2026-07-27

Home

Japanese

Omega Investment Co., Ltd.

KYODO PUBLIC RELATIONS (Investment report – Basic)

| Share price (6/17) | ¥1,022 | Dividend Yield (26/12 CE) | 1.6 % |

| 52weeks high/low | ¥826/1,103 | ROE(25/12) | 22.7 % |

| Avg Vol (3 month) | 13.5 thou shrs | Operating margin (25/12) | 15.2 % |

| Market Cap | ¥9.01 bn | Beta (5Y Monthly) | -0.37 |

| Enterprise Value | ¥5.59 bn | Shares Outstanding | 8.814 mn shrs |

| PER (26/12 CE) | 9.9 X | Listed market | TSE Standard |

| PBR (25/12 act) | 2.1 X |

| Click here for the PDF version of this page |

| PDF version |

AI and influencers were added to the highly profitable PR base. With capital policy also added, the stock is in a phase where a valuation uplift can be targeted

Investment View

AI and influencers were added to the highly profitable PR base. With capital policy also added, the stock is in a phase where a valuation uplift can be targeted

KYODO PUBLIC RELATIONS (the “Company”) is evolving its business structure from a traditional PR company into a highly profitable communication company by combining influencer marketing and AI & Big Data solutions on the foundation of stable retainer-type revenues accumulated over many years as an independent PR company. In FY12/2025, the Company renewed record-high levels, with net sales of 8.554 billion yen, operating profit of 1.302 billion yen, and net income attributable to owners of the parent of 863 million yen. In the first quarter of FY12/2026, it continued to post double-digit YoY growth in both sales and profits, with net sales of 2.346 billion yen, operating profit of 458 million yen, and quarterly net income attributable to owners of the parent of 268 million yen. The Company has set targets of net sales of 10.0 billion yen and operating profit of 1.6 billion yen for FY12/2026, and progress as of 1Q was 23.5% for net sales and 28.7% for operating profit, indicating a smooth start on the profit side.

The investment appeal of the Company’s stock can be organized into three elements. First, the PR business is expanding while maintaining a high profit margin. In the first quarter of FY12/2026, the PR business recorded net sales of 1.704 billion yen and operating profit of 373 million yen, representing YoY increases of 11.5% in net sales and 19.8% in operating profit. Retainer sales support stability, while spot projects push up net sales growth through demand recovery and the acquisition of large projects. The PR business is the core of the Company’s corporate value creation and plays a role in creating profit depth.

Second, influencer marketing and AI & Big Data solutions are driving growth and reshaping the business image of the PR business. In 1Q, the influencer marketing business recorded net sales of 308 million yen and segment profit of 39 million yen. The AI & Big Data solutions business recorded net sales of 335 million yen and operating profit of 81 million yen. In particular, the AI & Big Data solutions business grew significantly, with net sales up 40.0% and operating profit up 49.9%. We would like to positively note that the Company’s initiative to commercialize AI utilization and data analysis is beginning to appear in the numbers, including Dataiku hands-on support, ShtockData, CERVN, and Tableau-related human resources and services, is beginning to appear in numbers.

Third, the share buyback, stock split, and change to the shareholder benefit program announced in May 2026 are important moves that add capital-market measures to the business side of growth. The share buyback has an upper limit of 200 million yen and 200,000 shares, with the acquisition period from June 1 to November 30, 2026. The stock split divides one share into two shares, with July 1, 2026, as the effective date. The Company also simultaneously resolved to effect a stock split to improve stock liquidity and expand its investor base. In small-cap stocks, not only business growth but also liquidity, shareholder returns, and the expansion of the individual investor base significantly impact stock price formation. We believe the newly announced capital policy demonstrates the Company’s awareness of liquidity and capital efficiency issues, which have historically been conventional challenges.

On the other hand, the current stock price implies a forecast PER of 10.0x, an actual PBR of 2.07x, and a forecast ROE of 21.5%. It is necessary to carefully examine what the market is pricing in rather than simply concluding that the stock is undervalued. Assuming a forecast EPS of 103.2 yen and a forecast dividend of 16 yen, the dividend payout ratio is 15.5% and the internal retention rate is 84.5%. If ROE of 21.5% can be maintained, the theoretical sustainable growth rate is approximately 18.2%. On the other hand, the earnings yield based on the forecast PER of 10.0x is 10.0%, and the actual PBR of 2.07x is not an excessive valuation level for a high-ROE company. If the cost of capital is assumed to be around 9% to 10%, the EPS growth expectations priced into the current stock price appear to remain in the low- to mid-single digits. EPS CAGR from 2022 to 2025 was approximately 17%, and from 2021 to 2025 was approximately 57%, including the recovery from a temporarily low level. The market is not extending several years of profit growth into the future, and it is difficult to say it has sufficiently priced in growth expectations for the AI/data domain.

However, the background to the cautious stock price valuation of around a PER of 10x cannot be fully explained solely by insufficient pricing in of growth expectations. The larger constraint is the small market capitalization and low liquidity. In terms of high ROE, high ROIC, net cash, and double-digit profit growth, the Company has conditions that could attract institutional investors. However, its market capitalization remains at around 10.0 billion yen, and daily trading value is limited. For this reason, for domestic and overseas institutional investors that manage large amounts of capital, the stock has become one for which, apart from the appeal of the company’s fundamentals, it is difficult to invest sufficient capital, and liquidity risk at the time of sale must also be considered. It is natural to consider that the current valuation of around PER 10x reflects a small-cap stock discount associated with the small market capitalization and low liquidity, rather than indicating that the Company’s profitability and growth potential are viewed as low.

Based on the above, we believe the Company’s stock is in a phase where a valuation uplift can be targeted, supported by the high profitability of the PR business, growth in the AI & Big Data domain, and progress in capital policy. However, to achieve this, the AI & Big Data solutions business must continue to expand its profit contribution as well as net sales growth, so that both retainer sales and spot sales in the PR business continue to trend firmly, and that the share buyback and stock split lead to improved liquidity and expansion of the investor base. At this point, it should be effective at assessing the stock valuation and viewing the Company not merely as a PR company but as a highly profitable communications company that combines PR expertise, influencer IP, and AI/data utilization.

1. Business model and business structure

Three pillars combining influencers and AI/data on a retainer-type PR earnings base

KYODO PUBLIC RELATIONS is an independent PR company founded in 1964 and handles a wide range of services, including corporate public relations, media relations, crisis management public relations, IR support, digital PR, and overseas public relations. Unlike a traditional advertising agency business, the core of its business is supporting the building of relationships between client companies and the media, consumers, and stakeholders. The strength of the PR business lies not only in one-off projects but also in retainer-based revenue from ongoing contracts. Public relations activities for client companies do not end once they are designed; day-to-day information dissemination, media response, crisis management, and communication design according to management issues are continuously required. This is where the Company’s revenue stability is generated.

