2026-08-03

Home

Japanese

Omega Investment Co., Ltd.

Maruchiyo Yamaokaya Corporation (Price Discovery)

Buy

Conclusion

The shares are rated a Buy. Maruchiyo Yamaokaya operates in the ramen chain restaurant sector, which, at first glance, appears intensely competitive and difficult to differentiate. Yet, the company is rapidly expanding sales, operating profit, and net profit, supported by the strength of its existing stores, 24-hour operations, roadside locations, and product appeal driven by in-store preparation. The current share price discounts high growth to a reasonable extent, and with PBR in the 8x range and forecast PER in the low 20x range, the stock offers limited appeal as a low-valuation stock. However, the company combines exceptionally high ROE and ROIC, a sound financial base, brand strength that enables it to maintain customer numbers after price revisions, and room for store openings toward a 500-store structure in Japan. The fair share price under the three methods is estimated at around 3,600 to 4,300 yen under DCF, around 3,800 to 4,500 yen under the PER method, and around 3,400 to 4,300 yen under the PBR/ROE method, suggesting that the current share price is broadly within the fair value range. That said, the company’s plan for FY1/2027 assumes 107% YoY growth in existing-store sales, which appears somewhat conservative. If existing-store sales, store openings, and resilience to price revisions continue, there is scope to aim for a valuation upgrade toward the upper end of the range. Caution is warranted against overheating in the share price, but as long as earnings momentum continues, this is not a phase in which to turn bearish.

Profile

A roadside ramen chain with remaining growth potential. The company is achieving high earnings growth even within the restaurant sector, centred on directly operated stores, 24-hour operations, and in-store preparation.

Maruchiyo Yamaokaya is a ramen chain that originated in Hokkaido and is expanding nationwide, centred on its main brand, Ramen Yamaokaya. Its stores are mainly located along suburban roadsides, and it emphasises sites where large plots and parking spaces can be secured. The company basically operates all stores directly and on a 24-hour basis. It is characterised by preparing soup at each store without using a central kitchen or concentrated soup, and also preparing major ingredients such as chashu pork and green onions in-store. This creates a heavy operational burden for a restaurant chain, but this effort leads to brand distinctiveness, the addictive appeal of its taste, and a deep base of repeat customers. The ramen business is the core business, and the company develops brands such as Yamaokaya, Goku Niboshi Honpo, and Miso Ramen Yamaokaya. In Japan, there is room for store openings in areas such as the western Kansai region, where the company has yet to open stores, and overseas development is also progressing in Shanghai, Thailand, and Singapore—the ramen business accounts for almost 100% of sales.

Sales composition by business, % (operating margin, %): Ramen 99.5, Other 0.5 (FY1/2026)

| Securities Code |

| TYO:3399 |

| Market Capitalization |

| 62,551 million yen |

| Industry |

| Retail trade |

Stock Hunter’s View

Two price revisions were implemented, with no damage to customer traffic.

Maruchiyo Yamaokaya is a ramen chain that operates all its stores directly and 24 hours a day, with 198 stores across 32 prefectures. The company mainly opens stores along suburban roadsides where it can secure sites of at least 300 tsubo and a certain number of parking spaces. Its insistence on not using a central kitchen or concentrated soup, preparing soup by hand, and also preparing core ingredients such as chashu pork and green onions in-store, leads to differentiation from other ramen chains.

