2026-08-03

Home

Japanese

Omega Investment Co., Ltd.

pluszero (Price Discovery)

Sell on Strength

Conclusion

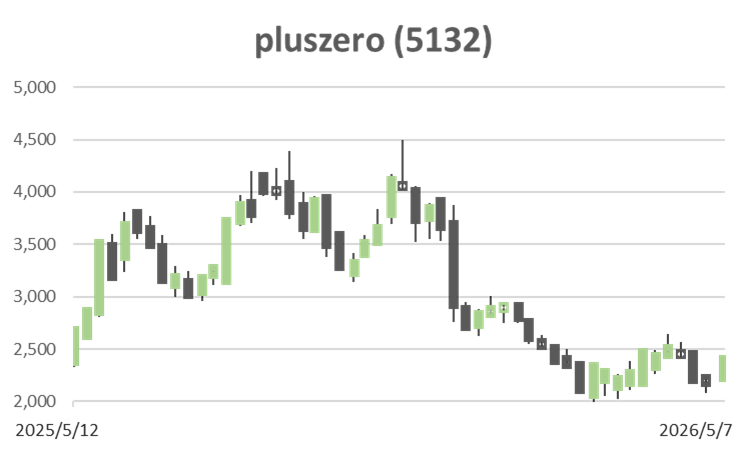

Sell on Strength. pluszero’s business quality and AEI commercialisation progress are clearly positive, but the current share price already discounts a substantial portion of future growth. The company is shifting from a simple AI contract development company to a high-value-added service-based AI company, centred on fourth-generation AI, AEI. Its gross profit margin, operating margin, ROIC, and operating cash flow are all high, and progress in introducing AI Operator and Brain Plus for Sales also indicates that the industrial application of AEI has begun to move from the demonstration stage to the commercialisation stage. On the other hand, the share price level, with a forecast PER of 39.4x, an actual PBR of 11.8x, and even a PER of around 37x after deducting net cash, already incorporates high EPS growth and AEI’s success to a considerable extent. Net cash is around 1.2 billion yen, which is only about 6% of market capitalisation, and the equity yield has consistently been below 2%, meaning the current share price does not offer a sufficient margin of safety. The quality of the business and the technical capabilities of the management team are evident, but caution remains warranted on the share price, and in phases where it strengthens, prioritising profit-taking is a reasonable judgement. The company plan for FY10/2026 calls for sales of 2,010 million yen and operating profit of 743 million yen, and profit progress at the 1Q stage is solid. However, sales growth remained at 4.3% YoY, and a clearer confirmation of the expansion of AEI-related sales will be necessary for a renewed re-rating.

Profile

An AI solutions company shifting from project-based AI/DX to high-value-added service-based revenue, centred on its proprietary AI, AEI

pluszero is a solutions company that provides design, development, maintenance, operations, and consulting services to address management and business issues for client companies by integrating technologies such as AI, natural language processing, and software and hardware. At present, it has a single segment, the Solutions Provision Business, and its mainstay is made-to-order AI/DX solutions. However, from an investment perspective, the essence of the company lies in its shift to service-based revenue using AEI, Artificial Elastic Intelligence, which it defines on its own. AEI is a dual-process AI model that the company positions as fourth-generation AI, and it aims to execute tasks after understanding meaning, like a human, by limiting its target to a specific genre. The company is developing AI call centre miraio, AI sales negotiation simulator Brain Plus for Sales, and AEIDesk, a collaboration platform for AI and humans, and is advancing commercialisation in areas such as AI Operator, AI coding, sales support and AEI for manufacturing. The management team consists of young members with advanced technical backgrounds, mainly graduates of the University of Tokyo, and the ability to combine technological and business development capabilities will determine the company’s future value.

Sales composition by business: Solutions Provision 100% in FY10/2025

| Securities Code |

| TYO:5132 |

| Market Capitalization |

| 18,516 million yen |

| Industry |

| Information / Communication |

Stock Hunter’s View

Strong inquiries for fourth-generation AI. Industrial application is entering full swing.

pluszero aims to develop and socially disseminate fourth-generation AI, AEI, a dual-process model that can understand meaning like a human, thereby overcoming the limitations of deep learning.

The Virtual Human Dispatch service using AEI is beginning to take off, and the company has already released AI call centre miraio, AI sales negotiation simulator Brain Plus for Sales, and AEIDesk, a collaboration platform for AI and humans. For FY10/2026, the company plans sales of 2.01 billion yen, up 30% YoY, and operating profit of 743 million yen, up 44% YoY. The AEI-related sales ratio is expected to rise from 24% in the previous fiscal year to 33%. The company cites AI Operator, AI coding and sales-related AEI services as areas with particularly significant impact on sales and profit.

