2026-08-03

Home

Japanese

Omega Investment Co., Ltd.

Ishikawa Seisakusho (6208)

Sell

Conclusion

Sell: The share price has surged amid the overlap between the defence theme and recent earnings performance, yet it is clearly overvalued relative to fundamentals. From the perspective of earnings sustainability and capital efficiency, there is a high hurdle for further re-rating.

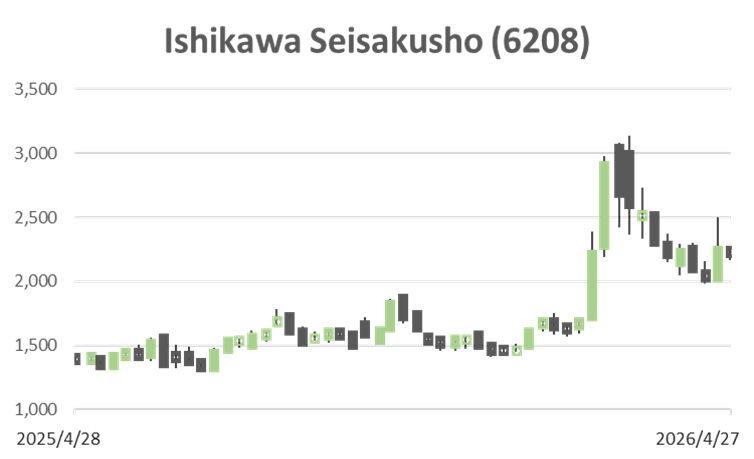

Against the backdrop of policy drivers such as the relaxation of export restrictions on defence equipment and the expansion of the defence budget, Ishikawa Seisakusho achieved significant profit growth in the third quarter of FY3/2026, with revenue of 11,655 million yen (+11.8% YoY) and operating profit of 910 million yen (+65.2% YoY). As a result, the share price has surged year-to-date, and its positioning as a defence-related stock has strengthened further.

On the other hand, the combination of a forecast PER of 32.6x, PBR of 2.37x, and ROE of 7.4% can be interpreted as implying a medium-term EPS growth rate of approximately 5–8% per annum in the share price. At the same time, the company’s earnings structure is highly dependent on project timing and raises concerns about the stability of cash flow and capital efficiency. The median fair value derived from the three methods of PBR, DCF, and ROIC is approximately 1,200 yen, and the current share price is at a level significantly exceeding this.

While the company positions a high-value-added defence equipment business at its core, the presence of low-profit businesses and the sustainability of capital efficiency indicate that a qualitative shift in earnings growth is required to justify the current valuation. In the short term, upside supported by thematic factors and supply-demand dynamics cannot be ruled out; however, from an investment perspective, profit-taking during the upward phase is considered rational.

Profile

| Securities Code |

| TYO:6208 |

| Market Capitalization |

| 14,170 million yen |

| Industry |

| Machinery |

Stock Hunter’s View

A representative small- and mid-cap defence-related stock. Tailwinds include budget expansion and the easing of weapons export restrictions.

Ishikawa Seisakusho is not only a manufacturer of paper machinery, such as corrugated box-making and printing machines, but also a well-known small- to mid-cap defence-related stock in Japan. The company began producing defence equipment in 1936, when the wartime atmosphere was intensifying. Three years later, in accordance with national policy, it fully shifted to military production and subsequently produced naval mines and depth charges until the end of the war.

It manufactures naval mines for the Japan Maritime Self-Defence Force and is a de facto domestic monopoly supplier. In 2017, it acquired Kanto Aircraft Instrument Co., Ltd. (Fujisawa City, Kanagawa Prefecture), which manufactures electronic equipment (flight recorders) for defence aircraft for the Japan Air Self-Defence Force, thereby strengthening its presence in the aircraft field. Its major customers are the Ministry of Defence and Mitsubishi Heavy Industries.

On April 21, the Japanese government decided to abolish the five categories (rescue, transport, warning, surveillance, and minesweeping) that had imposed restrictions on the export of defence equipment. There is a view that Japan’s defence industry will contribute particularly in missile-related areas, where inventories are believed to have declined. The abolition of the five categories and the expansion of the defence budget are expected to act as tailwinds in the medium to long term.

The benefits have already begun to appear in the numbers. In the previously announced third quarter of FY3/2026 (April–December), the company achieved revenue of 11,655 million yen (+11.8% YoY) and operating profit of 910 million yen (+65.2% YoY), representing a substantial increase in profit.

Investor’s View

Sell: The share price has been re-rated due to the overlap of policy themes and short-term earnings, and at the current level, it is overvalued relative to sustainable earnings growth and capital efficiency.

