2026-07-27

Home

Japanese

Omega Investment Co., Ltd.

Kidswell Bio (Company Note – update)

| Share price (12/16) | ¥279 | Dividend Yield (23/3 CE) | – % |

| 52weeks high/low | ¥503/200 | ROE(TTM) | -32.2 % |

| Avg Vol (3 month) | 12.3 thou shrs | Operating margin (TTM) | -58.6 % |

| Market Cap | ¥8.78 bn | Beta (5Y Monthly) | 1.16 |

| Enterprise Value | ¥9.08 bn | Shares Outstanding | 31.471 mn shrs |

| PER (23/3 CE) | – X | Listed market | TSE Growth |

| PBR (22/3 act) | 5.85 X |

| 本ページのPDF版はこちら |

| PDF Version |

Focus on SHED (cell therapy) business.

Aiming for launch in 2030, with a view to development abroad.

Summary

◇A drug discovery venture company originated from Hokkaido University, which began research into biosimilars (follow-on bio products) in 2007. Currently develops and markets three products. Since 2016, the company has been strengthening its cell therapy (regenerative medicine) business, focusing on developing drugs to treat unmet needs using stem cells from human exfoliated deciduous teeth (SHED). The master cell bank was built in May 2022. To further expand the SHED business, a strategy is planned for future expansion abroad. With the start-up of the SHED business, the company looks at accelerated profitability beyond 2030. In July 2021, the company changed its name to Kidswell Bio to provide new medical treatments for paediatric diseases and rare diseases of all generations, emphasising children.

◇Share price: The company’s share price fell sharply after the announcement of its financial results for FY2022/3 showed a postponement of achieving profitability in FY2023/3. The share price has remained depressed since then, partly due to adjustments in biotech stocks. The company has also indicated upfront investment in SHED and associated equity financing, making the environment surrounding the company’s share price difficult. However, in terms of PBR, they are well below the levels of the past three years. Hence, this may be a good buying opportunity for investors who can hold the shares for a long time in anticipation of the potential of regenerative medicine to be underpinned by the earnings of biosimilars.

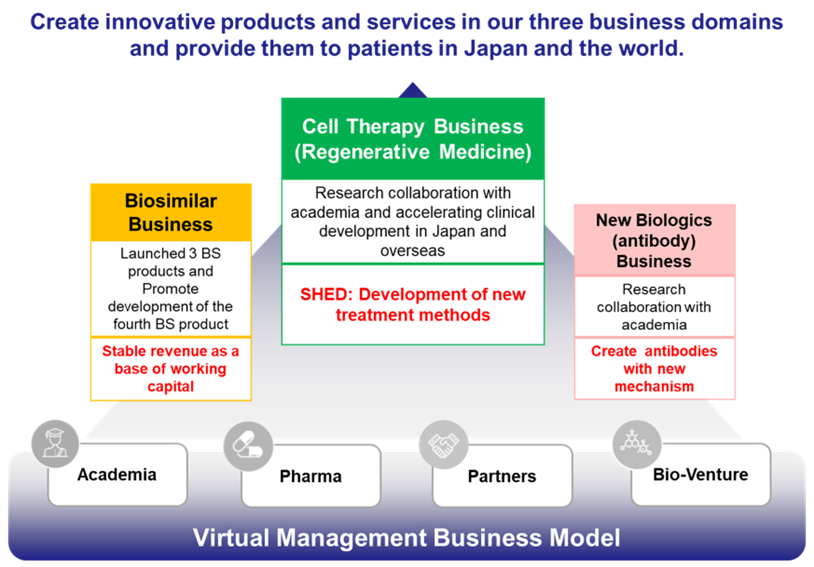

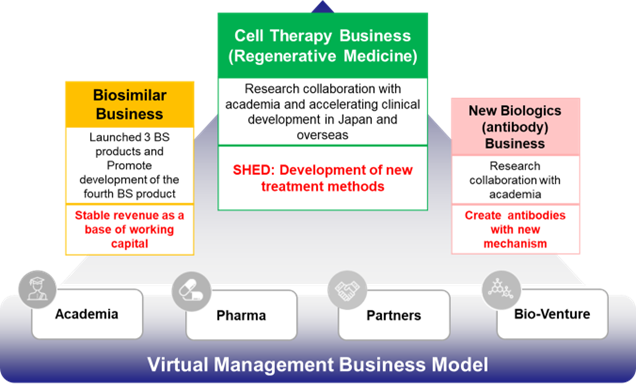

◇The company’s three business lines are as follows.

Cell therapy (regenerative medicine) business: The area the company has been focusing on most in recent years and aims to establish a cell therapy platform using stem cells. The company currently has a pipeline of nine products in stem cells from human exfoliated deciduous teeth (SHED) using deciduous teeth and is accelerating out-licensing activities to pharmaceutical companies and others. In addition, a master cell bank has been built to establish a stable supply of deciduous teeth. As a pillar of the company’s future growth, the upfront investment is being accelerated, with a view to overseas development.

Biosimilars business: Development of follow-on biopharmaceuticals. Pioneer in this field in Japan. Biosimilars provide an alternative option to biopharmaceuticals, which tend to be expensive. Partner pharmaceutical companies already market three products, and a fourth is expected to be launched by FY2025. In drug discovery ventures, where large amounts of capital are required to develop new drugs, the company’s profits from selling biosimilars lighten the burden of financing and create a solid management base.

New biologics: several new biologics are in the pipeline, including GND-004 (anti-RAMP2 antibody), which is being investigated as a drug candidate for ocular diseases and oncology. New biologics are expected to generate significant returns if successful but are still in the research phase. They are expected to be launched in the early 2030s.

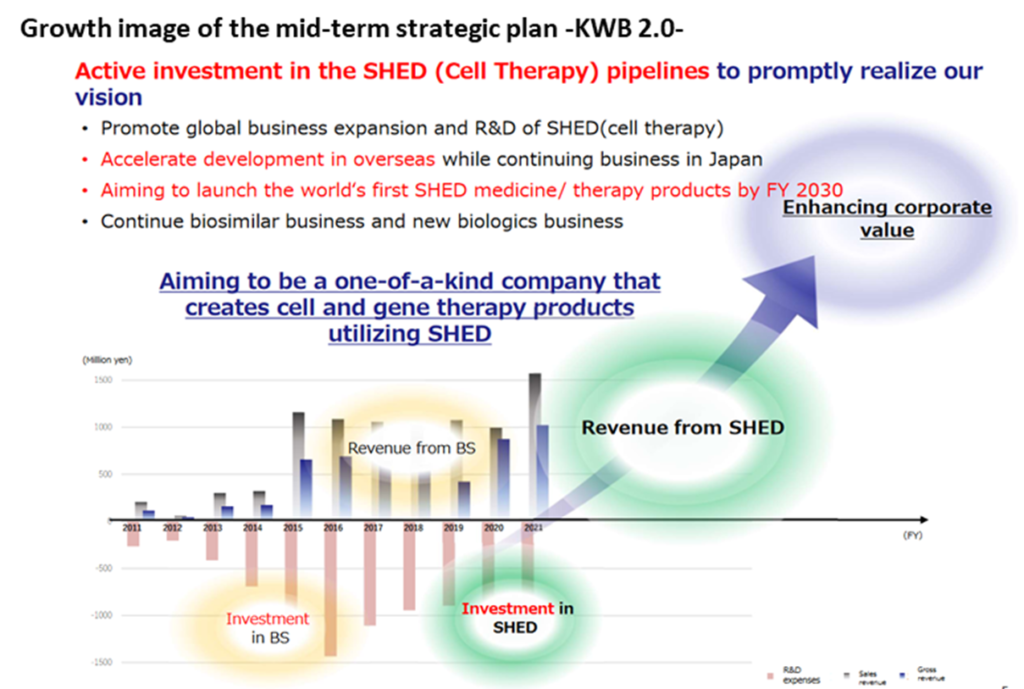

◇Mid-term strategic plan -KWB 2.0- : In May 2022, the company updated its mid-term strategic plan, announcing that it would further focus on the SHED business and increase upfront investment to achieve breakthroughs in this business. Due to changes in the market environment for the biosimilars business, the company plans to actively expand the SHED business overseas. In the future the company aims to significantly increase its corporate value based on the revenues generated from SHED.

◇Earnings results: In FY2022/3, sales increased by 58% (1.56 bn yen), R&D costs were 1.15 bn yen and an operating loss was 0.92 bn yen (operating loss of 0.96 bn yen in FY2021). Strong sales of GBS-007 contributed to earnings. Orders for GBS-007 are expected to increase rapidly in FY2023/3, and the company sales are expected to increase significantly to 2.9 billion yen and an operating loss is expected to be 980 million yen.

