2026-05-11

Home

Japanese

Omega Investment Co., Ltd.

Chugai Ro (Price Discovery)

Buy

Conclusion

Buy: As a thermal technology company making steady progress in capital efficiency, Chugai Ro’s valuation at around 1x PBR remains conservative.

Chugai Ro may appear to be an understated equipment company centred on industrial furnaces and heat-treatment equipment. In substance, however, it is an applied thermal technology company serving steel, non-ferrous metals, batteries, semiconductor-related applications, environmental fields, and decarbonisation. In FY3/2026, the Company delivered steady results, with sales of 37,332 million yen and operating profit of 2,879 million yen. For FY3/2027, management forecasts operating profit of 3,620 million yen. ROE has improved markedly, while shareholder returns have also become clearly more active, with targets of a dividend payout ratio of at least 60% based on NOPAT and a total shareholder return ratio of at least 50%—the shares trade at a forecast PER of 12.6x and an actual PBR of 1.05x. Based on the Company’s forecast EPS of 361.3 yen, the market-implied EPS growth rate appears to be roughly 3-5%. This appears insufficient to reflect operating profit growth over the past several years, improvement in capital efficiency, and the widening ROIC-WACC spread. It is reasonable to treat one-off profits from the sale of cross-shareholdings, sluggish order intake, and losses in the development business as discount factors. However, these factors do not point to a deterioration in fundamentals. Rather, the main reason the PBR remains around 1x appears to be limited market recognition and the market’s desire to confirm earnings sustainability. The median fair share price based on the three valuation methods is approximately 5,600-5,800 yen, with a range of 4,300-6,800 yen. Compared with the current share price of approximately 4,550 yen, there remains room for revaluation.

Profile

A leading industrial furnace manufacturer that applies thermal technology across steel, non-ferrous metals, batteries, environmental fields, and decarbonisation.