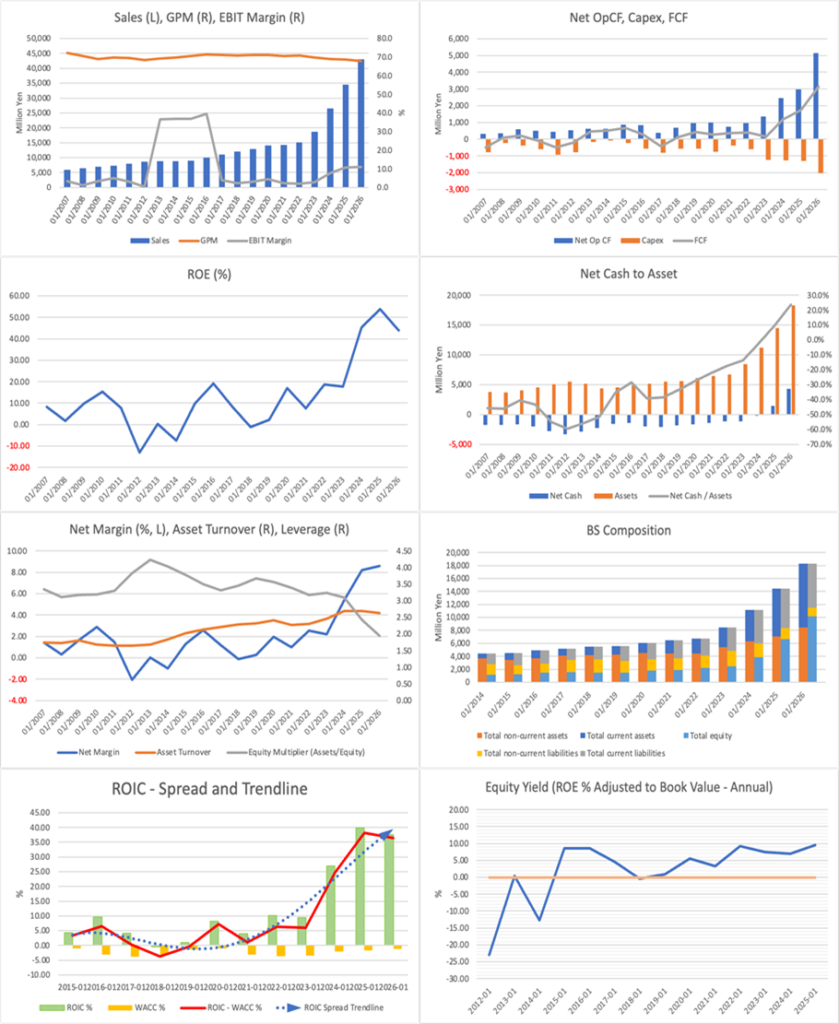

In FY1/2026, the company achieved record-high results, with sales up 24% and operating profit up 26%. Even after price revisions in April and October, the number of visitors did not decline, and full-year existing-store sales rose 19.1% YoY. Other companies in the same industry have also generally remained relatively firm with YoY increases, but the company has performed far above those levels, which is overwhelming. Regular products are priced at 690 yen, giving a sense of relative affordability compared with peers and working to the company’s advantage. In addition, after the COVID-19 pandemic, the number of restaurants operating late at night has decreased, and the advantage of being open 24 hours a day, all year round, appears to be continuing.

For FY1/2027, the company forecasts sales of 48,361 million yen, up 12.5% YoY, and operating profit of 5,184 million yen, up 10.8% YoY. Its assumption for existing-store sales is 107% YoY, which is somewhat conservative. The company plans to open 15 Yamaokaya stores and continues to strengthen property surveys in areas west of Kansai, including those where it has yet to open stores.

Investor’s View

Buy: High growth is discounted to a reasonable extent, but given the strength of existing stores and room for store openings toward a 500-store structure, this remains a phase in which medium-term valuation upside can be targeted.

Maruchiyo Yamaokaya operates in the ramen chain restaurant sector, which at first glance appears intensely competitive and difficult to differentiate, yet what first attracts attention is that sales, operating profit, and net profit are all expanding rapidly. This cannot be fully explained simply by a post-COVID recovery in restaurant demand or by an increase in store openings, and likely, the strength of existing stores, the depth of repeat customers, rising brand recognition, the ability to capture roadside and late-night demand, and improvements in store operations are all overlapping. Although it is in the ramen format, ROE is very high, and the equity ratio is sound at more than 50%. The company should therefore be evaluated not merely as a restaurant retailer but as a growth company with a highly profitable store rollout model.

The focus of the investment judgement is not on undervaluation, but on how far the company can sustain high growth and high ROE. The current share price has already risen substantially, and with PBR in the 8x range and forecast PER also in the low 20x range, there is limited appeal as a low-valuation stock. On the other hand, the company’s earnings growth remains strong. In Japan, the company is advancing a store opening strategy toward a 500-store structure by the end of FY1/2028, and overseas expansion into Shanghai, Thailand, and Singapore is also in view. Yamaokaya has the potential to be revalued from a regional roadside ramen chain into a Japanese restaurant chain with strong brand power. If the increase in existing-store sales continues and the company can maintain its operating margin by absorbing increases in raw material and labour costs through price revisions and store efficiency, the current high share price valuation can remain justified, and a further valuation upgrade can be expected.