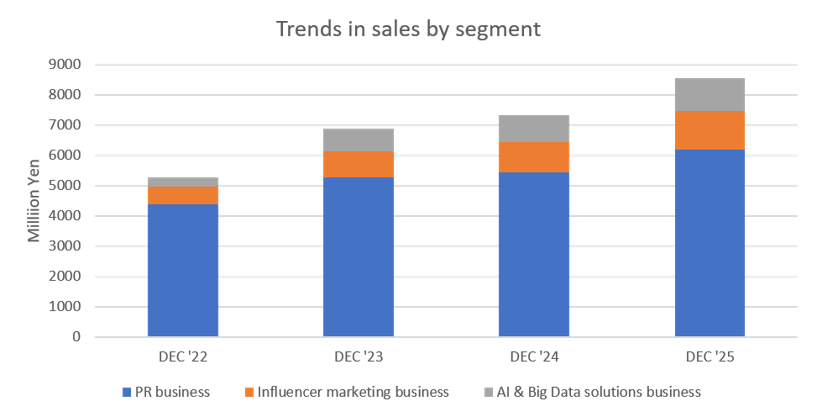

The Company’s business comprises three pillars: PR, influencer marketing, and AI & Big Data solutions. In the net sales composition for FY12/2025, the PR business accounted for approximately 70% of the total, while the influencer marketing business and the AI & Big Data solutions business each grew to the 1 billion yen range. In the first quarter of FY12/2026, the PR business recorded net sales of 1.704 billion yen, the influencer marketing business recorded 312 million yen, and the AI & Big Data solutions business recorded 336 million yen. The structure in which two growth businesses are added to the mainstay PR business continued.

The PR business is the source of stable earnings and profit margins in the Company’s corporate value formation. Retainer sales generally accumulate each quarter steadily, while spot projects support growth and fluctuate with demand for thematic public relations, large projects, government and municipal projects, and the expansion of commercial flow in the Kansai area. In the first quarter of FY12/2026, the Company also advanced the deepening of existing customer relationships and the acquisition of new inquiry projects through retainer transactions. It helped strengthen its capabilities in digital PR, influencer marketing, and AI & Big Data solutions. With retainer revenues providing support, the PR business as a whole remains highly profitable.

The influencer marketing business, centered on VAZ, utilizes youth-oriented media and creators for tie-up projects, fan-community initiatives, and product development. The Company utilizes its own media and creator base, including Merupuchi, MelTV, and CulDRAMA, to provide advertisers with touchpoints with Generation Z. In 1Q, the Company presented utilization of Merupuchi proprietary IP, the Merupuchi Audition 2026, the launch of the 11-member idol group α+, the surpassing of 1.5 million subscribers by Cosme Wota Channel Sara, and the launch of the Mel: See brand. This can be understood as a shift from merely undertaking tie-up projects to making proprietary IP and fan communities sources of revenue.

The AI & Big Data solutions business plays an important role in changing the Company’s business image. Centered on KeyWalker, the Company provides services for ShtockData, CERVN, Dataiku, and Tableau, as well as other offerings, and supports companies’ data collection, analysis, visualization, and AI utilization. In 1Q, the Company presented the continuation of Dataiku hands-on support, evaluations of ShtockData in the market and competitive research category, evaluations of CERVN, receipt of the Dataiku Award, and the selection of an employee for Tableau DataFam Rising Stars 2026. These are factors showing that the Company’s group has received a certain level of external evaluation in the AI/data domain.

What is important in evaluating the Company’s business model is that the three pillars are not simply arranged in parallel but are beginning to have mutually complementary relationships. The PR business has customer touchpoints and trust. The influencer marketing business has touchpoints with younger generations and on SNS. The AI & Big Data solutions business has functions for data collection, analysis, and improving operational efficiency. When these are combined, the Company can provide public relations activity design, execution, effectiveness measurement, SNS analysis, and data utilization in an integrated manner. What investors should focus on is not the simple sum of net sales, but the extent to which this combination increases project unit prices, retention rates, profit margins, and share of wallet with customers.

2. Business strengths and competitive advantages

Using PR expertise as the customer base, the Company increases revenue reproducibility through AI implementation and proprietary IP

The Company’s strength lies, first, in its long track record and customer base as a PR company. Because PR operations require relationships with the media, reading social contexts, crisis management, timing of information dissemination, and understanding of management issues, they are not simple operational outsourcing. For client companies, changing PR companies involves transferring past public relations context and media relations, and rebuilding understanding of management issues. Therefore, a PR company that has accumulated a certain level of results and trust is likely to maintain ongoing contracts. The Company’s retainer-type revenues can be considered stable revenues backed by these switching costs.

The most important KPIs for the PR business are the number of retainer-contracting companies, retainer sales, the number of spot projects, project unit prices, and operating profit margin. Retainer contracts support net sales by generating monthly or periodic revenue. On the other hand, spot projects help increase net sales through large public relations projects, campaigns, crisis management responses, and government- and municipal-related projects. In 1Q, the Company advanced the deepening of existing customer relationships and the acquisition of new inquiry projects through retainer transactions. The structure in which retainer sales provide stable earnings and spot sales drive growth is an easy-to-understand point when evaluating the Company’s PR business.

The second strength is the high profit margin of the PR business. In the first quarter of FY12/2026, the PR business recorded an operating profit of 373 million yen on net sales of 1.704 billion yen, with an operating profit margin of 21.9%. It also improved from the operating profit margin in the 20% range in the same period of the previous year. The PR business has aspects of a human-resource-intensive business, but if project expertise, the customer base, operational standardization, and AI utilization progress, it can maintain a value-added earnings structure without remaining merely a simple person-month-type business. The background to the Company setting forth the establishment of the AIC Center, promotion of companywide AI utilization, X linkage for SAKAE, development of SAKAE for Client, and AI talent development is its aim of achieving both sophistication and efficiency improvement of PR operations.

The point to confirm here is how AI utilization will be reflected in productivity improvement in the PR business, without remaining merely the introduction of operational support tools. Specifically, attention will be paid to net sales per person in charge, the number of projects processed, person-hours spent on preparing proposals, releases, and reports, efficiency improvements in media list management and SNS monitoring, and improvements in the accuracy of public relations effectiveness analysis. If these improve, the number of projects that can be handled with the same number of personnel will increase, and net sales and profits can be increased without significantly increasing fixed costs. The essence of the PR business lies in human expertise. Nevertheless, by combining it with AI, it is possible to increase revenue reproducibility while maintaining the quality of human resources.

The third strength is that the Company is cultivating proprietary IP in the influencer domain. Influencer marketing is in demand among advertisers, but it tends to depend on specific platforms and individual creators. Therefore, the Company’s integrated efforts involving Merupuchi, auditions, fan communities, product development, and brand launches are significant in that they do not limit revenue sources to tie-up projects alone. If fan communities and proprietary IP are cultivated, the Company can create multilayer revenue opportunities not only through project acquisition for advertisers, but also through product commercialization, live events, fan clubs, and commerce. Net sales in 1Q increased 15.4% YoY, and operating profit increased 10.4% YoY, and growth is continuing. However, the profit margin is lower than in the PR business and the AI & Big Data solutions business, and the focus going forward will be on whether IP development improves profit margins.

