2026-07-15

Home

Japanese

Omega Investment Co., Ltd.

Cosmo Bio (Company note – basic)

| Share price (4/9) | ¥1,272 | Dividend Yield (12/26 CE) | 3.9 % |

| 52weeks high/low | ¥1,486/971 | ROE(12/25) | 3.7 % |

| Avg Vol (3 month) | 10.2 thou shrs | Operating margin (12/25) | 3.2 % |

| Market Cap | ¥7.69 bn | Beta (5Y Monthly) | 0.17 |

| Enterprise Value | ¥4.29 bn | Shares Outstanding | 6.048 mn shrs |

| PER (12/26 CE) | 32.8 X | Listed market | TSE Standard |

| PBR (12/25 act) | 0.77 X |

| Click here for the PDF version of this page |

| PDF version |

Medium-term Management Plan 2028 launched. To reach an ROE of 8%, expectations are placed on the accumulation of results.

Summary

◇Cosmo Bio is a trading company specializing in the life sciences that upholds the objective of “contributing to the advancement of life sciences.” Founded in 1983 as a subsidiary of the former Maruzen Oil, it became an independent specialized trading company through an MBO. Approximately 80% of net sales are research reagents used at research facilities of pharmaceutical companies, universities, and research institutions. The company’s strengths are its high-quality customer base, its extensive procurement network that provides up to 10 million products and services from approximately 500 suppliers, including overseas suppliers, and its highly specialized personnel and their sales capabilities. In recent years, in addition to its purchasing and sales business, the company has been promoting measures to expand the intermediation of contract services, the sale of its own products, and the provision of its own contract services in Japan and overseas.

◇ Stable growth in the domestic research reagent market and business issues: The domestic market for life science research reagents is estimated at approximately 120 billion yen and has been growing steadily at an annual rate of about 1%. The company holds an approximately 5% share, competing with Japanese subsidiaries of foreign-affiliated reagent manufacturers, subsidiaries of major domestic chemical manufacturers, and independent trading companies.

However, it has issues such as the risk of stagnation in the growth rate of the market, commercial rights risk (for example, the risk of losing commercial rights due to the reorganization of reagent suppliers through M&A), and foreign exchange risk (a time lag occurs before changes in yen-denominated purchase costs can be passed on to selling prices, with profit and loss tending to benefit in phases of yen appreciation and to be adversely affected in phases of yen depreciation).

◇ Long-term vision “Co-creating value for the next generation through the power of life sciences” and five priority strategies: Based on this recognition of issues as well, the company newly established its long-term vision as “Co-creating value for the next generation through the power of life sciences,” and while carrying forward the measures it has promoted to date, reorganized them into five strategies. Specifically, these are portfolio transformation, evolution, and strengthening of marketing functions; full-scale development of new businesses; strengthening of global sales; and optimization and strengthening of business operations. Through these initiatives, the company aims to achieve an ROE of 8% or more, reduce the cost of capital, and reach a PBR of 1x or more.

◇ Medium-term Management Plan 2028: The Medium-term Management Plan 2028, which follows the Medium-term Management Plan 2025 that ended in FY12/2025, was announced. The company aims to monetize the five priority strategies above and achieve net sales of 13.0-14.5 billion yen and an ROE of 5%-8% in FY12/2028.

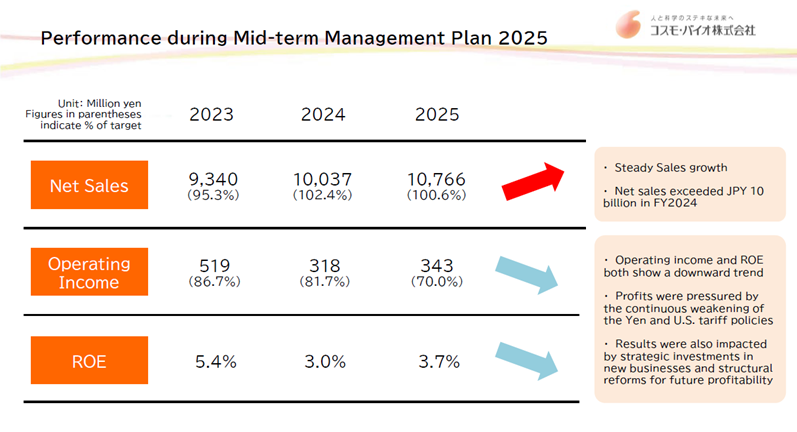

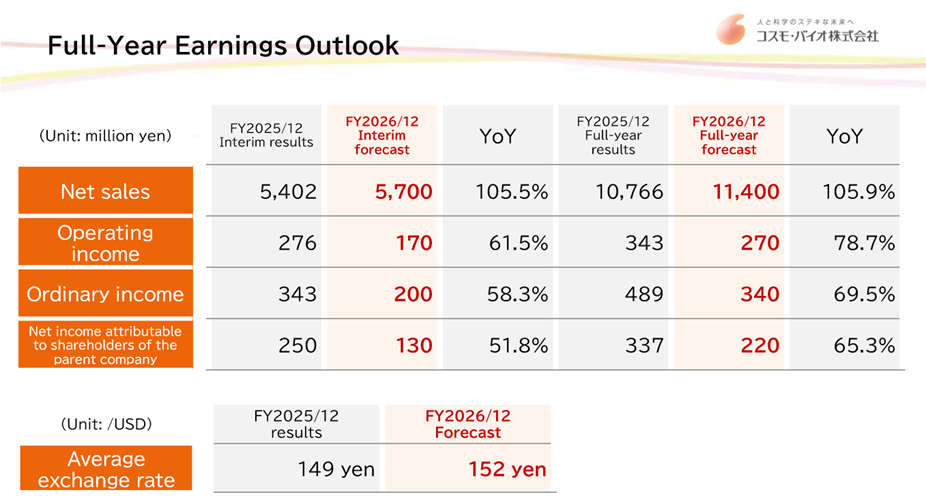

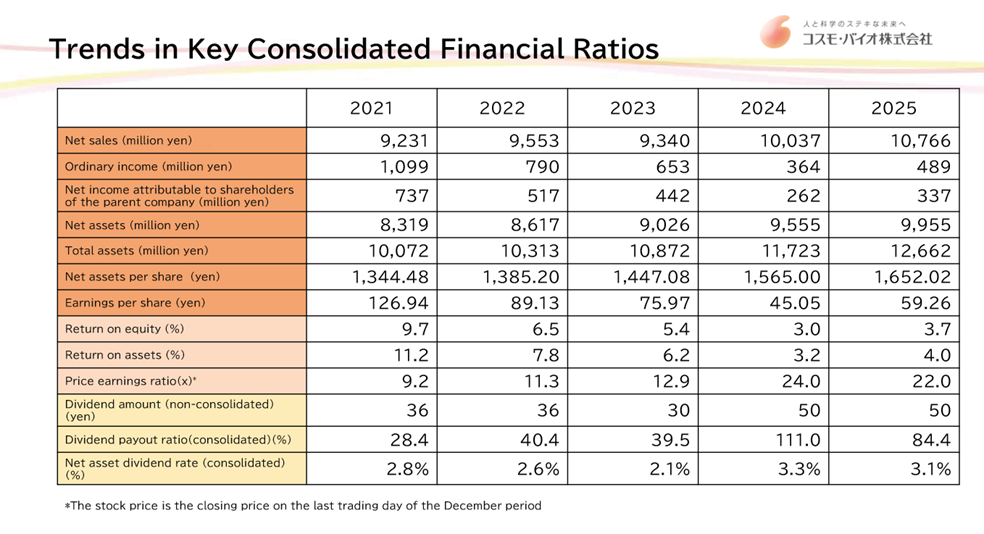

◇ FY12/2025 results: Net sales were 10.76 billion yen (up 7.3% YoY), operating profit was 343 million yen (up 7.7% YoY), and net income attributable to owners of the parent was 337 million yen (up 28.6% YoY). Net sales exceeded 10 billion yen for the second consecutive fiscal year and achieved the plan. On the profit and loss side, although the gross profit margin improved while the USD/JPY exchange rate was unchanged YoY at 149 yen/USD, SG&A expenses increased due to human capital investment, the promotion of DX, office expansion, and other factors, and operating profit increased but fell short of the plan. Tariff effects also arose.

◇ FY12/2026 company forecast: Net sales are 11.40 billion yen (up 5.9% YoY), operating profit is 270 million yen (down 21.3% YoY), net income attributable to owners of the parent is 220 million yen (down 34.7% YoY), and the assumed exchange rate is 152 yen/USD. In addition to the assumption of yen depreciation, the forecast calls for an increase in revenue but a decrease in profit, driven by higher expenses from a larger headcount, stronger sales activity, and the reinforcement of internal management systems. Annual dividends per share are forecast at 50 yen, the same amount as in the previous fiscal year.

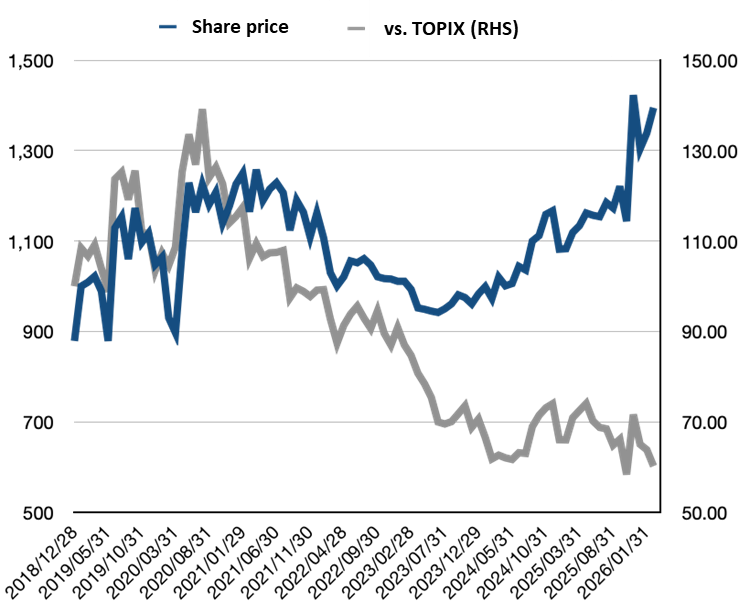

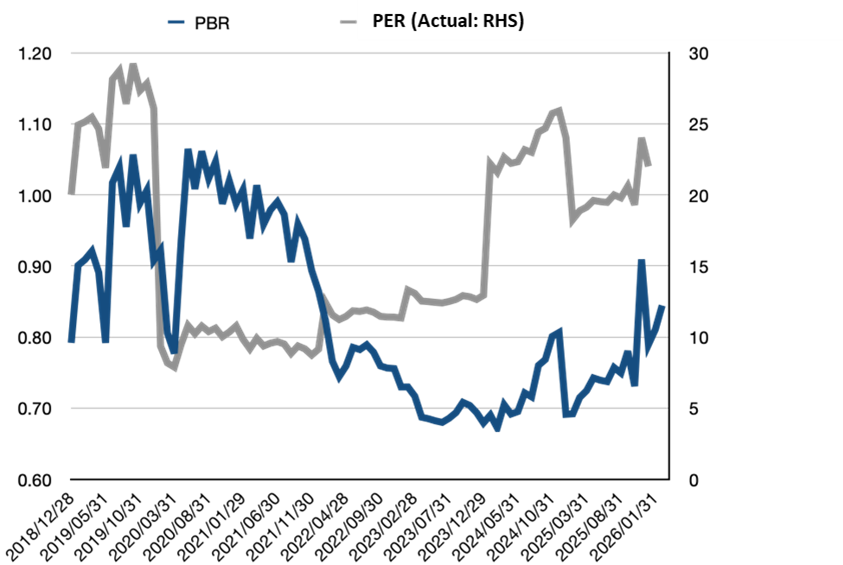

◇ Stock price trend: The stock price has continued on an upward trend since 2024. Recently, the announcement on November 13, 2025, titled “Successful development and manufacturing of the sweet protein ‘brazzein’ using the chicken egg bioreactor,” caused the stock price to surge from 1,100 yen to 1,400 yen. Since then, it has remained generally firm while also absorbing these financial results. The stock market is evaluating factors such as the trend of revenue growth, a profitable business structure, sound finances, low PBR, a dividend yield in the upper 3% range, and the commitment to achieving ROE of 8% and PBR of 1x, and the stock is in a phase where it reacts sensitively to positive developments. It is necessary to continue closely monitoring foreign exchange trends, but if the effects of the various initiatives begin to contribute to profit, a development in which PBR is aimed at 1x in earnest is likely to emerge.

