2026-08-03

Home

Japanese

Omega Investment Co., Ltd.

Komeda Holdings (Price Discovery)

Sell on Strength

Conclusion

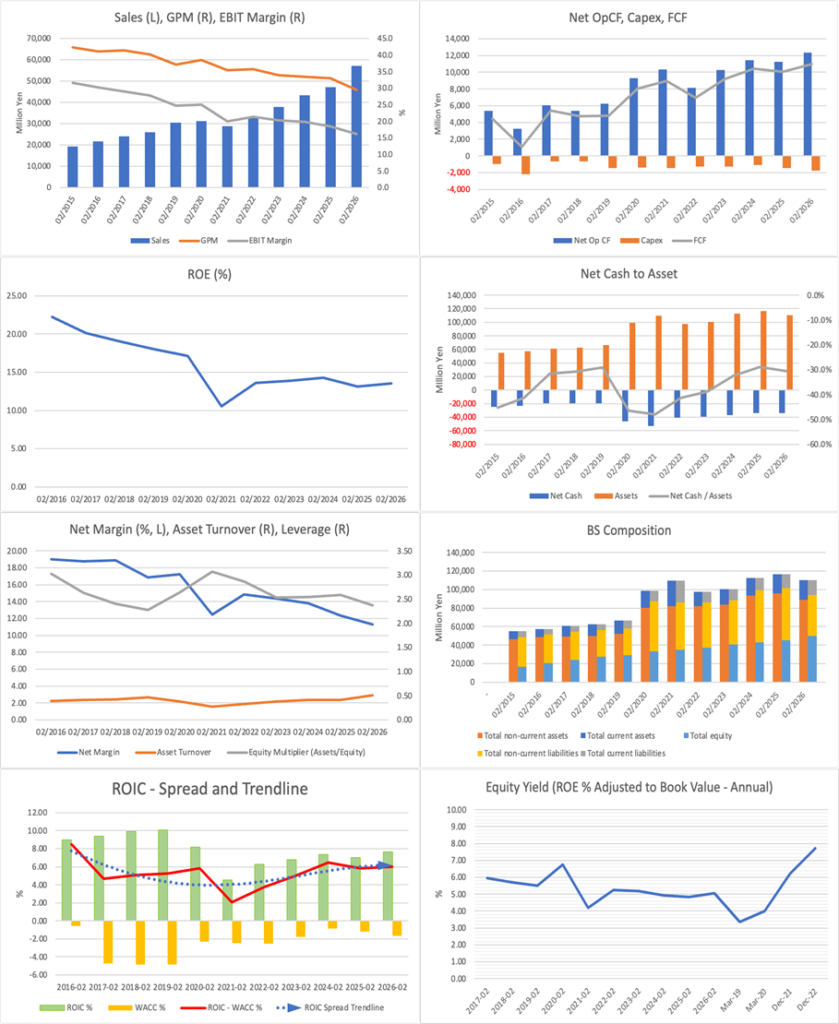

Sell on Strength: Over the past ten years, revenue and operating cash flow have grown steadily, and ROE and the ROIC spread have remained at healthy levels. On the other hand, the gross profit margin and EBIT margin have continued to decline, and the already sufficiently high equity ratio has risen further. The quality of the business is high, but the share price has already broadly priced in that strength, and any further re-rating would require a reversal in profitability and a review of capital policy.

Thanks to its FC headquarters-type earnings structure, the company has maintained high capital profitability and stable cash generation even as profit margins have gradually declined. That is a clear strength of the company. That said, from the perspective of equity investment, its capital structure remains overly conservative relative to the stability it provides, leaving something to be desired in terms of maximizing shareholder value. The current share price has already placed a considerable valuation on stable growth, strong cash generation, and steady shareholder returns, and to justify a further leg up from here, continued store openings alone will not be enough; a bottoming out in the gross profit margin and profitability, or a more decisive move in capital policy, will be required.

Profile

A high-quality operator of a domestic coffee shop chain that combines growth and shareholder returns through the strong cash-generating capacity of its FC headquarters model.

The company is the FC headquarters centred on “Komeda Coffee” and “Okagean,” with a revenue structure that combines wholesale sales of food ingredients to franchisees, royalty income, and sublease income. Its source of differentiation lies in having refined the coffee shop format not as a mere foodservice business but as a time-consumption business that sells comfort itself. As of the end of FY02/2026, the total number of stores had expanded to 1,150, of which 83 were overseas. Under the new medium-term management plan, “CONNECT 2030,” the company is targeting an operating profit of 13.0 billion yen, 180 overseas stores, and a cumulative total shareholder return ratio of 50% or more in the final year.

