becomes visible. At present, based on profit recovery in FY3/2027 and the sustainability of Korean investment, the Buy judgment is dominant.

Financials and Valuations

Assuming a share price of 4,700 yen, forecast EPS of 289.9 yen, actual BPS of 1,027 yen, forecast ROE of 28.0%, and forecast dividend of 85 yen, the forecast PER is 16.2x, PBR is 4.58x, and market capitalisation is 190.9 billion yen. The forecast earnings yield is 6.17%, and the Equity Yield is 6.12%. The company’s investment appeal lies not in a simple low PER, but in the certainty of a high ROE recovery and the sustainability of the order cycle.

| Item | Description |

| PBR method | Assumes forecast ROE of 28%, cost of equity of 8.0% to 9.0%, and medium-term growth of 4% to 6%. The fair share price range is 4,900 to 9,000 yen, with a median of 6,700 yen. |

| DCF method | Assumes the FY3/2027 forecast EPS as the starting point, an FCF conversion ratio of 55% to 75%, WACC of 8.0% to 9.0%, and terminal growth of 2.5%. The range is 3,850 yen to 6,225 yen, and the median is 4,936 yen. |

| ROIC method | Valued using normalised ROIC of 18% to 26%, WACC of 8.5%, growth of 3%, and after deducting net debt. The range is 4,600-7,600 yen, and the median is 6,100 yen. |

The central value across the three methods is around 6,000 yen. While the current share price of 4,700 yen is near the lower end of the DCF range, the PBR and ROIC methods indicate upside potential. In terms of investment judgement, what is important is not the short-term PER, but whether ROE returns to the high-20% range after the profit recovery in FY3/2027, and whether FCF normalises from the trough caused by large-scale projects.

Price

PBR (LTM)

PER (LTM)

ROE (LTM)

EPS (LTM)

BPS (LTM)

Shareholder Distribution

According to FactSet shareholder distribution data, the identifiable ownership ratio is 54.3%, and the free float ratio is 66.7%. Hokko Chemical Industry holds 10.3%, treasury shares account for 6.3%, and Nomura Shokusan, Resona Holdings, and individuals and business companies believed to be the founding family or related parties are among the top shareholders, giving the shareholder base a certain degree of stability. Meanwhile, holdings by overseas institutional investors and thematic and index-related funds, such as Vanguard, Robeco Sustainable Water, Legal & General Clean Water, American Century, and BlackRock, also stand out.

The merit of this shareholder distribution is that overseas funds can easily flow in through multiple investment themes, such as semiconductors, water treatment, and clean water. In contrast, the presence of stable shareholders provides a degree of support for supply and demand. Conversely, the greater the weight of thematic funds, the more likely PBR is to compress significantly if expectations for the AI and semiconductor investment cycle recede. Therefore, the shareholder distribution is both a driver of revaluation and a source of volatility when the theme reverses.

Conclusion

The investment judgement is Buy. The completion of large-scale projects and the weight of the working capital burden surfaced all at once in FY3/2026, but the FY3/2027 company plan indicates a recovery to a record-high profit zone, and the medium- to long-term themes of AI, memory investment, and Korean semiconductor investment are also strong. The current share price already prices in the recovery to a considerable extent, but when the PBR, DCF, and ROIC methods are combined, the central value exceeds the current share price. This is a phase to target medium-term share price revaluation while confirming expansion in orders and order backlog, as well as FCF normalisation.