2026-07-27

Home

Japanese

Omega Investment Co., Ltd.

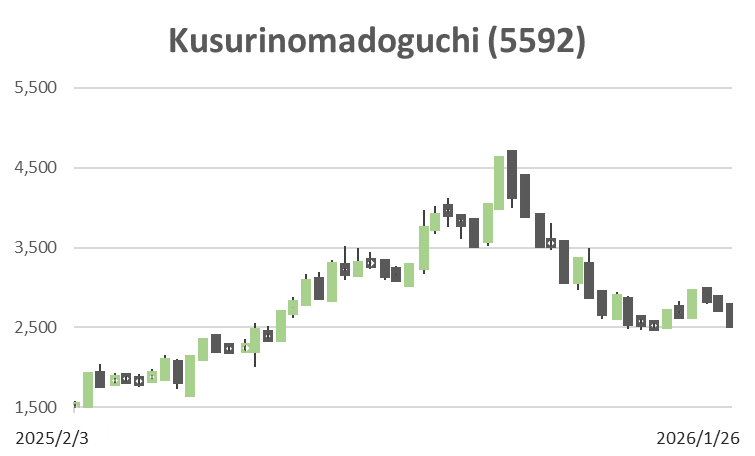

Kusurinomadoguchi (Price Discovery)

Buy

Conclusion

Buy. Against the tailwind of medical DX (electronic prescriptions and online prescription acceptance), stock revenue is accumulating, and profit-generating capacity is strong, supported by cost optimisation. The deterioration in cash flow in the previous fiscal year was driven mainly by temporary working capital factors. A DCF using approximately 2.3 billion yen of normalised FCF as the starting point suggests an appropriate share price of roughly 3,880 yen; the share price is judged to remain undervalued.

Profile

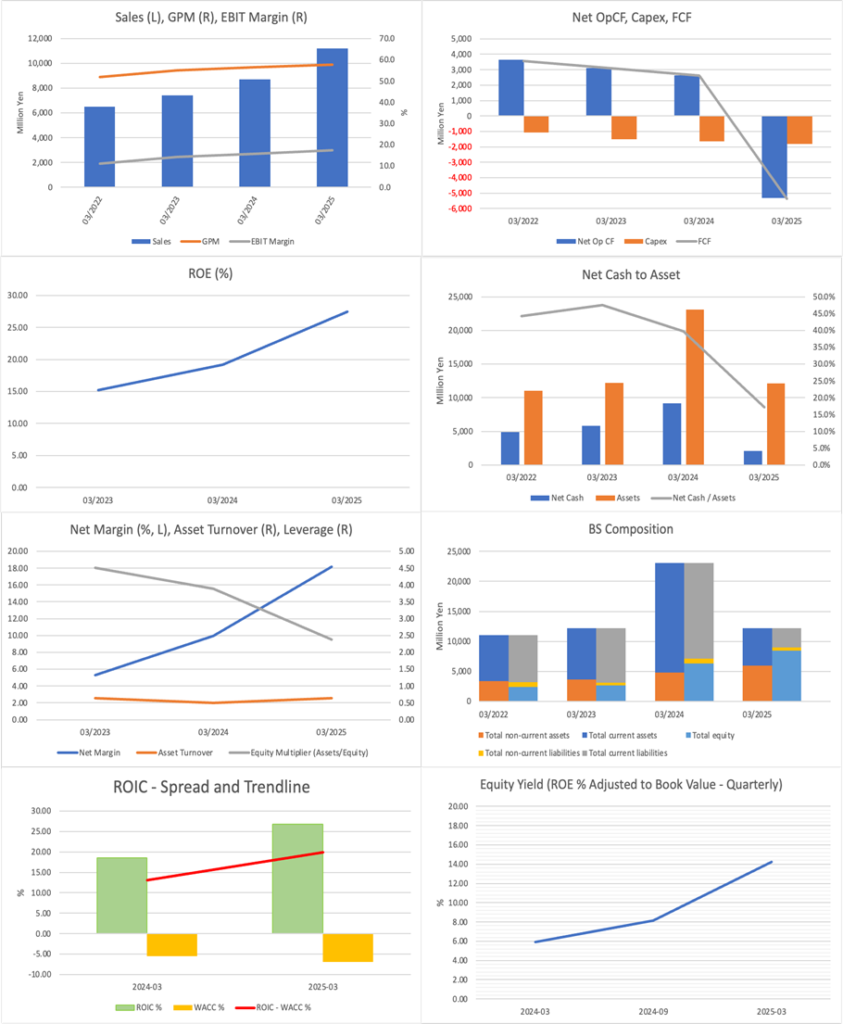

Kusuri no Madoguchi (5592) is a service company that supports DX in the medical domain centred on pharmacies; with the pharmacy search and reservation app “EPARK Kusuri no Madoguchi” and the electronic medication notebook app “EPARK Okusuri Techo” as its core, it promotes the digitalisation of patient touchpoints such as prescription acceptance before visiting a pharmacy and the management of medication information, and, for pharmacies, it develops a core system that undertakes operational efficiency and purchasing support (Minna no Okusuri-bako) through joint purchasing and other means. It has a revenue structure that combines “shot revenue”, obtained as initial fee revenue upon the introduction of various services, and “stock revenue”, obtained continuously as fixed amounts such as monthly usage fees and amounts that fluctuate in accordance with usage fees such as sales from prescription medicine pickup reservations and payments for joint purchasing services; it aims for medium-term growth through the expansion of the number of installed stores and the accumulation of stock. Revenue ratio by business %: Media 39, Minna no Okusuri-bako 28, Core system 32, Others 1 <FY3/2025>

| Securities Code |

| TYO:5592 |

| Market Capitalization |

| 28,844 million yen |

| Industry |

| Information / Communication |

Stock Hunter’s View

Kusuri no Madoguchi: Medium-term growth expected through pharmacy DX. At present, the accumulation of stock is progressing smoothly.