Table of contents

| Summary | 1 |

| Key financial data | 2 |

| Company profile | 3 |

| History/Breakdown of most recent sales/Company’s group | 3 |

| Business overview | 5 |

| Japanese research reagent market/products and services | 5 |

| Corporate uniqueness, strengths/Business issues (risk factors) | 9 |

| Earnings trend | 9 |

| Announcement of the “Long-term Vision” and “Medium-term Management Plan 2028” | 12 |

| Financial results | 21 |

| Full-year results for FY12/2025 | 21 |

| FY12/2026 full-year forecast | 22 |

| Share price trends and catalysts | 23 |

| Financial data | 25 |

| Corporate data | 27 |

| Corporate profile/history | 27 |

| The top management/Corporate governance | 28 |

| Major shareholders/Shareholding by ownership | 29 |

Key financial data

|

2020/12 |

2021/12 |

2022/12 |

2023/12 |

2024/12 |

2025/12 |

2026/12 |

|

| [Statements of income] | Company forecast |

||||||

| Net sales | 8,092 | 9,231 | 9,553 | 9,340 | 10,037 | 10,766 | 11,400 |

| Cost of sales | 4,940 | 5,572 | 6,112 | 6,090 | 6,708 | 7,064 | |

| Gross profit | 3,152 | 3,658 | 3,440 | 3,249 | 3,329 | 3,702 | |

| SG&A expenses | 2,399 | 2,609 | 2,624 | 2,729 | 3,010 | 3,359 | |

| Operating income | 752 | 1,048 | 816 | 519 | 318 | 343 | 270 |

| Ordinary income | 817 | 1,099 | 790 | 653 | 364 | 489 | 340 |

| Net profit before taxes | 1,008 | 1,099 | 790 | 653 | 369 | 504 | |

| Net profit attributable to owners of the parent | 674 | 737 | 517 | 442 | 262 | 337 | 220 |

| [Balance Sheets] | |||||||

| Current assets | 6,756 | 7,310 | 7,136 | 7,102 | 7,229 | 7,441 | |

| Cash equivalents and short-term securities | 3,259 | 3,555 | 3,036 | 3,025 | 2,393 | 2,946 | |

| Non-current assets | 2,883 | 2,761 | 3,176 | 3,770 | 4,493 | 5,220 | |

| Total assets | 9,640 | 10,072 | 10,313 | 10,872 | 11,723 | 12,662 | |

| Total liabilities | 1,779 | 1,752 | 1,695 | 1,846 | 2,167 | 2,706 | |

| Total net assets | 7,861 | 8,319 | 8,617 | 9,026 | 9,555 | 9,955 | |

| Equity ratio (%) | 76.3% | 77.3% | 78.1% | 77.7% | 76.5% | 74.0% | |

| [Statements of cash flows] | |||||||

| Cash flow from operating activities | 803 | 648 | 284 | 736 | 241 | 595 | |

| Cash flow from investing activities | 42 | -145 | -291 | -758 | -217 | 43 | |

| Cash flow from financing activities | -97 | -420 | -236 | -201 | -479 | -283 | |

| Increase/decrease in cash and cash equivalents | 743 | 95 | -218 | -210 | -433 | -1 |

Source: Omega Investment from company materials

Company profile

Cosmo Bio is a trading company specialising in the life-science field, focusing on reagents*, with the Group’s objective of “Contribute to the advancement of life sciences”. Its main business is purchasing and wholesale research reagents, equipment, contract services and clinical reagents related to life sciences. Reagents’ market size is different from those of diagnostics and therapeutics. Still, they are essential products and services indispensable for life science researchers worldwide to develop new drugs.

History

The company’s history can be traced back to 1983 when it was founded as Maruzen Oil Biochemical Co., Ltd as a subsidiary of the former Maruzen Oil (now Cosmo Oil) for basic biotechnology research reagent business. The company subsequently renamed itself to Cosmo Bio Co., Ltd. (1985) following a merger and restructuring of the parent company. In the same year, the company began selling equipment for bio-research. In September 2000, the company became independent frThe company’s history can be traced back to 1983 when it was founded as Maruzen Oil Biochemical Co., Ltd as a subsidiary of the former Maruzen Oil (now Cosmo Oil) for basic biotechnology research reagent business. The company subsequently renamed itself to Cosmo Bio Co., Ltd. (1985) following a merger and restructuring of the parent company. In the same year, the Company began selling equipment for bio-research. In September 2000, the Company became independent from Cosmo Oil through an MBO. In August 2004, it established Cosmo Bio USA, Inc. in San Diego, California, one of the world’s leading bioresearch centers and the location of many bio-ventures. It was made a base to search for reagents and promote the export of Japanese-made reagents (became a consolidated subsidiary in January 2018) . In September 2005, the Company was listed on the JASDAQ market. Subsequently, the Company expanded its operations by investing in and merging with companies in related fields. In December 2006, Primary Cell Co., Ltd. became a subsidiary, and Cosmo Bio entered the manufacturing business. In March 2010, BM Equipment Co., Ltd. was consolidated as a trading subsidiary that imports equipment and consumables for life science research. In October 2017, the Company relocated and consolidated its Sapporo business facilities and opened the Sapporo Office, establishing a structure to reinforce its recent focus on contract services and manufacturing and sales. (See also the Alignment Chart on p. 27)

Breakdown of most recent sales

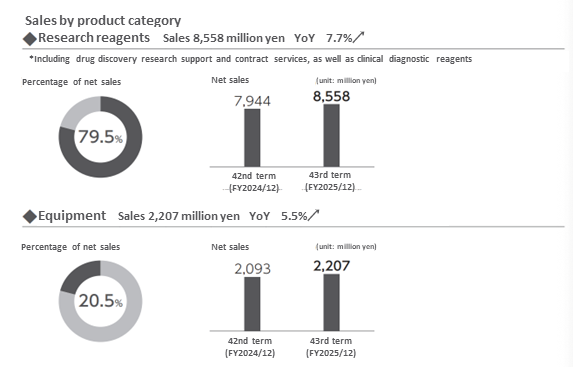

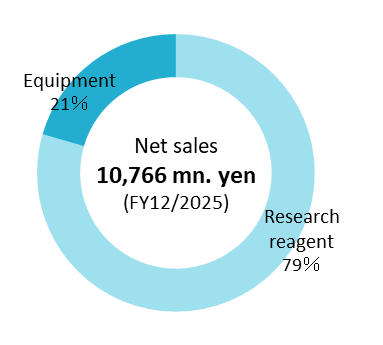

Research reagents and Equipment for 79.5% and 20.5% of the Company’s FY12/2025 sales of 10,766 million yen, respectively.

Breakdown of sales by product

*Reagents: according to the Japan Reagents Association, reagents are legally defined as ‘chemical substances used for the detection or quantification of substances by chemical methods, experiments in the synthesis of substances or for physical properties’.

The general concept is also defined as “chemicals used for measurement standards, detection and confirmation of substances, quantification, separation and purification, synthesis experiments and measurement of physical properties in testing and research cases, such as inspection, testing, research and experiments, in the form of supply suitable for small quantities with guaranteed quality for the respective purpose of use”. More specifically, they are agents used for experiments, research, and measurements and include chemical substances, components extracted from the body of a living organism (proteins, cells, nucleic acids, etc.), and solvents used to react with them. Reagents for life science are mainly extracted from living organisms or synthesised from such substances and are supplied in small quantities, such as several tens of micrograms.

On the other hand, diagnostic reagents are drugs doctors use in various tests to diagnose health or disease conditions. They are also known as in vitro diagnostic drugs or clinical diagnostic reagents and are distinguished from reagents.

Generally, we take therapeutic drugs (ethical drugs) to cure diseases. They are administered to treat various diseases and are researched, developed, manufactured, and marketed by major national and international pharmaceutical companies.

The domestic market for life science research reagents is around 120 billion yen (2021, company data), the market size for diagnostics is about 800 billion yen (2021, Japan Association of Clinical Reagents Industries), and the market for therapeutic drugs (ethical drugs) is approximately 9.4 trillion (2021, IQVIA) being by far the largest.

Company’s group

The company’s group comprises Cosmo Bio (the company), two consolidated subsidiaries: BM Equipment and Cosmo Bio USA, Inc., and the non-consolidated subsidiary Proteintech Japan Co., Ltd. For their respective businesses and product flows, see the diagram below. BM Equipment and Proteintech Japan are located on the same floor in the head office in Koto-ku, Tokyo, where Cosmo Bio is based, to facilitate communication as a group.

Overview of the company’s group and product flow

Source: Company materials

In addition to Koto-ku, Tokyo, mentioned above, where the company’s head office is located, the company’s other operating bases include the Sapporo Office and the Shinsuna Logistics Centre. As mentioned in history, the Sapporo Office (Otaru, Hokkaido) was established in October 2017 by relocating and consolidating the company’s Sapporo area business facilities. The facility is responsible for contract services and manufacturing and sales, which are the company’s growth areas of focus.

The Shinsuna Distribution Centre was opened in January 2013. The company runs a system to hold an inventory of hot-selling products (the Group’s products and inventory on its BS at end-December 2023 amounted to about 1 billion yen) and ship them. The company can respond precisely to the needs of pharmaceutical companies, universities, and research institutions, which often require prompt deliveries.

Source: Company materials, etc.

Business overview

Provides essential reagents and equipment for life science researchers worldwide

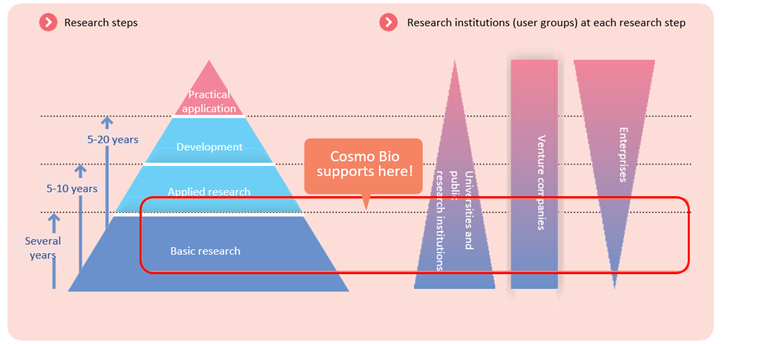

The company provides life science researchers worldwide with research reagents that are integral to the basic research process. The development of pharmaceuticals usually takes a long period, over ten years, involving basic research, applied research, development and clinical trials. In recent years, the development of antibody drugs and the linkage with IT, such as in silico (including the application of quantum computers to accelerate the process), are expected. Still, steady research activities in the research field are necessary.