A rough estimate of fair value across the three methods suggests a range of 3,600 to 4,300 yen under DCF, 3,800 to 4,500 yen under the PER method, and 3,400 to 4,300 yen under the PBR/ROE method. DCF suggests a range from around the current share price to slightly above it, assuming that sales growth from domestic store openings continues and the operating margin remains near its current level. Under the PER method, applying a growth-stock valuation of around 22x to 26x to forecast EPS for FY1/2027 gives a central range from the high 3,800-yen level to the mid-4,000-yen level. Under the PBR/ROE method, actual PBR is already high in the 8x range, but if ROE is maintained at a high level, the high PBR itself cannot immediately be described as overvaluation. Based on the three methods, the current share price is broadly within the fair value range, but given the strength of earnings momentum, it is positioned to reach the upper end of that range.

From this perspective, the stock is not an undervaluation-correction investment but an investment in which the continuation of growth subsequently justifies the current high valuation. It cannot be denied that the current share price already contains optimism, but the company retains multiple growth drivers, including room for domestic store openings, existing-store sales, average spend per customer, operating hours and location characteristics, and overseas expansion. In particular, if the path toward a 500-store structure is confirmed not merely as a store-number target, but as progress accompanied by earnings growth and sustained ROE, investors will find it easier to value the company not as a restaurant chain, but as a high-margin, high-turnover growth platform. This is the point that leads to a further upgrade in share price valuation.

The downside risk lies in the high sensitivity of the share price to a slowdown in earnings momentum, precisely because growth expectations are high. If existing-store sales growth slows, the pace of store openings is delayed by constraints on hiring or securing locations, increases in raw material and labour costs cannot be sufficiently passed on, or overseas expansion remains limited to upfront costs, the adjustment in PER and PBR could be larger than the decline in the earnings growth rate. In addition, because the ramen format is strongly linked to consumer preferences and cannot entirely avoid fads or changes in the competitive environment, the extent to which existing-store growth can continue should be monitored on an ongoing basis.

Even so, earnings momentum is strong at present, and the financial base is stable. The stock should be positioned as one that aims to capture the medium-term accumulation of value from domestic store expansion and brand value, rather than on short-term undervaluation. The fair share price under the three methods is not far below the current share price; rather, as long as earnings growth continues, the structure is such that the current share price level is justified, with the upper range targeted. Caution is warranted against overheating in the share price, but as long as earnings momentum continues, this is not a phase in which to turn bearish. Investment judgement is Buy.

A structure that appears inefficient, consisting of directly operated stores, 24-hour operations, and in-store preparation, supports the company’s competitive advantage.

The business characteristic of Maruchiyo Yamaokaya is that it deliberately restrains to some extent the efficiency and standardisation that restaurant chains usually pursue, and combines in-store preparation, rich soup, taste creation that readily generates repeat customers, roadside locations, and 24-hour operations. Using a central kitchen would lighten store operations and make it easier to accelerate store openings, but the company continues in-store preparation to maintain a taste with an individual-store feel despite being a chain. In the ramen format, the uniqueness of the taste and the repeat-customer rate determine profitability, so this effort should be viewed not merely as a commitment but as an investment that builds customer loyalty.

In addition, the rollout of roadside stores captures demand that differs from that of small urban ramen shops. Truck drivers, late-night users, suburban residents, and wide-area travellers are among the customer groups, and the company’s stores have unique customer touchpoints in both time period and location. With the number of restaurants operating late at night having decreased after COVID-19, the value of 24-hour operations year-round has increased. The fact that customer numbers did not decline after price revisions indicates that the company’s pricing power has been confirmed to some extent. For restaurant companies, the ability to pass on increases in labour and raw material costs through pricing is extremely important, and Yamaokaya is in a relatively strong position compared with peers in this respect.

In terms of store rollout, against the current level of 198 stores in 32 prefectures, the company is targeting a domestic structure of 500 stores. While it has already gained some recognition as a nationwide brand, there remains untapped potential in areas such as the western part of the Kansai region. Given that the number of stores remains below 200, as long as the strength of existing stores is maintained, there is significant medium-term growth potential in Japan alone. Because the company is primarily operated directly, it requires more investment capital than a franchise model, but at the same time, store operations, quality, and profits are more easily captured in-house. The fact that this directly operated model is compatible with high ROE indicates the strength of the company’s growth model.

The strength of existing stores and resilience to price revisions are driving profit growth. The company’s plan continues to allow for conservatism.

The company’s earnings have changed significantly since FY1/2023. Sales have expanded rapidly, and operating profit, ordinary profit, and net profit have also grown substantially. If this were merely a post-COVID recovery in restaurant demand, the same tailwind would be expected to apply to peers as well, but Yamaokaya’s existing-store sales growth has exceeded the peer average. The fact that customer numbers did not weaken significantly even after price revisions, and that existing-store sales showed strong growth, suggests that the price revisions were not merely cost pass-through, but were supported by brand value.