Table of contents

| Summary | 1 |

| Key financial data | 2 |

| Business summary | |

| Business model | 3 |

| Cell therapy (regenerative medicine: SHED) | 5 |

| Biosimilars | 8 |

| New Biologics | 11 |

| Mid-Term Strategic Plan –KWB 2.0– | 12 |

| Financial results trends | |

| FY2022/3 financial results actual | 14 |

| FY2023/3 Q2 financial results actual | 15 |

| FY2023/3 financial forecast | 15 |

| Stock price trends | 16 |

| Financial data | 18 |

| Company Profile | |

| Company profile/History | 19 |

| Management/Corporate governance system | 20 |

| Status of major shareholders/Initiatives for SDGs | 21 |

Key financial data

| Fiscal Year | 2017/3 | 2018/3 | 2019/3 | 2020/3 | 2021/3 | 2022/3 |

| Net sales | 1,089 | 1,059 | 1,021 | 1,077 | 996 | 1,569 |

| Cost of sales/SG&A expenses | 2,273 | 1,973 | 1,827 | 2,249 | 1,966 | 2,487 |

| R&D expenses | 1,433 | 1,107 | 945 | 898 | 963 | 1,150 |

| Others | 840 | 865 | 882 | 1,350 | 1,002 | 1,337 |

| Operating loss | -1,184 | -913 | -805 | -1,161 | -969 | -919 |

| Ordinary loss | -1,176 | -903 | -816 | -1,187 | -991 | -952 |

| Net loss | -1,224 | -904 | -856 | -7,316 | -1,001 | -535 |

| Current assets | 3,421 | 2,692 | 2,821 | 3,322 | 3,346 | 3,325 |

| Cash and cash equivalents | 2,379 | 1,891 | 2,009 | 2,032 | 1,461 | 1,187 |

| Total assets | 3,706 | 3,025 | 3,151 | 3,592 | 3,933 | 3,503 |

| Total shareholder’s equity | 3,500 | 2,604 | 2,731 | 1,487 | 1,610 | 1,718 |

| Equity ratio (%) | 93.8 | 85.0 | 85.6 | 39.8 | 38.0 | 43.8 |

| Cash flow from operating activities | -1,759 | -438 | -860 | -1,325 | -1,267 | -1,169 |

| Cash flow from investing activities | -149 | -50 | 0 | -137 | -22 | 526 |

| Cash flow from financing activities | 3,471 | – | 978 | 1,221 | 718 | 369 |

| Increase/decrease in cash and cash equivalents | 2,379 | 1,891 | 2,009 | 2,033 | 1,461 | 1,187 |

Notes) Consolidated financial statements from the FY2020/3 to the FY2022/3. There is no continuity before.

Cash flow from operating activities:Expenditures such as R&D expenses and SG&A expenses mainly centering on drug development.

Cash flow from financing activities:Income from issuance of shares associated with the exercise of stock rights

Source: Omega Investment from Company materials

Business summary

Business model: Portfolio construction through three business areas

In drug discovery ventures, it takes more than ten years from basic research to the launch of a new drug through out-licensing and clinical trials. Securing research and development funding in billions of yen yearly is generally necessary. The company began researching biosimilars in 2002. Being a pioneer of biosimilars in Japan, it has already launched three products. The biosimilar business generates revenues in the order of 1 billion yen per year, which exceeds the company’s working capital (fixed costs). The stable income from the biosimilar business supports fundraising, one of the biggest challenges for a drug discovery venture, and forms a solid management foundation.

See the table below for the characteristics and contents of each business.

Comparison of the characteristics of the three business areas

| Business | Period | Risk | Rate of return | Pipeline, etc. |

| Cell therapy (Regenerative medicine) |

Mid-term | Middle | Mid→High | Nine pipelines for SHED are in progress. Established a platform for cell therapy using SHED by building a master cell bank. Aggressive upfront investment with a view to overseas expansion in the future. |

| Biosimilar | Short term | Low | Mid→Low | Three products are already on the market, which will be expanded to 4 by FY2025. Responding to changes in the biosimilars market environment, the company will promote the development of cost-competitive biosimilars. |

| New biologics | Long term | High | High | Pipelines of multiple products are in the R&D stage. Launching is expected in the early 2030s. |

Thanks to the operation of three different businesses, the Company can keep the drug portfolio well-balanced by proper mix of timespan, risk and return. As a result, it does not suffer long-term deficit due to low or no sales, which is not unusual for drug discovery ventures.

In addition, the dilution by new shares resulting from the exercising of stock rights is of great concern to shareholders. The earnings contribution of biosimilars in the portfolio should moderate this concern.

Business structure

Business model: Virtual business development

Development of new drugs requires significant R&D expenditure, investment in clinical trials and manufacturing facilities, etc., and venture companies alone cannot bear the burden. Thus, there exists a system of cooperation among venture companies, academia, CRO/CMO and out-licensed pharmaceutical companies that allocate the burden in accordance with the expertise of each party. In the case of Kidswell Bio, it has built a collaborative system with best partners by utilizing its research and development capabilities, as well as the experience, know-how, and networking capabilities nurtured through business. By developing a virtual business that needs no manufacturing facilities, the Company delivers high capital efficiency by light equipment.

Business Partnership

Cell therapy business (regenerative medicine: SHED)

In the field of regenerative medicine, the Company aims to establish a cell therapy platform that utilizes stem cells from human exfoliated deciduous teeth (SHED) .

Regenerative medicine (cell therapy) is a medical treatment that repairs and regenerates the functions of lost tissues and organs by using the cultured and processed cells and tissues of the patient or others. Research and development of stem cells are progressing rapidly thanks to the advancement of cutting-edge biotechnology. Stem cells include pluripotent stem cells (ES cells, iPS cells) and somatic stem cells. The Company is looking at cell therapy (regenerative medicine) and the stem cells from human exfoliated deciduous teeth (SHED) applied to stem cells.

The Company has been working on regenerative medicine centered on SHED since 2019. In April 2019, the Company acquired Advanced Cell Technology and Engineering Ltd. (ACTE), which was developing medical technology and regenerative medicine products using SHED. The Company made it a fully owned subsidiary and has been accelerating the research and development of SHED-related business. In November 2020, the Company reorganized ACTE business, focusing only on areas related to cell therapy platforms.

In February 2020, the company made Japan Regenerative Medicine (JRM), which had been researching cardiac stem cells (CSCs) within the Noritsu Koki Group (JRM’s parent company), a wholly-owned subsidiary. The company had promoted the development of regenerative medicine using the cardiac stem cells (JRM-001) by JRM. In April 2022, JRM was transferred to Metcela Inc., aiming to further accelerate the research and development of JRM-001 and increase its future corporate value. JRM-001 is no longer in the company’s pipeline.

SHED potential

Dental pulp stem cells are collected from the dental pulp found inside the tooth (pulp cavity). Stem cells collected from deciduous teeth (SHED) are particularly active and have a high capacity for repair and regeneration. They can be harvested from deciduous teeth when children’s teeth are changing, and the timing of harvesting is more convenient and less burdensome for the donor. As is well known, bone marrow stem cells and other types of stem cells are highly burdensome on donors, but SHED has a high advantage and potential in this respect. Although SHED is a new stem cell technology with a short history of research worldwide, its potential is noteworthy. The company is a world leader in research, development and infrastructure. For a comparison with other stem cell types, see the figure below. SHED is also superior in terms of age and donor-derived risk balance.

Comparison of characteristics of various stem cells and other cells for regenerative medicine applications

In addition, embryologically, dental pulp stem cells are derived from neural crest cells and are expected to be particularly applicable to diseases of the nervous system and musculoskeletal systems. According to data from the company and joint research, the high proliferative capacity of the cells enables the securing of sufficient cells in a short period. The increased expression of neurogenesis-related genes, secretion of nervous system growth factors, and the high capacity for nerve regeneration mean that the cells are expected to be applied to diseases related to nerve regeneration, such as spinal cord injury and cerebral palsy. Furthermore, it is also shown to have a high bone regeneration capacity and is expected to be effective in diseases requiring bone regeneration.