The reagents and equipment provided by the company are essential items in basic research at pharmaceutical companies, universities, and research institutions, and demand is expected to grow steadily to ensure a stable and constant profit margin.

Life science research and User demographic

Source: Company materials

Japanese life science research reagents market

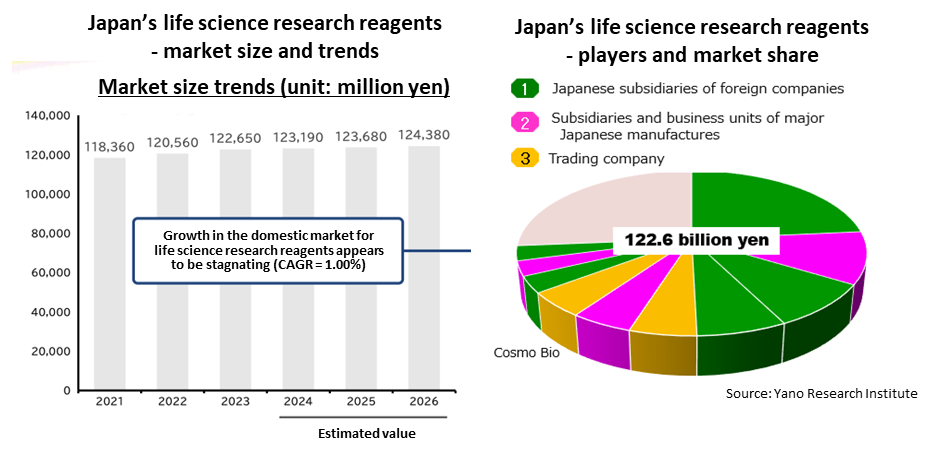

The domestic market for life science research reagents has grown steadily at an average annual rate of about 1% to date, and its market size is estimated at approximately 120 billion yen.

The market shares by operators are shown in the chart on the right below. Japanese subsidiaries of reagent companies in North America and elsewhere and group companies or business units of major Japanese chemical manufacturers account for a certain share. Two independent specialist trading companies, including the Company, are also in the Top 10, and their share is estimated to be around 5%. Although competition between the companies is intense, each has its own areas of specialisation, and they can secure a certain level of sales and profits.

Source: Omega Investment from company materials

Next, we examine the situation on the user side of reagents. As already stated, customers for reagents are research facilities in the life sciences field, such as pharmaceutical companies, universities, and research institutions.

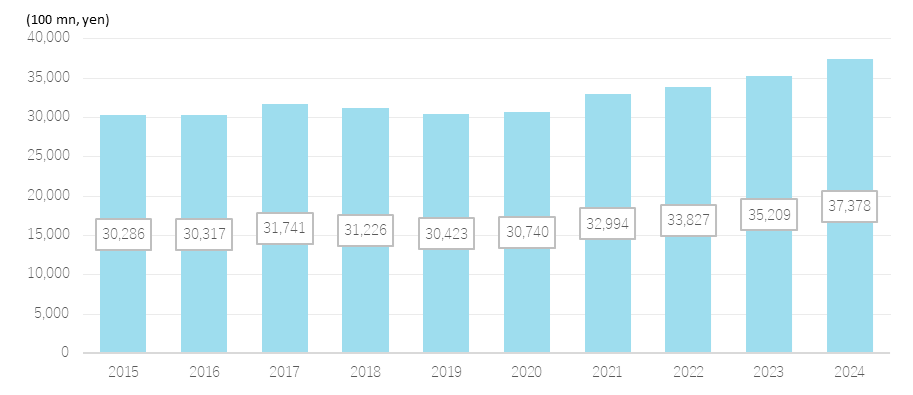

First, according to the Ministry of Internal Affairs and Communications’ “2025 Science and Technology Research Survey,” trends in life sciences research expenditures are as follows. In FY2024, such expenditures were 3.7 trillion yen and have been increasing steadily. This is expected to support the growth of the market for life science research reagents.

Trends in research expenditures for life sciences

Source: Prepared by Omega Investment based on Overview of the Results of the 2025 Science and Technology Research Survey, Ministry of Internal Affairs and Communications

Next, trends in Grants-in-Aid for Scientific Research at Japanese universities and educational institutions are as follows. It should be noted that growth has recently been somewhat sluggish and that there are phases in which rising utility costs put pressure on research site budgets, but the underlying trend remains firm.

Accordingly, the market for life science research reagents is experiencing stable growth.

Trends in Grants-in-Aid for Scientific Research

Source: Prepared by Omega Investment from the Ministry of Education website and other sources

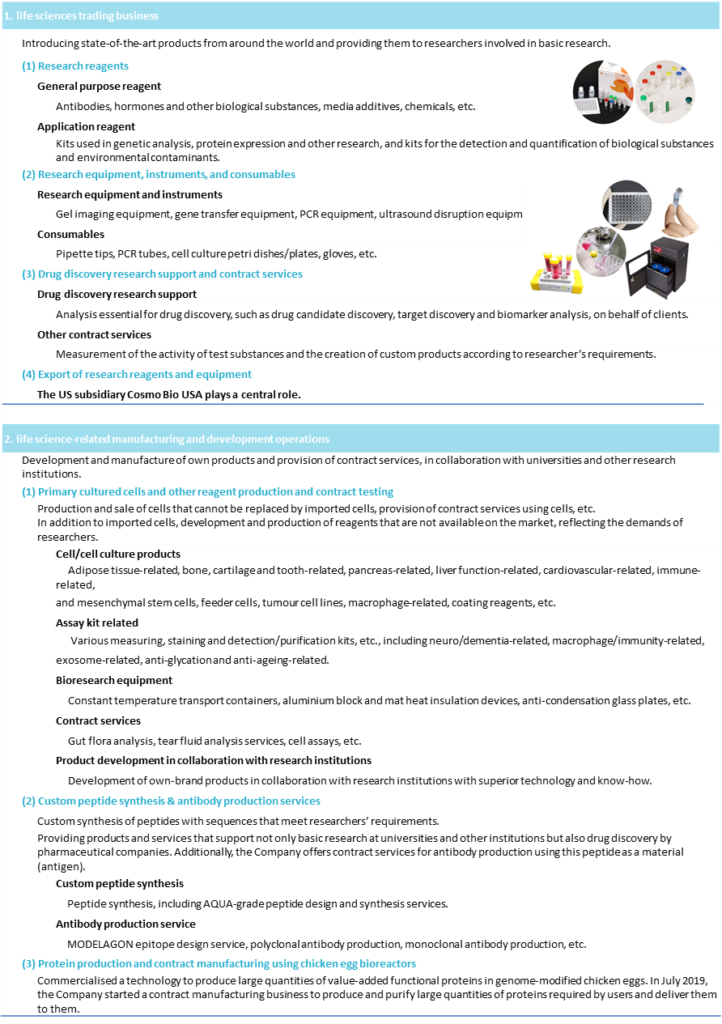

The range of products and services offered by the company

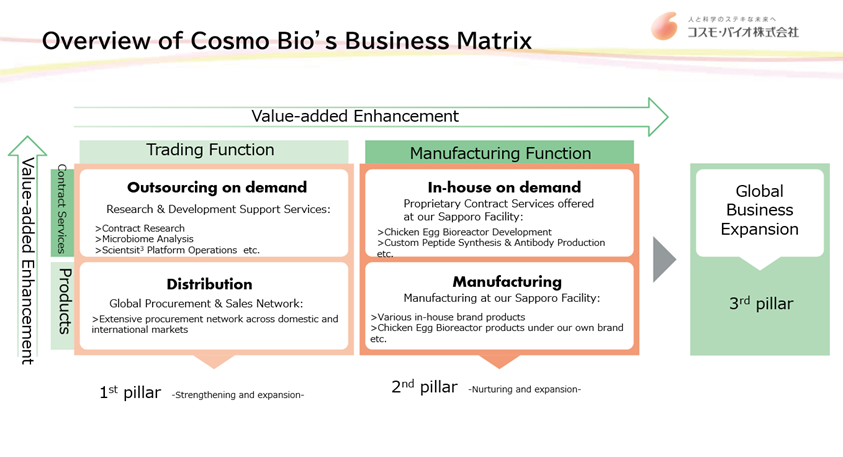

The company introduces as many as 10 million cutting-edge items from more than 500 suppliers worldwide, adds its unique value, and provides them to life science researchers through approximately 200 distributor locations. With the purchasing and sales business of this trading company as its core, it envisions expansion into contract service intermediation, the cultivation and expansion of manufacturing and sales, in-house contract services, and overseas expansion.

Business overview matrix of the company

The company’s business overview can be organized as follows.

Source: Company materials

Corporate uniqueness/strengths

Strong relationships of trust with clients and suppliers: In research and development, where reagents are used, a single reagent is rarely used in large quantities. A variety of reagents in microgram quantities are required at each research level. The company is attentive to diverse needs based on 40 years of building trusting relationships with clients and solid relationships with suppliers of state-of-the-art reagents, mainly in North America.

Providing state-of-the-art information in the life-science field: As a specialist life sciences trading company, in addition to the information-gathering capabilities of its head office, the company, in cooperation with COSMO BIO USA, INC, also exhibits and participates in various bio-related events, providing cutting-edge information in the life sciences sector to anticipate the needs of its clients.

Responding to user needs by manufacturing and developing in-house products: In addition to its principal business as an importer and trading company, it manufactures and sells cells that cannot be replaced by imported cells and provides contract services using cells. To achieve further growth, the company plans to focus on the manufacture and sale of its own products and the provision of contract services.

Accumulation and possession of various know-how related to the reagent business: Products in the life sciences sector, especially those related to reagents, require different knowledge and know-how than the import and export of ordinary products. Many of the products handled by the company need to comply with various laws and administrative guidance, such as the Pharmaceutical and Medical Device Act (Act on Securing Quality, Efficacy and Safety of Products Including Pharmaceuticals and Medical Devices), the Poisonous and Deleterious Substances Control Act and the Narcotics and Psychotropics Control Act. These laws vary from country to country, and knowledge and information on the differences between countries are also important. In addition, some reagents are of animal origin and are subject to animal quarantine. Furthermore, some reagents, such as proteins, nucleic acids, and cells, are of biological origins. Appropriate temperature control is required, such as packing dry ice during international transport procedures. The company has accumulated such know-how and expertise and regards them as one of its strengths.

Business issues (risk factors)

-Risk of deceleration in the growth rate of the domestic market for life science research reagents: Against the backdrop of the maturity of the domestic market, sluggish growth in the researcher population, restraint on increases in public R&D expenditures and “selection and concentration,” and the commoditization of reagents and intensifying price competition, market growth has been tending to stagnate, and there is a risk that this will continue.

-Commercial rights risk: Of the company’s 500 suppliers, approximately 400 are overseas (mainly in North America), and there is a risk that management rights of these suppliers could be transferred through M&A, potentially resulting in the company losing its commercial rights in Japan. Situations may also arise in which overseas suppliers build their own sales networks in Japan or switch to competing companies.

–Commercial rights risk: Of the Company’s more than 500 suppliers, 400 are overseas, mainly in North America. If the management rights of these companies were to change hands through M&A, the Company could lose its commercial rights in Japan. Overseas suppliers could also independently build up their own sales networks in Japan or switch to competing companies.

