2026-07-27

Home

Japanese

Omega Investment Co., Ltd.

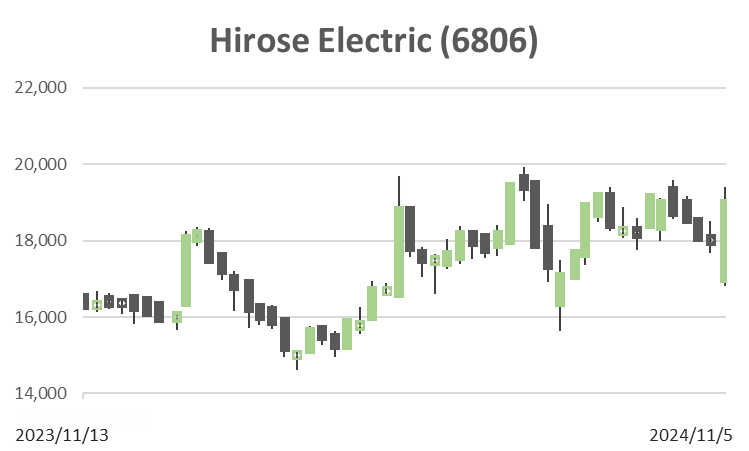

Hirose Electric (Price Discovery)

Sell

Profile

Manufactures and sells electrical and electronic connectors in applications such as automobiles, mobile communications, telecommunications, networks, and smart grids. The product lineup includes printed circuit boards, optical connectors, optical fiber cables, waterproof connectors, microwave components, switches and sensors, modular jacks and plugs, integrated circuit cards and sockets, coaxial cables, etc. Established in 1937 by Keizo Hirose. Sales by business segment % (OPM%): Multipole connectors 90 (20), Coaxial Connectors 7 (28), Others 3 (14) <Overseas> 80 (FY2024.3)

| Securities Code |

| TYO:6806 |

| Market Capitalization |

| 674,616 million yen |

| Industry |

| Electronic equipment |

Stock Hunter’s View

The revised forecast is conservative. There is a gradual recovery trend in industrial machinery.

Hirose Electric, a manufacturer specializing in connectors, can expect to see its business expand in line with the recovery of the industrial machinery market.

The company’s financial results for the second quarter of FY3/2025 (April to September), announced on November 1, showed sales revenue of 94,519 million yen (up 14% YoY) and operating profit of 22,216 million yen (up 29.2% YoY). At the same time, the company revised its full-year operating profit forecast upwards from 36 billion yen to 38 billion yen (up 11.7% YoY). This is a reasonably conservative forecast given that the 1H saw an upward swing of 6.2 billion yen.

Although the degree of recovery in the general industrial machinery market is thought to be lower than initially expected, sales of products for smartphones and mobile devices, which are usually slow due to seasonality, have been strong from the 1Q. Moreover, the automobile business is expected to exceed initial forecasts. It appears that demand was brought forward to the 1H of the year, but the company will continue to work on acquiring orders for new models and other products, such as notebook PCs and tablets. There is expected to be a replacement of devices in line with the AI boom this year and next year. In addition, demand for general industrial machinery such as FA equipment hit bottom in the 4Q of the previous fiscal year (January to March) and is gradually recovering.

In May this year, the company announced its first medium-term management plan with numerical targets, indicating its confidence in growth. In September, it announced a capital and business alliance with a manufacturer of optical devices, and other moves can be seen as laying the groundwork for growth.

Investor’s View

SELL. There is not much excitement in the stock price, and it is difficult to expect significant alpha. Based on experience, there is a risk that the decline in PER may accelerate from here.

Looking back over the company’s 20-year share price and fundamentals, while the growth in BPS is not particularly attractive at a CAGR of 4.2%, the consistent growth is impressive. In terms of earnings, there is a 5- to 9-year cycle in ROE and PER, so the company is thought to be cyclical. PER quickly incorporates the expectation of a recovery in ROE and EPS, but the decline after attaching the overly optimistic multiple is rapid.

Price

PBR

PER

ROE

EPS

BPS

PBR has been moving in a range of approximately 1.5-2.0x over the past 10 years. The stability of the PBR band suggests that investors are well aware of the extent of the company’s BPS growth power, and there are neither high expectations nor concerns.