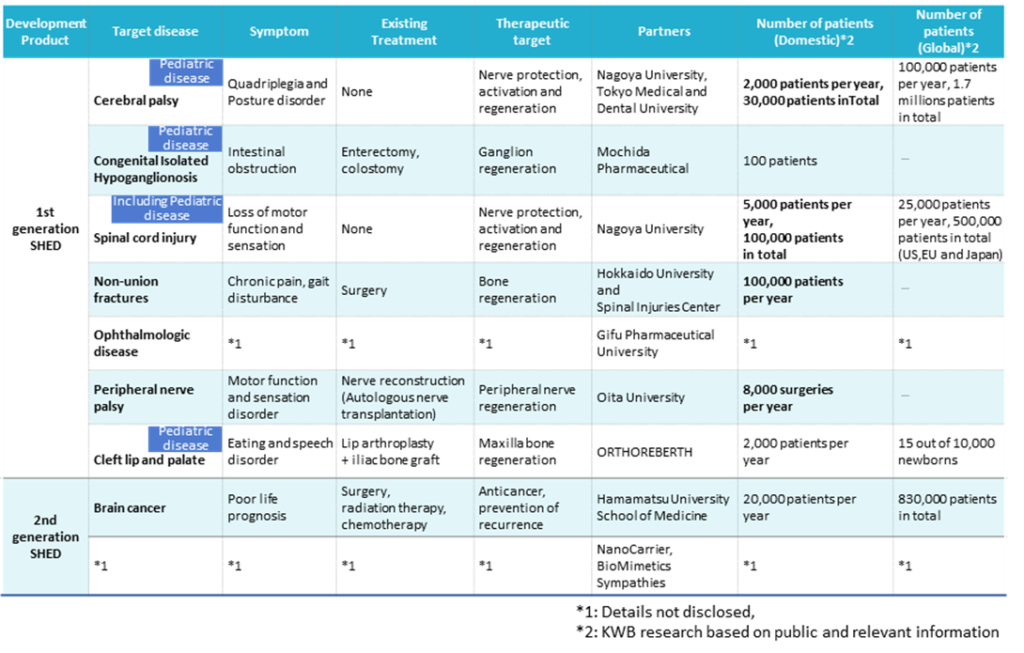

SHED project list

See the table above for details of SHED development projects. The company plans to start clinical trials by FY2022 and launch three products by FY2030. On November 7, 2022, research articles were published on a new treatment for brain tumours in collaboration with Hamamatsu University School of Medicine. Steady progress is also being made in the second-generation SHED project (see p. 8 for details).

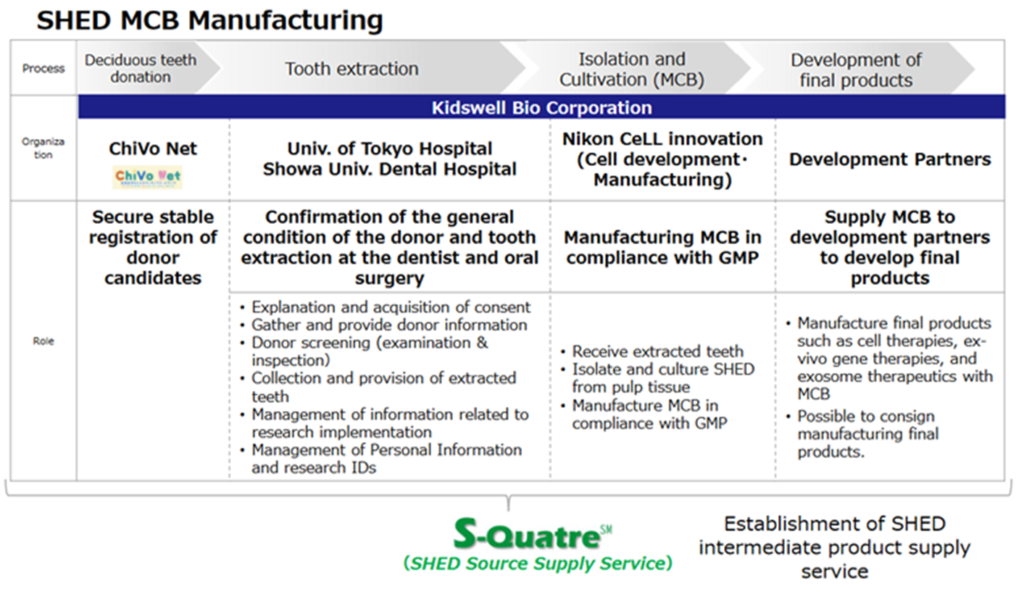

Construction of the SHED Master Cell Bank (MCB)

In promoting regenerative medicine using dental pulp stem cells, it is essential to establish a stable supply system for milk teeth, which are the raw material for various regenerative medicine products. The company has been building MCBs through the acquisition and restructuring of ACTE, partnerships with medical institutions and Nikon CeLL innovation. In August 2022, the company’s SHED clinical MCBs were constructed. As there is no precedent for the manufacture of MCBs for SHED by other companies, the company’s diverse expertise was utilised to solve the problem. Thus, the foundation for a full-fledged SHED business has been established.

SHED master cell bank process

SHED manufacturing and supply system (S-Quatre)

While completing the MCB is a crucial step, the MCB itself is one process in the company’s SHED manufacturing and supply system. Securing raw material baby teeth requires the development of an overall manufacturing and supply system: donor recruitment, ensuring the safety of potential baby teeth donors at the dentist, extraction, culture and production at the MCB, supplying the MCB to the development partner and developing the final product. The company plans to commercialise the service of providing MCBs, the intermediate product of SHED, as the SHED Source Supply Service (S-Quatre®).

SHED manufacturing and supply system

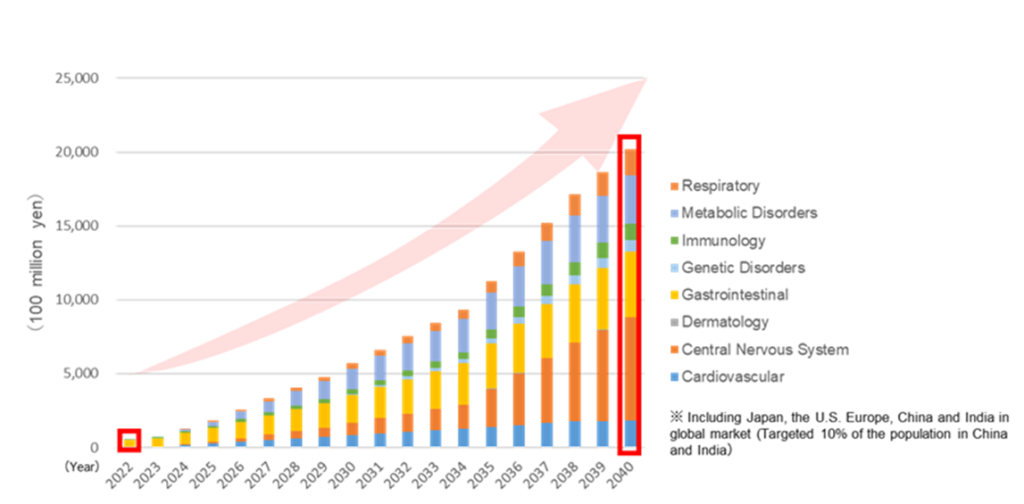

SHED market potential

In the pharmaceutical industry, the increasing speed of technological innovation has led to a rapid diversification of modalities (types of therapeutic means. See also later in this section the second-generation SHED: Designer cells). Regenerative medicine using cell-based medicines is expected to expand rapidly. In this context, the market for SHEDs for neurological and musculoskeletal diseases is expected to grow to 700-800 billion yen by 2040. Given the potential of this market and the progress of the SHED business, the company decided to formulate a mid-term strategic plan – KWB 2.0 – to accelerate SHED research and development (to be explained later).

Allogeneic stem cell market size forecast (global)

The second-generation SHED: Deployment in designer cells

Technological innovation in medicine has led to a diversification of modalities (types of treatment means) in recent years. Until around 2000, the focus was on traditional ‘low-molecular medicines’, but from 2000 to 2020, ‘antibody medicines’ made remarkable progress. Subsequently, research on stem cells, as represented by iPS, has developed, and regenerative medicine using cell therapy is currently attracting attention. As the next step after cell therapy using first-generation SHEDs (non-engineered stem cells), the company has started developing second-generation SHED ‘designer cells’ (engineered cell therapy in which functions are added or enhanced by gene transfer or other means).

Image of the second-generation SHED ‘designer cells’ and therapeutic modalities.

On November 7, the company announced that it had published a paper in collaboration with the Department of Neurosurgery, Hamamatsu University School of Medicine, following high research results from basic research into a new treatment for brain tumours using second-generation SHED, which was being conducted in collaboration with the university. Recent advances in various treatment techniques have improved clinical outcomes in brain tumours, but recurrence due to residual tumours significantly impacts prognosis. Therefore, developing localised therapies at the cellular level is desired to kill all major cells that have invaded the brain. The present treatment with second-generation SHEDs (engineered SHEDs) suggests that they may be a practical therapeutic approach for brain tumours and brain metastatic cancer.

