2026-06-22

Home

Japanese

Omega Investment Co., Ltd.

Sansei Technologies, Inc. (Price Discovery)

Buy

Conclusion

Investment judgement is Buy. Sansei Technologies is improving sales, EPS, ROE, and the ROIC-WACC spread simultaneously by capturing large-scale projects in Japan and overseas, refurbishment demand, and expansion in the live entertainment market across business fields that, at first glance, appear niche: amusement rides, stage equipment, and elevators. The forecast PER is only 8.34x, and the actual PBR is 0.81x, while the equity yield, calculated by dividing the forecast ROE of 10.3% by the actual PBR of 0.81x, is 12.7%. Although the share price has, to some extent, reflected profit growth over the past five years, it has not yet sufficiently discounted the earnings supported by the order backlog, refurbishment and maintenance demand, and global expansion, including Vekoma, S&S, and FORREC, from FY3/2027 onward. The fair share price is estimated at 3,100-4,500 yen across the PBR, DCF, and ROIC methods, with a median of around 3,800 yen, suggesting ample upside from the current share price.

Profile

Expanding into a global entertainment equipment company centred on amusement rides, stage equipment and elevators.

Sansei Technologies is an industrial machinery manufacturer engaged in the design, manufacture, installation, maintenance and refurbishment of amusement rides, stage equipment and elevators. The company was founded in 1951, began designing and manufacturing stage machinery in 1952, and manufactured Japan’s first roller coaster. Today, in addition to stage equipment and elevators in Japan, it has incorporated S&S Worldwide of the US in 2012, Vekoma of the Netherlands in 2018 and FORREC of Canada in 2023. It handles roller coasters, dark rides, river rapids rides, tower rides, concept proposals for theme parks, stage machinery for theatres and halls, temporary stage equipment for concerts and events, and elevators for public facilities and apartment buildings. Its main customers are theme parks and amusement parks in Japan and overseas, theatres, halls, arenas, concert and event operators, public facilities, apartment buildings and commercial facilities. In amusement rides, it has delivery track records with Walt Disney, Legoland and Six Flags, among others; in stage equipment, it has delivery track records with theatres representing Japan, including the National Theatre, the New National Theatre, Takarazuka Grand Theatre, the Imperial Theatre and Nissay Theatre.

Sales composition by business % (operating margin %): Amusement rides business 63.8% (5.0%), Stage equipment business 25.5% (21.3%), Elevator business 10.7% (26.6%) (FY3/2026)

| Securities Code |

| TYO:6357 |

| Market Capitalization |

| 47,364 million yen |

| Industry |

| Machinery |

Stock Hunter’s View

A global amusement ride company. Also benefiting from tailwinds from expansion in the live entertainment market.

Sansei Technologies is a world-class company specialising in mechanical equipment for amusement parks and theme parks, including roller coasters. It has a delivery track record with Fuji-Q Highland, Huis Ten Bosch, Sanrio Puroland, Tokyo Dome City Attractions, Nagashima Spa Land and Walt Disney, among others.

It also has Japan’s leading delivery track record as a long-established manufacturer of stage machinery. Demand for temporary stage equipment for concerts and events is currently strong. In addition to new-build demand, refurbishment demand for existing facilities is expected to continue for the time being, and the increasing diversification of stage production in recent years, which has made the need for equipment and operating systems more sophisticated, is also a tailwind.

Results for the previous FY3/2026 ended with an 18.1% increase in sales and a 37% increase in operating profit. In the amusement rides segment, large-scale works received in Japan and overseas through the previous fiscal year progressed smoothly, while demand for repair parts remained firm. In the stage equipment segment, temporary stage equipment was strong, and refurbishment works at permanent facilities also progressed steadily. In the elevator segment, new-build and refurbishment works for public facilities and apartment buildings progressed, and the maintenance and servicing business also remained stable.

For the current fiscal year, the company plans sales of 77.0 billion yen, up 5.4% YoY, and operating profit of 7.7 billion yen, up 17.2% YoY. The dividend is set at 95 yen, up 5 yen from the previous fiscal year.

Investor’s View

The shares are undervalued relative to profit growth, accompanied by an improvement in capital efficiency.

The shares are undervalued relative to profit growth, accompanied by an improvement in capital efficiency.