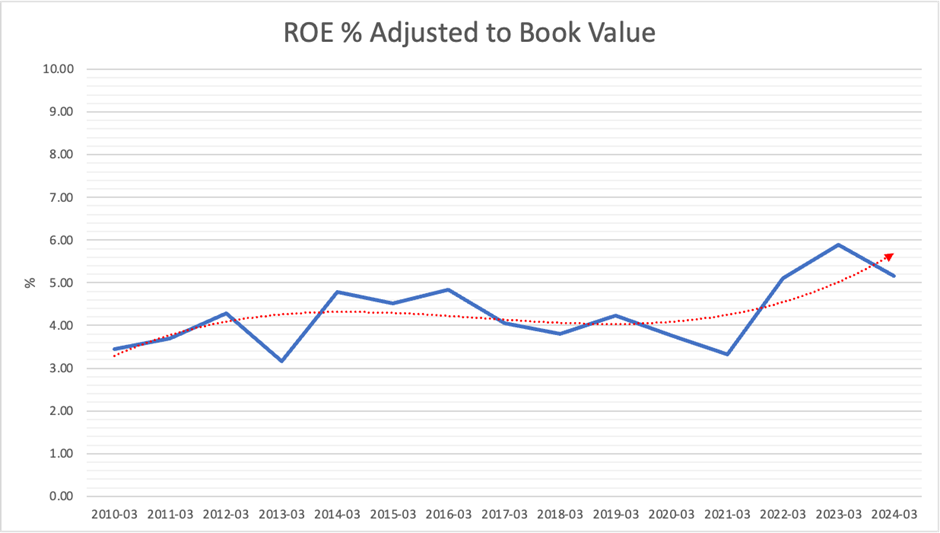

The long-term equity yield measured by ROE adjusted for PBR is roughly range-bound between 3-5%. The equity yield was attractive a year ago, but has declined and is currently converging to the long-term range. Thus there is no significant undervaluation in the current stock price.

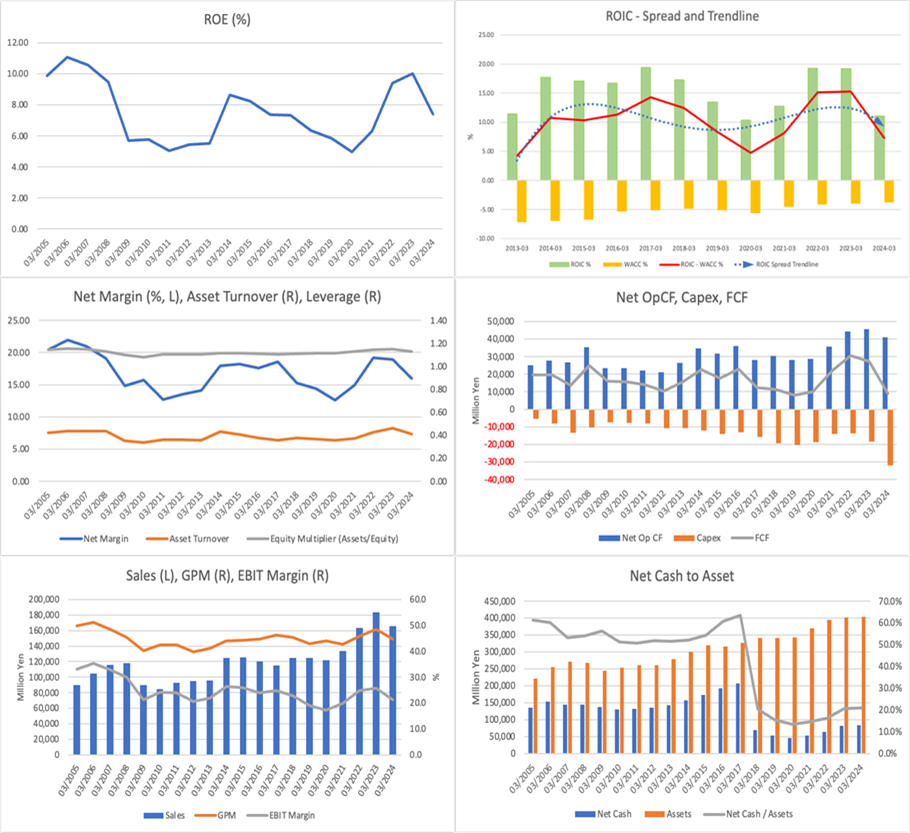

As with Japanese tech stocks, ROE, economic value, and operating cash flow peaked in the previous fiscal year. The best of the business cycle has been discounted in the share price.

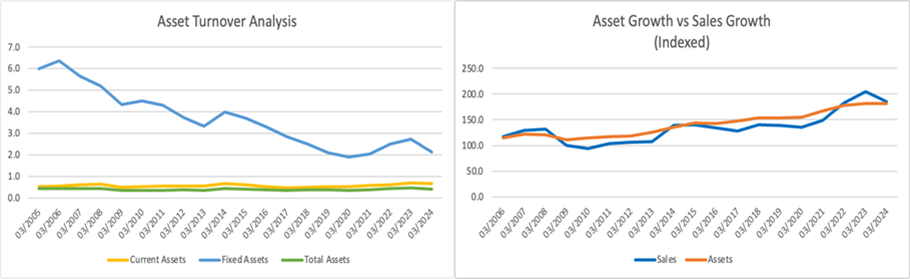

The long-term decline in the asset turnover ratio has not stopped. This is because the burden of fixed assets has only continued to increase. There could be an unprecedented industry boom that boosts the company’s PL profit margin. However, the expansion of assets will likely mute this, and it is expected that the ROE range will not move up from the past level. This is not the case if a significant business reengineering takes place, but this needs to be depicted in the medium-term plan.