As KPIs for the influencer business, the number of affiliated creators, the number of followers and subscribers of major creators, the number of video views, the number of tie-up projects, project unit prices, view counts for proprietary media, the number of fan community members, and net sales from product commercialization and brand development will be important. For advertisers, value lies not simply in having a large number of followers, but in reaching users in specific age groups and with specific preferences with high precision. Therefore, the Company’s ownership of proprietary media and proprietary IP has the potential to strengthen proposal capabilities to advertisers and raise project unit prices. Going forward, if monetization of Merupuchi and related brands progresses, the influencer business can be positioned not as a peripheral business to the PR business, but as an independent growth driver responsible for communication targeting younger generations.

However, in this domain, it is necessary to confirm not only the expansion in net sales but also the quality of revenue. If dependence on creators and SNS platforms is high, the business is susceptible to fluctuations in popularity and algorithmic changes. Therefore, the extent to which the Company has proprietary IP, proprietary media, proprietary brands, and fan communities, and can generate recurring revenue, will be important. If the two-stage structure is realized in which an increase in tie-up projects pushes up short-term net sales and cultivation of proprietary IP creates a medium-term earnings base, the contribution of this business to corporate value will increase.

The fourth strength is that the AI/data domain is trending with high growth and a high profit margin. In 1Q, the AI & Big Data solutions business recorded net sales of 335 million yen and operating profit of 81 million yen, and the operating profit margin reached the 24% range. YoY, net sales increased 40.1%, and operating profit increased 49.9%. This shows that the Company’s group is entering domains involved in corporate business transformation, including data infrastructure construction, BI implementation support, web monitoring, SaaS-type services, and Dataiku hands-on support, rather than simply providing digital support around PR.

KPIs that should be emphasized in the AI & Big Data solutions business are the number of companies adopting ShtockData, CERVN, and other services, contract retention rate, recurring fee sales, net sales per customer, the number of Dataiku hands-on support projects, project unit prices for BI implementation support, and the rate of additional proposals to existing customers. The AI/data domain has high market growth potential, but competition is also intense. Therefore, it is necessary to identify not merely whether AI-related net sales are growing, but also which services become ongoing revenue sources, which services generate high-unit-price project revenues, and which services increase share with customers through linkage to the PR business.

For the Company, the importance of the AI & Big Data solutions business lies in the potential to shift the axis of stock price valuation more than in its net sales scale. If it were only the PR business, the market would likely evaluate the Company as a mature services company. However, if it is confirmed that the AI/data domain is expanding rapidly, has high profit margins, and contributes to productivity improvements in the PR business, the Company may be redefined as a highly profitable communications company. In particular, if products such as ShtockData and CERVN take the form of accumulating recurring fee sales, product-type revenues will be added to labor-intensive service revenues, working positively for both profit margins and valuation.

The fifth strength is financial soundness. As of the end of March 2026, total assets were 6.638 billion yen, net assets were 4.885 billion yen, and the equity ratio was 65.0%. This has improved from the equity ratio of 62.9% at the end of December 2025, and dependence on liabilities is low. Cash on hand is also substantial, and net cash has accumulated to around 3.4 billion yen. Even though the Company is a small-cap growth company, its low financial risk is important when considering downside resilience in the stock price.

However, the Company’s strengths differ from the structure of a SaaS company that expands fully automatically. PR, influencers, and AI hands-on support all depend heavily on the quality of human resources. Therefore, the monitoring items going forward are not only the net sales growth rate but also net sales per employee, project unit prices, increases in retainer sales, reductions in person-hours through AI utilization, operating profit margin in the AI & Big Data domain, and monetization of influencer IP. We would like to confirm whether the Company’s full AI shift is not merely thematic but is linked to maintaining and improving the operating profit margin.

Overall, the Company’s competitive advantage lies in the convergence of PR expertise, customer base, influencer touchpoints, and AI/data technologies. The PR business generates stable profits, the influencer business expands communication targeting younger generations, and the AI & Big Data solutions business pushes up the growth rate and profit margin. As long as this three-layer structure functions, the Company can be positioned as a company that has advanced one step beyond the market perception of a traditional PR company and can target a stock price valuation uplift as a highly profitable communication company.

3. Positioning of the medium-term management plan and 1Q results

Toward net sales of 10.0 billion yen and operating profit of 1.6 billion yen, the 1Q profit progress is ahead

As its full-year plan for FY12/2026, the Company has set targets of net sales of 10.0 billion yen, operating profit of 1.6 billion yen, ordinary profit of 1.6 billion yen, and net income attributable to owners of the parent of 900 million yen. Compared with the FY12/2025 results of net sales of 8.554 billion yen and operating profit of 1.302 billion yen, the plan expects a 16.9% increase in net sales and a 22.8% increase in operating profit. First-quarter results were net sales of 2.346 billion yen, operating profit of 458 million yen, ordinary profit of 461 million yen, and quarterly net income attributable to owners of the parent of 268 million yen. Progress toward the full-year plan was 23.5% for net sales, 28.7% for operating profit, and 29.8% for net income attributable to owners of the parent. Profit progress exceeded the quarterly pace, and it is a favorable start toward the full-year plan.

The takeaway from the 1Q results is that all segments achieved growth in both sales and profits. The PR business recorded net sales of 1.704 billion yen and operating profit of 373 million yen, the influencer marketing business recorded net sales of 308 million yen and operating profit of 39 million yen, and the AI & Big Data solutions business recorded net sales of 335 million yen and operating profit of 81 million yen. The PR business played a core role in profits, and the AI & Big Data solutions business drove overall growth with high growth and a high profit margin. The influencer marketing business also maintained growth in both sales and profits, and the three-pillar structure is functioning firmly.

In assessing the achievement of the medium-term management plan, it is important not only to reach net sales of 10.0 billion yen but also to achieve an operating profit margin of 16%. The operating profit margin was 15.2% in FY12/2025 and 19.5% in the first quarter of FY12/2026. Since 1Q is affected by seasonality and project mix, caution is warranted when assuming this level will be maintained for the full year; at a minimum, the profit margin is not trending poorly. Given that operating profit margins in the PR and AI & Big Data solutions businesses exceed 20%, improving profitability in the influencer marketing business will increase the likelihood of achieving a companywide operating profit margin of 16%.

Factors incorporated into the Company’s plan are stable growth in the PR business, IP development in the influencer marketing business, continued growth in the AI & Big Data solutions business, consolidation contributions from M&A, and productivity improvement through AI utilization. As upside factors not sufficiently incorporated into the Company plan, first, the net sales growth rate and profit margin of the AI & Big Data solutions business may continue in a form close to the current 1Q level; second, PR operations support products such as SAKAE for Client may launch as recurring-fee revenues; third, the EPS uplift and capital efficiency improvement from the share buyback may be reflected in the market valuation; and fourth, liquidity may improve and the individual investor base may expand due to the stock split.

Downside factors are a slowdown in growth in the AI/data domain, dependence on specific creators and platforms in the influencer business, fluctuations in spot projects in the PR business, increases in personnel expenses, and integration costs for M&A subsidiaries. In particular, because the AI & Big Data solutions business has a high growth rate, it tends to influence investor expectations. Even if net sales grow, if personnel are needed for hands-on support and the profit margin declines, the stock price valuation uplift will become sluggish. In subsequent financial results, we would like to confirm net sales and operating profit margin in the AI & Big Data solutions business, the number of companies adopting products such as ShtockData and CERVN, continuity of Dataiku support, and revenue contribution from SAKAE-related products.