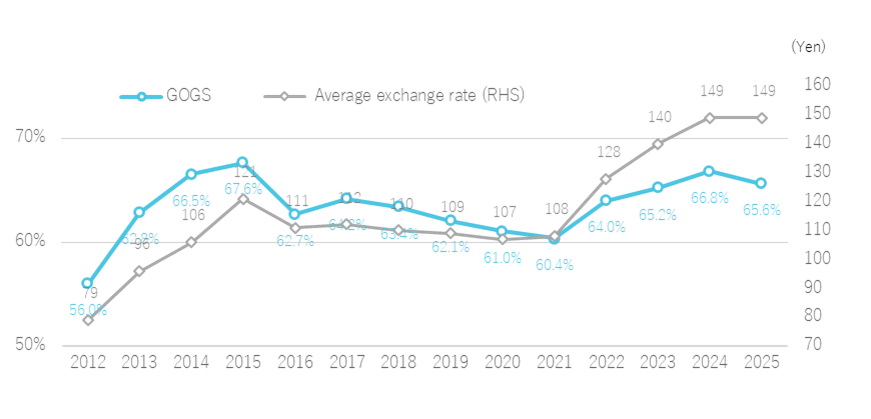

–Exchange rate risk: Approximately two-thirds of the Company’s purchases are in US dollars, so the cost of sales rises and falls with exchange rate fluctuations. Two-thirds of the Company’s purchases are in US dollars. Based on internal policy, the Company makes forward exchange contracts within a certain range of actual demand. Still, when the yen suddenly weakens, the cost of sales rises sharply as the price increase is delayed, which significantly impacts business performance. (See the figure below)

–Competitive risk: There is also intense competition within the industry in the domestic market.

–Regulatory risk: Some of the Company’s products require compliance with various laws and regulations. An accident or other event could result in a violation of the law, and if these laws and regulations are revised, new measures will be required. Recent changes in tariff policies are also a risk factor.

The Yen-dollar exchange rate and COGS ratio

Source: Omega Investment from company materials

Earnings trend

The Company’s long-term financial performance is reviewed. Sales have generally risen steadily due to the steady market expansion mentioned earlier and the Company’s precise business development. In terms of profits, the Company has been profitable since its establishment, providing investors with some degree of reassurance.

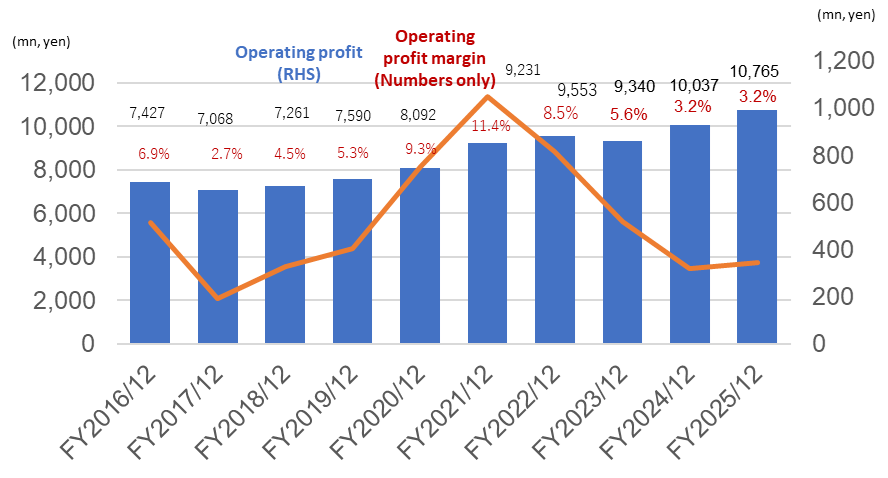

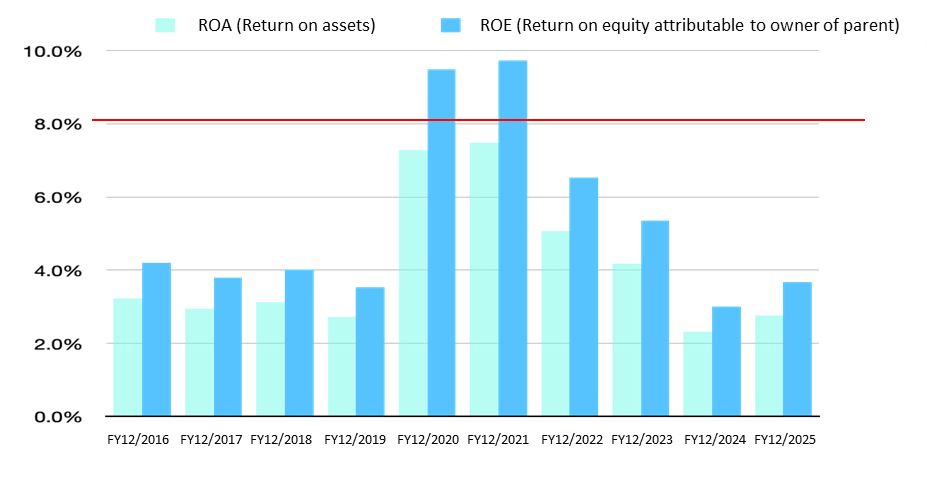

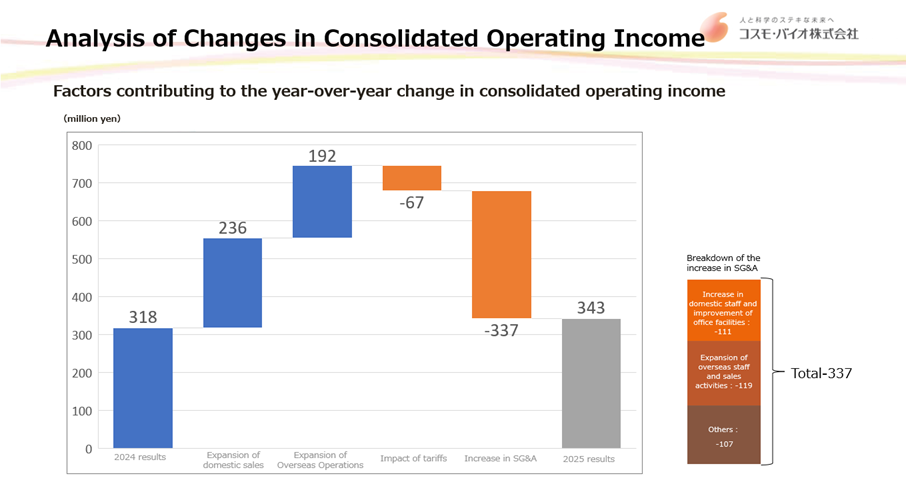

However, as shown in the graph below, operating profit has fluctuated between 200 million yen and 1 billion yen and is not trending upward. Because the company handles many imported products, it has a structure in which depreciation of the yen negatively affects profit and loss, and, more recently, U.S. tariff policy has become a factor putting pressure on gross profit. In addition, human capital, DX, and strategic investments have increased in recent years, and the SG&A ratio has also been rising. As a result, the operating profit margin has fluctuated between 2% and 11% and has recently been trending downward. As a result, ROA and ROE have also fluctuated widely, and in recent years, ROE has failed to meet the 8% target.

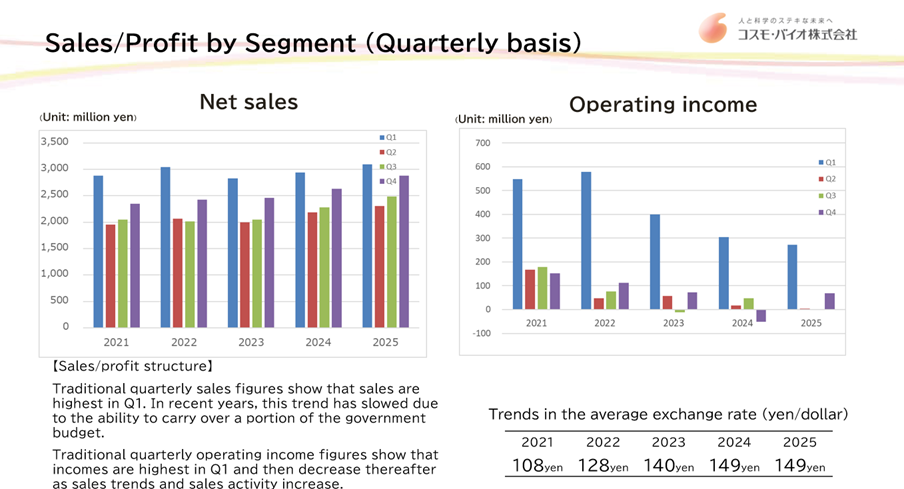

Sales/Profit by Segment

Source: Omega Investment from company materials

Trend in ROA/ROE

Source: Omega Investment from company materials

It should also be noted that, because many of the company’s customers have fiscal year-ends in March, the company’s revenue tends to be weighted toward the January-March period (its first quarter) in both net sales and profit.

Sales/Profit by Segment (Quarterly basis)

Source: Company materials

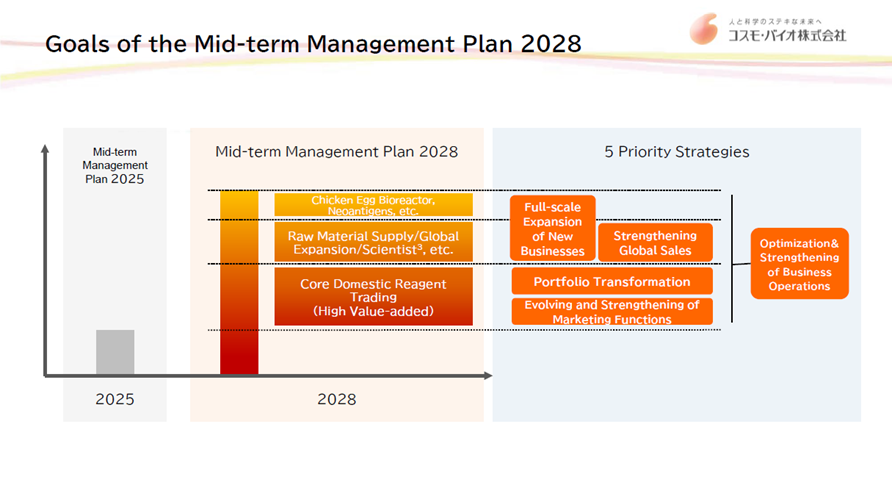

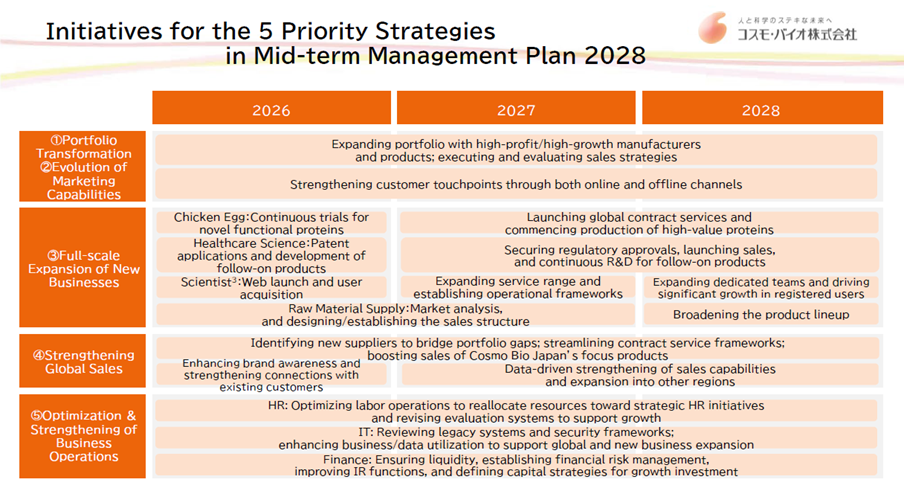

Announcement of the “Long-term Vision” and “Medium-term Management Plan 2028”

The company completed “Medium-term Management Plan 2025” with FY12/2025 and announced its “Long-term Vision” and “Medium-term Management Plan 2028” in February 2026.