Revenue composition by business (%), operating margin (%): Domestic 90 (22), Overseas 10 (2) (FY2/2026)

| Securities Code |

| TYO:3543 |

| Market Capitalization |

| 144,367 million yen |

| Industry |

| Wholesale business |

Stock Hunter’s View

Operating profit surpassed 10.0 billion yen, heading toward a fifth consecutive year of record-high earnings – unique positioning enabled by the full-service and FC model.

Komeda HD operates 1,150 stores in Japan and overseas as of the end of February 2026, with its main format being the full-service coffee shop “Komeda Coffee,” which focuses on comfort. The majority of its stores are FC (franchise) outlets, and it generates stable earnings through wholesale sales of food ingredients to franchisees and royalty income.

At 460 yen per cup of coffee and up, its prices are high for a coffee shop chain, but unique menu items such as “Shiro-Noir,” which places soft-serve ice cream on top of Danish pastry, as well as generously portioned food and drinks referred to as “reverse photo fraud,” have proven popular and helped it secure a repeat customer base. Even when the foodservice industry was hit hard during the COVID-19 pandemic, the company remained profitable, and its earnings have continued to perform well amid the recent surge in prices, underscoring its strength under headwinds.

The results for FY02/2026, announced on April 8, fell short of the company’s plan, but the company still posted higher revenue and earnings, with revenue up 21.6% and operating profit up 6.8%. In the current fiscal year, it expects revenue of 60.92 billion yen, up 6.5% YoY, and operating profit of 10.2 billion yen, up 8.2% YoY, marking a fifth consecutive year of record-high earnings. In addition to a recovery in the pace of new store openings for domestic “Komeda Coffee,” the effect of the wholesale price increase for franchisees implemented last September will contribute to the full year.

At the same time, it announced a new medium-term management plan, under which it targets consolidated group operating profit of 13.0 billion yen in FY02/2031, the final year. The total number of domestic and overseas stores is planned to expand to 1,400, with overseas stores increasing from 82 at the end of the previous fiscal year to 180, and a target of 1.0 billion yen in business profit.

Investor’s View

Sell on Strength: Even as profit margins decline, the asset efficiency and cash-collection capability of the FC headquarters model support capital profitability, but the problem lies in the capital structure being overly conservative.

First, the growth expectations priced into the share price are not excessively high. Back-solving from a forecast PER of 20.9x, an actual PBR of 2.85x, a forecast ROE of 13.1%, forecast EPS of 138.4 yen, and a forecast dividend of 60 yen, the EPS growth rate priced into the share price is in the low 7% range. By contrast, actual EPS rose from 77.89 yen in FY02/2021 to 141.98 yen in FY02/2026, implying a five-year CAGR of approximately 12.8%. In other words, the market is not pricing in the high growth seen over the past five years, but it still expects stable mid-level growth.

The fair value share price is approximately 2,220 yen under the PBR method, approximately 2,700 yen under the DCF method, and approximately 3,200 yen under the ROIC method. The assumptions are as follows: under the PBR method, ROE of 13.1%, cost of equity of 8.5%, and a long-term growth rate of 4.0%; under the DCF method, free cash flow of 7,580 million yen in FY02/2026 as the starting point, 4.5% growth for five years, a terminal growth rate of 2.0%, and a discount rate of 9.0%; and under the ROIC method, ROIC of 11.8%, WACC of 6.5%, and a long-term growth rate of 3.0%. The median is approximately 2,700 yen, and the range is approximately 2,220–3,200 yen. This does not deny that it is a high-quality company, but the share price is already pricing in a fairly bright future.

Why, then, have GPM and the EBIT margin been declining for more than ten years? This is due less to a weakening of the business than to the company’s susceptibility to the impact of rising raw material costs because of its wholesale model for franchisees, its step-by-step implementation of price pass-through with an emphasis on maintaining franchisee profitability, and, in addition, changes in the earnings mix accompanying expansion into overseas markets and new business formats. The company’s materials also make it clear that rising raw material costs, particularly higher coffee bean prices, are the main factor pressuring profitability. Revenue is growing, but profitability gains are not keeping pace.