4. Long-term performance trend and profitability

Profit levels have risen one step through growth since 2021, and ROE and ROIC remain high.

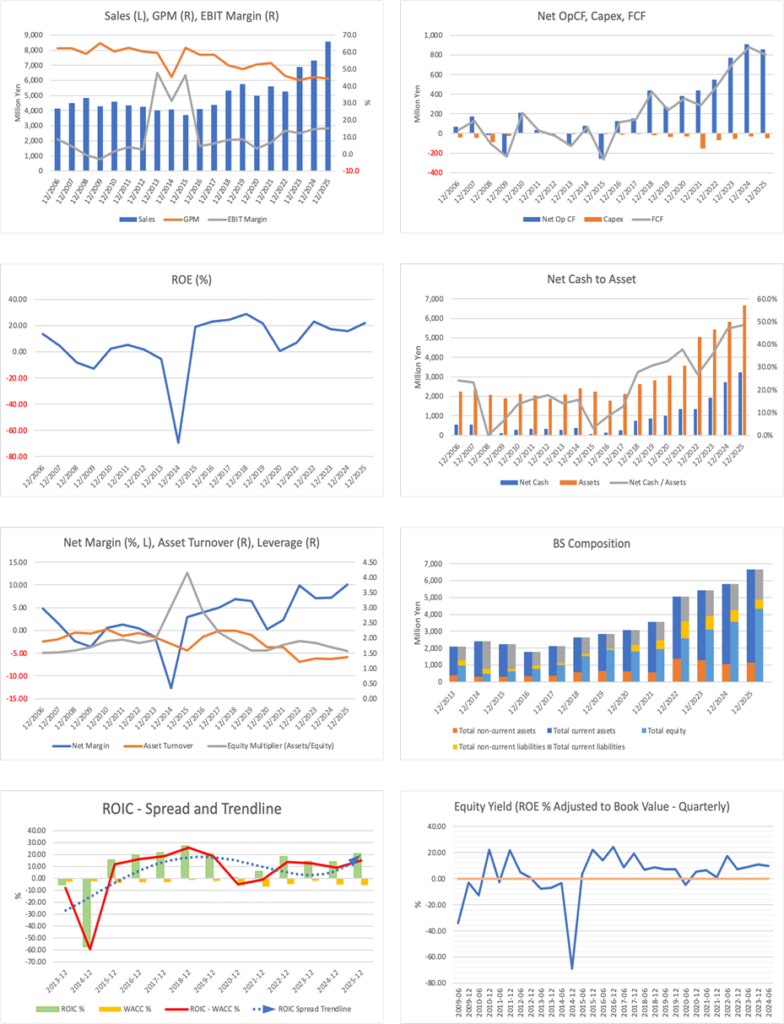

The Company’s long-term performance has improved significantly from the bottom in 2020. Net sales expanded from 4.990 billion yen in 2020 to 8.554 billion yen in 2025, and operating profit increased from 156 million yen to 1.302 billion yen. In 2020, profit levels fell sharply due to the COVID-19 pandemic. However, since 2021, the earnings structure has changed significantly due to a recovery in PR demand, consolidation of the influencer marketing business, the incorporation of the AI & Big Data solutions business, and improvements in operational efficiency.

Looking at performance since 2022, net sales expanded from 5.264 billion yen in 2022 to 6.895 billion yen in 2023, 7.323 billion yen in 2024, and 8.554 billion yen in 2025. Operating profit was 720 million yen in 2022, 840 million yen in 2023, 1.074 billion yen in 2024, and 1.302 billion yen in 2025. The operating profit margin also remained high at 13.7% in 2022, 12.2% in 2023, 14.7% in 2024, and 15.2% in 2025. The fact that the profit margin temporarily declined in 2023 and then improved in 2024 and 2025 shows that growth accompanied by profitability has continued, rather than mere net sales expansion.

ROE was 22.9% in 2022, 17.2% in 2023, 15.8% in 2024, and 21.9% in 2025. In 2025, net income attributable to owners of the parent increased to 863 million yen, bringing ROE back into the 20% range. ROIC has also recently risen into the 21% range, and economic value creation is continuing to exceed WACC significantly. The high ROIC is due to the Company’s asset-light business, the PR business’s profit margin, the high profitability of the AI/data domain, and the low burden of capital expenditures. Net cash has also accumulated, and the Company’s high capital efficiency while suppressing financial risk is an important pillar in the Company’s investment evaluation.

Cash flow is also favorable. In FY12/2025, net operating cash flow was 855 million yen and free cash flow was 804 million yen, indicating strong consistency between profits and cash-generating capacity. Capital expenditures remained at 51 million yen, and large-scale tangible fixed asset investment is not required for business expansion. This means a structure in which it is easy to secure funds that can be allocated to growth investment and shareholder returns.

On the other hand, whether the high capital efficiency will be maintained going forward depends on two conditions. First, net sales growth must exceed increases in personnel expenses, and the operating profit margin must rise from the 15% range to the 16% range. The PR business and the AI & Big Data solutions business have high profit margins, whereas the influencer business has a relatively low one. Because the companywide profit margin fluctuates with the business mix, it is necessary to assess each business’s growth rate and profit margin separately. Second is how accumulated cash will be allocated to growth investment, M&A, share buybacks, and dividends. Strong financial performance supports the stock price, but merely accumulating excessive cash is unlikely to lead to a further rise in PBR. The current share buyback can be positively evaluated as a response to this point.

5. Shareholder distribution and supply-demand characteristics

Stable shareholders are substantial in number, and tradable shares are limited. Improved liquidity and an expanded investor base are key to stock price valuation.

The substantial presence of stable shareholders characterizes the Company’s shareholder distribution. According to FactSet-based shareholder distribution, Shinto Tsushin Co., Ltd. holds 32.6%, Mitsuru Yabuki holds 12.5%, Tadayoshi Mase holds 4.3%, Tetsuya Tani holds 3.8%, and Masataka Ishiguri holds 2.0%. The employee shareholding association also holds 1.4%. Because many of the major shareholders have stable characteristics, this provides a certain support factor for downside resilience in the stock price. On the other hand, the floating share ratio remains around 36%, and daily trading volume is not large. As a small-cap stock, it has two aspects: its price can move easily when positive factors emerge, while sizable funds have difficulty entering.

Holdings by domestic and overseas institutional investors are limited. Although holdings by Sumitomo Mitsui DS Asset Management, Asset Management One, and others are visible, their holding ratios are small. Overseas institutional investors’ holdings also do not have a major presence at this stage. This is considered to reflect the fact that the Company’s market capitalization, liquidity, and IR recognition are limited. Conversely, if performance improves and capital policy progresses, the investment unit declines due to the stock split, and liquidity improves; domestic small-cap funds, individual investors, and growth-stock-oriented investors may find it easier to enter.