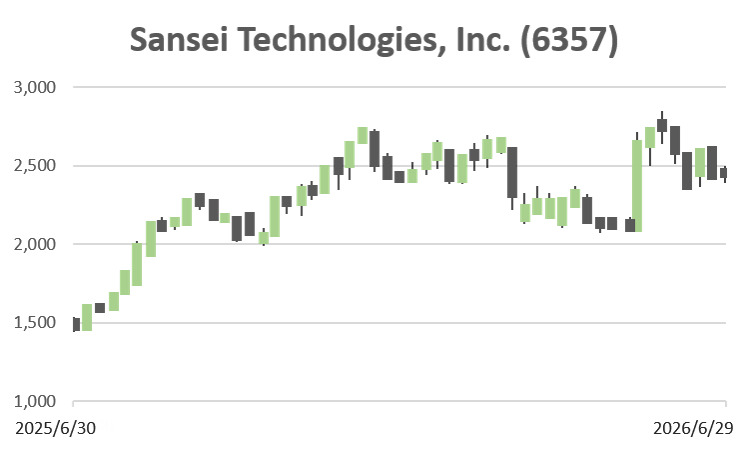

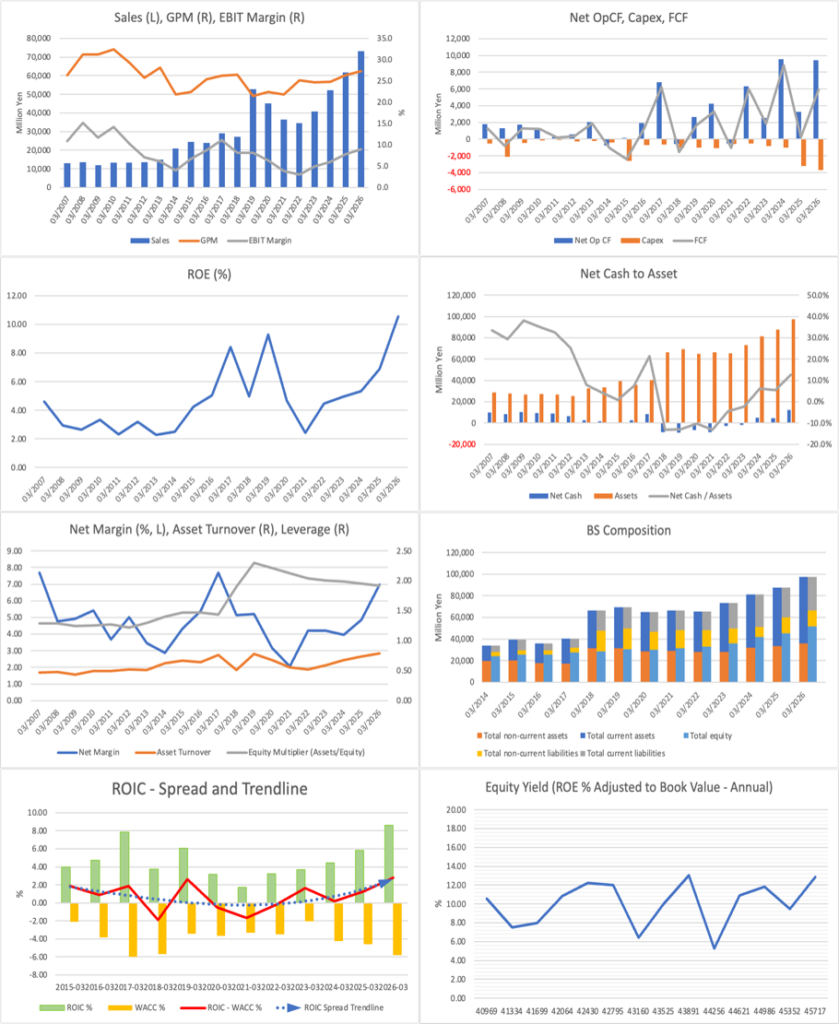

The share price rise over the past five years is not simply a thematic re-rating, but the result of demand recovery after Covid-19, overseas business acquisitions through M&A, refurbishment, and temporary demand for stage equipment, and the stabilisation of earnings from elevators, which has translated into profits. Sales shifted from recovery to expansion from 2021 onward, EPS rose from 2023 onward, and ROE improved to around the double-digit level after a temporary slump. The share price performance from 2021 to 2023 largely anticipated the recovery in demand for leisure and live entertainment after COVID-19. However, market valuation at the time was still centred on a low PBR of around 0.5x, reflecting the discounting of earnings normalisation rather than a revaluation of business value. The marked share price rise in 2025 can be regarded as the point at which the market began to reassess the company not as a low-growth order-based equipment company, but as a global entertainment equipment company, as it reached the stage of achieving sales of 73.07 billion yen, operating profit of 6.57 billion yen and profit attributable to owners of parent of 5.10 billion yen in FY3/2026, and forecasting sales of 77.0 billion yen and operating profit of 7.7 billion yen in FY3/2027.