Review of “Medium-term Management Plan 2025”

First, we review the progress of “Medium-term Management Plan 2025,” which covers FY2023 through FY2025, and “Measures toward achieving management that is conscious of capital costs and stock price,” announced in August 2024. Put simply, this can be summarized as follows:

- Recognition of the issues and the measures taken was appropriate

- Initiatives achieved steady results on the qualitative side, and net sales also achieved the target

- However, profits were under pressure because yen depreciation and U.S. tariffs had adverse effects, and expenses for new businesses and organizational reinforcement were incurred before the effects of these initiatives began to appear.

- As a result, ROE also declined.

Source: Company materials

“Long-term Vision” and “Medium-term Management Plan 2028”

Next, we review the “Long-term Vision” and “Medium-term Management Plan 2028” presented this time.

Long-term Vision

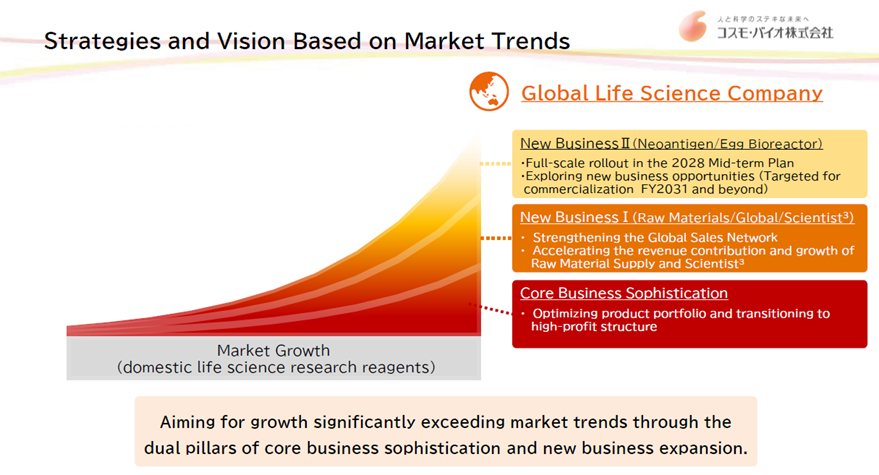

As its “Long-term Vision,” the company newly set forth “Co-creating value for the next generation through the power of life sciences.” It also declared that it will carry forward the various measures of the “Medium-term Management Plan 2025” and aim to transform itself from a “Japanese Distributor” into a “Global Life-Science Company.” This policy strongly reflects awareness of the company’s issues mentioned earlier, particularly the risk of deceleration in the growth rate of the domestic market for life science research reagents and foreign exchange risk.

Source: Company materials

Five priority strategies

Next, five priority strategies for realizing the long-term vision are presented. It can be said that these are a reorganization of conventional strategies, carried forward.

Specifically:

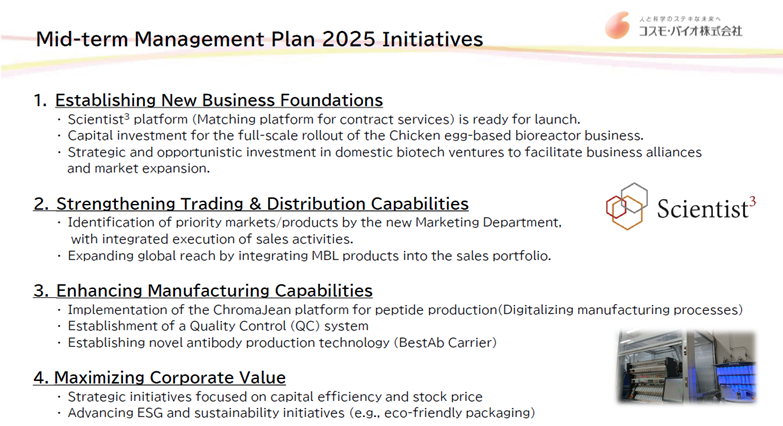

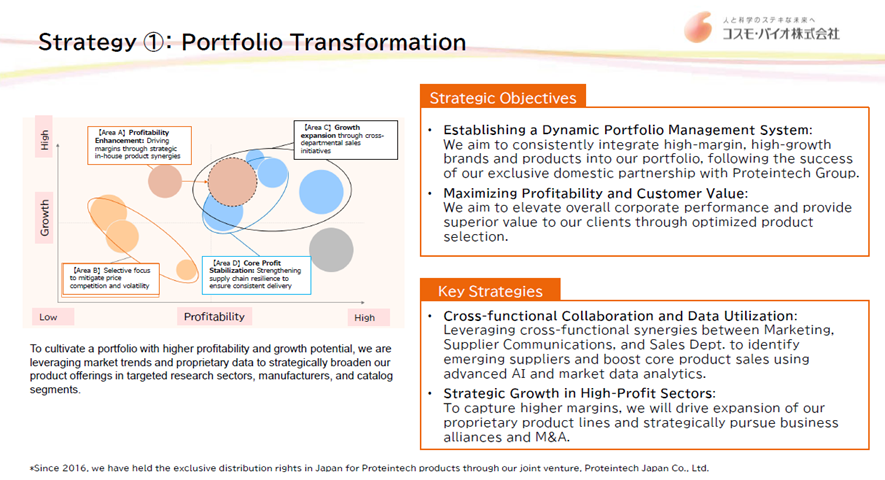

1.Portfolio transformation: continuously discover and supply high-value-added products

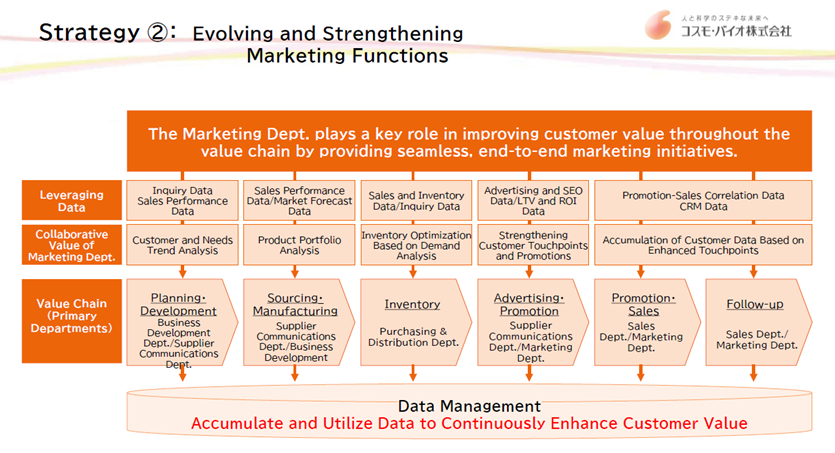

2.Evolution and strengthening of marketing functions: make broad use of data-based marketing by utilizing the Marketing Department established in 2024

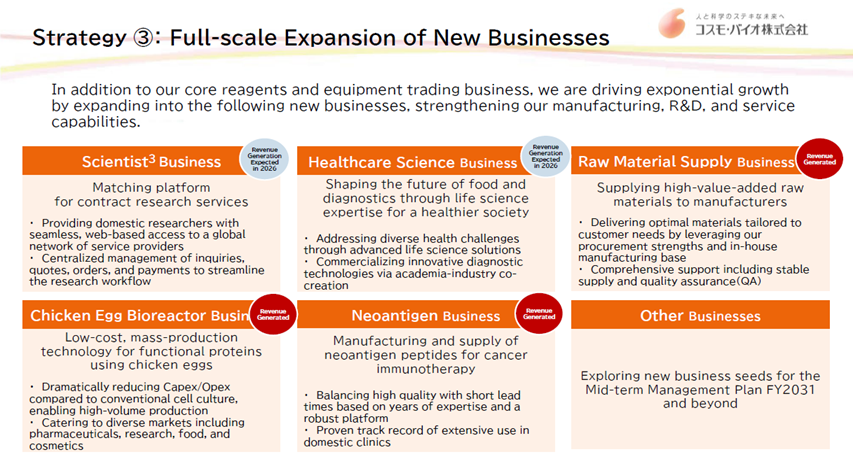

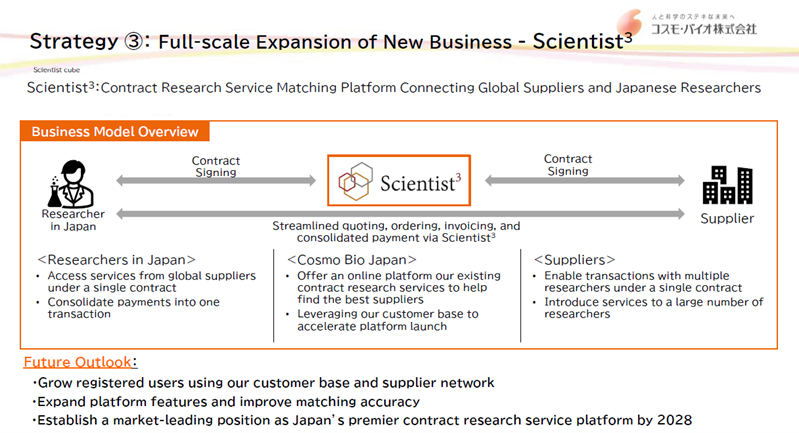

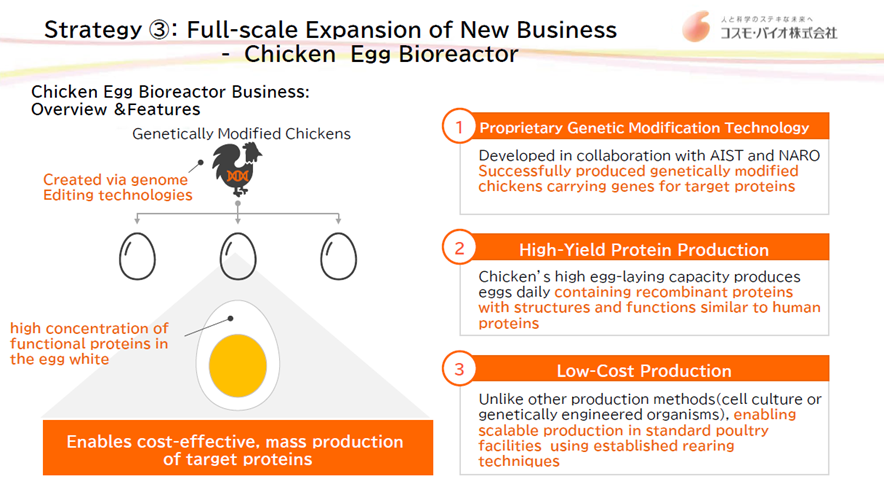

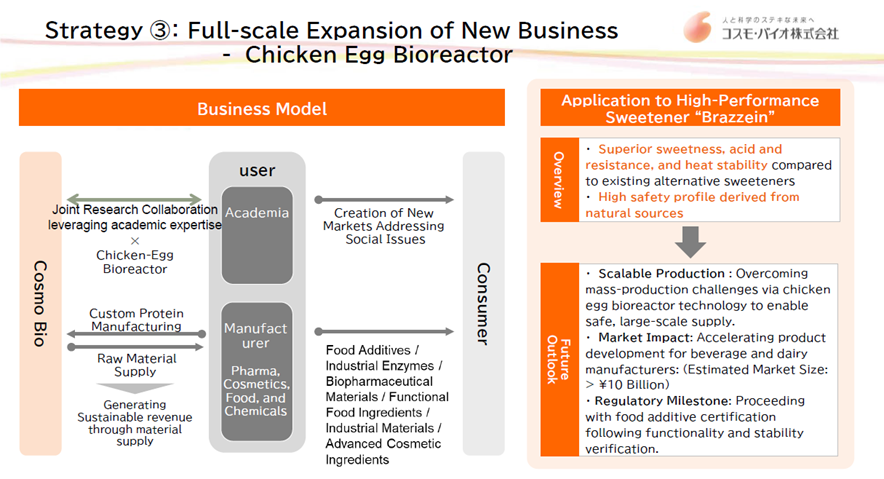

3.Full-scale development of new businesses: accelerate growth through the full-scale development of new businesses such as Scientist3 (a contract service matching platform for researchers), the chicken egg bioreactor (a low-cost, mass-production technology for useful proteins using chicken eggs), and neoantigens (manufacture and supply of neoantigen peptides used in cancer immunotherapy), through the strengthening of manufacturing/development functions and service functions