In considering the Company’s shareholder distribution, it should not be overlooked that, while stable shareholders are substantial, the small market capitalization limits institutional investors’ participation. Looking only at the Company’s fundamentals, it is an attractive small-cap growth stock with high profitability, net cash, high ROIC, and double-digit growth. However, for investors managing large-scale funds, insufficient liquidity makes it difficult to build a position. In particular, for a stock with a market capitalization of around 10.0 billion yen, even if the corporate value is evaluated highly, it is difficult to secure an investment ratio meaningful to the overall fund. In addition, the difficulty of unwinding a position without affecting the stock price at the time of sale constrains the investment target.

The structure in which stable shareholders are substantial suppresses short-term selling pressure, but a lack of liquidity can delay an uplift in the stock price. Given the capital efficiency of ROE 21.5% and ROIC in the 21% range, the PER of 10.0x and PBR of 2.07x do not sufficiently reflect the company’s growth profile. We view one reason the market has not fully evaluated the Company as lying not only in insufficient understanding of the business model, but also in constraints imposed by market capitalization and liquidity. The stock split is a direct response to this constraint. If the investment unit declines due to the 2-for-1 split and individual investor participation increases, daily trading volume may rise, and stock price formation may become smoother.

The share buyback also has significance from the perspective of shareholder distribution. The upper limit of 200,000 shares is approximately 2.3% of the 8.81 million shares outstanding, a scale that cannot be ignored in terms of supply and demand. Because the acquisition period is relatively long, from June to November 2026, the effects are expected to support the stock price and improve EPS. Of course, a share buyback alone does not increase corporate value, but for the Company, which has high ROE and net cash, allocating part of its surplus funds to shareholder returns helps improve capital efficiency.

The shareholder composition issue for a stock price valuation uplift going forward is to increase the number of trading participants in tradable shares while maintaining the stability of stable shareholders. For domestic and overseas institutional investors, market capitalization and liquidity tend to become constraints on investment decisions. Therefore, the focus will be on whether the Company can narrow the current small-cap stock discount by achieving the medium-term plan, expanding revenue in the AI/data domain, maintaining its capital policy, and enhancing IR information. We would like to evaluate the stock split and share buyback as the first step toward that.

6. Stock price trend and valuation

Stock price valuation remains cautious relative to performance expansion. A small-cap stock discount is also at play.

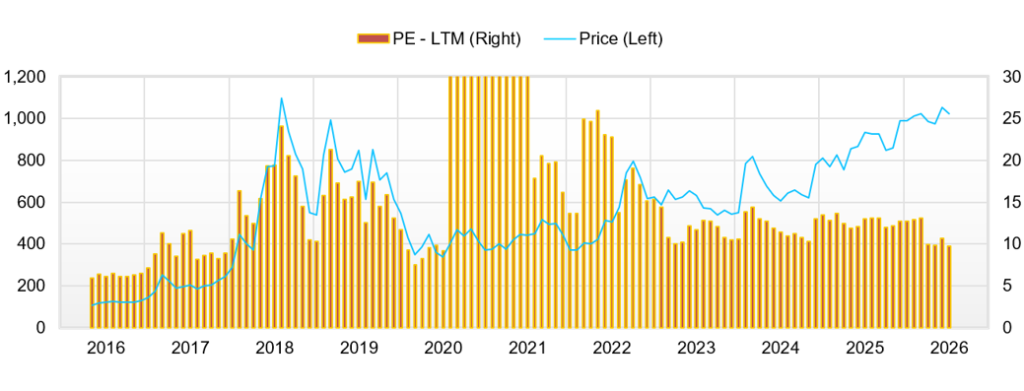

Although the Company’s stock has achieved significant performance improvement over the past five years, the stock price has not consistently moved in a straightforward relationship with performance. From 2020 to 2021, expectations for performance recovery from the COVID-19 pandemic, recovery in PR demand, and the incorporation of growth businesses supported the stock price. Since 2022, the consolidation effects of the influencer marketing business and the AI & Big Data solutions business, improvement in the operating profit margin, and the rise in ROE have been evaluated, and the stock price has risen in stages. However, PER remains around 10x because the market capitalization is small and liquidity is low, the PR industry has difficulty projecting a high-growth image, and quantitative disclosure of revenues in the AI/data domain is limited.

Recently, from the end of 2025 to the beginning of 2026, the stock price rose to the 1,000-yen range, and as of May 2026, it has been trading around 1,000 yen. The fact that performance updated record highs and 1Q got off to a strong start is a support factor for the stock price. On the other hand, the reason the stock price is being valued cautiously relative to performance growth is not only a lack of quantitative information regarding the quality of growth. A larger background factor is the constraint of market capitalization and liquidity. In terms of high ROE, high ROIC, net cash, and double-digit profit growth, the Company has conditions that could attract institutional investors. However, its market capitalization remains at around 10.0 billion yen, and daily trading value is limited. For this reason, for domestic and overseas institutional investors that manage large amounts of capital, the stock has become one for which, apart from the appeal of the company’s fundamentals, it is difficult to invest sufficient capital, and liquidity risk at the time of sale must also be considered.

Therefore, it is natural to consider that the current valuation of around PER 10x includes a small-cap stock discount accompanying the small market capitalization and low liquidity, rather than indicating that the Company’s profitability and growth potential are viewed as low. This is not so much a weakness specific to the Company as a market-structure constraint common to Japanese small-cap growth stocks. On the other hand, if market capitalization expands through performance growth and trading participants broaden through the stock split and share buyback, this discount could gradually narrow. The current stock split is intended to lower the investment unit and encourage participation by individual investors. At the same time, the share buyback is positioned as a measure that supports stock price formation through both capital efficiency and supply-and-demand dynamics.

We confirm the EPS growth expectations priced into the stock price. Assuming a forecast PER of 10.0x, actual PBR of 2.07x, forecast ROE of 21.5%, forecast EPS of 103.2 yen, and forecast dividend of 16 yen, the stock price is back-calculated at approximately 1,030 yen, and BPS at approximately 498 yen. The dividend payout ratio is 15.5%, and the internal retention rate is 84.5%. If ROE of 21.5% is maintained, the sustainable growth rate will be approximately 18.2%. However, the market is not pricing in this 18% long-term growth. The PER of 10.0x is appropriate for a mature services company, but it is a cautious valuation for a growth company with high ROE and ROIC. If the cost of capital is assumed to be 9%-10%, the EPS growth expectations priced into the current stock price are generally in the low- to mid-single digits.

Compared with past results, the CAGR for EPS, from 61.2 yen in 2022 to 99.0 yen in 2025, was approximately 17%. From EPS of 16.3 yen in 2021 to 2025, it was approximately 57%, because it includes the recovery from a low level. The CAGR from 2020 as the starting point is even higher, but since it includes the low profit level during the COVID-19 pandemic, it is too strong a standard for judging the growth rate going forward. In investment evaluation, it is natural to use the EPS CAGR of approximately 17% since 2022 as the comparison axis. The current stock price does not reflect this actual growth rate, and instead appears to assume that the future growth rate will settle in the single digits.

