2026-08-03

Home

Japanese

Omega Investment Co., Ltd.

Timee (Price Discovery)

Buy

Conclusion

We rate Timee highly as a labour-market platform, maintaining high ROE and ROIC, with attractive scope for re-rating following valuation adjustment.

The investment judgement is Buy. Timee not only leads the spot work market but also accumulates trust data, such as workers’ work records, reviews, qualifications, and repeat rates, and is building a labour supply infrastructure that combines immediacy and productivity to address structural labour shortages in logistics, retail, nursing care and welfare, and restaurants. In FY27/4, the company is in a phase of advocating “from defence to offence” and advancing the deepening of logistics and retail, the improvement of utilisation rates in nursing care and welfare, and the development of Timee Career Plus, Timee Solutions, Field Manager, Fintech, and other areas. Despite strong earnings and the maintenance of high ROE, the share price has been lacklustre since last year, and PER and PBR remain sharply lower from the end of Q3 2025 and have not recovered sufficiently. However, this is considered to be the result of a combination of the normalisation of the high-growth stock premium formed immediately after listing, concerns over the sustainability of growth in the spot work market and over regulation and competition, and caution over the short-term profit margin due to investment in new businesses, rather than deterioration in fundamentals. Based on the forecast PER of 23.7x, actual PBR of 9.57x, actual ROE of 36.8%, forecast EPS of 28.9 yen, and a forecast dividend of 0 yen, the EPS growth rate embedded in the share price is generally limited to the high single-digit range, around 10% annually. Taking into account the recent growth in sales and operating profit, the high level of ROIC, and business options beyond spot work, market expectations are not excessive. The PBR method has limitations in explaining the current share price, but the DCF method and ROIC method indicate upside potential, and the company’s shares have scope for re-rating as a high-quality growth stock after valuation adjustment.

Profile

A labour-market platform that uses spot work as its foundation and extends workers’ trust data into the human resources, operations and financial domains

Timee is a labour-market platform company whose main business is Timee, a spare-time part-time work service that matches “the time people want to work” with “the time employers want people to work”. The company was established in August 2017 and launched the service in August 2018. Workers can simply choose the conditions under which they want to work, without a CV or interview, and receive remuneration immediately after finishing work. On the other hand, clients are automatically matched with workers who meet the conditions by specifying only the time they want workers to arrive and the skills they require. The essence of the business is not merely the matching of supply and demand for short-term labour, but lies in accumulating work counts, no-lateness and no-absence records, experienced job types, working hours, repeat rates, badges earned, qualifications, Good rates, reviews, favourites from companies and other data, and visualising workers’ trust. Through this, for industries where labour shortages are structural, such as logistics, retail, restaurants, and nursing care and welfare, the company has a breadth that includes not only immediate labour supply, but also work decomposition, reduction of the burden of accepting workers, Field Manager, long-term part-time employment support, and future Fintech development. From FY27/4, the company has organised sales other than spot work fees as “other than spot work” and clarified Timee Career Plus, Timee Solutions, Field Manager, the long-term part-time employment support plan and other services as growth options.

Sales composition by business % (operating profit margin %): “Timee” matching service 99%, Timee Career Plus 0%, Other 0% (FY10/2025)

| Securities Code |

| TYO:215A |

| Market Capitalization |

| 151,517 million yen |

| Industry |

| Service |

Stock Hunter’s View

Leading in spare-time part-time work. This April fiscal year is “from defence to offence”.

Timee operates Timee, a spare-time part-time work service that matches “the time people want to work” with “the time employers want people to work”. The work matched through Timee is direct employment on a one-day basis between clients (employers) and workers (workers), and workers can work immediately, without a CV or interview, simply by choosing the conditions under which they want to work. They can receive remuneration immediately after finishing work. On the other hand, clients are automatically matched with workers who meet the conditions simply by setting the time they want workers to arrive and the skills they require.