The rapid expansion in ROE is the result not only of a recovery in sales but also of high margins in stage equipment and elevators, progress in large-scale amusement-ride projects, contributions from repair parts, refurbishment, and maintenance, and improved asset turnover. DuPont analysis suggests that the net profit margin and asset turnover have improved, and that ROE has recovered without relying on excessive increases in leverage. This point is important. If the improvement in ROE depended on an increase in financial leverage, the valuation’s sustainability would be low. Still, in the company’s case, it is an improvement supported by sales growth, stable gross margins, the profitability of stage equipment and elevators, and a thick order backlog. It is sustainable at least over the medium term. However, in amusement rides, fluctuations between fiscal years are unavoidable due to the progress of large-scale projects, and the future issue is the extent to which earnings peaks and troughs can be smoothed by project acquisition capabilities, including Vekoma, S&S and FORREC, and by a rise in the proportion of maintenance and refurbishment revenues.

From an equity yield perspective, the current share price has not sufficiently discounted profit growth. Based on forecast EPS of 299.0 yen, the PER is 8.34x; the dividend yield on the forecast dividend of 95 yen is 3.8%; and the equity yield, calculated by dividing forecast ROE of 10.3% by actual PBR of 0.81x, is 12.7%. Assuming a cost of equity of around 10%, the EPS growth rate discounted in the share price, back-calculated using a dividend discount model, is around 6% per annum. By contrast, the EPS trend shows that the actual CAGR over the past five years has greatly exceeded this level, and the market is discounting a rebound from large-scale projects, earnings volatility as an order-based business, and weak price discovery due to the large number of domestic corporate shareholders. However, given the steady expansion in the ROIC-WACC spread, the company’s ability to create business value has, in fact, strengthened compared with the past, and the valuation at a PER in the 8x range and a PBR below 1x remains conservative.

The expansion of the ROIC-WACC spread provides the basis for shifting the company’s valuation axis from an undervalued stock trading below 1x PBR to a capital-efficiency-improvement stock. ROIC is improving and steadily exceeding WACC, and the trendline is rising as well. This means not merely that profits have increased, but that the ability to generate excess returns on invested capital has strengthened. For future enhancement of shareholder value, disciplined project selection to raise ROIC, management of order backlog profitability, expansion of maintenance and refurbishment revenues, cross-selling with overseas subsidiaries, and consistency in capital policy, including share buybacks and dividends, will be important. The targets in the FY3/2028 medium-term plan of ROE of 10% or more and PBR of 1x or more are not excessive at present; rather, the focus is on whether market valuation catches up with them.

Maruichi Steel Tube’s becoming the largest shareholder is an important feature of the company’s shareholder distribution. Maruichi Steel Tube holds 8.66% of the company’s shares and has increased its holding over the past six months. Maruichi Steel Tube is a steel pipe manufacturer and is not a shareholder with a direct parent-subsidiary relationship or keiretsu relationship with Sansei Technologies’ main businesses, but as an industrial goods company, it can be regarded as a long-term corporate shareholder that values the company’s technology, project execution capabilities and scope for earnings improvement. The presence of stable shareholders supports the long-term management decisions required for an order-based business. In contrast, the large proportion of domestic corporate shareholders, financial institutions, and treasury shares in the shareholder distribution may lead to limited free float and delays in price discovery for foreign and active investors. Therefore, the company should maintain a stable shareholder base while gradually broadening its investor base through English-language IR, quantitative disclosure of capital efficiency, and explanations for overseas investors.