An analysis of stock price levels using three methods shows that the PBR method, DCF method, and ROIC method all indicate a certain upside potential relative to the current stock price. Under the PBR method, assuming a PBR of 1.8x to 2.6x relative to BPS of approximately 496 yen, taking into account the Company’s ROE, financial soundness, and growth potential, the stock price level is approximately 890 yen to 1,290 yen, and the median is approximately 1,140 yen. Under the DCF method, using conservative assumptions of normalized free cash flow of 500 million yen to 700 million yen, a growth rate of around 4%, a discount rate of 9% to 10%, and a perpetual growth rate of 1%, the stock price level is generally 1,100 yen to 1,500 yen, and the median is around 1,300 yen. Under the ROIC method, given that ROIC is in the 20% range and significantly exceeds WACC, a PBR of 2.2x to 2.8x can be justified, with a stock price of approximately 1,090 to 1,390 yen and a median of approximately 1,240 yen.

Averaging the medians of the three methods yields an indicative stock price of around 1,230 yen. Compared with the current stock price of around 1,030 yen, the stock is positioned for a valuation uplift if the business’s high profitability and capital policy are sufficiently reflected. However, this is not intended to encourage buying or selling at a specific price; rather, it is an analysis of the stock price level based on the Company’s earnings power, capital efficiency, and financial flexibility. For the stock price to be evaluated one step further, the AI & Big Data solutions business must continue to grow at a high rate, the PR business’s profit margin must be maintained, and the share buyback and stock split must have a meaningful impact on liquidity and EPS.

7. Growth strategy and risks

AI utilization and monetization of proprietary IP are upside factors. Human resources, disclosure, and liquidity are items to confirm

The Company’s growth strategy can be organized as deepening of the PR business, IP development in the influencer business, expansion of the AI & Big Data solutions business, productivity improvement through AI utilization, and improvement in capital policy. In the PR business, the Company has indicated a policy of advancing conventional public relations support with data and AI through the establishment of the AIC Center, X linkage for SAKAE, development of SAKAE for Client, an alliance with WaveNet, Inc., and AI talent development. If this progresses, the PR business will evolve into a high-value-added service that combines operational standardization, effectiveness measurement, SNS monitoring, and client-facing progress visualization, without remaining human-resource-dependent.

In the influencer marketing business, the focus is on multilayering revenue opportunities by utilizing proprietary IP. Merupuchi proprietary IP, auditions, α+, beauty communities, and Mel: See are not merely advertising projects but moves to hold fan touchpoints in-house and connect them to product development and community operations. If these are successful, in addition to net sales from each project, ongoing fan-based revenues and brand revenues will be generated. However, the influencer business is susceptible to changes in creator popularity, algorithm changes on SNS platforms, the risk of controversy, and advertisers’ stance on ad spending. Going forward, we would like to confirm not only net sales growth but also profit margins, IP-level revenues, community scale, and the profitability of product commercialization.

In the AI & Big Data solutions business, hands-on support for Dataiku, ShtockData, CERVN, and Tableau-related human resources is a growth pillar. Net sales growth of 40.0% and operating profit growth of 49.9% in 1Q were strong results, and this domain has the potential to change the Company’s stock price valuation. AI-related services attract high market interest, but competition is also intense. Amid competition from major IT, consulting, and SaaS companies, the question is which customer segments the Company can serve, at what prices, and how consistently it can provide services. If ShtockData and CERVN increase the number of adopting companies, annual net sales, and customer retention rates, and Dataiku hands-on support expands with high profitability, the AI/data domain can become a core area that changes the Company’s evaluation axis.

Capital policy has also become important as part of the growth strategy. The share buyback leads to improved EPS and ROE and strengthened shareholder returns. The stock split has the potential to reduce the investment unit size, increase liquidity, and expand the individual investor base. The change to the shareholder benefit program may serve to encourage long-term holding. For small-cap stocks whose market valuation does not rise sufficiently through business growth alone, these are important auxiliary lines.

The first risk is a slowdown in growth in the AI & Big Data solutions business. The current stock price valuation has not yet fully priced in high growth. However, if the Company is evaluated as an AI company going forward, expectations for the growth rate and profit margin in this domain will increase. At that time, if disclosure of the number of adopting companies and recurring fee revenues remains limited, the market will find it difficult to judge the certainty of growth. The second is securing human resources and personnel expenses. PR, AI hands-on support, and influencer operations all depend on the quality of human resources. If hiring difficulties or increases in personnel expenses persist, profit margins may be suppressed even if net sales grow. The third is liquidity. Although the stock split lowers the investment unit, whether trading volume actually increases will depend on the breadth of market participants.

Even so, the Company has multiple support factors: a highly profitable PR base, a growing AI/data business, financial strength, and strengthened shareholder returns. If profit contribution from the AI/data domain and execution of capital policy are confirmed while downside factors are mitigated, the Company’s stock may move away from the conventional evaluation as a small-cap PR company and closer to an evaluation as a highly profitable, high-ROIC communication technology company.

8. Conclusion based on performance and stock price valuation

With growth in the three pillars and capital policy overlapping, a stock price valuation uplift can be expected

KYODO PUBLIC RELATIONS is expanding the axes of its corporate value formation by growing influencer marketing and AI & Big Data solutions based on the stability and high profitability of the PR business. In the first quarter of FY12/2026, it got off to a strong start, reporting net sales of 2.346 billion yen, operating profit of 458 million yen, and quarterly net income attributable to owners of the parent of 268 million yen, and achieved growth in both sales and profits across all segments. The PR business continues to be the profit pillar, and the AI & Big Data solutions business is positioned to drive up the overall evaluation with high growth and a high profit margin.

In terms of the stock price, the forecast PER of 10.0x and actual PBR of 2.07x remain cautious valuations, given capital efficiency metrics such as ROE of 21.5% and ROIC in the 21% range. The EPS growth expectations the market has priced into the Company appear to remain in the low- to mid-single digits, and even compared with the EPS CAGR of approximately 17% from 2022 to 2025, it is difficult to say that excessive expectations are reflected in the stock price. When organizing stock price levels by three methods, the medians under the PBR, DCF, and ROIC methods also exceed the current stock price. We believe the current stock price, while pricing in the Company’s earnings power and financial strength to some extent, does not adequately reflect growth in the AI/data domain and the effects of capital policy.

On the other hand, behind the cautious valuation is a small-cap stock discount resulting from the small market capitalization and low liquidity. The Company’s fundamentals are attractive, with high profitability, high ROIC, net cash, and double-digit profit growth. However, for institutional investors managing large-scale funds, position building and liquidity at the time of sale are often constraints. Therefore, for the Company’s stock price to be raised, expansion of market capitalization through performance growth, an increase in trading volume after the stock split, improvement in capital efficiency through share buybacks, and expansion of the investor base through IR will be important. We would like to position the current capital policy as the first step toward easing this constraint.