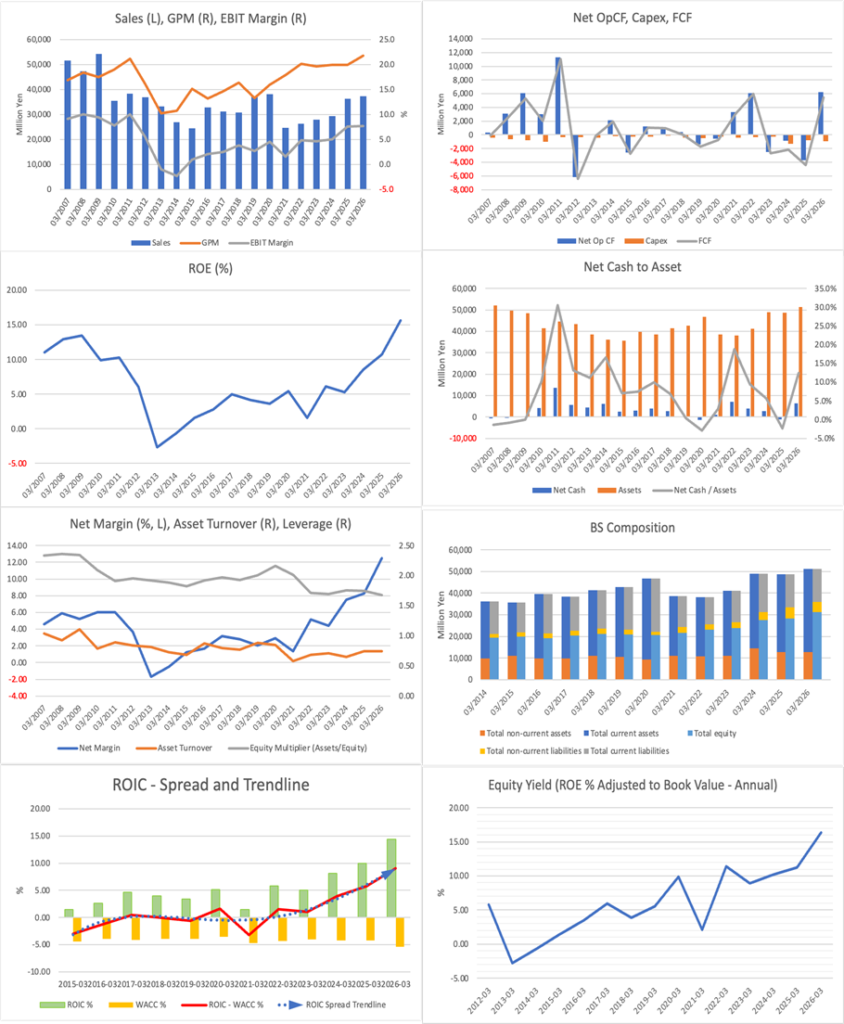

Established in 1945 and headquartered in Osaka, Chugai Ro is a manufacturer of industrial furnaces and heat treatment equipment. With thermal technology as its core, the Company supplies equipment to a wide range of industries, including metal materials, automotive parts, electronic components, battery materials, steel and non-ferrous metals, environmental equipment, and decarbonisation-related equipment. Its main businesses are heat treatment, plant, and development, while subsidiaries and other operations are included under other. In FY3/2026, consolidated sales were 37,332 million yen, operating profit was 2,879 million yen, and the equity ratio was 60.8%, indicating a sound financial position. Under its medium-term management plan, the Company has positioned the creation of new markets centred on carbon neutrality, sales expansion and profit improvement through the brush-up of existing products, and productivity enhancement as key strategies.

Sales composition by business % (operating margin %): Heat treatment 48 (8), Plant 36 (12), Development 5 (-12), Other 10 (0) [Overseas] 23 (3/2026)

| Securities Code |

| TYO:1964 |

| Market Capitalization |

| 34,047 million yen |

| Industry |

| Construction industry |

Stock Hunter’s View

Thermal technology is indispensable to a wide range of industries. Demand is also increasing in decarbonisation.

Chugai Ro is a leading industrial furnace manufacturer. Its core businesses are the Heat Treatment Business, Plant Business, and Development Business, which apply thermal technology indispensable to manufacturing. The Company has strengths in heating furnaces for steelmakers, heat-treatment equipment for various applications in the metal materials industry, and heat-treatment furnaces for automotive steel sheets and various machine parts. It also develops coating, film-forming, and firing equipment indispensable to the semiconductor market.

The previous FY3/2026 results announced on April 28 showed a 3.0% increase in sales and a 5.3% increase in operating profit. The shift in management policy towards emphasising operating profit, including the pass-through of higher input costs, a focus on highly profitable projects, and improved cost management, progressed steadily, and results were broadly in line with forecasts.

In the previous fiscal year, the Company received orders for continuous annealing line construction for domestic steelmakers, heating furnaces for non-ferrous metals, electric furnace dust-recycling equipment for steelmakers, ladle preheating equipment for electric furnaces, next-generation battery-related heat-treatment equipment, and firing furnaces for housing equipment components. In the current fiscal year, orders are expected for functional material heat treatment equipment, solar ionisation-related equipment, and combustion systems for steelmakers.

At present, the business environment is favourable, with Nippon Steel announcing a 300.0 billion yen investment in U.S. Steel and JFE Steel’s plan to double steel production in India also becoming clear. In addition, amid underlying medium- to long-term concerns over crude oil supply against the backdrop of the situation in Iran, attention to the Company’s energy-saving and decarbonisation technologies for industrial furnaces may increase further over the medium to long term.

Investor’s View

Buy: The share price is being restrained by concern over the stripping out of one-off profit, but the underlying improvement in capital efficiency is being underestimated.

The most important point in evaluating Chugai Ro’s shares is that the Company is moving beyond the profile of a cyclical industrial furnace manufacturer and becoming a company that clearly recognises the importance of capital efficiency and shareholder returns. In FY3/2026, sales were 37,332 million yen, operating profit was 2,879 million yen, and the operating margin was 7.7%. Operating profit expanded significantly from 1.26 billion yen in FY2021 to 2.87 billion yen in FY2025, and is expected to increase further to 3.62 billion yen in the FY2026 forecast. What deserves attention is not only the effect of higher sales but also the maintenance and improvement of the gross profit margin through price pass-through, a focus on highly profitable projects, and better cost management.