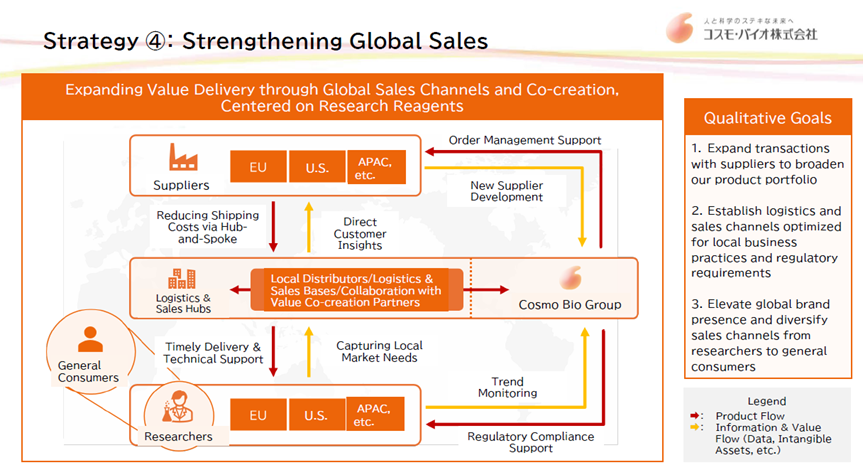

4.Strengthening global sales: seek to transform the current U.S. sales structure for Japanese products into one that conducts global procurement and sales. As a result, this will also reduce foreign exchange risk.

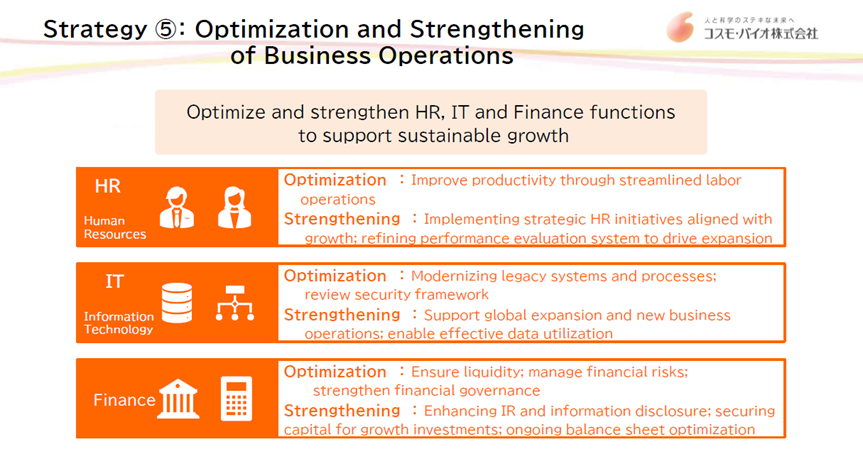

5.Optimization and strengthening of business operations: optimize and strengthen human resources, IT, and finance.

Source: Company materials

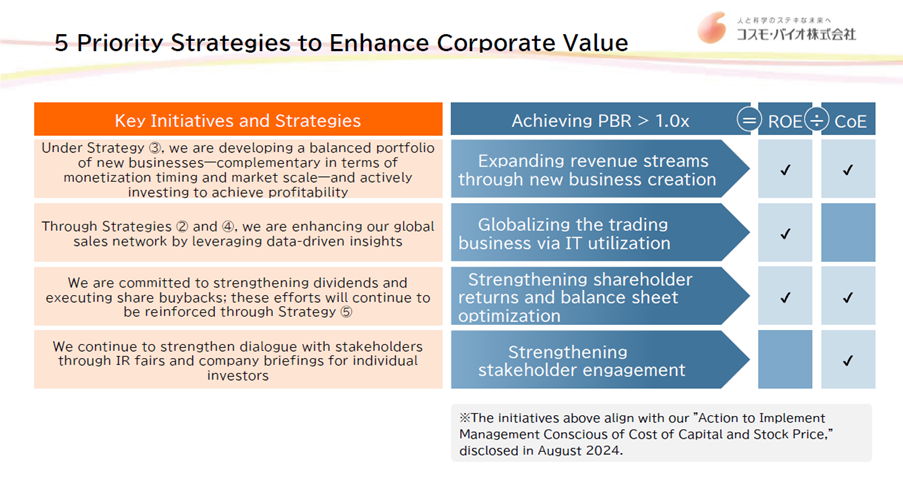

Path toward enhancement of corporate value through the five priority strategies

These five priority strategies are linked to enhancing corporate value and specifically aim to improve ROE (as expected) and achieve a PBR of 1x or higher. The details are as follows. Organizing the concept, from the bottom upward:

- Through the expansion of IR measures, ESG initiatives and their disclosure, governance enhancement and its disclosure, and more proactive PR disclosure, the company will reduce information asymmetry with investors and seek to lower shareholders’ cost of capital

- By promoting Priority Strategy 5 (optimization and strengthening of business operations), strengthening shareholder returns, and avoiding excessive expansion of shareholders’ equity, the company will keep the denominator of ROE at an appropriate level and also control the cost of capital. The dividend policy uses whichever is higher of a dividend on equity ratio (DOE) of 3.5% or a dividend payout ratio of 60% as the benchmark, and since FY2024, the consolidated dividend payout ratio has been at around 100%

- While continuously carrying out Priority Strategy 1 (portfolio transformation), the company will promote the globalization of its trading company business through Priority Strategy 2 (evolution and strengthening of marketing functions) and Priority Strategy 4 (strengthening of global sales), thereby underpinning earnings by becoming more resilient to foreign exchange fluctuations and capturing growth potential in Japan and overseas, and raising the numerator of ROE.

- The company will cultivate Priority Strategy 3 (full-scale development of new businesses) and make concrete the future potential for discontinuous growth. As a result, it will improve the expected future value of ROE and, at the same time, lower the cost of capital as business performance enters a stable growth trajectory.

The company’s policy is to enhance corporate value through these steps.

This way of thinking is, in substance, a continuation of “Measures toward achieving management that is conscious of capital costs and stock price,” announced in August 2024.

Source: Company materials

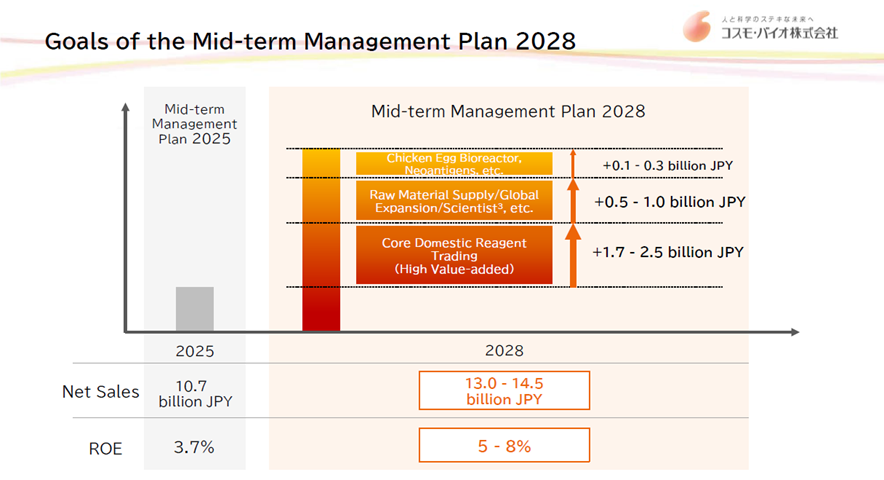

“Medium-term Management Plan 2028”

“Medium-term Management Plan 2028” translates the five priority strategies described above into a three-year plan for 2026 to 2028. In terms of financial figures, the plan is to raise net sales from 10.7 billion yen in FY2025 to 13.0 – 14.5 billion yen in FY2028, and ROE from 3.7% to 5% – 8% in FY2028. The company plans to first steadily achieve revenue growth through Priority Strategies 1, 2, and 5, and then further increase net sales through Priority Strategies 3 and 4.

Source: Company materials

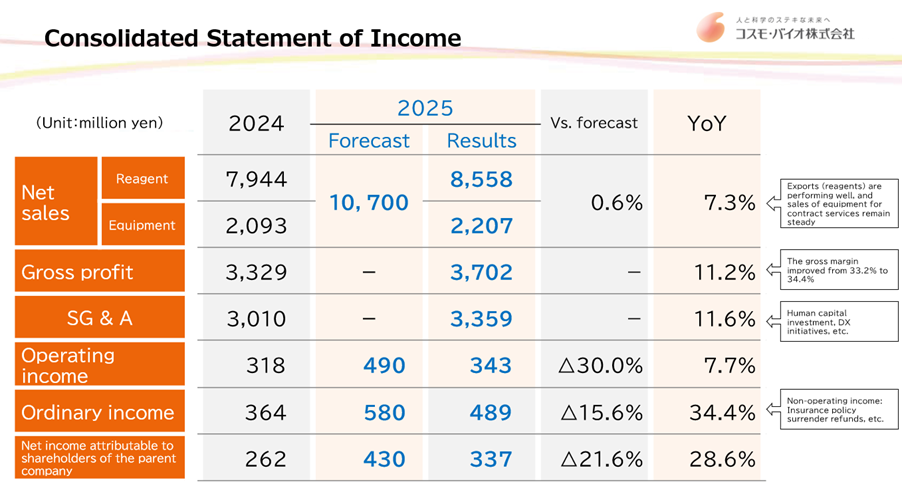

Financial results

1) FY12/2025 financial results: 7.3% increase in revenue, 7.7% increase in operating profit

Net sales were 10.76 billion yen (up 7.3% YoY), operating profit was 343 million yen (up 7.7% YoY), and net income attributable to owners of the parent was 337 million yen (up 28.6% YoY). Net sales exceeded 10 billion yen for the second consecutive fiscal year and achieved the plan. On the other hand, regarding profit, although the USD/JPY exchange rate was unchanged YoY at 149 yen/USD and the depreciation rate improved, SG&A expenses increased due to human capital investment, the promotion of DX, office expansion, and other factors, and although operating profit and other profit measures increased, they fell short of the plan. Tariff effects also arose.

Annual dividends per share were 50 yen (unchanged YoY), and the dividend payout ratio was 84.4%, indicating that the dividend policy focused on ROE continues. As for the balance sheet, the continued high equity ratio (74.0%) indicates no material change in the financial condition.