The focus going forward is, first, continued growth in the AI & Big Data solutions business. If growth close to 40% in net sales and 50% in operating profit continues, the Company’s business image will change significantly. Second is maintaining the profit margin in the PR business. If the stability of retainer sales and the expansion of spot projects are achieved simultaneously, achieving the full-year plan for an operating profit margin of 16% will become more realistic. Third is the monetization of IP in the influencer business. We would like to confirm whether multilayering revenues through proprietary IP and fan communities leads to improved profit margins. Fourth is capital policy. Attention will be paid to the extent to which the share buyback, stock split, and change to the shareholder benefit program affect EPS, ROE, liquidity, and the expansion of the investor base.

In conclusion, the Company’s stock is in a phase of expected valuation uplift, supported by stable PR revenues, growth in the AI/data domain, and capital market measures, including a share buyback and a stock split. There is no need to lean toward excessive optimism, but it is difficult to say that the current PER level adequately reflects the Company’s high ROE and ROIC, as well as the progress in 1Q profits. If the profit contribution from the AI & Big Data solutions business expands, the PR business maintains its high profitability, and capital policy is consistently executed, the Company is highly likely to be re-rated as a highly profitable communications company beyond the conventional view of a small-cap PR company. In subsequent financial results, we would like to focus on net sales and operating profit margin in the AI/data domain; retainer and spot sales in the PR business; monetization of influencer IP; progress on the share buyback; and changes in trading volume following the stock split.

Key financial data

| Unit: million yen | 2021 | 2022 | 2023 | 2024 | 2025 | 2026 CE |

| Sales | 5,610 | 5,265 | 6,896 | 7,324 | 8,555 | 10,000 |

| EBIT (Operating Income) | 381 | 720 | 841 | 1,075 | 1,303 | 1,600 |

| Pretax Income | 288 | 768 | 862 | 1,034 | 1,305 | |

| Net Profit Attributable to Owner of Parent | 132 | 520 | 488 | 526 | 863 | 900 |

| Cash & Short-Term Investments | 1,943 | 2,318 | 2,691 | 3,260 | 3,578 | |

| Total assets | 3,572 | 5,044 | 5,428 | 5,810 | 6,656 | |

| Total Debt | 591 | 967 | 767 | 539 | 357 | |

| Net Debt | -1,352 | -1,351 | -1,925 | -2,721 | -3,221 | |

| Total liabilities | 1,630 | 2,267 | 2,097 | 1,921 | 1,957 | |

| Total Shareholders’ Equity | 1,942 | 2,595 | 3,090 | 3,553 | 4,336 | |

| Net Operating Cash Flow | 442 | 546 | 771 | 911 | 855 | |

| Capital Expenditure | 155 | 67 | 54 | 33 | 51 | |

| Net Investing Cash Flow | -26 | -397 | -35 | -37 | -109 | |

| Net Financing Cash Flow | 16 | 220 | -375 | -311 | -428 | |

| Free Cash Flow | 286 | 479 | 717 | 878 | 804 | |

| ROA (%) | 3.97 | 12.08 | 9.31 | 9.36 | 13.85 | |

| ROE (%) | 7.03 | 22.94 | 17.15 | 15.84 | 21.88 | |

| EPS (Yen) | 16.3 | 61.2 | 56.6 | 60.6 | 99.0 | 103.2 |

| BPS (Yen) | 236.1 | 299.5 | 356.7 | 408.2 | 496.4 | |

| Dividend per Share (Yen) | 7.00 | 8.00 | 10.00 | 12.00 | 14.00 | 16.00 |

| Shares Outstanding (Million shares) | 8.64 | 8.74 | 8.78 | 8.79 | 8.81 |

Source: Omega Investment from company data, rounded to the nearest whole number The number of shares outstanding is reported as the adjusted figure before the split.

Share price

Key stock price data

Financial data (quarterly basis)

| Unit: million yen | 2024/12 | 2025/12 | 2026/12 | ||||||

| 1Q | 2Q | 3Q | 4Q | 1Q | 2Q | 3Q | 4Q | 1Q | |

| (Income Statement) | |||||||||

| Sales | 1,788 | 1,779 | 1,716 | 2,041 | 2,037 | 1,922 | 2,052 | 2,544 | 2,347 |

| Year-on-year | 8.4% | 10.2% | 1.6% | 5.0% | 13.9% | 8.0% | 19.6% | 24.7% | 15.2% |

| Cost of Goods Sold (COGS) | 972 | 966 | 925 | 1,147 | 1,108 | 1,077 | 1,107 | 1,470 | 1,250 |

| Gross Income | 816 | 814 | 791 | 894 | 929 | 845 | 945 | 1,074 | 1,096 |

| Gross Income Margin | 45.6% | 45.7% | 46.1% | 43.8% | 45.6% | 44.0% | 46.1% | 42.2% | 46.7% |

| SG&A Expense | 519 | 545 | 530 | 646 | 560 | 581 | 620 | 730 | 638 |

| EBIT (Operating Income) | 297 | 269 | 261 | 248 | 369 | 264 | 325 | 345 | 459 |

| Year-on-year | 11.2% | 49.2% | 34.4% | 24.4% | 24.1% | -1.7% | 24.8% | 38.8% | 24.4% |

| Operating Income Margin | 16.6% | 15.1% | 15.2% | 12.2% | 18.1% | 13.7% | 15.9% | 13.6% | 19.5% |

| EBITDA | 349 | 319 | 312 | 298 | 414 | 311 | 375 | 395 | 507 |

| Pretax Income | 277 | 271 | 230 | 256 | 366 | 260 | 328 | 351 | 461 |

| Consolidated Net Income | 147 | 177 | 147 | 150 | 244 | 167 | 218 | 349 | 311 |

| Minority Interest | 31 | 28 | 26 | 10 | 28 | 27 | 34 | 25 | 42 |

| Net Income ATOP | 116 | 148 | 121 | 141 | 215 | 140 | 184 | 324 | 269 |

| Year-on-year | -19.5% | 49.1% | 13.6% | 2.5% | 85.1% | -5.6% | 51.9% | 130.4% | 24.8% |

| Net Income Margin | 6.5% | 8.3% | 7.0% | 6.9% | 10.6% | 7.3% | 9.0% | 12.7% | 11.4% |

| (Balance Sheet) | |||||||||

| Cash & Short-Term Investments | 2,657 | 2,980 | 2,946 | 3,260 | 3,115 | 3,422 | 3,305 | 3,578 | 3,732 |

| Total assets | 5,286 | 5,448 | 5,342 | 5,810 | 5,598 | 5,871 | 5,876 | 6,656 | 6,638 |

| Total Debt | 707 | 647 | 586 | 539 | 490 | 445 | 400 | 372 | 311 |

| Net Debt | -1,950 | -2,333 | -2,360 | -2,721 | -2,625 | -2,977 | -2,906 | -3,206 | -3,421 |

| Total liabilities | 1,885 | 1,855 | 1,615 | 1,921 | 1,704 | 1,782 | 1,558 | 1,957 | 1,753 |

| Total Shareholders’ Equity | 3,129 | 3,293 | 3,401 | 3,553 | 3,617 | 3,786 | 3,979 | 4,336 | 4,481 |

| (Profitability %) | |||||||||

| ROA | 9.12 | 9.79 | 10.20 | 9.36 | 11.49 | 10.90 | 12.12 | 13.85 | 14.98 |

| ROE | 15.92 | 16.72 | 16.57 | 15.84 | 18.54 | 17.43 | 18.42 | 21.88 | 22.64 |

| (Per-share) Unit: JPY | |||||||||

| EPS | 13.4 | 17.1 | 13.9 | 16.2 | 24.7 | 16.0 | 21.0 | 37.1 | 30.7 |

| BPS | 361.1 | 379.0 | 391.4 | 408.2 | 415.5 | 433.6 | 455.8 | 496.4 | 512.9 |

| Dividend per Share | 0.00 | 0.00 | 0.00 | 12.00 | 0.00 | 0.00 | 0.00 | 14.00 | 0.00 |

| Shares Outstanding (million shares) | 8.79 | 8.79 | 8.79 | 8.79 | 8.81 | 8.81 | 8.81 | 8.81 | 8.81 |

Source: Omega Investment from company data, rounded to the nearest whole number The number of shares outstanding is reported as the adjusted figure before the split.