Biosimilars

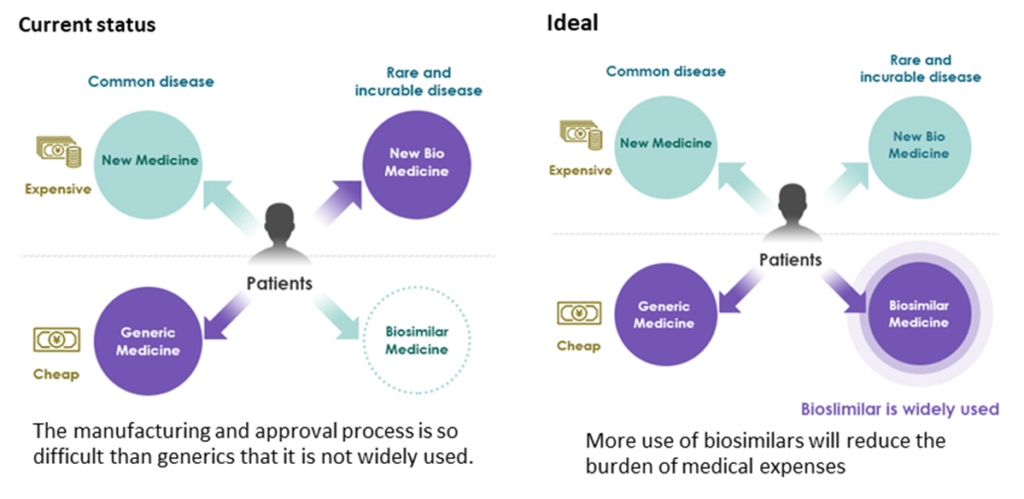

The term generic drug has become commonplace. It is a medicine with the same active ingredients, quality, efficacy and safety as the new drug, and is sold after the patent for the original drug is expired. The development of new medicine requires huge R&D expense and clinical costs, their prices become very expensive. Therefore, the use of generic medicines is recommended from the viewpoint of controlling medical costs.

Traditional pharmaceuticals are for general diseases and are produced mainly by chemical synthesis of small molecule compounds. But in recent years, bio medicines produced by recombinant proteins has progressed. Biomedicines are produced by purifying polymer compounds synthesized in microorganisms and cells. They are therapies for intractable diseases and rare diseases. Biomedicine has become even more expensive due to the difficulty of its manufacturing process, and there is a need to develop biosimilars, such as generics as against the traditional medicines.

Positioning of Biosimilars

The production of biomedicine requires high technology, and it is produced by gene recombination technology or cell culture, therefore, unlike generics for the traditional small molecule drugs, it is not possible to produce the same product. Compared to the predecessor, it is possible to produce the same protein with similar efficacy and safety, but it is difficult to show identity due to the complicated molecular structure. Biosimilar is required to show equivalence and homogeneity. Unlike generic drugs, biosimilar development must meet the requirements as rigid as those for new drug development, and the hurdles are high.

Comparison of generic drugs and biosimilars

Generic drug |

Biosimilar |

|

Definition |

Drugs with the same active ingredient, route ofadministration, usage/volume, efficacy/effect asthe original drug |

If a safe volume exerts a sufficient effect, there arefew side effects. |

Product characteristics |

Small molecule compound |

Polymer compound |

Stable |

Ingenuity required for stabilization |

|

Easy to show identity |

The molecular structure is complicated, and it isdifficult to show identity. So, it is necessary toshow equivalence/homogeneity. |

|

Manufacturing |

Manufactured by chemical synthesis |

Manufactured by using cell culture technology,etc. |

Development requirements |

Bioequivalence test |

Comparison of quality characteristicsequivalence/homogeneityComparison of pharmacological actions andconfirmation of safety in non-clinical studiesEquivalence/homogeneity comparisonand safety confirmation in clinical trialsPost-marketing surveillance |

NHI price listing |

50% of the original product |

70% of leading biomedicine |

Source : Omega investment from various materials

In recent years, biosame (biomedicines that are produced by the same manufacturing equipment for the original biomedicine, and have the same molecular structure, but are sold by the original drug pharmaceutical company via its group companies) has emerged. Biosames are currently listed at 70% of the original drug price, which is the same as biosimilars. The appearance of biosame poses a threat to biosimilars as a competitor, and biosimilar manufactures are required to take actions such as further reduction of manufacturing costs.

Biosimilar’s revenue model consists of revenue from main drug substance supply to manufacturing pharmaceutical companies, and milestone revenue paid in accordance with the progress of drug development. The Company also earns revenue by concluding a joint R&D contract to provide its know-how to pharmaceutical companies.

As described above, the development of biosimilars requires advanced R&D capabilities and cost reduction know-how at the manufacturing stage, so only those with real experience can enter the market. The entry barrier is high. The Company was one of the first to pay attention to biosimilars and developed it by utilizing the technology, knowledge and know-how cultivated in new biomedicine development. The launch of GBS-001 in May 2013 marked the Company’s great achievement as a pioneer in the Japanese biosimilar market. Currently, the Company is the only bio-venture company that sells more than ¥1bn in biosimilars. It is ahead of other companies in the biosimilar competition.

See the table on the next page for the company’s current biosimilar pipeline. It has already launched three products, GBS-001, GBS-011 and GBS-007.

☆ GBS-001 (Filgrastim BS (biosimilar), target disease area: cancer)

A successor to predecessor GRAN® (Kyowa Kirin)/NEUPOGEN® (Amgen, USA). GRAN is preparation of G-CSF (granulocyte colony stimulating factor) used for neutropenia caused by cancer chemotherapy, which increases neutrophils. A joint research with Fuji Pharma Co., Ltd. started in October 2007, and Fuji Pharma and Mochida Pharmaceutical Co., Ltd. obtained domestic manufacturing and marketing approval in November 2012, and the medicine was launched in May 2013.

Biosimilar pipeline

The Company provides a stable supply of undiluted solution to Fuji Pharma, and Fuji Pharma and Mochida Pharmaceutical sell it in two brands and via two channels. The GBS-001-producing cell line is introduced from Dong-A ST Co., Ltd. (formerly Dong-A Pharmaceutical Co., Ltd., South Korea). In July 2022, Mochida announced that it would discontinue sales of Filgrastim BS.

☆ GBS-011 (Darpeboetin alpha BS, coping disease area: renal disease)

Epoetin Alpha, a treatment for renal anemia, enhances the sustainability of the effect. Its predecessor is NESP® (Kyowa Kirin) /Aranesp® (Amgen, USA). It was jointly developed with Sanwa Kagaku Kenkyusho Co., Ltd, which later in September 2019 obtained domestic manufacturing and marketing approval. It was launched in November 2019. Sanwa Kagaku Kenkyusho is solely responsible for manufacturing and sales, and the Company shares profits based on the sales.

☆ GBS-007 (Ranibizumab BS, target disease area: Eye Disease)

An angiogenesis inhibitor for treating age-related macular degeneration and other forms of sight loss. The preceding product is Lucentis (Novartis, Switzerland). In November 2015, a basic agreement on capital and business cooperation was signed with Senju Seiyaku K.K., a company with solid expertise in ophthalmology, followed by a joint commercialisation agreement in May 2016. In September 2020, Senju applied for approval to manufacture and market the drug in Japan. This was granted in September 2021, and the drug was marketed from December 9, 2021. GBS-007 is the first and only biosimilar in the ophthalmology field, and sales have been strong with good customer response. The company has decided to raise approximately 2 billion yen in order to expand its manufacturing capacity and secure working capital over the medium to long term. GBS-007 was licensed out to Ocumension Therapeutics for the overseas market and will be marketed in China and Taiwan.

In addition to the above three products, the Company schedules to launch the fourth product by FY2025 and plans to promote the development of highly cost competitive biosimilars. Candidates include Nivolumab BS (Opdivo), Pembrolizumab BS (Keytruda), Ravulizumab BS (Ultomiris), Brolucizumab BS (Beobu) and Ustekinumab BS (Stelara).

The market size of biosimilars is expected to reach 100 billion yen as the patents of biopharmaceuticals (original drugs) continue to expire (source: Fuji Keizai). In the general pharmaceutical market, the share of generic drugs in volume is approaching 80%, and the biosimilar market is expected to grow in the future.

Most recently, however, the market environment for biosimilars has become more challenging earlier than anticipated with the advent of biosame. Due to deteriorating profitability caused by the NHI price revision, Mochida Pharmaceutical announced the discontinuation of Filgrastim BS. Kidswell Bio has stated that it will promote the development of new, more cost-competitive biosimilars in the future.

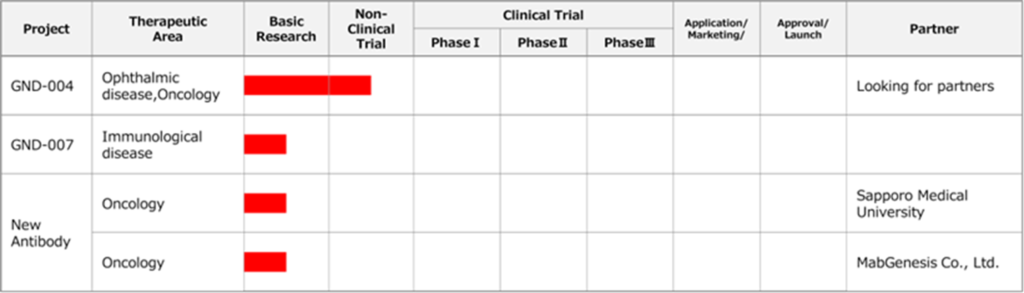

New biologics pipeline

New biologics

The development of antibody drugs has been the main business since the Company was founded. Currently, biomedicine comprises over 30% of the global pharmaceutical market, and 4 of the top 10 large-scale pharmaceuticals (blockbusters) are biomedicines.