Source: Company materials

2) FY12/2026 earnings forecast

The company’s earnings forecast for FY12/2026, the first fiscal year of the new medium-term management plan, assumes revenue growth and profit decline. Net sales are 11.40 billion yen (up 5.9% YoY); operating profit is 270 million yen (down 21.3% YoY); net income attributable to owners of the parent is 220 million yen (down 34.7% YoY); and the assumed exchange rate is 152 yen/USD. In addition to the assumption of yen depreciation, the forecast calls for an increase in revenue but a decrease in profit, driven by higher expenses from a larger headcount, stronger sales activity, and the reinforcement of internal management systems. Annual dividends per share are forecast at 50 yen, the same amount as in the previous fiscal year (dividend payout ratio of 129.0%).

Source: Company materials

Share price trends and catalysts

The stock price has continued to trend upward since 2024.

When compared with business performance, it appears that the market recognizes the company remains on a revenue growth trend, and it is difficult to regard the market as becoming more concerned about the holding pattern in profits and ROE. In addition, when the announcement titled “Successful development and manufacturing of the sweet protein ‘brazzein’ using the chicken egg bioreactor” was released on November 13, 2025, the market responded favorably to it, and the stock price surged from 1,100 yen to 1,400 yen. The announcement of FY12/2025 financial results was also absorbed, and although the company’s forecast for FY12/2026 calls for higher revenue and lower profit, the stock price has remained firm.

In light of these developments, it can be said that the stock market:

- is evaluating factors such as the trend of revenue growth, a profitable business structure, sound finances, low PBR, a dividend yield in the upper 3% range, and the commitment to achieving ROE of 8% and PBR of 1x

- has begun to react sensitively to positive developments that will lead to future improvement in ROE

It is necessary to continue closely monitoring foreign exchange trends, but if the various strategies become concrete and their effects begin to contribute to profits, a development in which PBR is aimed at 1x in earnest can be envisaged.

The following points can be summarized as future catalysts that will move the stock price:

- Trends in the USD/JPY exchange rate (with no major yen depreciation)

- Early realization of increased sales and higher added value in the domestic reagent trading company function

- Establishment of a path toward increased global sales and progress in reducing and strengthening the management of foreign exchange risk

- Actual ROE is beginning to rise steadily as a result of these factors

- Full-scale development of new businesses, such as raw material supply, the launch of Scientist3, the chicken egg bioreactor, and neoantigens, leading to stronger expectations for future ROE improvement

- Proactive expansion through M&A and other means by utilizing the sound financial base

Financial data

| Unit: mn, yen | 2016/12 | 2017/12 | 2018/12 | 2019/12 | 2020/12 | 2021/12 | 2022/12 | 2023/12 | 2024/12 | 2025/12 | 2026/12 |

| [Statements of income] | Company forecast |

||||||||||

| Net sales | 7,427 | 7,068 | 7,261 | 7,590 | 8,092 | 9,231 | 9,553 | 9,340 | 10,037 | 10,766 | 11,400 |

| Year-on-year basis | 1.0% | -4.8% | 2.7% | 4.5% | 6.6% | 14.1% | 3.5% | -2.2% | 7.5% | 7.3% | 5.9% |

| Gross profit | 2,772 | 2,532 | 2,659 | 2,879 | 3,152 | 3,658 | 3,440 | 3,249 | 3,329 | 3,702 | |

| SG&A expenses | 2,257 | 2,339 | 2,330 | 2,474 | 2,399 | 2,609 | 2,624 | 2,729 | 3,010 | 3,359 | |

| Operating profit | 514 | 193 | 328 | 405 | 752 | 1,048 | 816 | 519 | 318 | 343 | 270 |

| Year-on-year basis | 157.0% | -62.5% | 69.9% | 23.5% | 85.7% | 39.4% | -22.2% | -36.3% | -38.7% | 7.7% | -21.3% |

| Operating profit margin | 6.9% | 2.7% | 4.5% | 5.3% | 9.3% | 11.4% | 8.5% | 5.6% | 3.2% | 3.2% | 2.4% |

| Non-operating profit | 21 | 208 | 89 | 72 | 71 | 71 | 57 | 136 | 86 | 158 | |

| Non-operating expenses | 51 | 3 | 13 | 7 | 6 | 20 | 83 | 2 | 40 | 12 | |

| Ordinary Profit | 483 | 397 | 403 | 470 | 817 | 1,099 | 790 | 653 | 364 | 489 | 340 |

| Extraordinary profit | 55 | 8 | 190 | 53 | 69 | ||||||

| Extraordinary expenses | 82 | 5 | 81 | 48 | 54 | ||||||

| Income before income taxes | 456 | 400 | 403 | 388 | 1,008 | 1,099 | 790 | 653 | 369 | 504 | |

| Total income taxes | 180 | 148 | 126 | 142 | 307 | 331 | 238 | 191 | 99 | 170 | |

| Net profit | 254 | 237 | 260 | 237 | 674 | 737 | 517 | 442 | 262 | 337 | 220 |

| Year-on-year basis | 10.4% | -6.7% | 9.7% | -8.8% | 184.4% | 9.3% | -29.9% | -14.4% | -30.0% | 28.6% | -34.7% |

| Net profit ratio | 3.4% | 3.4% | 3.6% | 3.1% | 8.3% | 8.0% | 5.4% | 4.7% | 2.6% | 3.1% | 1.9% |

| [Balance Sheets] | |||||||||||

| Current assets | 5,495 | 5,143 | 5,668 | 5,927 | 6,756 | 7,310 | 7,136 | 7,102 | 7,229 | 7,441 | |

| Cash equivalents and short-term securities | 1,948 | 1,483 | 2,268 | 2,516 | 3,259 | 3,555 | 3,036 | 3,025 | 2,393 | 2,946 | |

| Non-current assets | 2,438 | 2,982 | 2,832 | 2,962 | 2,883 | 2,761 | 3,176 | 3,770 | 4,493 | 5,220 | |

| Property, plant and equipment | 319 | 690 | 636 | 695 | 636 | 599 | 577 | 572 | 701 | 862 | |

| Investments and other assets | 1,842 | 2,041 | 1,943 | 2,068 | 2,081 | 1,979 | 2,428 | 3,042 | 3,629 | 4,190 | |

| Total assets | 7,934 | 8,126 | 8,501 | 8,890 | 9,640 | 10,072 | 10,313 | 10,872 | 11,723 | 12,662 | |

| Current liabilities | 916 | 799 | 945 | 987 | 1,226 | 1,093 | 1,038 | 1,123 | 1,166 | 1,422 | |

| Short-term borrowings | 20 | 20 | 20 | 20 | 20 | 20 | 20 | 20 | 20 | 20 | |

| Non-current liabilities | 436 | 488 | 502 | 581 | 552 | 658 | 656 | 722 | 1,001 | 1,284 | |

| Total liabilities | 1,352 | 1,288 | 1,448 | 1,568 | 1,779 | 1,752 | 1,695 | 1,846 | 2,167 | 2,706 | |

| Total net assets | 6,581 | 6,838 | 7,053 | 7,321 | 7,861 | 8,319 | 8,617 | 9,026 | 9,555 | 9,955 | |

| Shareholders’ equity | 6,135 | 6,381 | 6,581 | 6,843 | 7,358 | 7,787 | 8,052 | 8,444 | 8,967 | 9,373 | |

| Share capital | 918 | 918 | 918 | 918 | 918 | 918 | 918 | 918 | 918 | 918 | |

| Capital surplus | 1,251 | 1,251 | 1,251 | 1,251 | 1,251 | 1,258 | 1,260 | 1,261 | 1,263 | 1,267 | |

| Retained earnings | 3,680 | 3,812 | 4,026 | 4,181 | 4,761 | 5,274 | 5,560 | 5,805 | 5,891 | 5,880 | |

| Treasury shares | -67 | -67 | -67 | -67 | -67 | -239 | -216 | -194 | -317 | -379 | |

| Valuation/exchange differences | 352 | 466 | 451 | 558 | 494 | 574 | 530 | 654 | 1,211 | 1,687 | |

| Total liabilities and net assets | 7,934 | 8,126 | 8,501 | 8,890 | 9,640 | 10,072 | 10,313 | 10,872 | 11,723 | 12,662 | |

| (Shareholders’ equity ratio) | 77.3% | 78.5% | 77.4% | 77.0% | 76.3% | 77.3% | 78.1% | 77.7% | 76.5% | 74.0% | |

| [Statements of cash flows] | |||||||||||

| Cash flow from operating activities | 573 | 89 | 908 | 549 | 803 | 648 | 284 | 736 | 241 | 595 | |

| Cash flow from investing activities | 99 | -235 | -185 | -115 | 42 | -145 | -291 | -758 | -217 | 43 | |

| Cash flow from financing activities | -107 | -109 | -85 | -85 | -97 | -420 | -236 | -201 | -479 | -283 | |

| Net increase in cash and cash equiv. | 549 | -264 | 684 | 348 | 743 | 95 | -218 | -210 | -433 | 354 | |

| Cash and cash equiv. at beginning of period | 1,098 | 1,648 | 1,383 | 2,068 | 2,416 | 3,159 | 3,255 | 3,036 | 2,826 | 2,393 | |

| Cash and cash equiv. at end of period | 1,648 | 1,383 | 2,068 | 2,416 | 3,159 | 3,255 | 3,036 | 2,826 | 2,393 | 2,747 | |

| Free cash flow | 672 | -146 | 723 | 434 | 845 | 503 | -7 | -22 | 24 | 638 |

Company data

Company Profile

Sales by product category

Cosmo Bio Co., Ltd.

【Head Office】

Toyo-Ekimae Bldg., 2-20, Toyo 2-chome

Koto-ku, Tokyo 135-0016

【Sapporo Office】

3-513-2, Zenibako, Otaru City, Hokkaido

【Shinsuna logistics centre】

12-39, Shinsuna, Koto-ku, Tokyo

3F, Building B, Warehouse No. 3, Shinsuna, Nippon Express Co.

Number of Employees : 182 (Consolidated; as of Dec.31, 2025)

History

| Month/Year | Event |

|---|---|

| Aug. 1983 | Maruzen Oil Biochemicals Co. Ltd. was established as a subsidiary of Maruzen Oil (now Cosmo Oil Co., Ltd.) in Minato-ku, Tokyo, for the purpose of marketing basic biotechnology research reagents. |

| Apr. 1986 | Company name changed to Cosmo Bio Ltd. and sales of bio-research equipment begun. |

| Dec. 1986 | Licensed to sell medicines |

| Apr. 1998 | Establishment of wholly-owned subsidiary CB Development Co., Ltd. to search for suppliers. |

| Sep. 2000 | Independence from Cosmo Oil through a management buyout (MBO). CB Development Co., Ltd. became a non-subsidiary company through a share transfer. |

| Dec. 2000 | Absorption merger of CB Development Co., Ltd. |

| Aug. 2004 | Establishment of wholly-owned subsidiary Cosmo Bio USA Inc. in San Diego, California, USA, to search for suppliers and promote exports. |

| Sep. 2005 | Listed on the JASDAQ stock exchange. |

| Dec. 2006 | Acquired 80% of the shares of Primary Cell Co., Ltd., a company engaged in the research, development, manufacture and sale of primary cultured cells (primary cells) and contract analysis using these cells, and made it a subsidiary. |

| Nov. 2007 | Acquired 30% of the outstanding shares of BM Equipment Co., Ltd., an importer and distributor of consumables and equipment for bio-research, and made it an equity-accounted affiliate. |

| Jul. 2008 | Primary Cell Co., Ltd., a consolidated subsidiary, became a wholly owned subsidiary. |

| Mar. 2010 | Acquired an additional 33% of the outstanding shares of BM Equipment Co., Ltd., making it a consolidated subsidiary with a total shareholding of approximately 63%. |

| Jan. 2013 | Relocated the distribution centre and started operation at the Shinsuna Logistics Centre. |

| Jul. 2013 | Merged with Primary Cell Co., Ltd. |

| Jul. 2013 | Listed on the JASDAQ (Standard) of the Tokyo Stock Exchange following the merger of the Tokyo Stock Exchange and the Osaka Securities Exchange. |

| Nov. 2016 | Established a joint venture Proteintech Japan Co., Ltd. with Proteintech Group, Inc. |

| Oct. 2017 | Relocated and consolidated Sapporo business facilities and opened the Sapporo Site. |

| Jan. 2018 | Cosmo Bio USA, became a consolidated subsidiary. |

| Mar. 2022 | Transition to a company with an audit committee |

| Apr. 2022 | Listed on the TSE Standard following the reorganisation of the Tokyo Stock Exchange. |

Top management

President: Norihiko Shibayama

Apr. 1994 Joined Maruzen Petrochemical Co., Ltd.

