2026-07-27

Home

Japanese

Omega Investment Co., Ltd.

Serendip Holdings (Price Discovery)

Buy

Conclusion

Non-continuous growth through M&A, a funding strategy designed to restrain share dilution, and still-high equity yield warrant a positive rating.

Serendip Holdings is a roll-up-type business investment company that starts with business succession-type M&A in the manufacturing industry and raises enterprise value by combining post-acquisition management modernisation, PMI, the introduction of professional managers, and DX/RX support. The share price has risen significantly over the past year, but the Equity Yield calculated from the forecast ROE of 31.1% and the actual PBR of 3.08x is high at approximately 10.1%, and the EPS expected growth rate implied by the market, back-calculated from the forecast PER of 18.9x, remains only around 2.7% per annum, assuming a cost of equity of 8%. Based on the actual growth in sales, operating profit, and EPS over the past several years, the growth expectations priced in by the market remain conservative. In funding M&A, the company’s stance of subordinating equity finance and combining borrowings, mezzanine financing, treasury shares, and external capital platforms can be evaluated as a structure that balances growth with the protection of per-share value. Attention needs to be paid to financial leverage, the success or failure of PMI, and the stability of FCF, but we judge that the current share price does not sufficiently price in the company’s medium-term EPS growth capacity and improvement in capital efficiency.

Profile

A roll-up type business investment company that starts with business succession M&A in manufacturing and raises enterprise value through PMI and management modernisation

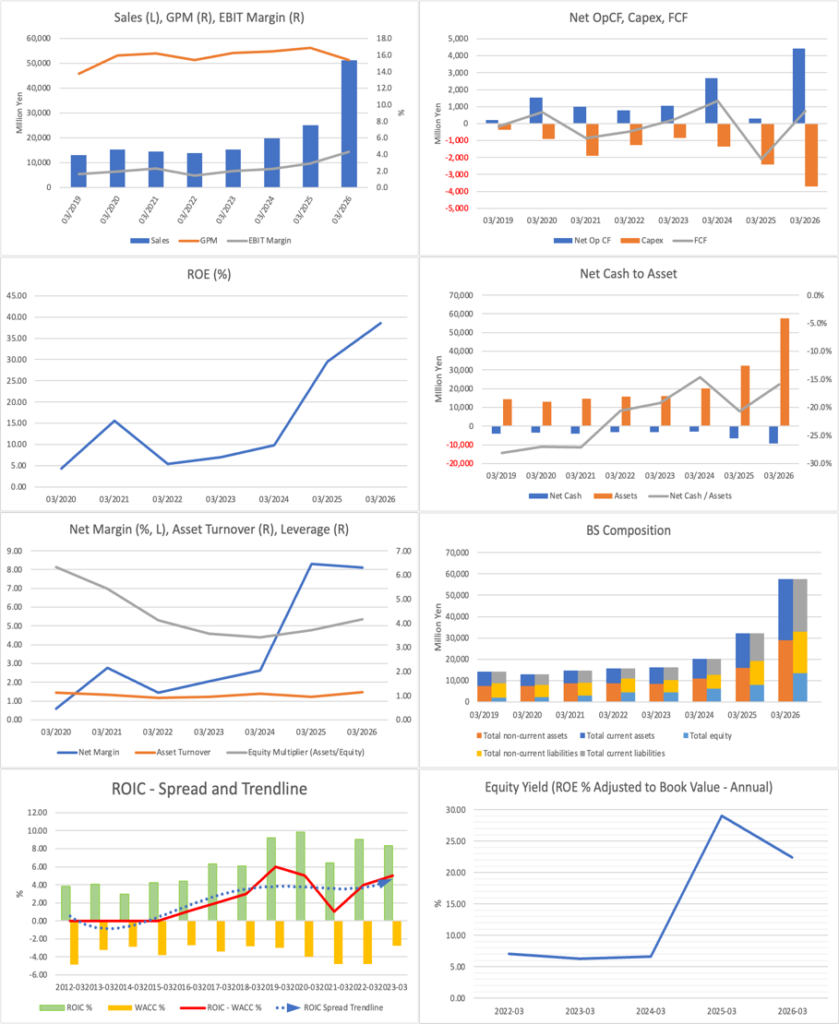

Serendip Holdings is a business investment company that primarily targets medium-sized and small manufacturing companies and provides integrated support for business succession-type M&A, post-acquisition management improvement, dispatch of professional managers, and DX/RX support. Its main businesses comprise automotive suppliers centred on automotive components, FA equipment and planning/development-type manufacturing, professional solutions, and investment. In FY3/2026, the full-year contribution from Excel Group and the consolidated contribution from Surtic Kariya resulted in sales of ¥51.163bn and operating profit of ¥2.189bn, setting record highs across all major profit items. The essence of the business is not merely acquisition and consolidation, but the point that the company makes combined use of its ability to acquire deals by being chosen by sellers, its post-acquisition management control platform, its capability for improvement at manufacturing sites, and its funding capability that restrains dilution, thereby raising the earnings power of acquired companies in stages.