In the company plan for FY1/2027, sales are forecast at 48,361 million yen and operating profit at 5,184 million yen. Sales and profit are expected to continue rising YoY, but the assumption of existing-store sales at 107% YoY appears somewhat conservative when compared with the previous fiscal year’s results. In the restaurant sector, a change of just several percentage points in the existing-store sales assumption has a large impact on operating profit. In the company’s case in particular, because stores are directly operated, an increase in sales is likely to be accompanied by a certain degree of fixed-cost absorption. Therefore, if existing-store sales outperform the company plan, the structure is such that operating profit is likely to exceed expectations.

However, attention must be paid to the sustainability of the profit margin. In the ramen format, increases in costs such as wheat, pork, oils and fats, utilities, and labour can easily pressure earnings. In addition, maintaining 24-hour operations requires securing personnel and managing profitability during late-night hours. At present, price revisions, customer-number maintenance, and store openings are forming a virtuous cycle, but if this cycle breaks down, investors’ expected growth rate could be revised quickly. Therefore, in future results, the four points to monitor on an ongoing basis are existing-store sales, customer numbers, average spend per customer, operating margin, and the pace of store openings.

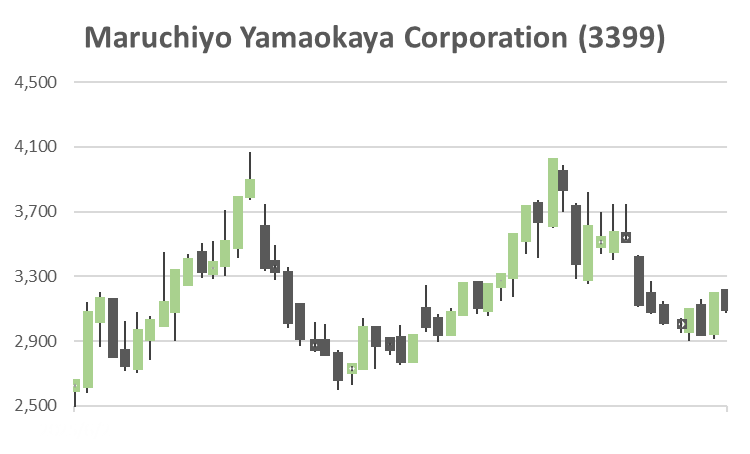

Share Price Trends and Valuation

High PBR is a cautionary sign, but as long as high ROE and high growth continue, it cannot be described as overvaluation immediately.

The company’s shares have risen significantly over the past several years, and the current share price discounts high growth expectations. In the Shikiho share price indicators, the forecast PER is in the low 20x range, and the PBR is in the 8x range, indicating a fairly high valuation for a restaurant company. Normally, a PBR in the 8x range should be viewed with caution. However, in the company’s case, ROE is extremely high, and profit growth continues, so it is not appropriate to judge the stock as overvalued based solely on PBR. For a company that can maintain a high ROE while growing profits at a compounding rate, a high PBR can be seen as a reflection of growth value.

Under the three methods of DCF, PER, and PBR/ROE, fair value is unlikely to yield a conclusion far below the current share price. Under DCF, assuming domestic store openings continue, existing-store sales grow steadily, and the operating margin remains near the current level, the appropriate range is around 3,600 to 4,300 yen. Under the PER method, applying a multiple of 22x to 26x to forecast EPS for FY1/2027 yields a range of 3,800 to 4,500 yen. Under the PBR/ROE method, a range of around 3,400 to 4,300 yen is expected, based on a high ROE. Averaging the central values of the three methods, the current share price is close to the fair value range, but if earnings exceed the plan, a valuation toward the upper end remains possible.

What is important here is not to try to explain the stock in terms of cheap valuation. The investment appeal of the stock does not lie in a low current PER or PBR, but in the fact that continued high growth absorbs the current high valuation over time and creates an even larger profit beyond that. Investors are looking not at the current static PER, but at the number of stores, sales, operating profit, and EPS three and five years from now. If the path toward a 500-store structure becomes more concrete and the strength of existing stores is maintained, the current valuation will gradually lose its sense of being expensive, and the share price will be more likely to rise in line with profit growth.

Domestic store openings, pricing power, and overseas expansion are upside factors. A slowdown in existing stores and cost increases are the greatest risks.