In the recently announced first-quarter results for November 2025 to January 2026, a solid start was confirmed, with sales of 391 million yen, up 4.3% YoY, and operating profit of 126 million yen, up 0.4% YoY. Within this, AEI-related sales grew by 178% YoY, and the sales ratio reached 34%. AI Operator is now being prepared for introduction to seven companies, with one in the final stage of introduction, and the application of AI Operator technology to entertainment and other fields is also progressing. AEI’s industrial application is therefore beginning to gain momentum.

Investor’s View

Sell on Strength: Progress in AEI commercialisation can be appreciated, but the current share price is discounting the realisation of growth in advance

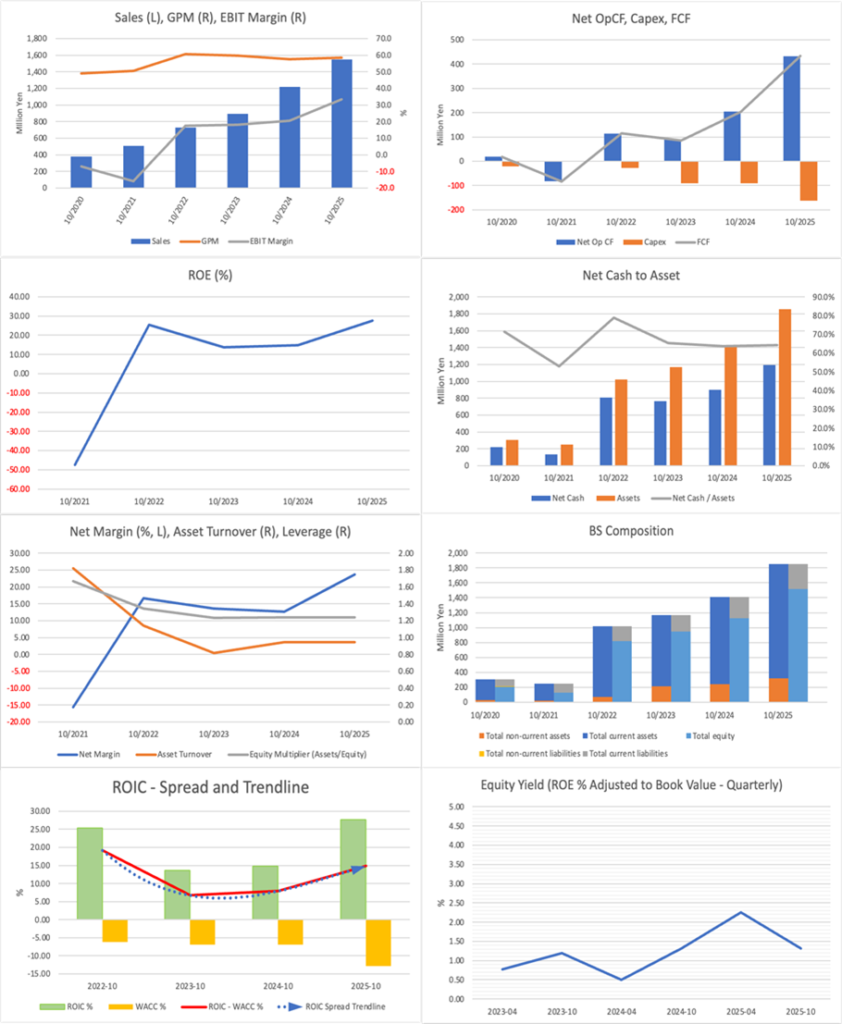

pluszero’s business fundamentals are clearly superior to those of other listed small-cap AI companies. Sales expanded to 1,546 million yen and operating profit to 516 million yen in FY10/2025, and the company’s plan for FY10/2026 calls for sales of 2,010 million yen and operating profit of 743 million yen. The gross profit margin is stable at a high level, and the operating margin is expected to rise from 33.4% in FY10/2025 to 37.0% in the FY10/2026 plan. This indicates that the company is not a loss-making growth company dependent solely on the AI theme, but a profitable company with high gross and operating margins. In 1Q, sales were limited to 391 million yen and operating profit to 126 million yen, and sales growth was sluggish at 4.3% YoY. However, the progress rate against the first-half operating profit plan was 48.8%, and the progress rate for net profit was 57.1%, so there is no excessive concern on the profit side about achieving the plan.

The important points in the company’s track record are that sales growth, margin improvement, operating cash flow and ROIC have improved simultaneously. Sales have expanded consistently since FY10/2021, and GPM has remained high. Operating cash flow has also improved, and FCF is also moving towards profitability and expansion. Furthermore, ROE has recovered to a high level, and ROIC has improved in a manner that exceeds WACC. This provides the basis for valuing the company not merely as a research-and-development type AI company, but as an AI growth stock with capital efficiency. The improvement in the net margin is also due to margin improvement, not to excessive financial leverage, and earnings quality is not poor.