Sales composition by business % (operating margin %): Manufacturing business 94.4 (4.3), Professional Solutions business 5.3 (4.5), Investment business 0.3 (-19.2) (FY3/2026)

| Securities Code |

| TYO:7318 |

| Market Capitalization |

| 39,306 million yen |

| Industry |

| Transportation equipment |

Stock Hunter’s View

A funding strategy that thoroughly pursues the “avoidance of share dilution”. Building a new funding platform of around ¥10bn.

Serendip Holdings has continued to achieve non-continuous growth through business succession-type M&A in manufacturing, centred on automotive components and FA equipment. Similar companies include Seiwa Holdings (523A), which listed in March this year, and Japan Technology Succession (319A), but compared with these companies, Serendip’s flexible funding strategy is impressive. On 1 June, it announced a new funding scheme that attracted attention.

As a new framework for funding and investment, the company will establish a new company, “Monozukuri Business Succession Holdings” (JMS), specialising in business succession and long-term holding investment in small and medium-sized manufacturing companies. Serendip will invest ¥500m, while The Shoko Chukin Bank, with which it has collaborated in the business succession field, and Kyoto Capital Partners, under Kyoto FG (5844), will each invest ¥1bn, making a total investment of ¥2bn in JMS. Thereafter, it will sequentially seek strategic partners until the total reaches ¥10bn.

What the company is conscious of in its funding strategy is the “avoidance of share dilution”. When raising M&A funds, the company has traditionally combined multiple financing schemes, including bank borrowings, mezzanine financing, bonds, and the use of treasury shares, to minimise the outflow of its own funds. To restrain share-price dilution, it has adopted a policy of subordinating equity finance. Under the current scheme as well, while avoiding share dilution, it will become possible to pursue large-scale M&A with a small amount of its own funds in a form similar to an LBO.

Investor’s View

With the company balancing high ROE with dilution-controlled M&A, investment attraction remains even after the share price rises.

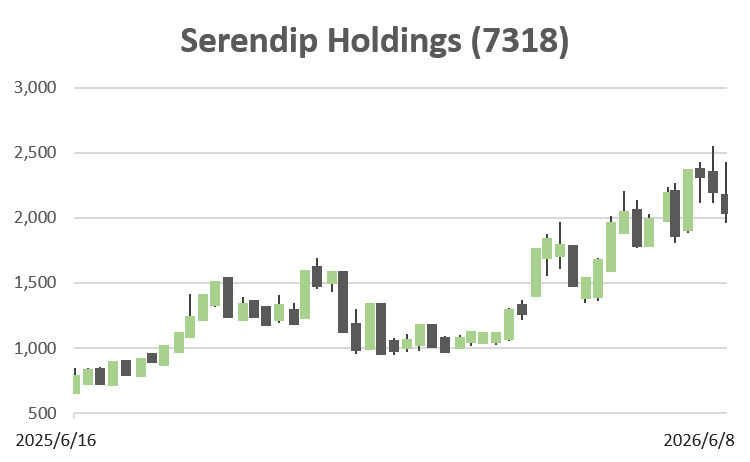

The first point for investors considering the company is whether the current share price, even after the sharp rise over the past year, adequately reflects its EPS growth potential and capital efficiency. The share price, back-calculated from a forecast PER of 18.9x and forecast EPS of ¥120.7, is approximately ¥2,281. If the cost of equity is set at 8%, the expected EPS growth rate priced into the share price is approximately 2.7%. Meanwhile, the company’s actual EPS has expanded sharply, from ¥17.88 in FY3/2023, ¥29.62 in FY3/2024, and ¥115.62 in FY3/2025 to ¥227.28 in FY3/2026. However, because negative goodwill is included in FY3/2026, the actual CAGR should not be used as the future growth rate. Even so, using the FY3/2027 forecast EPS of ¥120.7 as the base, the annual growth rate from FY3/2023 is approximately 61%, and the market-priced growth expectation of around 2.7% is conservative, given the company’s actual growth and M&A pipeline.

The company’s equity yield merits attention. When the forecast ROE of 31.1% is divided back by the actual PBR of 3.08x, the effective yield on shareholders’ equity is approximately 10.1%. This substantially exceeds the simple PER-based earnings yield forecast of 5.3% and indicates that high profit-generating capacity remains relative to book-value capital. Because the rise in ROE includes M&A, debt-related goodwill, and some one-off factors, the surface-level ROE should not be extrapolated on a straight line. However, even after PBR has risen to the 3x level, the ROE-relative equity yield reaching double digits is an important basis for investment appeal following the rise in the share price.