The revenue model of the new biologics business can be divided into two. One is a service revenue, which is gained by concluding a joint R&D agreement at the research and development stage and providing the Company’s know-how to pharmaceutical companies. The other revenue comes from out-licensing patent to pharmaceutical companies. This includes lump-sum contract payments, milestone payments paid according to development progress, and royalty payments paid in accordance with sales after launch.

See the figure above for the Company’s new biologics pipeline.

☆ GND-004 (Anti-RAMP2 antibody, target disease: eye disease, cancer)

The Company succeeded in creating candidate antibodies for epoch-making new antibody drugs that inhibit neovascularization on a new mechanism, and applied for domestic and international patents. The Company is proceeding with non-clinical trials for a therapeutic drug candidate for patients with ophthalmology-related diseases for which existing preparations do not work and those cancer patients for whom Bevacizumab does not work. The Company will continue out-licensing activities to pharmaceutical companies.

☆ New antibody

The Company concluded a joint research agreement with Sapporo Medical University for developing anti-cancer drugs using antibodies that invade cancer cells in January 2020. Another joint research agreement for the acquisition of new antibodies that kill cancer cells was signed with MabGenesis Inc. in January 2020. The Company aims at out-licensing to pharmaceutical companies from both projects.

Creation of new therapeutic antibodies for malignant lymphomas: Malignant lymphomas are blood cancers in which some white blood cells (B cells and T/NK cells) become cancerous, accounting for about 10% of childhood cancers. There are few curative treatments for highly malignant lymphomas, and the mortality rate is high. CAR-T cell therapy has been developed for some B-cell lymphomas, but there are problems with substantial side effects and high treatment costs. The company is researching and developing antibodies with a new mechanism of action that binds to and directly kills malignant lymphoma cells.

Creation of new therapeutic antibodies against vasculitis: Vasculitis (e.g. Kawasaki disease) is an intractable disease that causes inflammation of the vessel walls, bleeding and thrombus formation, and impaired organ and tissue function. Current treatment methods include the administration of immunoglobulins. Still, there are safety concerns, and their effectiveness is insufficient for some children, so there is an urgent need to develop a curative therapy. The company is promoting research into the causes of vasculitis to identify the underlying causative substance. After placing the causative substance, the company aims to create an inhibitory antibody and a breakthrough treatment for vasculitis. The company estimates that the market for therapy for Kawasaki disease is worth approximately 4 billion yen, while the market for vasculitis is worth about 100 billion yen.

Creation of new therapeutic antibodies against pulmonary hypertension: Pulmonary hypertension is a group of progressive diseases that cause high blood pressure in the pulmonary arteries, leading to heart and lung dysfunction. It is a fatal disease with a five-year survival rate of 50% if untreated. Although treatment with vasodilators is available, their effectiveness is limited in patients with advanced disease. The company is developing inhibitory antibodies against a candidate for the underlying cause of pulmonary hypertension. The number of potential patients is estimated to be around 250,000 in Japan, and assuming 25% of these patients receive treatment, the market is expected to be worth approximately 250 billion yen.

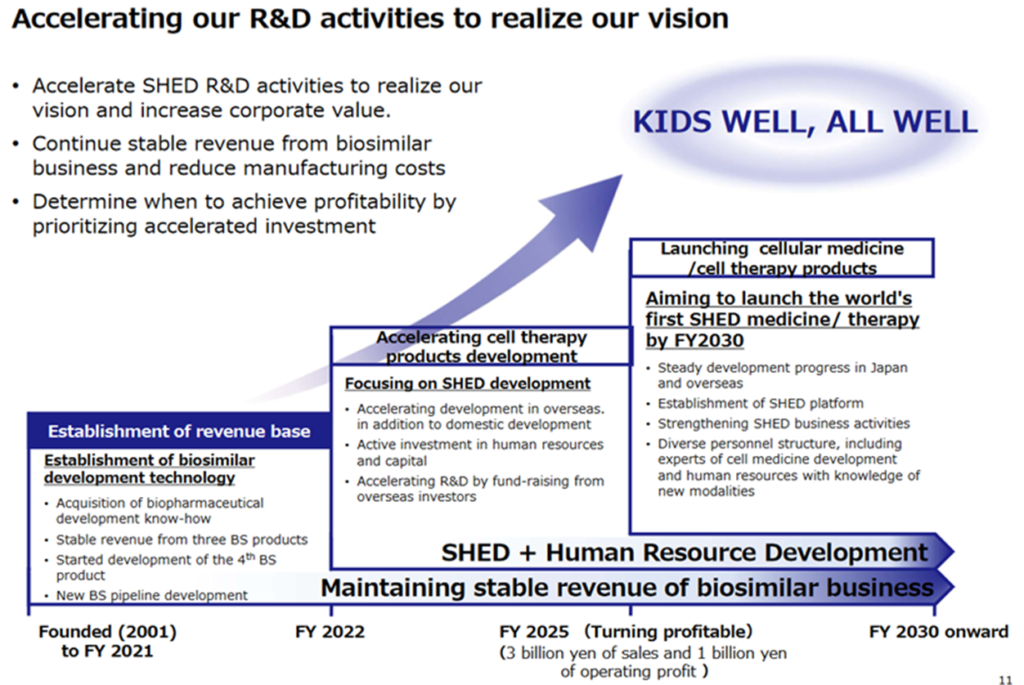

Mid-term strategic plan -KWB 2.0-

In May 2022, the company updated its already published mid-term strategic plan. It was intorduced as a mid-term strategic plan – KWB 2.0.

The points are

1) Increase upfront investment in the rapid start-up of the SHED business. For this end

・Promote SHED research and development by promoting new international developments.

・Continue domestic business, and accelerate development abroad.

・Bring SHEDs to market and put them into practical use by 2030.

2) The biosimilars and biotech new drug businesses will also continue.

The company cites the following reasons to have revised its mid-term strategic plan.

1) Changes in the external environment of the biosimilars market.

2) Implementation of a share price conscious development strategy.

Concerning (1) changes in the external environment of the biosimilars market, as previously mentioned, biosame’s entry into the market has started to affect the biosimilars market, pushing down the profitability of biosimilars. The company launched GBS-007 in December 2021, while Bayer Pharmaceuticals received approval for biosame (Eylea) in February 2022. A competitor biosame (Nesp) for GBS-011 is also on the market. It is anticipated that the inevitable competition with biosimilars due to a further increase in the number of biosames entering the market will make potential biosimilar partner pharmaceutical companies cautious about launching new biosimilars. As a result, the number of biosimilar projects with sufficient profitability is expected to decline.

About (2), an analysis of the share price movements over the past ten years shows that, although the company has made upfront investments with the funds raised since listing and has steadily launched three biosimilar products, the launch of biosimilars alone could not be expected to boost the share price. The company has decided that it cannot expect a significant increase in corporate value (i.e. share price) if the biosimilar business is the only way to achieve profitability. (See also FY2022/3 handout for the financial results, p 15).

On the other hand, the SHED business is progressing well, with the completion of MCBs. It is a logical choice to change course to focus more on the SHED business to increase future corporate value.

SHED’s research and development have been carried out in-house in Japan, so the company faces new challenges in the future, such as establishing overseas offices, raising funds from overseas markets and building networks with overseas medical institutions and academia. Many of the company’s managers have overseas experience, but a further strengthening of human resources will be necessary.

See the table above for the schedule of upfront investments. The company’s basic policy is to raise funds through equity financing. Considering the current share price level, dilution is a concern for investors. The ability of the management team to maximise corporate value by steadily implementing the roadmap shown in the chart below will be tested.

Mid-Term Strategic Plan –KWB 2.0– Roadmap

Financial results trends

1)FY2022/3 financial results – 57.5% increase in revenue, operating loss reduced by 0.5 billion yen

The company’s full-year results for FY2022/3 show a 57.5% increase in sales (1,569 million yen), an operating loss of 910 million yen (960 million yen of loss in the previous year) and a net loss attributable to the parent company of 530 million yen (a loss of 1.0 billion yen in the last year).

Sales of biosimilars (BS) GBS-001 and GBS-011 exceeded the plan, while the third product, GBS-007, which commenced sales in December 2021, contributed. Some sales of APIs (active pharmaceutical ingredients) related to the manufacturing process for the fourth BS product were also recorded. On the other hand, sales related to the SHED Master Cell Bank (MCB), which were initially expected to be recorded, were carried forward to the next financial year. All in all, the full-year forecast of 1.9 billion yen was not achieved.

In terms of profit, the gross profit exceeded the company forecast due to steady revenue from BSs. In addition, R&D costs were significantly reduced from the initial forecast of 1.8 billion (1.15 billion yen) due to flexible revisions of development costs, including a review of development related to JRM-001 following the transfer of a subsidiary (JRM). As a result, the operating loss was smaller than the initial forecast of 1.72 billion by posting 0.91 billion yen. As previously reported in the 3Q results, a gain of 0.41 billion yen on the sale of investment securities was recorded, resulting in a net loss attributable to owners of the parent reduced by 0.46 billion yen from the previous year.