On the other hand, there are clear constraints on the share price valuation. Given a forecast PER of 39.4x, an actual PBR of 11.8x, a forecast ROE of 31.7%, a forecast EPS of 61.1 yen, and no dividend, the current share price reflects continued high EPS growth. Assuming a terminal PER of 25x five years from now and a cost of equity of 8.5%, EPS growth in the high 18% range per annum would be necessary to justify the current PER. The EPS CAGR over the past five years is high, but this includes the start-up phase from a small profit base. The current share price is based not on past growth performance itself, but on the premise that the commercialisation of AEI will enable the company to maintain EPS growth in the high teens going forward.

Net cash is around 1.2 billion yen, and the company has a strong financial base with no debt. At the end of 1Q FY10/2026, cash and deposits stood at 1,095 million yen, and the equity ratio was 88.2%, providing sufficient capacity to continue growth investment. However, net cash is only around 6% of market capitalisation and does not materially reduce the share price. Even on a PER basis after deducting net cash, the multiple is around 37x, and the sense of undervaluation is limited. The equity yield has also consistently been below 2%, and even on a forecast PER basis, it is difficult to regard it as sufficiently attractive. Therefore, financial safety supports the valuation, but it does not justify aggressively buying at the current share price.

Looking at the three methods of PBR, DCF and ROIC, the current share price is close to the bullish DCF scenario. Under the PBR method, with a BPS of around 204 yen and an appropriate PBR of 6.0x to 9.0x, the fair share price range is around 1,220 to 1,840 yen, with a median of around 1,530 yen. Under the DCF method, using an EPS of 61.1 yen as the starting point and incorporating high growth over five years followed by deceleration, the range is approximately 1,540 to 3,460 yen, with a median of approximately 2,510 yen. Under the ROIC method, assuming an FY10/2026 operating profit of 743 million yen, an after-tax operating profit, a WACC of 8% to 9%, and medium- to long-term growth of 3% to 4%, the range is approximately 1,110 to 1,600 yen, with a median of approximately 1,410 yen. The median of the three methods is around 1,530 yen, and the current share price, in the 2,400-yen range, is significantly above it. Valuation toward the upper end is justified only if AEI scales in earnest as a high-margin service.

The background to the lacklustre share price from 2025 to early 2026 should be viewed not as business deterioration, but as a correction of excessive valuation. Earnings are solid, and the AEI-related sales ratio is also expected to rise from 24% in FY10/2025 to 33% in the FY10/2026 plan. Even at the 1Q stage, AEI sales grew by 178% YoY, and the AEI sales ratio rose to 34%. AI Operator is under preparation for introduction at seven companies, including four Prime Market-listed companies, and signs of commercialisation are visible. Even so, the reason the share price finds it difficult to move higher is that the market has already moved from asking about the AI theme to asking how quickly and at what scale AEI will convert into profit. The fact that sales growth remained at 4.3% in 1Q also reinforces this cautious stance.

Ownership has clear merits and drawbacks for investment judgment. Among the largest shareholders are Yoshiyuki Shodai at 25.76%, Motoki Nagata at 11.88%, Ryota Mori at 10.98%, Ai Shodai at 5.10%, and ABIST at 4.05%, with the total shareholding ratio of the major shareholders reaching 68.05%. The high shareholding ratio of founders, management, and related parties strengthens alignment between management and shareholders and supports continued medium- to long-term technological and business development. In particular, for a company such as this, where the commercialisation of the proprietary technology AEI requires time, an ownership structure that is not overly influenced by short-term market pressures is significant. On the other hand, the limited free float and the difficulty for institutional investors to build meaningful positions constrain liquidity and valuation stability. The share price is prone to upside swings on thematic interest, but when expectations unwind, buying support also tends to be thin.

Regarding management, the fact that it is a highly educated and young group of technologists centred on graduates of the University of Tokyo is an important competitive strength for the company. Excluding outside directors, the average age is in the late 30s, and a deep understanding of AI, natural language processing, mathematical models and software development can be a clear advantage in a technology-led business such as AEI. The fact that young management members hold large equity stakes can also be evaluated as a strong commitment to improving corporate value. However, from an investor’s perspective, research and development capability and capital market capability as a listed company are separate abilities. Going forward, the company needs to demonstrate not only technological capability but also a shift to service-based revenue, sales expansion, an increase in the number of companies adopting it, and the reproducibility of the revenue model, all backed by concrete numbers.

What should be asked in the current investment judgement is not the future potential of pluszero itself, but how much of an appropriate price the current share price is demanding for that future potential. Among AI-related small-cap growth stocks, the company is high quality across gross margin, operating margin, ROIC, financial base, and management’s technical capabilities. If AEI’s industrial applications advance, there is ample growth potential beyond its current earnings scale. However, the share price already incorporates that future picture to a considerable extent and does not give investors a sufficient margin of safety. In phases where the share price rises on strong earnings progress or expansion in AEI adoption, prioritising profit-taking is a reasonable judgment.

Financials and Valuations

Price

PBR (LTM)

PER (LTM)

ROE (LTM)

EPS (Actual)