The core growth strategy is expanding the number of stores in Japan. The current number of stores is slightly below 200, and for the company, which aims for a 500-store structure, there remains significant room in Japan. In particular, areas west of Kansai are targets for property surveys and strengthened store openings. The company has the potential to be revalued from an East Japan-centred roadside ramen chain into a nationwide brand. If store openings proceed with profit growth, not only sales but also brand recognition, procurement efficiency, recruiting capability, and store operation know-how will accumulate. The fact that an increase in store numbers is not merely scale expansion but is directly linked to corporate value creation is the focus for investors.

Pricing power is also an important growth factor. The company is maintaining customer numbers after price revisions, which is extremely significant for a restaurant company. In an inflationary environment, there is a major difference in corporate value between companies whose customer numbers decline after price increases and those that can maintain them. In Yamaokaya’s case, the addictive nature of its products, repeat customers, 24-hour operations, and roadside locations support resilience to price revisions. Raw material and labour costs may continue to rise, but the confirmation of a certain level of price pass-through capability supports the maintenance of profit margins.

Overseas expansion should not be excessively discounted in the valuation at this stage, but if successful, it will become a factor for a share price valuation upgrade. Ramen is a Japanese food category that is relatively easy to accept overseas, and Yamaokaya’s rich taste, clear brand, and chain operation know-how have a certain degree of rollout potential. However, overseas markets present difficulties that differ from those in Japan, including location, staffing, ingredient sourcing, local preferences, and franchise management. Therefore, it is appropriate, for now, to view domestic growth as the primary axis and overseas expansion as an additional medium- to long-term growth driver.

The first risk is a slowdown in existing-store sales. The current high share price valuation is premised on the strength of existing stores. If customer-number growth stops and the company enters a phase in which sales are supported only by higher average spend per customer, the market may reassess the quality of growth strictly. The second is increases in labour, raw material, and utility costs. 24-hour operations and in-store preparation are strengths of the company, but they also impose a significant cost burden. The third is a delay in the pace of store openings. Because the company uses a roadside format that requires sites of a certain size and parking spaces, securing good locations is not easy. The fourth is the upfront cost of overseas expansion. If costs come before the overseas business contributes to earnings, the profit margin may be squeezed in the short term.

Even taking these risks into account, the company’s investment appeal has not been impaired. The combination of high ROE, strong existing stores, resilience to price revisions, and room for domestic store openings is relatively rare among restaurant companies. The share price is not low, but there is a reason why it is not cheap. What matters for investors is not simply being cautious about the current high valuation, but assessing whether earnings growth can exceed it. At present, that possibility remains sufficient.

Ownership has a strong owner-oriented character. Liquidity is limited, but commitment to medium- to long-term growth is strong.

The shareholder composition shown in the Shikiho indicates that founding family members and related parties hold substantial stakes and that the company has a strong owner-oriented character. The major shareholders include Tadashi Yamaoka, Maruchiyo Shoji, Toshiyuki Yamaoka, Rie Yamaoka, and Masahiro Yamaoka, and the stable shareholder ratio is high. Financial institutions, securities companies, and foreign investors also account for a certain proportion, but the free-float ratio is not large, and the specified shareholder ratio is high. This creates a liquidity constraint in the supply and demand of shares and also supports management’s medium- to long-term orientation.

In the growth phase of a restaurant chain, the fact that management and the founding family hold meaningful stakes tends to work positively as a commitment to store opening strategy, quality maintenance, and brand building. In particular, for a company such as this, which maintains a labour-intensive operating model of in-store preparation, direct-operated stores, and 24-hour operations, a management stance that emphasises brand value rather than solely short-term profit is necessary. The strong owner-oriented character increases the likelihood that long-term business growth will be prioritised over short-term capital-market responses.

On the other hand, there are also issues with broadening the investor base going forward. Market capitalisation has already reached a certain scale, but if the free float is limited, the amount that large institutional investors can invest will be constrained. For the share price to be valued further, not only earnings growth but also dialogue with investors and enhanced disclosure on the quantitative explanation of the growth strategy, room for store openings, overseas expansion, and capital policy will be important. The quality of a growth company is high, but there remains room to communicate its appeal to domestic and overseas institutional investors fully.

Overall, Maruchiyo Yamaokaya is well placed to advance its medium- to long-term growth strategy, supported by a stable shareholder composition with a strong owner-oriented character. On the other hand, with the share price already discounting high growth expectations, dialogue with the capital markets will become even more important. If the company can continue to show earnings growth, progress toward the 500-store structure, existing-store KPIs, customer-number trends after price revisions, and initial results from overseas expansion, this may lead to a broader shareholder base and a higher share price valuation.

Financials and Valuations

Price

PBR (LTM)

PER (LTM)

ROE (LTM)

EPS (Actual)