◇Biosimilar business: GBS-007 is now manufactured and marketed

*Ranibizumab (GBS-007): The third product in the BS business, ranibizumab BS, an anti-VEGF antibody drug for the treatment of age-related macular degeneration, was launched on December 9 by development partner Senju Pharmaceutical. The anti-VEGF antibody drug market in Japan alone is expected to be worth under 100 billion yen in FY2020. The direct competitor Lucentis (Novartis Pharma) alone is expected to be worth approximately 27 billion yen. Being the first BS in the ophthalmology field, it attracts much attention. Before sales, the API was sold to Senju Pharmaceutical, contributing to earnings from 3Q.

*Filgrastim (GBS-001) and darbepoetin alfa (GBS-011): For BS, GBS-001 and GBS-011, which have already been launched by the partners, each of the revenues from API sales and royalties outpaced the plan. Ongoing cost reduction measures are also adding to improving profitability.

*Fourth BS: In addition to the above three products, the company is currently developing a fourth BS, intending to bring it to market by FY2025, having booked API sales in FY2022/3 related to API manufacturing process development.

◇Cell therapy business (regenerative medicine): each project progressed

In the cell therapy business, the company’s future focus, progress was made in each of the following areas.

*Master cell bank (MCB) completion: The company has been working on establishing a stable supply system for the raw materials required for research and development, an essential element in advancing the SHED business. The company has also established a SHED MCB supply system in partnership with ChiVo Net, which recruits donors for producing raw materials, university hospitals, Nikon CeLL innovation and others, and conducted final quality confirmation tests on MCBs produced under GMP standards, all of which were achieved.

*Designer cells: In December 2021, the company signed a contract development agreement with BioMimetics Sympathies (BMS) Inc. to develop ‘designer cells. BMS owns the culture medium development technology. By combining this with its SHED, the company aims to obtain cells with enhanced disease site-directedness while retaining the strong cellular characteristics of SHED that make it suitable for bone and neurological diseases. The company announced in September 2021 that it had signed a joint research agreement with NanoCarrier, and will focus on developing ‘designer cells’ as part of its response to modality diversification, leveraging its alliances with other companies.

Revenue trends

| JPY, mn, % | Net sales | YoY % |

Oper. profit |

YoY % |

Ord. profit |

YoY % |

Profit ATOP |

YoY % |

EPS (¥) |

DPS (¥) |

| 2019/3 | 1,021 | -3.6 | -805 | – | -816 | – | -856 | – | -43.84 | 0.00 |

| 2020/3 | 1,077 | – | -1,161 | – | -1,187 | – | -7,316 | – | -264.65 | 0.00 |

| 2021/3 | 996 | -7.5 | -969 | – | -991 | – | -1,001 | – | -34.79 | 0.00 |

| 2022/3 | 1,569 | 57.7 | -919 | – | -952 | – | -535 | – | -17.35 | 0.00 |

| 2023/3 (CE) | 2,900 | – | -980 | – | -999 | – | -1,000 | – | -31.82 | 0.00 |

| 2022/3 2Q* | – | – | – | – | – | – | – | – | – | – |

| 2023/3 2Q | 1,116 | – | 11 | – | -42 | – | -42 | – | -1.36 | – |

* Figures through FY2022/3 are on a consolidated basis. Figures for 1Q FY2023/3 and thereafter are on a non-consolidated basis, and year-on-year comparisons are not shown. Figures for 1Q FY2022/3 are on a consolidated basis and are for reference only.

Source: Omega Investment from Company materials

2) FY2023/3 2Q results – sales of 1,100 million yen, achieved positive operating profit

2Q results were sales 1,116 million yen, an operating profit of 11 million yen and a net loss of 42 million yen. Sales exceeded 1 billion yen for the first time on a half-year basis, and the company also achieved a surplus operating profit. (In April 2022, the consolidated subsidiary Japan Regenerative Medicine Co., Ltd. was transferred to Metcela Inc., so from this financial year, the company has been reporting on a non-consolidated basis.)

In terms of sales, GBS-007, the third BS product, has received more orders than expected since its launch in December 2021, contributing significantly to sales growth. Sales of existing BSs, GBS-001 and GBS-011, also remained strong. Moreover, 2Q sales included revenue related to the completion of the MCB for SHED, and milestone revenue from the fourth BS product appear to have been included.

In addition to an increase in gross profit backed by the growing BS business, the company achieved surplus at the operating profit level thanks to cost reductions and the curbing of R&D investment until the completion of MCB.

A bank loan of 1 billion yen was taken out at the end of June to secure working capital for the increased sales of GBS-007, with interest paid (13 million yen) and commission paid (30 million yen) recorded as non-operating expenses. Furthermore, a foreign exchange loss (10 million yen) related to the overseas manufacture of active pharmaceutical ingredients was registered as a non-operating expense, resulting in a recurring loss of 42 million yen.

Establishment of new COO position: As an R&D-oriented drug discovery venture, Masayuki Kawakami has led basic research and exploration as CTO. The management executive structure has been strengthened to expand the SHED business and promote clinical development and product strategy with a greater awareness of commercialisation in the future. Mr Kawakami has been appointed to the newly created Chief Operating Officer (COO) position. He will be responsible for translating basic research into clinical development and commercialisation.

Reinforcement of intellectual property strategy: The company has formulated and promoted R&D and business development strategies as a drug discovery venture company. As the SHED business expands, the company plans to focus on IP strategies in conjunction with R&D and business development strategies. Strategic patent applications and patent lifecycle management are promoted. In addition to domestic patent applications, the company will also promote the acquisition of patents in Europe, the US and major Asian countries. Specifically, the company intends to promote its IP strategy by filing ‘substance (cell) patents’ to differentiate SHED from other cells, ‘use patents’ to secure rights for the treatment of target diseases, and ‘formulation’ and ‘administration method’ patents to extend the patent term.

3) FY2023/3 full-year forecasts – no change in the initial estimates, but operating loss may lessen.

The company’s full-year forecasts for FY2023/3 – sales of 2.9 billion yen, an operating loss of 0.98 billion yen and a net loss of 1 billion yen – remain unchanged from those at the start of the fiscal year. However, as sales of GBS-007 and other BSs will likely remain strong, the company believes it can achieve its sales forecast. On the other hand, forecasting full-year R&D expenditure of 1.4 billion yen, the company expects an operating loss of 980 million yen. However, up to 2Q, R&D expenditure was 250 million yen. Even considering that R&D expenditure is heavily weighted towards the second half of the fiscal year, the company will unlikely spend more than 1 billion in the second half. Therefore, the full-year operating loss will likely be smaller than initially forecast.

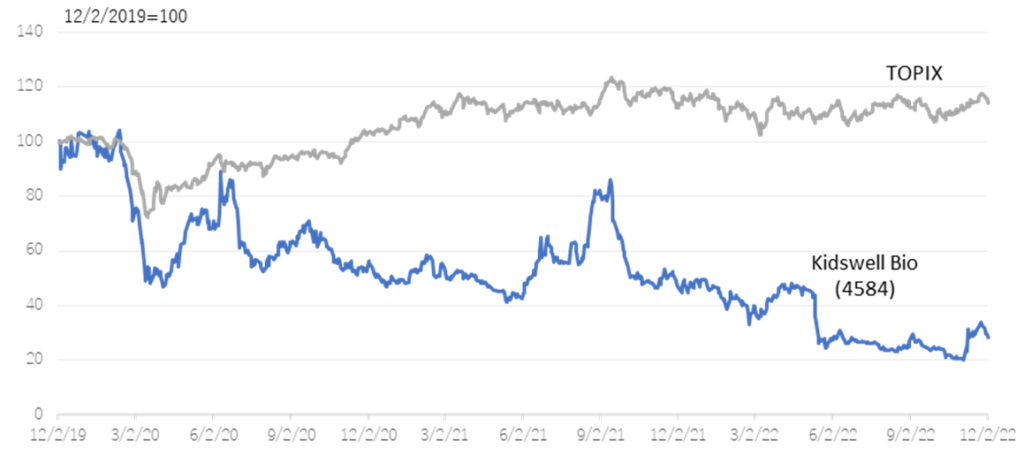

Stock price trends

Valuations based on standard financial analysis are difficult to apply for drug-discovery biotech ventures because of the limited short-term profit opportunities and long periods of losses. Calculations based on various methods of valuing companies are quite challenging to do rationally, given the unpredictable sales when a drug is launched and uncertainties until the drug is launched. The only way to make a comprehensive judgement would be to scrutinise the progress of the pipeline and the financing of research and development costs required for new drug development.