Representative Director Ryo Ogawa started an apparel business while at university, but gave up after one year. The trigger for the birth of Timee was that, while subsequently experiencing various part-time jobs, he strongly felt, “I want money immediately” and “I want to work immediately, without interviews or a CV”. It is a service developed from his own experience from a “worker’s perspective”, and he is said to continue working through Timee once a year even now.

In the mainstay spot-work business, logistics and retail are driving the overall trend, while nursing care and welfare are maintaining high growth. Growth in spot work fees is also accelerating. In the current FY27/4, the company advocates “from defence to offence” and has a policy of implementing upfront investment weighted towards the first half. For earnings, in range format, it plans sales of 47.613 billion yen to 48.823 billion yen and operating profit of 8.821 billion yen to 9.746 billion yen. At the lower end of the range, compared with the same period of the previous year, the company expects a 22.6% increase in sales and a 20.9% increase in profit.

Investor’s View

After the erosion of high-growth expectations, the share price is in a phase of re-evaluating high capital efficiency and growth options.

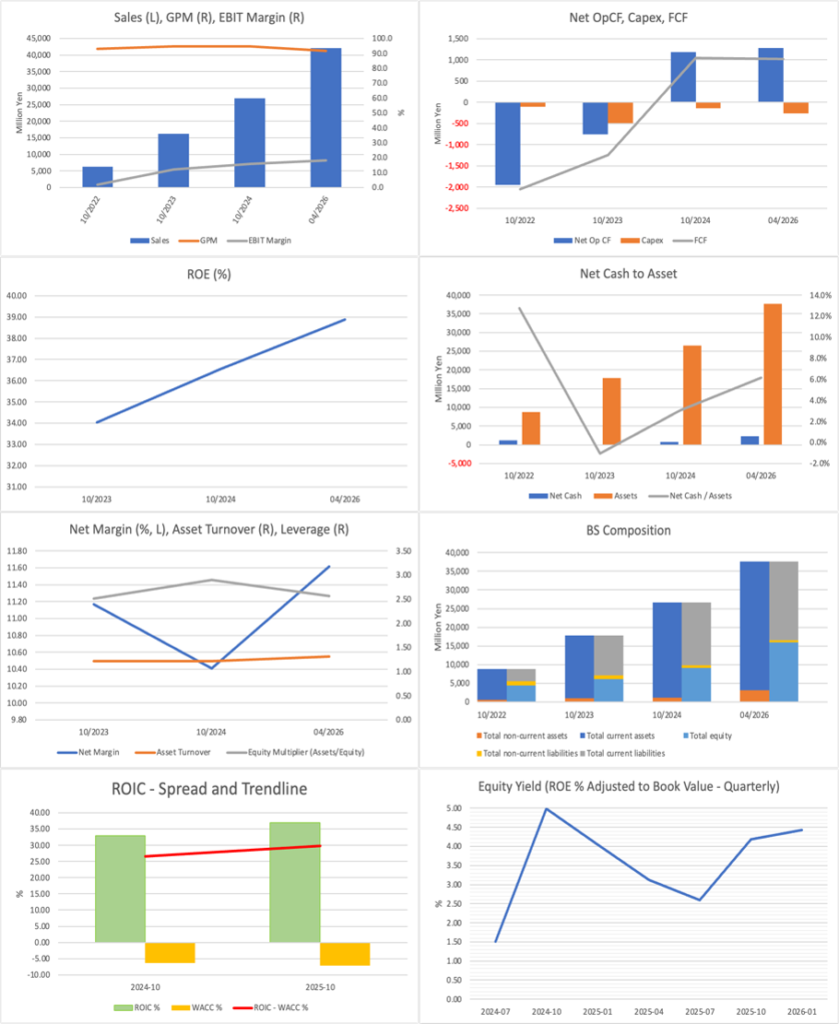

The first point for investors when looking at the company is that, while earnings are strong and ROE and ROIC are high, the share price has not reacted sufficiently. Sales continue to expand rapidly, and the operating profit margin has remained in the 18% range. ROE is in the high 30% range, ROIC is also high, and capital efficiency stands out even among listed growth companies in Japan. In addition, the company has net cash, the balance sheet is light, and the working capital burden is also limited. The graphs in Financials and Valuations in this document also confirm, at the same time, expanding sales, a stable operating profit margin, high ROE and ROIC exceeding WACC, and a sound financial structure accompanied by net cash. This indicates that the company’s business model is not merely an advertising-type recruitment medium but a platform-type model in which gross transaction value, worker base, client base, work data, and acceptance know-how are accumulated.