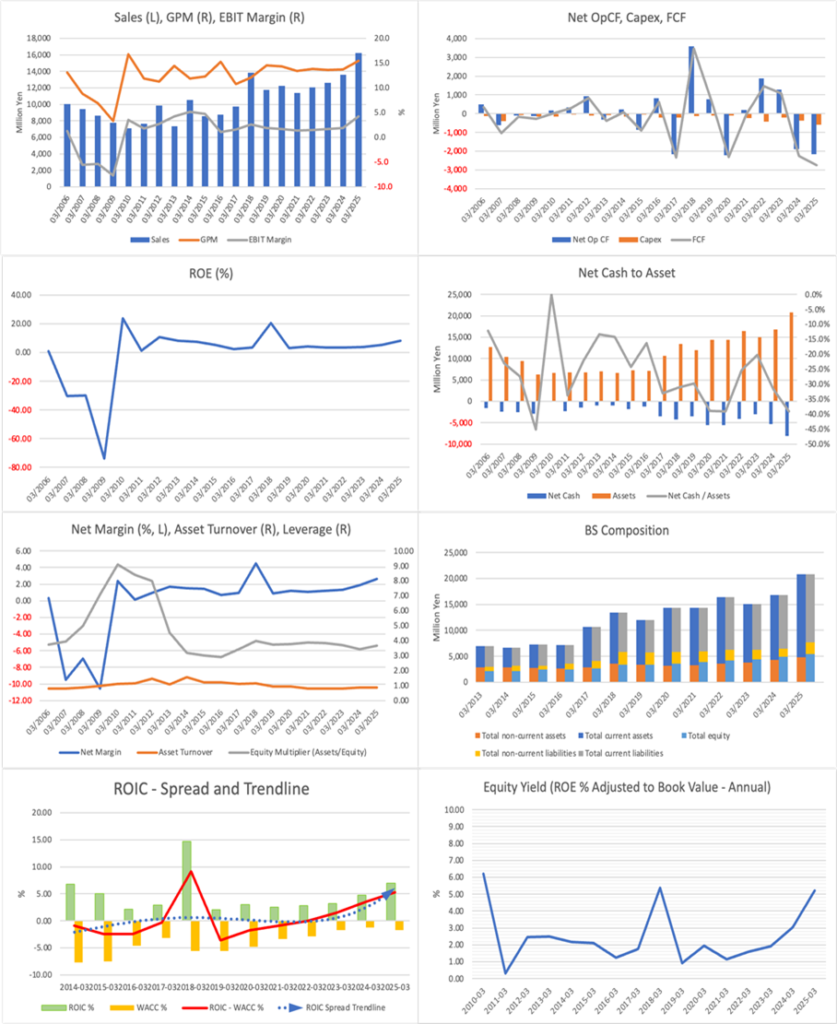

The company’s business structure is characterised by the coexistence of a high-value-added, high-margin defence equipment business and low-profit businesses centred on paper machinery. Defence equipment accounts for approximately 70% of revenue. It is the core of earnings, with an operating margin of 12%, whereas paper machinery is close to loss-making, resulting in a highly skewed portfolio. This structure constrains ROE and the stability of consolidated cash flows.

As confirmed in the graphs, revenue is on a gradual growth trend, whereas operating margin and ROE remain within a certain range of fluctuation, and cash flow also fluctuates significantly. This reflects a business model that depends on the timing of defence-related orders and suggests characteristics more akin to a project-based company than to a stable-growth company. Although the ROIC spread is generally positive, its level is not high, and it is difficult to conclude that a clear superiority in capital efficiency has been established.

The recent sharp rise in the share price is attributable to the simultaneous occurrence of policy themes such as the relaxation of export restrictions on defence equipment and the expansion of the defence budget, together with confirmation of performance through increased defence equipment sales and substantial profit growth. In past share price movements, the stock has tended to surge when defence-related themes became apparent, and even when earnings improved to some extent thereafter, the share price has not been easily sustained at higher levels.

In fact, a valuation based on a forecast PER of 32.6x and PBR of 2.37x is consistent with a medium-term EPS growth rate of approximately 5–8% per annum. However, the historically high EPS growth rate has been driven by a recovery from a low base and project contributions, and the likelihood that this growth will be sustained is low. The fair value estimates from the three methods range from 1,000 to 1,800 yen, with a median of approximately 1,200 yen, whereas the current share price significantly exceeds this range.

From the perspective of ownership, while the presence of stable shareholders provides a certain degree of downside support, participation by overseas institutional investors remains limited, and the share price tends to be influenced more by thematic fund inflows than by fundamentals. As a result, in upward phases, overheating driven by supply-demand dynamics is likely, whereas in phases when themes subside, there is an inherent risk that valuations will contract rapidly.

Overall, the company is an event-driven stock closely linked to defence policy, and the current share price reflects thematic factors rather than improvements in fundamentals. For a sustained re-rating, improvement in earnings stability, structural reform of low-profit businesses, and a clear enhancement of capital efficiency are essential. At present, these have not yet been sufficiently confirmed.

Financials and Valuations

Price

PBR (LTM)

PER (LTM)

ROE (LTM)

EPS (Actual)