Even so, the reason ROE has been maintained at just under 15% and the ROIC-WACC spread has also remained healthy is that the FC headquarters model has high asset efficiency. The annual securities report also explains that, because of the high FC ratio, the headquarters bears a low capital expenditure burden and has strong cash-generating capability. In fact, in the final year of VALUES 2025, ROIC was 11.8%, and the reference value for WACC was 6.5%, meaning the spread, which is the source of value creation, remains substantial. Even as profitability is gradually eroded, capital profitability is less likely to collapse because the structure under which the headquarters earns through wholesale and royalties, using franchisee investment as leverage, is being maintained. This is the company’s essential strength, which cannot be found in foodservice companies centred on directly operated stores.

The reason operating cash flow does not decline even though the gross profit margin continues to fall is the same. The FC headquarters bears a relatively light inventory and fixed-asset burden, and if existing-store sales remain stable, cash collection is unlikely to deteriorate. Operating cash flow in FY02/2026 increased YoY to 12,353 million yen, and free cash flow also came to 7,580 million yen. In other words, even if a decline in profitability is visible on the P/L, cash flow remains very strong. This is the key point from an investor’s perspective: even if the gross profit margin declines, the company is still able to leave enough cash each year to continue shareholder returns and growth investments simultaneously.

That said, from the perspective of equity investment, a rise in the equity ratio is not an unqualified positive. The company steadily maintains a healthy ROIC-WACC spread, has strong operating cash flow, and, because of its FC headquarters model, does not face excessive business risk. That being the case, the current situation, in which the equity ratio has risen to the mid-40% range, should be viewed less as an improvement in financial soundness than as an unnecessary reduction in leverage. Under VALUES 2025, the target was an equity ratio of 40% or more, whereas the FY02/2026 result rose to 45.2%. This is also an accumulation of a safety buffer, but from the shareholder’s perspective, it means that capital that should otherwise be available for higher returns, additional share buybacks, M&A, or more aggressive growth investments remains within the company. While it is fair to acknowledge that ROE remains high, the company’s capital policy is still conservative, and this is a clear area for improvement.

Shareholder returns are clearly positive. The annual dividend for FY02/2026 was 60 yen, and the forecast for FY02/2027 is 62 yen. Under the previous medium-term management plan, the cumulative total shareholder return ratio reached 50.9%, achieving the target. Under the new medium-term management plan, the company is also targeting a cumulative total shareholder return ratio of 50% or more through FY02/2031. It has also carried out share buybacks in the past, and its shareholder return stance, which does not depend solely on dividends, deserves recognition. That said, what remains insufficient at the company is not so much the shareholder return policy itself as the need to optimise the capital structure somewhat more in favour of shareholders.

As for Ownership, the presence of stable shareholders can support supply and demand, but it is less likely to become a strong catalyst for improving capital efficiency. A shareholder structure in which global asset managers and passive funds rank among the top holders contributes to liquidity and valuation stability, but at the same time makes it less likely that strong pressure will be brought to bear against declining profitability and a conservative capital policy. For the share price to move up another stage, it will be necessary not only to accumulate earnings but also for management to adopt a more aggressive capital policy.

The share price trend over the past five years is also consistent with this view. The share price has risen over the medium to long-term, supported by the post-COVID recovery in earnings, the normalisation of existing-store sales, store expansion, improved ROIC, and stronger shareholder returns. On the other hand, over the past two to three years, the pace of share price appreciation has been muted even as earnings have grown. The reason is clear: although revenue and EPS have increased, GPM and the EBIT margin have continued to decline, and investors have entered a phase in which they place greater emphasis on improvements in profitability and capital policy than on volume growth. When the share price remains uninspiring despite strong earnings, it is not because growth is insufficient, but because deterioration in earnings conversion efficiency and the conservatism of accumulating an already sufficiently high equity ratio are further capping the upside from re-rating.

Overall, Komeda Holdings is a high-quality FC headquarters company that can maintain ROE, ROIC, operating cash flow, and dividends even as profitability declines. Through its FC headquarters-type earnings structure, the company has maintained high capital profitability and stable cash generation even as profit margins have gradually declined. That is a clear strength of the company. That said, from the perspective of equity investment, its capital structure remains overly conservative in pursuit of stability, leaving something to be desired when it comes to maximising shareholder value. The current share price has already placed a considerable valuation on stable growth, strong cash generation, and steady shareholder returns, and to justify a further leg up from here, continued store openings alone will not be enough; a bottoming out in the gross profit margin and profitability, or a more decisive move in capital policy, will be required.

Financials and Valuations

Price

PBR (LTM)

PER (LTM)

ROE (LTM)

EPS (Actual)

BPS (LTM)