The company’s share price had adjusted sharply since the result announcement of FY2022/3 in May when it announced that it had postponed a return to profitability in FY2023/3. However, the share price rebounded sharply on the Nov 7 announcement of the publication of a paper on the results of research conducted in collaboration with Hamamatsu University School of Medicine. The share price went up further with the announcement of an operating surplus in 2Q FY2023/3. The share price hit a limit high on the 9th, the day after the results were revealed. On the 10th Nov, trading volume recorded 22.9 million shares, an exceptionally high level in recent years. In addition to completing the MCB, the company’s project to apply SHED to various diseases has become more concrete, clearing up uncertainty regarding the project. On the other hand, the share price looks undervalued, considering that the company’s PBR is still way below the three year average of 9.01 (see figure on next page). We will keep a close eye on the company’s share price to see when it returns to pre-May levels.

Stock price transition (last 5 years)

TOPIX Chart for TSE (last 3 years)

Historical PBR(4584, last three years, LTM)

Financial data

| FY (¥mn) | 2013/3 | 2014/3 | 2015/3 | 2016/3 | 2017/3 | 2018/3 | 2019/3 | 2020/3 | 2021/3 | 2022/3 |

| [Statements of income] | ||||||||||

| Net sales | 60 | 301 | 321 | 1,160 | 1,089 | 1,059 | 1,021 | 1,077 | 996 | 1,569 |

| Cost of sales | 15 | 141 | 147 | 500 | 397 | 422 | 412 | 653 | 119 | 550 |

| Gross profit | 45 | 159 | 174 | 660 | 692 | 637 | 609 | 424 | 876 | 1,018 |

| SG&A expenses | 403 | 671 | 998 | 1,480 | 1,876 | 1,550 | 1,414 | 1,585 | 1,846 | 1,937 |

| R&D expenses | 206 | 412 | 689 | 1,075 | 1,433 | 1,107 | 945 | 898 | 963 | 1,150 |

| Operating loss | -358 | -512 | -824 | -820 | -1,184 | -913 | -806 | -1,161 | -969 | -919 |

| Non-operating income | 0 | 0 | 34 | 50 | 35 | 11 | 3 | 1 | 2 | 2 |

| Non-operating expenses | 16 | 5 | 0 | 15 | 27 | 0 | 14 | 27 | 24 | 36 |

| Ordinary loss | -373 | -516 | -790 | -785 | -1,176 | -903 | -816 | -1,187 | -991 | -952 |

| Extraordinary income | 0 | 7 | 5 | 418 | ||||||

| Extraordinary expenses | 0 | 45 | 45 | 6,132 | 8 | |||||

| Loss before income taxes | -373 | -517 | -790 | -785 | -1,222 | -902 | -854 | -7,314 | -999 | -533 |

| Total income taxes | 3 | 2 | 1 | 1 | 2 | 1 | 1 | 2 | 1 | 1 |

| Net loss | -377 | -519 | -792 | -787 | -1,224 | -904 | -856 | -7,316 | -1,001 | -535 |

| [Balance Sheets] | ||||||||||

| Current assets | 919 | 1,881 | 1,092 | 1,520 | 3,421 | 2,692 | 2,821 | 3,322 | 3,346 | 3,325 |

| Cash and cash equivalents | 887 | 1,610 | 599 | 817 | 2,379 | 1,891 | 2,009 | 2,032 | 1,461 | 1,187 |

| Non-current assets | 3 | 4 | 54 | 173 | 284 | 332 | 329 | 269 | 587 | 177 |

| Tangible assets | 1 | 0 | 0 | 2 | 1 | 1 | 1 | 1 | 3 | 1 |

| Investments and other assets | 2 | 3 | 53 | 171 | 282 | 330 | 328 | 267 | 581 | 172 |

| Total assets | 922 | 1,886 | 1,146 | 1,694 | 3,706 | 3,025 | 3,151 | 3,592 | 3,933 | 3,503 |

| Current liabilities | 24 | 50 | 92 | 1,279 | 189 | 404 | 400 | 880 | 1,114 | 1,128 |

| Short-term borrowings | 810 | 25 | 75 | |||||||

| Non-current liabilities | 9 | 783 | 783 | 11 | 16 | 16 | 19 | 1,223 | 1,209 | 656 |

| Total liabilities | 34 | 833 | 876 | 1,290 | 205 | 421 | 420 | 2,104 | 2,323 | 1,784 |

| Total net assets | 888 | 1,052 | 270 | 403 | 3,500 | 2,604 | 2,731 | 1,487 | 1,610 | 1,718 |

| Total shareholders’ equity | 888 | 1,031 | 249 | 383 | 3,472 | 2,568 | 2,695 | 1,451 | 1,291 | 1,533 |

| Capital stock | 1,239 | 1,571 | 1,576 | 2,037 | 4,194 | 100 | 591 | 611 | 1,032 | 1,421 |

| Legal capital reserve | 1,143 | 1,474 | 1,479 | 1,940 | 4,097 | 3,372 | 3,864 | 9,917 | 10,337 | 10,726 |

| Retained earnings | -1,495 | -2,014 | -2,806 | -3,594 | -4,818 | -904 | -1,760 | -9,077 | -10,078 | -10,613 |

| Evaluation/conversion difference | -0 | 3 | 2 | 1 | -21 | 202 | ||||

| Subscription rights to shares | 21 | 21 | 21 | 23 | 32 | 34 | 57 | 116 | 184 | |

| Total liabilities and net assets | 922 | 1,886 | 1,146 | 1,694 | 3,706 | 3,025 | 3,151 | 3,592 | 3,933 | 3,503 |

| [Statements of cash flows] | ||||||||||

| Cash flow from operating activities | -304 | -729 | -970 | -607 | -1,759 | -438 | -860 | -1,325 | -1,267 | -1,169 |

| Loss before income taxes | -373 | -517 | -790 | -785 | -1,222 | -902 | -854 | -7,314 | -999 | -533 |

| Cash flow from investing activities | -0 | -1 | -49 | -121 | -149 | -50 | -0 | -137 | -22 | 526 |

| Purchase of investment securities | -49 | -116 | -149 | -100 | ||||||

| Cash flow from financing activities | 907 | 1,454 | 9 | 946 | 3,471 | 978 | 1,221 | 718 | 369 | |

| Proceeds from issuance of common shares | 917 | 234 | 9 | 486 | 3,932 | 973 | 40 | 138 | 369 | |

| Net increase in cash and cash equiv. | 601 | 722 | -1,010 | 217 | 1,562 | -488 | 118 | -240 | -571 | -273 |

| Cash and cash equiv. at beginning of period | 285 | 887 | 1,610 | 599 | 817 | 2,379 | 1,891 | 2,009 | 2,032 | 1,461 |

| Cash and cash equiv. at end of period | 887 | 1,610 | 599 | 817 | 2,379 | 1,891 | 2,009 | 2,032 | 1,461 | 1,187 |

| FCF | -305 | -732 | -1,021 | -729 | -1,909 | -488 | -860 | -1,462 | -1,289 | -643 |

Company Profile

Company Profile

Main business image

Kidswell Bio Corporation

【Head Office】

1-2-12, Shinkawa, Chuo-ku, Tokyo, 104-0033, Japan

https://www.kidswellbio.com/en/

【Laboratory】

Kita 21-jyo, Nishi 11-chome, Kita-ku, Sapporo

Center for Promotion of Platform for Research on Biofunctional Molecules, Creative Research Institution, Hokkaido University

Number of Employees : 39

History

| Month/Year | Event |

| Mar. 2001 | Gene Techno Science Co., Ltd. in Kita-ku, Sapporo City, with the aim of developing the results of functional research on immune-related proteins at the Institute for Genetic Medicine, Hokkaido University as diagnostic and therapeutic agents, and providing contract service services in drug development. Established (capital 10,000 thousand yen) |

| Jun. 2002 | Established a new research institute in the Hokkaido Center of the National Institute of Advanced Industrial Science and Technology to strengthen research and development of new biopharmaceuticals and start considering entry into the biosimilars business. |

| Nov. 2003 | Moved the head office to the laboratory |

| Jun. 2007 | Licensed out anti-α9 integrin antibody to Kaken Pharmaceutical Co., Ltd. in the new biopharmaceutical business |

| Oct. 2007 | In the biosimilar business, licensed in with Fuji Pharma Co., Ltd. for production cells and basic production technology for filgrastim biosimilars. |

| Apr. 2008 | Moved the head office to Chuo-ku, Sapporo |

| May 2008 | Relocated to the Institute for Genetic Medicine, Hokkaido University |

| Jun. 2008 | Established Tokyo office in Chuo-ku, Tokyo |

| Nov. 2012 | Fuji Pharma Co., Ltd. and Mochida Pharmaceutical Co., Ltd. acquired domestic manufacturing and sales products for filgrastim biosimilar products jointly developed with Fuji Pharma Co., Ltd. (launched in May 2013) |

| Dec. 2012 | Listed on the Tokyo Stock Exchange Mothers |

| Sep. 2013 | Relocated the research institute to the Center for Promotion of Biological Functional Molecular Research and Development, Hokkaido University Research Organization |