Oct. 2000 Joined the Company

Apr. 2012 General Manager, Information Systems Department

Mar. 2014 Director, BM Equipment Co., Ltd.

Nov. 2016 General Manager of General Affairs Department and General Manager of the Information Systems Department

Mar. 2017 Director and General Manager of the General Affairs Department and Information Systems Department

Mar. 2020 Managing Director and General Manager of the General Affairs Department and Information Systems Department

Director and General Manager of General Affairs Department, BM Equipment Co., Ltd.

Mar. 2022 President and Representative Director of BM Equipment Co., Ltd. (to present)

Apr. 2022 Managing Director and General Manager of the General Affairs Department

Mar. 2023 Senior Managing Director and General Manager of the General Affairs Department

Nov. 2023 Representative Director, Senior Managing Director and General Manager of the General Affairs Department of the company, acting for the President and CEO

Mar. 2024 Representative Director and President

Apr. 2026 Representative Director and President, President Operating Officer (to present)

Managing Director : Junko Tochigi

Apr. 1998 Joined the Company

Apr. 2013 Head of Product Communications Department

Mar. 2017 Director and Head of Product Communications Department

Apr. 2017 Director and Head of Corporate Planning Department

Mar. 2021 Director, BM Equipment Co., Ltd

Mar. 2022 President and Representative Director, Cosmo Bio USA, Inc., Representative Director, Proteintech Japan Co., Ltd. (to present)

Mar. 2023 Managing director and Head of Corporate Planning Department

Nov. 2025 Director and CEO (Chief Executive Officer), Cosmo Bio USA, Inc. (to present)

Apr. 2026 Managing director and Managing Operating Officer, Head of Corporate Planning Department (to present)

Director : Masanori Hayashi

Apr. 1994 Joined Kyowa Hakko Kogyo Co., Ltd.

May. 2012 Joined the Company

Apr. 2019 Head of Finance Department

Mar. 2022 General Manager, Finance Department, BM Equipment Co., Ltd

Mar. 2023 Director and Head of Finance Department

Mar. 2024 Director, General Manager of Finance Department BM Equipment Co., Ltd (to present)

Apr. 2026 Director and Operating Officer, Head of Finance Department (to present)

Director, Full-time Audit and Supervisory Committee:Kazutoshi Sato

Apr. 1987 Joined Sumitomo Real Estate Sales Co., Ltd.

Jan. 1993 Joined Cosmo Oil Co., Ltd.

Jun. 2011 Branch Manager, Sapporo Branch, Cosmo Oil Co., Ltd.

Jun. 2014 Branch Manager, Takamatsu Branch, Cosmo Oil Co., Ltd.

Oct. 2015 Cosmo Oil Marketing (Japan) Co., Ltd., Takamatsu Branch Branch manager

Jun. 2017 Director, Executive Officer and General Manager, General Affairs Department, Maruzen Petrochemical Co., Ltd.

Mar. 2020 Outside auditor of the company Auditor of BM Equipment Co., Ltd. (present post)Mar. 2022 Director and full-time audit committee member (to present)

Director, Audit and Supervisory Committee Member:Haruo Sasaki

Nov. 1974 Joined Chuo Audit Corporation

Feb. 1990 Established Sasaki Accounting Office, Director (to present)

Dec. 2000 Outside auditor of the Company

Mar. 2022 Director and Audit Committee member (to present)

Director, Audit and Supervisory Committee Member:Kazuya Shimamura

Oct. 1995 Joined Deloitte Touche Tohmatsu (now Deloitte Touche Tohmatsu LLC)

Apr. 1998 Registered as a chartered accountant

Oct. 2004 Registered as a lawyer Joined Abe, Ikubo & Katayama Law Office

Mar. 2008 Established Shimamura Law & Accounting Office,Representative (to present)

Mar. 2014 Outside director of the Company

Mar. 2022 Director and Audit Committee member (to present)

Director, Audit and Supervisory Committee Member:Junichiro Haraguchi

Apr. 1984 Joined Tokyo Small and Medium Business Investment & Consultation Co., Ltd.

Apr. 2017 Counsellor, Acting Chief Examiner, Tokyo Small and Medium Business Investment & Consultation Co., Ltd.

Jun. 2017 Outside Auditor, Kimoto Co., Ltd. (to present)

Oct. 2020 Acting Director of Tokyo Small and Medium Business Investment & Consultation Co., Ltd.

Apr. 2021 Specially Appointed Counsellor (Operations Department 5 and Sales Management Department), Tokyo Small and Medium Business Investment & Consultation Co., Ltd.

Apr. 2023 Specially Appointed Counsellor (Operations Department 5 and Business Management Department), Tokyo Small and Medium Business Investment & Consultation Co., Ltd. (to present)

Mar. 2024 Director and Audit Committee member of the Company (to present)

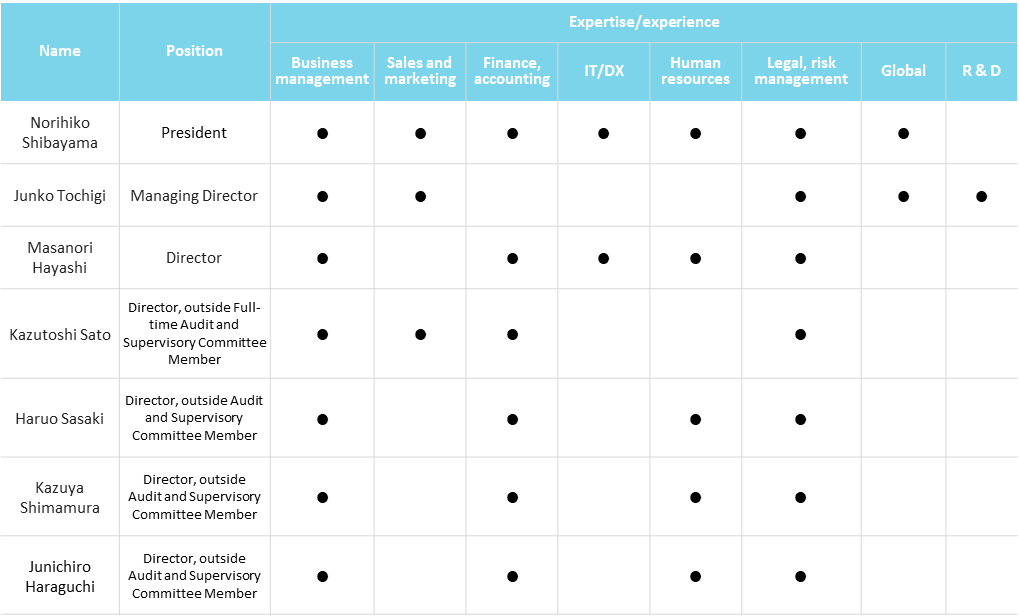

Skills matrix of the Board of Directors’ Members

Source: Company materials

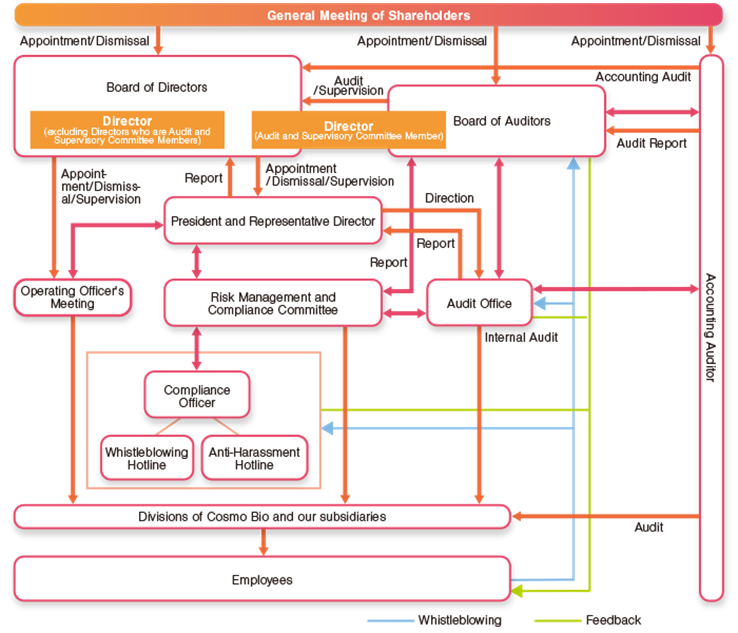

Corporate governance structure

Source: Omega Investment from company materials

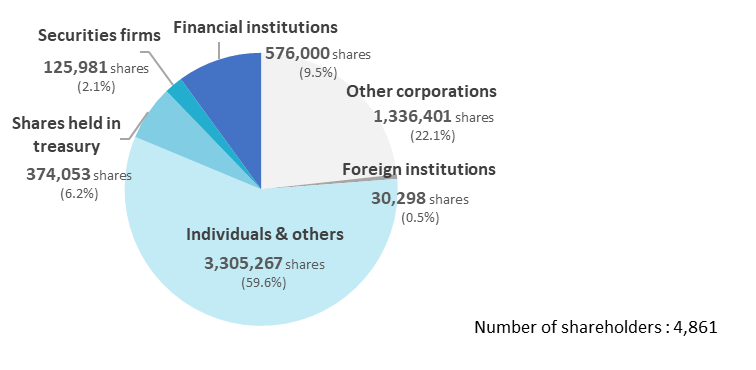

Major shareholders (As of December 31, 2025)

| Name | Number of shares owned | Shareholding Ratio |

| Tokyo Small and Medium Business Investment & Consultation Co., Ltd. |

1,152,000 | 20.30 |

| Mizuho Trust & Banking Corporation Cosmo Oil Co., Ltd. Pension Fund. Re-trustee Custody Bank of Japan, Ltd. |

576,000 | 10.15 |

| UH Partners 2 Limited Partnership for Investment Purposes – General Partner: UH Partners 2 Co., Ltd. |

438,300 | 7.72 |

| Hikari Tsushin KK Investment Limited Partnership: General Partner – Hikari Tsushin Co., Ltd. |

375,500 | 6.61 |

| UH Partners 3 Limited Partnership for Investment Purposes – General Partner: UH Partners 3 Co., Ltd. |

119,500 | 2.10 |

| Haruhisa Sakurai | 96,000 | 1.69 |

| Yumiko Suzuki | 82,300 | 1.45 |

| Cosmo Bio Employee Stock Ownership Plan | 78,500 | 1.38 |

| Kiyoshi Takahashi | 75,700 | 1.33 |

| Toshiaki Funato | 75,400 | 1.32 |

Note: The percentage of shares held to the total number of shares issued (%) excludes treasury shares (374,053 shares).

Source: Omega Investment from company materials

Shareholding by ownership (As of December 31, 2025)

Source: Omega Investment from company materials

Sustainability initiatives

Source: Company materials