Kusuri no Madoguchi develops the pharmacy search website/app “EPARK Kusuri no Madoguchi” and the electronic medication notebook app “EPARK Okusuri Techo”. The medication notebook has gained traction for its convenience in pickup reservations and bulk data management and recently surpassed 7 million cumulative downloads. In the results for the second quarter (April–September) of FY3/2026, announced last November, operating profit was 1,262 million yen (up 32.9% YoY), renewing the record high for the same period. Cost optimisation across the entire group, including Kusuri no Madoguchi, was driven by the rationalisation of subsidiaries.

Revenue consists of “shot revenue”, obtained as initial fee revenue at the time of introducing various services, and “stock revenue”, obtained continuously as fixed amounts, such as monthly usage fees,s and as amounts that fluctuate depending on usage fees, such as sales from prescription medicine pickup reservations and payments for joint purchasing services. Shot revenue has been declining recently because the previous fiscal year involved revisions to medical and dispensing remuneration, and the special demand for services eligible for remuneration add-ons and subsidies has run its course. Meanwhile, stock revenue has been trending favourably, driven by increased acceptance of online prescriptions and a higher number of facilities held.

Electronic prescriptions are a core measure of medical DX promoted by the government, and the Ministry of Health, Labour and Welfare aims to introduce them to all medical institutions by no later than 2030. This is a tailwind for the company, which is steadily increasing the number of stores adopting the online prescription acceptance service, and continued growth is expected.

Investor’s View

Buy. A DCF using approximately 2.3 billion yen of normalised FCF as the starting point derives an appropriate share price of roughly 3,880 yen, and, considering the high level of capital efficiency and the degree of certainty of cash flow creation over the next 4–5 years, the share price appears to remain undervalued.

Whether “EPARK Kusuri no Madoguchi” and the electronic medication notebook app “EPARK Okusuri Techo”, which have now achieved a certain degree of penetration, can continue over the long term as an unchanging competitive advantage is, frankly, still difficult to be confident about. However, if one views the investment horizon realistically, it is unlikely that the company’s model will materially slow cash flow generation over the next 4–5 years. The balance sheet is tight, profitability is high relative to sales and invested capital, and from a capital-efficiency perspective, the company’s business is attractive.

In the previous fiscal year, cash flow swung significantly negative due to a temporary adjustment in working capital. Still, under normal conditions, it can generate an operating cash flow of around 2.0 billion yen per year. It would be reasonable to view this as the business’s underlying capability. The fact that Hikari Tsushin, which places cash flow creation at the core of its investment judgment, is, in effect, the most significant shareholder, holding close to 40% of the shares, also suggests that management stability is likely to be maintained. Treating approximately 2.3 billion yen, which excludes the distortion in FY3/2025, as the starting point for normalised annual FCF, and assuming WACC of 8.5%, a perpetual growth rate of 2.0%, and decelerating growth rates in FY2028–FY2030 (+10%, +8%, +6%), a DCF trial calculation yields an appropriate share price of approximately 3,880 yen.

On the other hand, while EPS has expanded at a CAGR of 57% from FY2022 (46.96 yen) to the FY2025 forecast (180.63 yen), the implied potential growth rate embedded in the current indicators (forecast PER 12.3, actual PBR 3.04, forecast ROE 25.2%, forecast dividend 30 yen) is estimated to be approximately a little over 20%. In other words, although the market is not assuming the rapid growth of the past few years will continue as is, it is still pricing the share price on expectations of a relatively high level of continued growth. This point should not be overlooked: when negative factors emerge in performance, the share price reaction may also be significant; however, if one judges them to be temporary after scrutinising the content, such phases will constitute opportunities to build a position actively.

In addition, the main factors behind the sharp contraction in assets and current liabilities in FY3/2025 were: (1) short-term borrowings became net repayment, as repayments of approximately 10.1 billion yen exceeded borrowings of approximately 5.0 billion yen, resulting in a net decrease of approximately 5.1 billion yen and a reduction in the period-end balance; and (2) in the Minna no Okusuri-bako business (purchasing support service), in line with a change in the business alliance partner for receivables collection agency, the combination of collection and payment terms was reorganised, accounts payable decreased by approximately 7.6 billion yen, and the conventional retention funds (working capital buffer) were eliminated (as the relevant change in alliance partner, the start of a business alliance with E-BOND Holdings [subsidiary Weeds] in November 2024 is disclosed). These also directly affected operating cash flow: the decrease in accounts payable (approximately 7.69 billion yen) was a major driver of cash outflow, and FCF deteriorated YoY. The company indicates that, excluding this decrease, operating cash flow was substantially positive (approximately 2.3 billion yen).

Financials and Valuations

Price

PBR (LTM)

PER (LTM)

ROE (LTM)

EPS (Actual)

BPS (LTM)