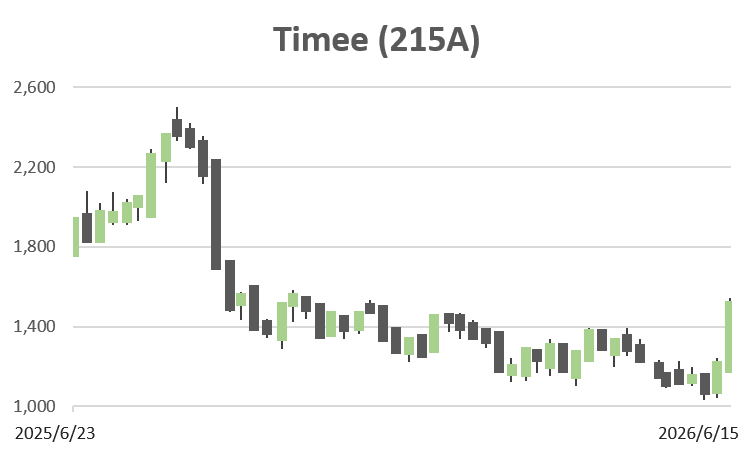

On the other hand, the trends in the share price and valuation are at odds with these favourable business fundamentals. After a phase of expectation-driven performance following the listing and testing highs towards the end of Q3 2025, the share price saw PER and PBR cut sharply and has not recovered sufficiently thereafter. Last year’s share price was lacklustre, and year to date it has remained only in line with TOPIX. There are mainly three reasons why the share price has not recovered despite no deterioration in earnings. First, the high-growth stock premium formed immediately after listing has eroded, and investors have entered a phase of looking not strictly at the growth rate itself, but at the sustainability of growth, the maintenance of profit margins, and reinvestment efficiency. Second, regarding the spot work market, concerns remain over regulation, competition, take rate, worker supply and the maturity of client usage. Third, in FY27/4, the policy of weighting strategic investment towards the first half as “from defence to offence” is liable to be received in the short term as a risk of a decline in the operating profit margin.

However, the expectations embedded in the current share price are not excessive relative to actual growth. The share price, reverse-calculated from a forecast PER of 23.7x and a forecast EPS of 28.9 yen, is approximately 685 yen. BPS reverse-calculated from the actual PBR of 9.57x is approximately 71.6 yen, and the Equity Yield against the actual ROE of 36.8% is approximately 3.8%. The forecast dividend is 0 yen, and the company should be evaluated not by dividend yield but by EPS growth through internal reinvestment. If the cost of shareholders’ equity is set in the 8% range and the terminal PER five years ahead is 18-20x, the EPS growth rate expected by the market is generally limited to the high single-digit range, around 10% annually. In the most recent comparable actual results, the sales CAGR from 22/5-23/4 to 25/5-26/4 is approximately 51%, and the operating profit CAGR is approximately 71%, so market expectations are considerably restrained relative to past growth results.