Financial data (full-year basis)

| Unit: million yen | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 |

| (Income Statement) | ||||||||||

| Sales | 4,100 | 4,379 | 5,318 | 5,758 | 4,990 | 5,610 | 5,265 | 6,896 | 7,324 | 8,555 |

| Year-on-year | 10.7% | 6.8% | 21.4% | 8.3% | -13.3% | 12.4% | -6.1% | 31.0% | 6.2% | 16.8% |

| Cost of Goods Sold | 1,703 | 1,822 | 2,546 | 2,879 | 2,367 | 2,614 | 2,843 | 3,894 | 4,010 | 4,762 |

| Gross Income | 2,396 | 2,558 | 2,772 | 2,879 | 2,623 | 2,996 | 2,422 | 3,002 | 3,314 | 3,793 |

| Gross Income Margin | 58.5% | 58.4% | 52.1% | 50.0% | 52.6% | 53.4% | 46.0% | 43.5% | 45.3% | 44.3% |

| SG&A Expense | 2,216 | 2,293 | 2,324 | 2,374 | 2,456 | 2,597 | 1,685 | 2,147 | 2,225 | 2,490 |

| EBIT (Operating Income) | 180 | 265 | 444 | 502 | 157 | 381 | 720 | 841 | 1,075 | 1,303 |

| Year-on-year | -89.5% | 46.7% | 68.0% | 12.9% | -68.8% | 143.8% | 88.7% | 16.8% | 27.8% | 21.2% |

| Operating Income Margin | 4.4% | 6.0% | 8.4% | 8.7% | 3.1% | 6.8% | 13.7% | 12.2% | 14.7% | 15.2% |

| EBITDA | 195 | 284 | 468 | 534 | 202 | 447 | 857 | 1,059 | 1,279 | 1,495 |

| Pretax Income | 181 | 257 | 432 | 502 | 70 | 288 | 768 | 862 | 1,034 | 1,305 |

| Consolidated Net Income | 163 | 221 | 366 | 372 | 13 | 132 | 539 | 546 | 621 | 977 |

| Minority Interest | 0 | 0 | 0 | 0 | 0 | 0 | 18 | 58 | 95 | 114 |

| Net Income ATOP | 163 | 221 | 366 | 372 | 13 | 132 | 520 | 488 | 526 | 863 |

| Year-on-year | 51.2% | 35.3% | 65.8% | 1.5% | -96.6% | 943.0% | 294.4% | -6.3% | 7.9% | 64.1% |

| Net Income Margin | 4.0% | 5.0% | 6.9% | 6.5% | 0.3% | 2.4% | 9.9% | 7.1% | 7.2% | 10.1% |

| (Balance Sheet) | ||||||||||

| Cash & Short-Term Investments | 611 | 659 | 1,012 | 1,032 | 1,531 | 1,943 | 2,318 | 2,691 | 3,260 | 3,578 |

| Total assets | 1,784 | 2,113 | 2,637 | 2,831 | 3,068 | 3,572 | 5,044 | 5,428 | 5,810 | 6,656 |

| Total Debt | 462 | 390 | 280 | 163 | 531 | 591 | 967 | 767 | 539 | 357 |

| Net Debt | -149 | -269 | -732 | -869 | -1,000 | -1,352 | -1,351 | -1,925 | -2,721 | -3,221 |

| Total liabilities | 1,003 | 1,105 | 1,109 | 930 | 1,254 | 1,630 | 2,267 | 2,097 | 1,921 | 1,957 |

| Total Shareholders’ Equity | 782 | 1,008 | 1,528 | 1,901 | 1,814 | 1,942 | 2,595 | 3,090 | 3,553 | 4,336 |

| (Cash Flow) | ||||||||||

| Net Operating Cash Flow | 125 | 152 | 437 | 274 | 384 | 442 | 546 | 771 | 911 | 855 |

| Capital Expenditure | 13 | 9 | 15 | 36 | 30 | 155 | 67 | 54 | 33 | 51 |

| Net Investing Cash Flow | -16 | -15 | -131 | -123 | -102 | -26 | -397 | -35 | -37 | -109 |

| Net Financing Cash Flow | 31 | -89 | 47 | -132 | 242 | 16 | 220 | -375 | -311 | -428 |

| Free Cash Flow | 112 | 144 | 422 | 238 | 355 | 286 | 479 | 717 | 878 | 804 |

| (Profitability ) | ||||||||||

| ROA (%) | 8.11 | 11.34 | 15.43 | 13.60 | 0.43 | 3.97 | 12.08 | 9.31 | 9.36 | 13.85 |

| ROE (%) | 23.24 | 24.69 | 28.89 | 21.69 | 0.68 | 7.03 | 22.94 | 17.15 | 15.84 | 21.88 |

| Net Margin (%) | 3.99 | 5.05 | 6.89 | 6.46 | 0.25 | 2.35 | 9.89 | 7.07 | 7.18 | 10.09 |

| Asset Turn | 2.03 | 2.25 | 2.24 | 2.11 | 1.69 | 1.69 | 1.22 | 1.32 | 1.30 | 1.37 |

| Assets/Equity | 2.87 | 2.18 | 1.87 | 1.59 | 1.59 | 1.77 | 1.90 | 1.84 | 1.69 | 1.58 |

| (Per-share) Unit: JPY | ||||||||||

| EPS | 22.2 | 30.0 | 46.6 | 46.6 | 1.6 | 16.3 | 61.2 | 56.6 | 60.6 | 99.0 |

| BPS | 106.0 | 136.7 | 191.9 | 237.9 | 229.8 | 236.1 | 299.5 | 356.7 | 408.2 | 496.4 |

| Dividend per Share | 0.00 | 0.00 | 2.50 | 5.00 | 6.00 | 7.00 | 8.00 | 10.00 | 12.00 | 14.00 |

| Shares Outstanding (million shares) | 7.56 | 7.56 | 8.15 | 8.17 | 8.18 | 8.64 | 8.74 | 8.78 | 8.79 | 8.81 |

Source: Omega Investment from company data, rounded to the nearest whole number The number of shares outstanding is reported as the adjusted figure before the split.