This improvement in earnings is also clearly reflected in capital efficiency. ROE rose from 6.1% in FY2021, 5.2% in FY2022, 8.5% in FY2023, and 10.7% in FY2024 to 15.7% in FY2025. FY2025 ROE includes the impact of gains on the sale of cross-shareholdings. Even so, given that the Company has achieved the ROE target of 10% set in its medium-term management plan, reduced cross-shareholdings, and maintained a sound financial base with an equity ratio of 60.8%, the improvement in capital efficiency cannot be dismissed as merely one-off. The ROIC-WACC spread has also widened markedly. From an investor’s perspective, it is highly significant that the expansion of operating profit is not simply a function of sales growth, but is accompanied by improved profit generation relative to capital employed.

At the same time, the reasons for the lacklustre year-to-date share price performance are clear. First, EPS of 643.70 yen in FY3/2026 was lifted by gains on the sale of investment securities of 3,315 million yen. This was part of the improvement in capital efficiency through the reduction of cross-shareholdings and should not be regarded as low-quality profit. However, it is not recurring profit. The Company’s forecast normalises EPS to 361.31 yen in FY3/2027, which makes earnings appear to decline sharply on the surface. Second, order intake in FY3/2026 was 37,100 million yen, equivalent to 94.0% of the previous fiscal year, while the FY2026 forecast of 38,700 million yen remains below the initial medium-term plan target of 42,000 million yen. Third, although the development business is responsible for growth themes related to decarbonisation, precision coating, and recycling, it recorded an operating loss of 247 million yen in FY3/2026. Monetisation of new market creation will therefore still require time.

The growth expectations currently priced in by the market are conservative. Based on a forecast PER of 12.6x, EPS of 361.3 yen, and a dividend of 180 yen, the implied share price is approximately 4,550 yen. The payout ratio is approximately 49.8%. Assuming a cost of capital of around 7-9%, the EPS growth rate implied by the share price is only around 3-5%. In contrast, operating profit expanded at an annual rate of more than 20% from FY2021 to FY2025, and the Company’s forecast for FY2026 also calls for further profit growth. The market appears to be placing greater weight on the expected decline following gains from the sale of cross-shareholdings, sluggish order intake, Middle East-related risk, and the delay in monetising new markets than on the Company’s past profit growth.

Shareholder returns are an important factor supporting the Company’s valuation. Since FY2024, the Company has targeted a dividend payout ratio of at least 60% of NOPAT (after-tax operating profit). It has also set a policy to aim for a total shareholder return of at least 50%, including share buybacks. The dividend for FY3/2026 was 166 yen; the forecast dividend for FY3/2027 is 180 yen; and in April 2026, the Company also resolved to repurchase treasury shares up to a maximum of 300,000 shares or 1,140 million yen. For an equipment-related company, its stance on shareholder returns is clearly active, and this should strengthen downside support around 1x PBR.

The medium-term management plan should be evaluated by separating the positives from the risks. The positives are that the Company is maintaining its final-year operating profit target of 3.62 billion yen while simultaneously pursuing ROE improvement, reducing cross-shareholdings, and delivering stronger shareholder returns. In decarbonisation-related areas, the Company has a technology base in fields with strong social demand, including hydrogen combustion, ammonia combustion, electric heating technology, electric furnace dust recycling, and next-generation battery heat-treatment equipment. Sales accumulated through the brush-up of existing products have also reached 11.0 billion yen, indicating that the shift towards management focused on operating profit is progressing. The risk is that sales related to new market creation were only 870 million yen in FY2025, leaving a large gap to the FY2026 target of 4.0 billion yen. The decarbonisation-related technology themes are attractive, but for the equity market to assign a higher valuation, it will need to confirm a transition from the research and development stage to earnings contribution.