The sales drivers of the main businesses are, in amusement rides, capital investment by theme parks in Japan and overseas, new attractions, renewal of existing rides, repair parts, maintenance and large-scale projects at overseas parks; and in stage equipment, new construction of theatres and halls, refurbishment of existing facilities, temporary stage equipment for concerts and events, and demand for control systems accompanying increasingly sophisticated stage production. In elevators, new-build and refurbishment for public facilities, apartment buildings and special applications, as well as maintenance and servicing, provide a stable base. Regarding market share, the company explains that it is world-class in amusement rides and a leading company in Japan in stage equipment. Although explicit numerical share data is limited, based on its delivery track record and the positions of its group companies, it can suggest it is a strong player in niche markets. Competitors in amusement rides include overseas specialist manufacturers such as Mack Rides, Intamin, Bolliger & Mabillard, Zamperla and Gerstlauer; in stage equipment, domestic stage machinery and event equipment companies; and in elevators, major elevator manufacturers and regional maintenance companies. However, the company’s distinctive characteristic is that the group covers everything from theme park concept design to ride manufacturing, stage and production equipment, and maintenance and refurbishment, and its axis of competition differs from that of single-product manufacturers.

Valuation

The PBR, DCF and ROIC methods all indicate upside from the current share price

Based on forecast EPS of 299.0 yen, the current share price of 2,495 yen is valued at a PER of 8.34x. Based on actual BPS of 3,085 yen, the PBR is 0.81x. Market capitalisation, based on 19.33 million shares outstanding, is 48.2 billion yen. Assuming a forecast dividend of 95 yen, a forecast payout ratio of 31.8%, a dividend yield of 3.8%, and a cost of equity of around 10%, the expected EPS growth rate discounted in the share price is around 6% per annum. This is well below the actual EPS growth rate over roughly the past five years, indicating that the market is discounting, to a considerable degree, the rebound from large-scale projects and the volatility inherent in an order-based business.

| Method | Main assumptions | Fair share price range | Median |

| PBR method | Forecast ROE of 10.3%, cost of equity of 10%, medium- to long-term growth rate of 2-4%, fair PBR of 1.0-1.4x | 3,100-4,300 yen | 3,700 yen |

| DCF method | Mid-single-digit profit growth from FY3/2027 onward, terminal growth rate of 2%, cost of equity of 10% | 3,300-4,500 yen | 3,900 yen |

| ROIC method | WACC of around 6%, ROIC in the 8-9% range, continued expansion in the ROIC-WACC spread | 3,400-4,300 yen | 3,800 yen |

| Median of three methods | Average of the central values of each method | 3,100-4,500 yen | Around 3,800 yen |

The median of the three methods is around 3,800 yen, indicating 52% upside from the current share price of 2,495 yen. A recovery to 1x PBR alone would bring the share price to 3,085 yen, 23.6% above the current share price, and if the company’s medium-term plan targets of ROE of 10% or more and PBR of 1x or more become accepted by the market, a PBR of around 1.2x, or around 3,700 yen, can be sufficiently explained.

Shareholder distribution

Stable shareholders support long-term management, but also tend to delay price discovery.

The leading shareholders include Maruichi Steel Tube, Sansei Technologies treasury shares, Sumitomo Mitsui Financial Group, Keihanshin Building, Sanju San Financial Group, Torishima Pump Mfg., Sumitomo Mitsui Finance and Leasing, and Sumitomo Realty & Development. The leading shareholders include many domestic corporates, financial institutions and treasury shares, and their combined ownership ratio is high. This has the merit of management stability, but also the drawbacks of constrained free float, limited scope for overseas investors to enter, and a time lag before improvements in ROE and ROIC are reflected in the share price. In particular, for a company such as Sansei Technologies, whose business content is niche and whose business model, including overseas subsidiaries, takes time to understand, broadening the investor base is likely to lead directly to normalisation of share price valuation.

| Shareholder | Ownership ratio | Change in shares [6M] | Comment |

| Maruichi Steel Tube Ltd. | 8.66% | +374 thousand shares | Largest shareholder. Considered to be a corporate shareholder with a long-term perspective. |

| Sansei Technologies, Inc. | 8.32% | +456 thousand shares | Treasury shares. Indicates scope for capital policy. |

| Sumitomo Mitsui Financial Group | 7.75% | +1 thousand shares | Stable financial-sector shareholder. |

| Keihanshin Building Co., Ltd. | 4.28% | 0 | Domestic corporate shareholder. |

| Sanju San Financial Group | 4.16% | 0 | Stable financial-sector shareholder. |

| Torishima Pump Mfg. Co., Ltd. | 4.14% | 0 | Industrial goods corporate shareholder. |

Financials and Valuations

Price

PBR (LTM)

PER (LTM)

ROE (LTM)

EPS (LTM)

BPS (LTM)