Looking at the past share price trend, for some time after the 2021 listing, market understanding of the company’s business succession-type M&A model was limited, and the share price response to earnings expansion was muted. The background was that investors needed a verification period to determine whether growth through M&A would lead to sustained EPS growth, whether PMI at acquired companies would function, and whether growth accompanied by financial leverage would impair shareholder value. Since 2025, the acquisition effects of Excel Group, Surtic Kariya, and others have been reflected in actual sales and profit, and operating profit, ROE, and EPS have stepped up in stages, causing the share price and PBR to be revalued rapidly. In other words, the main cause of the share price rise is not merely buying into the M&A theme, but the confirmation of acquisition execution, consolidated contribution, profit expansion, and improved capital efficiency.

At first glance, the company’s business model appears to be merely an accumulation of manufacturing M&A. However, the source of the company’s strength lies not in the ability to buy deals itself, but in the integration of relationships through which sellers choose it, the optimisation of acquisition prices through negotiated transactions, post-acquisition management control, the introduction of professional managers, on-site improvement, DX/RX support, and the design of funding schemes. In the manufacturing business succession market, while excellent small and medium-sized companies face a lack of successors, there also remains resistance to transferring businesses to mere financial investors. By assuming long-term holding, management modernisation, and growth investment, the company has gained trust among sellers as a recipient and has formed a cycle that leads to subsequent deals. This point is the core differentiating factor that sets the company apart from mere M&A intermediaries and short-term exit-oriented investment firms.

Similar companies have also begun to appear in the Japanese market. Japan Technology Succession and Seiwa Holdings are comparable in terms of business succession, manufacturing, and roll-up. However, their history as listed companies is still short, and this category is not a mature sector in the Japanese equity market. Serendip is one of the leading companies in a model that combines manufacturing business succession, M&A, PMI, management talent, and a funding platform. For investors, it is positioned as a stock through which to evaluate the formation process of a group of Japanese roll-up companies.

In valuation terms, the current share price still has upside potential when evaluated using the PBR, DCF, and ROIC methods. Under the PBR method, assuming a forecast ROE of 31.1% and a cost of equity of 8%, setting a justified PBR of 3.5–4.5x with the growth rate placed conservatively, and using a BPS of around ¥740, the fair share price range is approximately ¥2,600–3,300, with a median of approximately ¥2,900. Under the DCF method, using forecast EPS of ¥120.7 as the starting point, assuming an FCFE conversion ratio of 80–100%, a five-year profit growth rate declining in stages from 15–25% per annum to 5%, a terminal growth rate of 2%, and a cost of equity of 8%, the fair share price range is approximately ¥2,300–3,600, with a median of approximately ¥2,900. Under the ROIC method, starting from FY3/2027 operating profit of ¥3.5bn and after-tax operating profit of approximately ¥2.5bn, and incorporating WACC of 8%, medium-term ROIC improvement, and recovery of invested capital after M&A, the fair share price range is viewed as approximately ¥2,100–3,000, with a median of approximately ¥2,500. The median across the three methods is roughly ¥2,800, suggesting upside potential in the 20% range relative to the current share price of around ¥2,280.

In the shareholder structure, the ownership ratio of founders, management, and related parties is high, and the stable shareholder base, including Mr Zai Takeuchi (President), Mr Noriyuki Takamura (Director), Moroto Group Management, treasury shares, and the employee shareholding association, is thick. This structure is a clear advantage for consistently pursuing the medium- to long-term M&A strategy, controlling dilution, and investing in PMI. On the other hand, the float remains at around 35%, and ownership by external institutional investors remains limited. This is a constraint in terms of liquidity, share price volatility, and the depth of the investor base, but if a move to the TSE Prime Market, IFRS adoption, and IR enhancement proceed, room for institutional investors to enter should instead become a revaluation factor.

The risks investors should pay attention to are clear. First, while the funding strategy that avoids share dilution is attractive, the use of borrowings, mezzanine financing, SPCs, and external capital increases the importance of financial leverage management. A rise in interest rates, deterioration in the funding environment, and a decline in the cash-generating capacity of acquired companies could directly affect shareholder value. Second, the success or failure of M&A depends on acquisition prices and the quality of PMI. As the number of acquisitions increases and deal sizes grow, supply constraints in management talent, internal controls, and on-site improvement capabilities may become apparent. Third, because negative goodwill is included to a large degree in net profit for FY3/2026, investors should focus not on net profit but on improvement in operating profit, adjusted EBITDA, FCF, ROIC, and continuing EPS. Fourth, dependence on the manufacturing business centred on automotive components is high, and the company is affected by customer production schedules, raw material prices, foreign exchange rates, and trade policy.

Based on the above, the company’s shares cannot simply be described as overvalued even after the sharp rise in the share price. The equity yield remains high, the growth expectations indicated by PER are conservative, and the dilution-control measures in M&A funding help protect per-share value. The focus going forward is not the number of acquisitions itself, but the extent to which the company can build up post-acquisition ROIC improvement, FCF generation, and continuing EPS growth with high reproducibility. As long as these are confirmed, the company has room to receive a still higher valuation as a rare manufacturing roll-up growth stock in the Japanese equity market.

Financials and Valuations

Price

PBR (LTM)

PER (LTM)

ROE (LTM)

EPS (Actual)