2026-08-05

Home

Japanese

Omega Investment Co., Ltd.

ibis inc. (Price Discovery)

Buy

Conclusion

Buy: ibis is an asset-light, highly profitable company that generates extremely high ROE and ROIC, with its mobile painting app, “ibisPaint,” at its core. The current share price remains at a forecast PER of 11.9x. Furthermore, given that net cash accounts for approximately 16% of market capitalisation and the cash-adjusted PER is 9.9x, the market values the stock quite conservatively. There are reasons for the low PER, including fluctuations in advertising unit prices, dependence on platforms, losses in the AI singing voice synthesis business, and the recovery of investment after M&A, but given the shift to subscription sales, the high operating margin of the Mobile business, and the large cash position, the current share price looks to have excessively priced in risks. Shareholder returns have been driven mainly by dividends, but there remains room for improvement in capital policy, including share buybacks. If this point is clarified, the share price should be significantly re-rated.

Profile

An asset-light, highly profitable app development company whose core earnings are ibisPaint, which has a global user base

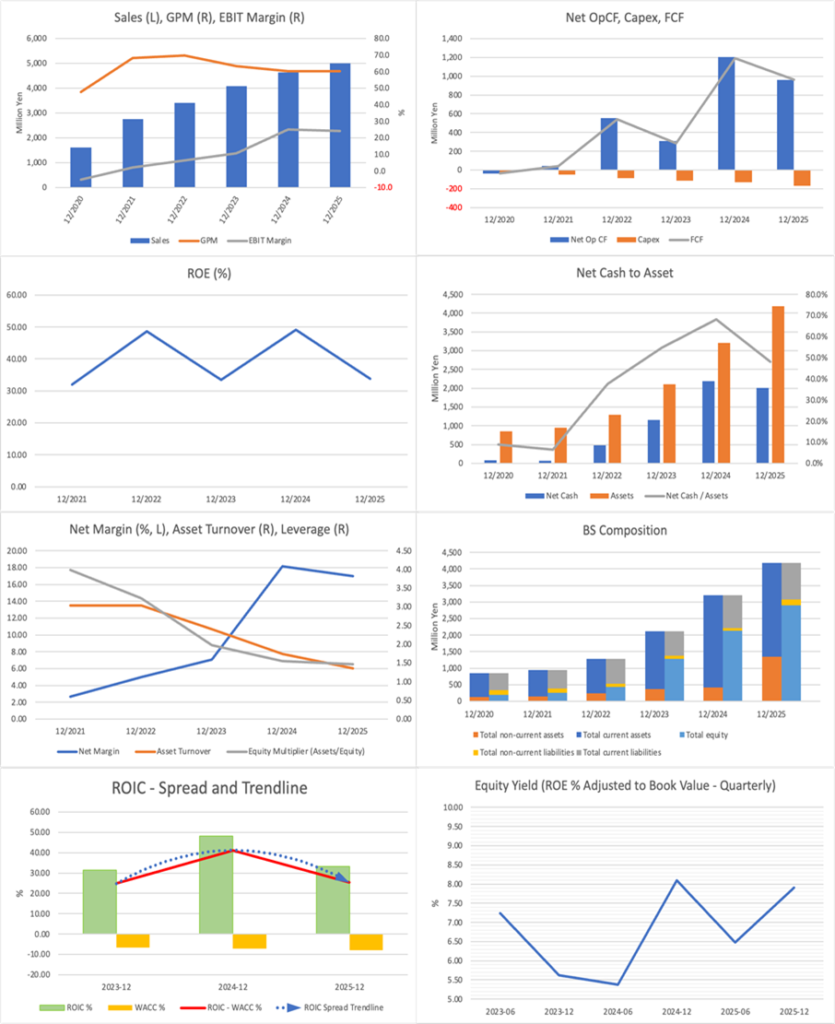

ibis operates the Mobile business, centred on the development and operation of the mobile painting app “ibisPaint”; the Solution business, which provides application development support for smartphones and tablets and dispatches IT engineers; and the AI Singing Voice Synthesis business, which develops the AI singing voice synthesis app “VoiSona” and other services. ibisPaint is used in more than 200 countries and regions worldwide, and cumulative downloads reached 520.52 million as of the end of December 2025. In addition to conventional app advertising, the earnings structure has expanded to subscription billing and one-time purchase apps, and in FY12/2025, app billing sales exceeded app advertising sales. Going forward, growth themes will include multi-device expansion through the launch of the Mac version, development of the professional-use market, the addition of AI functions, and the creation of synergies with Techno-Speech.

Sales composition by business % (operating margin %): Mobile 57 (53), Solution 41 (13), AI Singing Voice Synthesis 2 (-52) (FY12/2025)

| Securities Code |

| TYO:9343 |

| Market Capitalization |

| 12,451 million yen |

| Industry |

| Service |

Stock Hunter’s View

A painting app whose user base is rapidly growing in the SNS era. The shift from “free” to “subscription” is progressing well.

ibis operates “ibisPaint,” a mobile painting app that lets users draw illustrations on their smartphones. Overseas users account for 94% of cumulative downloads, and the share of users under 25 is 91.7%, making it the painting app closest to the creative activities of the Alpha and Z generations.

The sources of revenue are app advertising sales for the free version and app billing revenue, including subscription sales from the premium membership service and one-time purchase app sales. Around 2024, the revenue ratio between subscription and non-subscription reversed, and subscriptions are now the pillar of earnings. The company’s app has high customer satisfaction, many app downloads come from natural inflows such as word of mouth, and MAU (monthly active users) is also high. Advertising expenses have fallen to less than half their previous level, but the company has already established an overwhelming user share through many years of overseas advertising investment, and it has been proven that even halving advertising expenses has almost no impact on sales growth.