| Jan. 2014 | Concluded a joint development contract with Sanwa Kagaku Kenkyusho Co., Ltd. for darbepoetin alfa in the biosimilar business (launched in November 2019) |

| Mar. 2016 | Concluded a capital and business alliance agreement with NK Relations Co., Ltd. and Launchpad 12 GK (both are affiliated companies of Noritsu Koki Co., Ltd. and are currently absorbed and merged with Noritsu Koki Co., Ltd.). |

| Jun. 2016 | As a result of a tender offer for the Company’s shares by Noritsu Koki Bio Holdings GK (a company whose trade name was changed from GK Launchpad 12), the voting rights of the Company became over 50%, and Noritsu Koki Bio Holdings GK became the parent company of the Company together with NK Relations and Noritsu Koki. |

| Apr. 2019 | Made Advanced Cell Technology and Engineering Ltd. a wholly owned subsidiary of the Company through a share exchange. Due to the issuance of new shares in connection with the share exchange, Noritsu Koki Bio Holdings LLC and Noritsu Koki Co., Ltd. will have less than 40% of voting rights, and will no longer be the parent company and will become other affiliated companies. |

| Jul. 2019 | Moved the head office to Chuo-ku, Tokyo |

| Feb. 2020 | Made Japan Regenerative Medicine Co., Ltd. a wholly owned subsidiary by transferring shares from Noritsu Koki Co., Ltd. |

| Nov. 2020 | Advanced Cell Technology and Engineering Ltd. no longer an affiliated company as the Company sold all the stock. |

| Jul. 2021 | Company name changed to Kidswell Bio Corporation. |

| Apr. 2022 | Transfer from the Mothers market to the Growth market of the Tokyo Stock Exchange due to a review of the TSE’s market segment. |

| Apr. 2022 | Japan Regenerative Medicine Co. was excluded from the scope of consolidation following the transfer of all shares. |

| Aug. 2022 | Completion of the establishment of the stem cells from human exfoliated deciduous teeth (SHED) master cell bank. |

| Sep. 2022 | Basic transaction agreement with Showa Denko Materials K.K. for developing manufacturing methods for regenerative medical products and the manufacture of investigational drugs. |

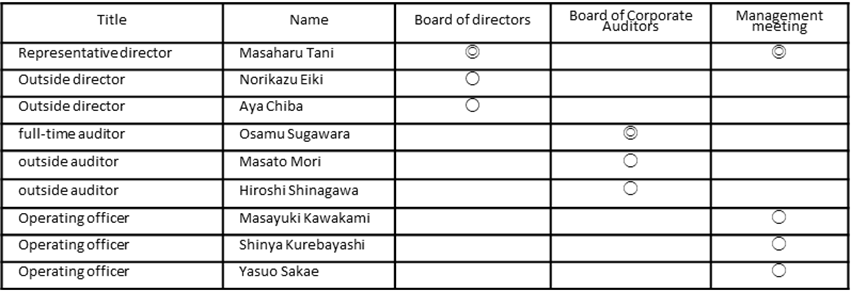

Management (Officer)

President & CEO:

Masaharu Tani

The Univ. of Tokyo, MSc, MBA.

Joined the Clinical Development Dept. at Suntory, implementing clinical trials and moved to Takeda Pharmaceutical, where worked at the Business Development Dept. and Strategic Product Planning Dept. After Takeda, joined Whiz Partners, a Japanese investment company in 2013 and joined GTS (currently KWB) in 2014. Appointed as CFO in 2015 and CEO in 2017 at GTS.

Corporate Officer, COO, Research & Development Div.:

Masayuki Kawakami

Kyoto Univ. Graduate School of Engineering, Ph.D.

Worked for research laboratories of FUJIFILM Corp. mainly in oncology area with Harvard Univ. and Novartis (then Sandoz). Worked for Toyama Chemical Corp. and then for FUJIFILM Pharmaceuticals USA to promote an anti-influenza drug clinical development. Joined GTS (currently KWB) in April 2017 and appointed as CTO in April 2018.

Corporate Officer, CBO, Business Development Div.:

Shinya Kurebayashi

Massachusetts Institute of Technology, MSc, Physics.

Worked in Investment Banking Div. at Goldman Sachs Japan and involved in M&A, IPOs and bond offerings of pharmaceutical and medical device companies at Morgan Stanley (Mitsubishi UFJ Morgan Stanley Securities). A member of launching ImPACT of Cabinet Office. In 2015, joined Advanced Cell Technology And Engineering Ltd. (ACTE) and established Administration Dept. and led business development and IPO preparation at ACTE. Joined GTS (currently KWB) in March 2019.

Corporate Officer, CFO, Business Administration Div.:

Yasuo Sakae

Graduated from the Faculty of Sociology, Hitotsubashi University. After being in charge of securities sales at the Tokyo branch of Commerzbank (a subsidiary of Commerzbank) and the head office in Germany, Sakae joined Yamanouchi Pharmaceutical Co., Ltd. (currently Astellas Pharma Inc.), mainly promoting the globalization of the finance division and established CVC (Corporate Venture Capital) and took the lead. Joined the Company in 2018 after working as CFO at Astellas US, General Manager of Procurement Department and General Manager of Management Promotion Department (in charge of budget and finance) at Astellas Pharma Inc., and Vice President, Corporate Strategy & Communications at Astellas Europe.

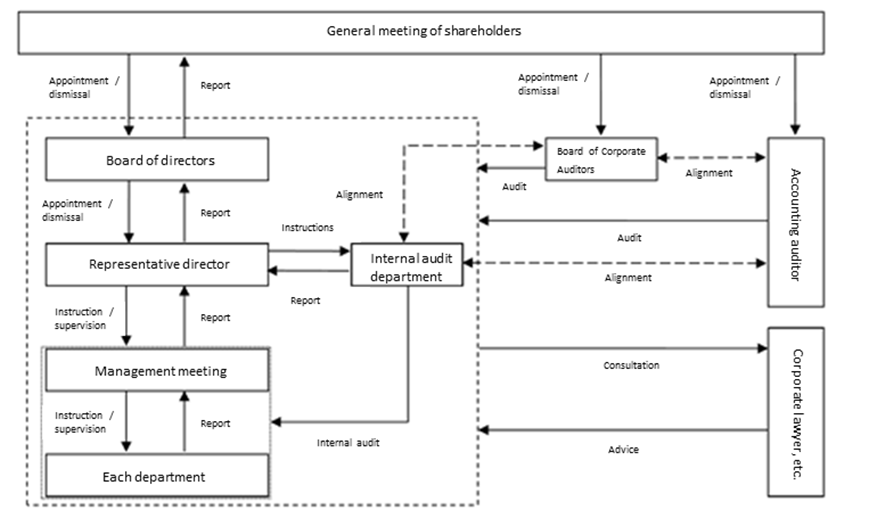

Corporate governance system

Members of each institution (◎ is the chair)

Status of major shareholders

| Name | Number of shares owned | Ratio of the number of shares owned to the total number of issued shares (%) |

| Noritsu Koki Co., Ltd. | 9,471,832 | 30.10 |

| Koichi Otomo | 1,206,150 | 3.83 |

| NanoCarrier Co., Ltd. | 1,000,000 | 3.18 |

| Nomura Trust & Banking Co., Ltd. (Trust Unit 2052241) | 721,000 | 2.29 |

| JSR Corporation | 686,814 | 2.18 |

| NINE Corporation | 610,000 | 1.94 |

| Senju Pharmaceutical Co., Ltd. | 555,200 | 1.76 |

| Taro Koike | 460,000 | 1.46 |

| Kinsei Tsuda | 436,800 | 1.39 |

| SBI Securities Co., Ltd. | 346,918 | 1.10 |

| Total | 15,494,714 | 49.23 |

Source : The Company quarterly report (FY2023/3 Q2)

Initiatives for SDGs

The company aims to create an organisational culture full of creativity and innovation, and to contribute to society by securing and developing human resources and organisational structures that lead to sustainable value enhancement. The company also states that it will seek to contribute to S (Social = Society) by providing new medical services.

Specifically, the Company will maintain the health of children, families, and people in the local community while providing necessary therapeutic agents and treatments. It will continue healthy growth as an enterprise and contribute to maintaining the sustainable social security system.

To realize new medical care from the perspective of children, as expressed in the corporate slogan “Kids Well, All Well”, the Company provides inexpensive and high-quality medical services by biosimilar business and reduces medical expenses for the elderly. The reduced costs can be allocated to pediatric diseases that tend to be neglected. This enhances pediatric disease medical care. Young stem cells that many children, including those saved by the improved medical care, can provide new medical care for intractable diseases that people of all ages could suffer. In its new company name, Kidswell Bio puts its wish to save children responsible for tomorrow by maintaining this cycle, and this is in addition to the wish to provide therapies for intractable and rare diseases, which the Company has been chasing since its inception. The Company is decided to contribute to developing new medicines and cures by making full use of its biotechnology nurtured up to now.