On valuation, views differ across the three methods: PBR, DCF, and ROIC. Under the PBR method, assuming a BPS of 71.6 yen, normalised ROE of 30-37%, cost of shareholders’ equity of 8-9% and a long-term growth rate of 3-4.5%, the fair share price range is seen at approximately 320-660 yen, with a median of approximately 460 yen. This method makes it difficult to justify the current share price, but for a high-ROIC platform company whose equity remains limited and whose value lies in intangible assets and data accumulation, the PBR method is likely to produce conservative results. Under the DCF method, assuming a forecast EPS of 28.9 yen, an EPS CAGR of 10-18% over five years, a cost of shareholders’ equity of 8.5% and a terminal PER of 18-22x, the fair share price range is seen at approximately 690-1,180 yen, with a median of approximately 910 yen. Under the ROIC method, assuming an ROIC in the 30% range, a WAa CC of 7-9%, and continued investment efficiency, the fair share price range is approximately 90-9300 yen, with a median of approximately 810 yen. Combining the medians of the three methods, the fair share price of the company’s shares is around 800 yen, suggesting upside potential of around 15-20% against the current share price of approximately 685 yen, reverse-calculated from the indicators in this document.

Looking in greater detail at the company’s business fundamentals, the sources of growth are clear. Spot work fees are accelerating YoY, with logistics and retail driving the overall trend. In logistics, deepening with large-scale clients, Field Manager, reducing the burden of accepting workers, and productivity-improvement solutions support higher penetration. In retail, in addition to deeper daily use, spot work has been incorporated into company-wide measures such as large-scale sales. In nursing care and welfare, gross transaction value and the number of active accounts continue to grow rapidly, and the business alliance with Benesse Carios may also contribute to greater recognition and client development. On the other hand, restaurants continue to record negative growth, but the margin is narrowing, and there are signs of a bottoming out, with proposed solutions aimed at resolving management issues. There are differences across industries, but overall, spot work is moving from a temporary labour-shortage response to a stage in which it is incorporated into clients’ work design.

The areas for improvement are also clear. First, in nursing care and welfare, as client development progresses, improving utilisation rates remains an issue. Not only the acquisition of qualified workers, but also marketing and product improvement to make acquired workers actually work in the nursing care and welfare field will be necessary. Second, in restaurants, negative YoY growth in gross transaction value remains, and improvement in client unit price and gross transaction value per AA will take time. Third, although businesses other than spot work have significant growth potential, Timee Career Plus, Timee Solutions, and Field Manager remain in the investment stage, incurring losses, and investors need to confirm not only sales growth but also control over the loss amount and future profitability. Fourth, the average take rate has declined slightly due to strategic discounting, and the balance between expanding gross transaction value and maintaining profitability will be important.

On Ownership, the high ownership ratio of founder Ryo Ogawa makes the management incentive for long-term business expansion clear. In addition, the conspicuous holdings by overseas institutional investors such as Keyrock Capital Management, Fidelity, Norges Bank and BlackRock indicate that the company is being evaluated not so much as a domestic small-cap growth stock but rather, in the context of international comparisons, as a labour-market platform. The background to attention from overseas institutional investors is considered to include high capital efficiency, net cash, a data-accumulation platform, and growth room amid structural labour shortages. This is positive for share price formation, but in phases when risk tolerance for global growth stocks declines, it is also a weakness, as valuations are likely to be compressed more than earnings. The lacklustre share price since last year is attributed precisely to this.

Looking back at past share price trends, immediately after listing, high growth expectations were embedded due to its position as a leading company in the spot work market. Thereafter, although earnings continued to expand, investor interest shifted from the growth rate itself to the quality of growth, profit margins, reinvestment efficiency, regulatory risk, and the monetisation of new businesses. The downward bend in PER and PBR from the end of Q3 2025 does not indicate an earnings stall, but rather a resetting of expectations for high-growth stocks. Therefore, for future revaluation of the share price, the company will need to demonstrate simultaneous deepening in logistics and retail, an improvement in the utilisation rate in nursing care and welfare, a bottoming in restaurants, a reduction in losses in businesses other than spot work, and maintenance of a high level of ROIC. If these are confirmed, the company’s shares may be re-rated not merely as a high-PER, human resources-related stock, but as a labour-market infrastructure company with high capital efficiency.

Financials and Valuations

Price

PBR (LTM)

PER (LTM)

ROE (LTM)

EPS (LTM)

BPS (LTM)