The fair share price based on the three valuation methods indicates upside potential relative to the current share price. Under the PBR method, using an actual BPS of approximately 4,330 yen and a PBR of 1.0-1.35x, the range is approximately 4,300-5,850 yen, with a median of approximately 5,100 yen. Under the DCF method, assuming the company’s forecast operating profit of 3.62 billion yen for FY2026, WACC of 6.5%, a medium-term growth rate of 2-3%, a terminal growth rate of 1%, and taking net cash into account, the range is approximately 5,100-6,800 yen, with a median of approximately 5,900 yen. Under the ROIC method, based on forecast NOPAT, invested capital of approximately 25.0 billion yen, WACC of 6.5%, and the improvement in the ROIC-WACC spread, the range is approximately 5,200-6,500 yen, with a median of approximately 5,850 yen. Averaging the medians of the three methods gives a central fair share price of approximately 5,600-5,800 yen. The current share price of approximately 4,550 yen is close to the lower end of the PBR-based range, while the DCF and ROIC methods suggest upside potential of around 20-30%.

Shareholder distribution has both merits and drawbacks. According to FactSet data, the total holding ratio is 54.93%, and the free float ratio is 63.14%. Domestic financial institutions and asset managers, including Sumitomo Mitsui DS Asset Management, Resona Holdings, and Dai-ichi Life Group, hold a certain level of shares. At the same time, treasury shares also account for the 7% range. The presence of stable shareholders helps limit downside risk in the share price and makes the stock more appealing to domestic institutional investors that value high dividends and share buybacks.

On the other hand, participation by overseas investors and growth-oriented investors still appears limited. As a result, it may take time for decarbonisation, ROIC improvement, and changes in capital policy to be reflected in the share price. One reason the PBR remains around 1x lies not in weak fundamentals but in insufficient liquidity, recognition, and breadth of the investor base.

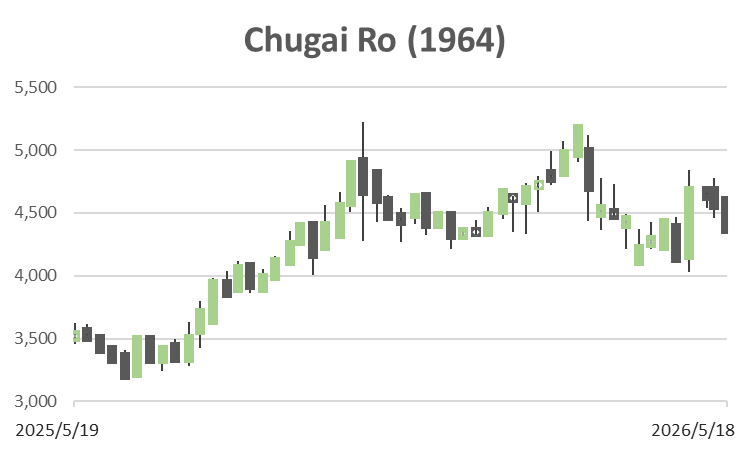

Looking back at the share price trend over the past five years or so, the Company has long traded at a low valuation below 1x PBR. PBR was 0.55x in FY2019, 0.75x in FY2020, 0.53x in FY2021, and 0.59x in FY2022, before improving to 0.84x in FY2023 and 0.96x in both FY2024 and FY2025. The share price has been revalued in response to the medium-term management plan, the expansion of operating profit, ROE improvement, and stronger shareholder returns. After temporarily exceeding 1x PBR from September 2025 onward, however, it remained at 0.96x at the end of FY2025, partly due to the impact of the situation in the Middle East. Rather than indicating a share price that is simply lacklustre despite strong earnings, this suggests that the revaluation process has stalled midway.

In conclusion, the current PBR of around 1x does not indicate a serious problem with the Company’s business fundamentals. Rather, the expected decline following the EPS uplift from gains on the sale of cross-shareholdings, temporary weakness in orders, and the market’s wait for monetisation of decarbonisation-related businesses is restraining investor evaluation. However, growth in operating profit, improvement in ROE, expansion of the ROIC-WACC spread, and an increasingly active stance on shareholder returns are clear. The Company appears to be overlooked as an understated equipment-related company. If the quality of earnings and sustainability of orders are confirmed, a revaluation to around 1.2-1.3x PBR is entirely possible. The investment judgment is Buy.

Financials and Valuations

Price

PBR (LTM)

PER (LTM)

ROE (LTM)

EPS (Actual)