In the previous fiscal year ending December, subscription billing sales maintained a high growth rate of 71.6% YoY and strongly led the harvest phase. The company plans to grow subscription billing sales to 2.79 billion yen over the next three years, 2.3 times the previous fiscal year’s result, and aims for operating profit growth of 20% or more from FY12/2027 onward.

Investor’s View

Buy: Considering the high ROE, ROIC and net cash, the current low PER excessively prices in business risks.

The most important point in the investment judgement for Ibis is that the company is not merely a small-cap app company, but has already, to a considerable degree, established an asset-light global software revenue model. Consolidated ROE in FY12/2025 was 29.9%, ROE on a non-consolidated basis was 37.2%, and the Shikiho forecast ROE for FY12/2026 is also high at 36.6%. This is due to a structure in which ibisPaint does not require large-scale factories, stores, or inventories, and can provide services to users worldwide through development personnel and platform distribution. Although the Mobile business accounts for 57% of sales, its operating margin is 53%, improving the company’s overall capital efficiency.

The background to the high ROIC is also the same. ibisPaint is a model that uses a broad user base generated through free use as the entry point and monetises it through advertising revenue, subscriptions, and one-time purchase apps. Cumulative downloads exceed 500 million, and the overseas ratio is also high. Moreover, in FY12/2025, app billing sales exceeded app advertising sales, improving the quality of revenue. Advertising revenue is affected by eCPM and advertising market conditions, but subscriptions have high continuity and high profit margins. This is why the company’s high ROE and ROIC can be assessed as not temporary but rather structurally driven.

On the other hand, the reason why the PER is low is also clear. The forecast PER of 11.9x is low given the current ROE level and, on the surface, appears to indicate undervaluation. However, the market is discounting the combined dependence on ibisPaint and on platforms such as Google and Apple, the downside in advertising unit prices, losses in the AI singing voice synthesis business, the amortisation of goodwill and technology-related assets following M&A, and liquidity constraints as a Growth Market-listed stock. The company’s forecast operating profit growth rate for FY12/2026 is also 12.8%, and, compared with the rapid growth over the past several years, it is normalising. Therefore, the low PER reflects not only market irrationality but also a lack of confidence in the sustainability of growth.

Nevertheless, the EPS growth expectation priced into the current share price is only approximately 8% per annum. This is extremely low compared with an EPS CAGR of approximately 61% from FY12/2021 to the FY12/2026 forecast. Of course, past high growth cannot simply be extended into the future. However, considering the expansion of subscription contracts, professional-use and multi-device expansion, AI function billing, and synergies with VoiSona in the creator domain, an expected growth rate of around 8% per annum is excessively cautious.

The presence of net cash is also an important support for the investment judgment. Net cash amounts to approximately 16% of market capitalisation, and the net cash-adjusted PER remains at 9.9x. This means that the market is assigning an earnings multiple of less than 10x to business value excluding cash. Considering the high ROE, high ROIC, the Mobile business’s high operating margin, and the rising subscription ratio, this valuation is extremely conservative.

Regarding capital policy, it cannot be said to be aggressive at present. The dividend for FY12/2025 was 10 yen, the forecast for FY12/2026 is 12 yen, and the forecast payout ratio is 23.4%. This is reasonable for a phase in which growth investments, investment in development personnel, and M&A are prioritised, but when net cash is large, and the share price remains at a low PER, there is room to present capital policy options more clearly, including share buybacks. In particular, if the company can clearly distinguish between cash required for business investment and surplus funds, M&A investment discipline, and the shareholder return policy, this may lead to an upward revision of valuation.

Ownership also affects the valuation of the share price. Founder Eiji Kamiya holds approximately 48.1% of the shares; the total holding ratio of all holders is approximately 70.5%, and the float remains at approximately 30%. This is a strength in terms of management’s long-term orientation and stability of control. On the other hand, it imposes constraints on institutional investor ownership, liquidity, and the price discovery function. To broaden the institutional investor base, including overseas investors, English-language IR, capital policy, recovery of investment in growth investments, and continuous disclosure of subscription KPIs will be important.

After attracting high expectations at the time of the 2023 IPO, the share price was once re-rated on the back of a large increase in profit in 2024, but since 2025, despite high profitability, the upside has been limited. This is not due to poor earnings but to PER compression driven by the normalisation of growth rates and the reassessment of risk factors. Conversely, if the high profitability of the Mobile business is maintained, subscription sales stably exceed advertising sales, the deficit in the AI Singing Voice Synthesis business narrows, and capital policy becomes clearer, the current low valuation multiple could be corrected.

The median fair value calculated by the three methods is approximately 817 yen, implying upside of approximately 22% from the current share price of 672 yen. Even the lower end of the range is roughly in line with the current share price, and the DCF method also allows for a valuation near 1,000 yen. Downside risks include a further decline in advertising unit prices, a slowdown in subscription growth, and delays in recovering investment from M&A. On the other hand, the keys to upside are the continuation of the Mobile business’s high profitability, further progress in the shift to subscriptions, and the presentation of measures to improve the capital efficiency of the large net cash position. The current share price does not sufficiently price in these positive factors.

Price

PBR (LTM)

PER (LTM)

ROE (LTM)

EPS (Actual)